|

onlinetaxupdate team wish to express sincere thanks to all the readers, authors, subscribers for the support extended to us. Please share your feedback at

|

taxupdate.otu@gmail.com or 7738647904

|

Newsletter 141 dated 29.10.2024

|

|

|

|

|

|

|

|

|

Dear Reader,

|

Please find newsletter for your reading and reference.

|

|

Index of the Newsletter

- Recent updates

- Portal updates

- Article

- Lawgics by Ms.Nidhi Aggarwal

- GST Notes by CMA Anil Sharma

- GST Daily by CA Pradeep Modi

- PPT/Handbook

- GST/IT/Customs in media

|

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Circular no. 255/01/2026-GST dated 25.06.2026 to provide Clarification regarding jurisdiction in cases involving migration/ transfer of taxable persons from one jurisdiction to another jurisdiction.

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Notification no. 01/2026-Central Tax (Rate) dated 30.04.2026 that Seeks to amend Notification No 9/2025 - Central tax (Rate) to align them with changes made vide Finance Act, 2026

|

|

|

|

|

|

CBIC issued Notification No. 58/2026-Customs (N.T.) dated 22.06.2026 to hereby appoint the officer to exercise the powers and discharge the duties conferred on the officers for the purpose of adjudication of the show cause notices.

|

|

|

|

|

|

|

|

CBIC issued Notification No. 57/2026-Customs (N.T.) dated 18.06.2026 to further amend Notification No. 27/2018-Customs (N.T.) dated 28.03.2018.

|

|

|

|

|

|

|

|

CBIC issued Notification No. 56/2026-Customs (N.T.) dated 16.06.2026 to make further amendment in Notification no. 21/2022-Customs (N.T.) dated 31.03.2022.

|

|

|

|

|

|

|

|

CBIC issued Notification No. 55/2026-Customs (N.T.) dated 11.06.2026 regarding Fixation of Tariff Value of Edible Oils, Brass Scrap, Areca Nut, Gold and Silver

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Corrigendum on 12.06.2026 to Notification no. 45/2025 -Customs dated 24.10.2025 -

|

G.S.R…(E).- In the notification of the Government of India, Ministry of Finance (Department of Revenue) No. 45/2025-Customs, dated the 24th October, 2025, published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i), vide number G.S.R. 781(E), dated the 24th October, 2025, at page 291, in lines 12 and 14, for ‘1993’ read ‘1983’.

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Instruction no. 11/2026-Customs dated 23.06.2026 regarding Establishment of Green Channel for Customs Clearance of Pollution Response Equipment and Materials during Oil and Hazardous and Noxious Substances (HNS) Spill Emergencies

|

|

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Instruction no. 10/2026-Customs dated 18.06.2026 regarding Completion of Data Entry in DIGIT.

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Notification no. 12/2026-Customs (ADD) dated 19.06.2026 Seeking to continue anti-dumping duty on imports of Polyethylene Terephthalate resin having an intrinsic viscosity of 0.72 decilitres per gram or higher originating in or exported from China for a period of 5 years

|

|

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Notification no. 11/2026-Customs (ADD) dated 19.06.2026 Seeking to impose anti-dumping duty on imports of Sulphenamides Accelerators originating in or exported from China for a period of 5 years

|

|

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Notification no. 10/2026-Customs (ADD) dated 10.06.2026 to amend the Notification no. 51/2021-Customs (ADD) dated 16.09.2021

|

Government of India

Ministry of Finance

(Department of Revenue)

|

Notification No. 10/2026-Customs (ADD) dated 10.06.2026

|

G.S.R…-(E). - In exercise of the powers conferred by sub-sections (1) and (5) of section 9A of the Customs Tariff Act, 1975 (51 of 1975) read with rules 18 and 23 of the Customs Tariff (Identification, Assessment and Collection of Anti-dumping Duty on Dumped Articles and for Determination of Injury) Rules, 1995, the Central Government hereby makes the following amendment in the notification of the Government of India, in the Ministry of Finance (Department of Revenue) No. 51/2021-Customs(ADD), dated the 16th September, 2021, published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i), vide number G.S.R. 637(E), dated the 16th September, 2021, namely:-

|

In the said notification, after paragraph 2 and before Explanation, the following paragraph shall be inserted, namely:-

|

“3. Notwithstanding anything contained in paragraph 2, the anti-dumping duty imposed under this notification shall remain in force up to and inclusive of the 15th December, 2026, unless revoked, superseded or amended earlier.”.

|

(Dheeraj Sharma)

Under Secretary

|

Note: The principal notification No. 51/2021-Customs (ADD), dated the 16th September, 2021 was published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i), vide number G.S.R. 637(E), dated the 16th September, 2021.

|

|

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Notification no. 09/2026-Customs (ADD) dated 22.05.2026

|

|

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Notification no. 08/2026-Customs (ADD) dated 22.05.2026

|

|

|

|

|

|

OFFICE OF THE PRINCIPAL COMMISSIONER OF CUSTOMS (AIR CARGO), AIR CARGO COMPLEX, MEENAMBAKKAM, CHENNAI 600 016 issued PUBLIC NOTICE No : 15/2025 dated 29.07.2025 regarding Enablement of Voluntary Payment electronically on ICEGATE e-Payment Platform

|

Attention of all the Importers, Exporters, General Trade, Other stakeholders, members of trade and Officers of Air Cargo Commissionerate, Chennai is invited to CBIC's circular No. 27/2024- customs dated 23.12.2024 on above mentioned subject.

|

2. In line with Government's commitment to digitize all the services and to make it paperless, ICEGATE e-Payment Platform has been enabled with electronic collection of Voluntary/Self-Initiated Payments (SIP).

|

3. This new functionality has been envisaged to replace the existing TR6 payments which are currently being done manually at various Customs Stations. This functionality shall enable the users to generate a self-initiated challan for voluntary payments and then make payments through the ICEGATE e-payment platform without any further approval by officers of Customs.

|

4. While using the voluntary payment Facility at ICEGATE, the users may take note of the below-mentioned aspects:

|

- a. The Voluntary Payment module will be accessible as a post login functionality. Users must be registered on ICEGATE to access this feature;

- b. This facility is enabled with payments which are primarily meant for imports/exports cleared in the past. In other words, the facility is not a replacement for challans generated by ICES/ECCS/SEZ online/ACES applications. Therefore, it should not be used for payment of customs duties for clearance of any live consignments;

- c. The various purposes, for which the payment can be made are provided in Annexure-A, wherein, it is advised to select the same carefully while making payment.

- d. The proof of payment may be submitted to the concerned sections/field formations for taking further action,

- The officer may verify the payment details using https://foservices.icegate.gov.in/#/epayment/enquiry

5.1 Currently, ICEGATE users can make voluntary payments as a debit from the Electronic Cash Ledger (only available for IEC holders and Customs Brokers).

|

5.2 In case, users wish to initiate challan-wise payment, the ICEGATE platform also allows user to make transaction-wise payment on the platform, whereby the systems design takes care of routing the payment instantaneously through Electronic Cash Ledger before accounting for duty payment. On completion of testing for voluntary payment acceptance, at present, following modes are enabled for such challan wise payments:

|

- a. Nine (9) banks under internet banking through authorized bank mode, as per Annexure-B

- b. NEFT/RTGS through RBI

- Payment Aggregator mode

5.3 Remaining banks shall be enabled as and when the testing is complete. In all other modes, users already have an option to deposit the amount in the Electronic Cash Ledger through remaining authorized modes and use the same for making voluntary payment using Electronic Cash Ledger

|

6. Since the above facility is aimed at replacing the current procedure of making Over The-Counter (OTC) payment using TR-6 Challan, all the officers in Air Cargo Complex, Chennai are not to accept any payments through manual TR-6 challan after 19 JULY, 2025, unless the same is approved by the concerned Pr. Commissioner/Commissioner of Customs. The approval must clearly spell out the reasons for resorting to the manual method of payment. The field officers can view the voluntary challans through 'Payment Status - Voluntary Payment' option available in 'Service' section of ICEGATE portal (http://www.icegate.gov.in)

|

7. An user manual on the Voluntary/Self-Initiated Payment (SIP) facility to handhold and onboard the users has been uploaded (http://www.icegate.gov.in/guidelines/voluntary-payment) on the ICEGATE platform

|

8. Difficulties faced, if any, may be brought to the notice of Joint Commissioner/Additional Commissioner designated as Systems manager in Air Cargo Complex Chennai for necessary action or e-mail the difficulties faced to the following e-mail ID, pcommr7acc-cuschn@gov.in.

|

9. All the stakeholders including the trade and concerned associations are requested to take note of the above. All officers to treat this as Standing instruction.

|

This is issued with the approval of Principal Commissioner of Customs, Air Cargo Commissionerate

|

To,

All Concerned

Copy submitted to:

The Principal Chief Commissioner of Customs,

Chennai Customs Zone .

Copy to:

|

- The Principal Commissioner/Commissioner of Chennai Customs ZoneChennai- I/Chennai–II/ Chennai-III/Chennai-IV/ Chennai Audit.

- The Additional / Joint Commissioners of Customs, Chennai VII

Commissionerate

- All Dy. /Asst Commissioners of Customs, Chennai VII Commissionerate.

- The D.C. (EDI), ACC, Chennai, for uploading on website of Chennai–VII

Commissionerate.

- The Supdt. CHS for notice board display purpose

- Hindi Cell

Annexure-A

One of the following purposes to be selected while using Voluntary

Payment Facility at ICEGATE:

|

- i. Payment pursuant to an Investigation:

- ii. Payment pursuant to Audit;

- iii. Payment pursuant to Internal Compliance; EPCG (Payment of Duty,

- interest. penalty);

- iv. EODC (Payment of Duty, interest, penalty);

- v. Advanced License/Authorization (Payment of Duty):

- vi. IGCR (Payment of Duty, interest, penalty);

- vii. Payment at the time of Pre-Notice Consultation;

- viii. Payment for notices under section 28(2) and 28(4) of Customs Act,

- 1962;

- ix. Payment for closure of proceedings in terms of section 28(5) of the

- Customs Act. 1962:

- x. Payment of interest:

- xi. Payment of penalty:

- xii. Pre-Deposit against appeals:

- xiii. Amounts arising out of proceedings before Settlement Commission:

- xiv. Fines imposed by any order;

- xv. Payment of outstanding demands/ Arrear payments:

- xvi. Amounts arising out of disposal of Uncleared/Unclaimed Goods:

- xvii. Amounts arising out of disposal of seized goods;

- xviii. Amounts arising out of disposal of confiscated goods:

- xix. Amounts arising out of Court Attachment orders;

- xx. Advance ruling (CAAR) fees;

- xxi. Cost recovery charges;

- xxii. Transshipment fees;

- xxiii. Merchant overtime charges;

- xxiv. Bill of Entry (BE) amendment fees;

- xxv. Shipping Bill (SB) amendment fees;

- xxvi. Payments not mentioned above;

- Punjab National Bank (PNB)

- Kotak Mahindra Bank

- IDBI Bank

- Karnataka Bank

- Canara Bank

- Karur Vysya Bank (KVB)

- South Indian Bank (SIB)

- Federal Bank

- IndusInd Bank

|

|

|

|

|

|

|

Office of the Commissioner of Customs (Import-I), New Customs House, Ballard Estate, Mumbai, issued PUBLIC NOTICE NO. 35/2025 dated 04.03.2025. File no. CUS/AG/SO/4/2024-A/G , DIN No. 2025037700000000BDAE on Single Unified Multi-Purpose Electronic Bond in Customs - Ekal Anuband.

|

|

|

|

|

|

Export consignments to West Asia will continue to receive enhanced insurance cover against payment defaults until September 30, the Directorate General of Foreign Trade (DGFT) said in a notification on Monday.

|

Earlier, the enhanced cover for exporters taking credit risk insurance from Export Credit Guarantee Corporation (ECGC) was available for shipments to West Asia sent between March 16 and June 15.

|

The enhanced risk cover announced on March 19 was part of the Resilience and Logistics Intervention for Export Facilitation (RELIEF) scheme under the Export Promotion Mission (EPM) to support exports to West Asia in view of the Iran war.

|

"The eligibility timelines under Component II of the EPM RELIEF intervention are extended up to September 30, 2026 to support Indian exporters and mitigate logistics challenges arising out of the continuing West Asia Crisis," the DGFT said.

|

Source: The Economic Times

|

|

|

|

|

|

|

|

Directorate General of Foreign Trade (DGFT) issued Public Notice No. 17/2026-27 dated 04.06.2026 regarding Enlistment under Appendix 2E of FTP, 2023-Agency Authorised to issue Certificate of Origin (Non-Preferential)

|

|

|

|

|

|

|

|

Directorate General of Foreign Trade (DGFT) issued Trade Notice 07/2026-27 dated 03.06.2026 regarding request for comments on alignment of Schedule-II (Export Policy) of ITC (HS), 2022 consequent to amendments introduced under the Finance Act, 2026

|

|

|

|

|

|

|

|

Directorate General of Foreign Trade (DGFT) issued Notification No. 20/2026-27 dated 02.06.2026 regarding Applicability of Quality Control Orders (QCOs)/ BIS requirements on imports by Special Economic Zone (SEZ) Units and Developers - Amendment in Para 2.03(A)(iii) of FTP 2023

|

|

|

|

|

|

|

|

Directorate General of Foreign Trade (DGFT) issued Notification No. 19/2026-27 dated 02.06.2026 regarding Amendment in import policy condition of specific ITC HS Codes covered under Chapter 71 of ITC (HS), 2022, Schedule - I (Import Policy)

|

|

|

|

|

|

Central Board of Direct Taxes issued Circular no. 4 of 2026 dated 31.03.2026 regarding Document Identification Number (DIN).

|

|

|

|

|

|

|

|

|

GSTN is taking downtime to enhance its services on the GST Portal on 27.06.2026 from 12:00 AM onwards until 2:30 am of 27.06.2026.

|

|

We shall be enhancing services on the GST portal on : 27th June’26 12:00 AM onwards. GST Portal services will not be available until 27th June’26 02:30 AM. The inconvenience caused is regretted.

|

|

|

|

|

|

|

|

|

|

|

GSTN is taking downtime to enhance its services on the GST Portal on 12.06.2026 from 11:30 AM onwards until 7:30 am of 13.06.2026.

|

We shall be enhancing services on the GST portal on : 12th June’26 11:30 PM onwards. GST Portal services will not be available until 13th June’26 07:30 AM. The inconvenience caused is regretted.

|

|

|

|

|

|

|

|

GSTN Advisory no. 664 dated 17.06.2026

|

Reference is invited to the GSTN Advisory dated 20.05.2026 regarding enhancements in the e-Way Bill system, wherein it was informed that “Ship-to GSTIN” shall be mandatorily captured in Bill-to/Ship-to transactions. It was also clarified that where the consignee is an unregistered person, the value “URP” shall be entered in the Ship-to GSTIN field.

|

In this regard, representations have been received from trade, ERP vendors, GSPs, ASPs, private IRPs and other stakeholders seeking clarification on the applicability of the said requirement in cases where e-Way Bill is generated along with e-Invoice or by using IRN. Representations have also been received regarding the Voluntary Closure of e-Way Bill facility and its impact on portal-based and API-based operations.Accordingly, an advisory has been issued to apprise stakeholders of the corresponding changes introduced in the e-Invoice API, e-Way Bill by IRN API and EWB Closure API. It has also been informed that the aforesaid changes have been made available in the Sandbox environment for testing and system preparedness. The changes are scheduled to be implemented in the Production environment with effect from 1st August, 2026.

|

All concerned stakeholders may accordingly be advised to access the advisory through the link given below and undertake necessary testing, system changes and preparedness within the prescribed timeline.

|

|

|

|

|

|

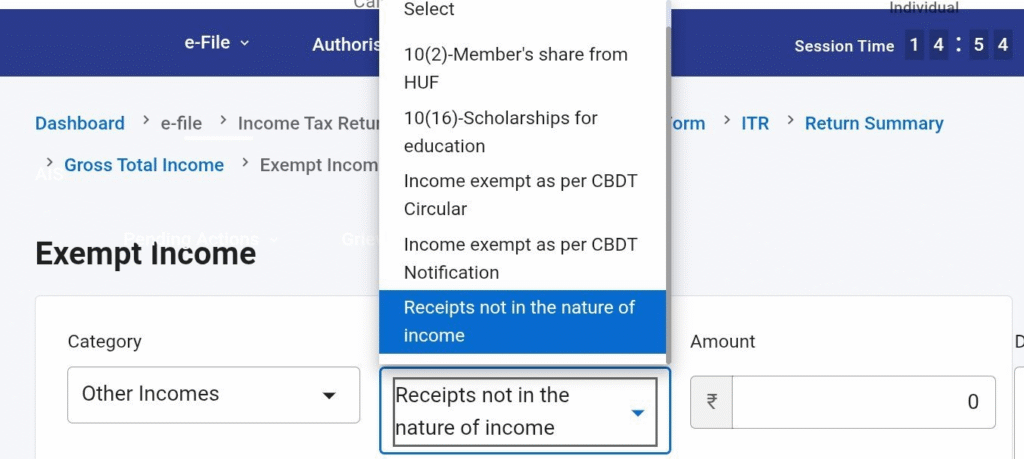

From AY 2026-27, the option to report 'Other Exempt Income' was removed.

|

Earlier, this was useful in situations such as:

|

- Sale of rural agricultural land/ Reporting of Gifts from Relatives - although disclosure was not required as same is not income .

|

The column of 'Other Income' under Exempt incomes has now been added.

|

|

|

|

|

|

|

|

|

|

|

Before applying for Income Tax registration, GST registration, ICEGATE, or DSC mapping, you can use the TRACES PAN Verification facility to check whether the name in the PAN database is correctly aligned with the PAN number.

|

Helps identify name mismatches in advance and avoid registration issues.

|

|

|

|

|

|

|

|

GST UPDATEZ ON 22-10-2024

|

The AAR, Tamil Nadu in the case of M/s. CMA CGM Global Business Services (India) (P.) Ltd., ruled that an Assessee is eligible to avail input services in respect of leasing/ renting/ hiring of motor vehicles of motor vehicles to provide transportation facility to ensure safety and security of women employees as per Tamil Nadu Shops and Establishments Act, 1947.

|

Further, Input Tax Credit (“ITC”) shall be available to the taxpayer only on the tax paid on services or renting, leasing or hiring of motor vehicles for providing transport facilities to women employees alone who are arriving or leaving the workplace between 8 pm to 6 am.

|

M/s. CMA CGM Global Business Services (India) (P.) Ltd. (“the Applicant”) operated in the Information Technology Enabled Services (“ITes”) sector.

|

It was a captive service provider which was engaged in providing back-office support services to its parent company located outside India.

|

As per the Tamil Nadu Shops and Establishment, 1947, it is mandatory for the Applicant to provide a transportation facility for the women employees working in the shifts and provide adequate protection of safety for women employees.

|

Therefore, in compliance with the same, the Applicant procured services of renting of motor vehicle for women employees working beyond 8.00 PM. Also, the Applicant has the policy where women employees have to login from 9 pm till 6 am or if leaving after 8pm till 6 am to use cab facility, this facility is provided irrespective of login/logout timing.

|

"Whether the Assessee can avail ITC on the Input Services for leasing/ renting motor vehicles for women’s safety?"

|

Further, as per the provisions of Tamil Nadu Shops and Establishment Act, 1947, it is obligatory on the part of the Applicant to provide transport facilities to women employees working beyond 8 pm.

|

Hence, the Applicant is eligible to avail input services in respect of leasing/renting/hiring of women employees subject to satisfying conditions of eligibility provided under Section 16 of the CGST Act.

|

Though Rent a cab is generally blocked credit in terms of Section 17(5), ITC in respect of such goods and services or both shall be available, where it is obligatory for an employer to provide the same to its employees which has been done in terms of mandatory obligation as per the Notification (G.O. Ms No. 60, Labour and Employment (K2) dated May 28, 2019 by the Government of Tamil Nadu.

|

R.SRIVATSAN, IRS,

NACIN, Chennai

|

|

|

|

|

|

4. Lawgics by Ms.Nidhi Aggarwal

|

Ms. Nidhi Aggarwal is delighted to present judgment with a great vision to spread complex GST law in a simple manner amongst the taxpayers, tax professionals, students and knowledge seeker.

|

|

Recently added notes are listed below:

|

|

|

|

|

|

Synopsis: The Delhi High Court dismissed the writ petition involving fraudulent ITC claims, directing the petitioner to pursue appellate remedy u/s 107 of the CGST Act.

|

Caste name: Banson Enterprises & Anr. vs Assistant Commissioner CGST & Ors.

|

Citation: W.P. (C) 6503/2025 dated 15.05.2025

|

Authority: Delhi High Court

|

The petition challenges the Order-in-Original dated 02.02.2025 based on a Show Cause Notice (SCN) dated 03.08.2024 A search was conducted, and statements were recorded including that of one Director admitting to the issuance of fake invoices during the Central Excise period. It was alleged that the Petitioner issued goods-less invoices to enable fraudulent Input Tax Credit (ITC) claims amounting to Rs. 1.85 crore.

|

Contentions of the Petitioner:

|

SCN was issued by unauthorized officer, thus, violates Rule 142(1)(a) of CGST Rules. No pre-consultation as required under Rule 142(1A) of CGST Rules was issued. Consolidated SCN for multiple financial years was issued and challenge to such consolidated action is pending in a separate matter (Quest Infotech case).

|

Contentions of the Department:

The impugned order is appealable, hence writ is not maintainable. The Petitioner’s Director admitted to allegations. Natural justice was followed as the Petitioner received the SCN, filed a reply, and availed of personal hearing. Reliance must be made on SC judgments and Allahabad HC rulings emphasizing alternate remedy u/s 107 CGST Act.

|

Findings and Decision of the Court:

The Court refused to interfere under writ jurisdiction, citing:

|

- No breach of fundamental rights or principles of natural justice.

- Availability of a statutory remedy (appeal) under Section 107 CGST Act.

The Court noted that the Allegations involve serious misuse of ITC, requiring fact-based adjudication, not suited for writ jurisdiction. Thus, the Petitioner was granted liberty to file appeal, and if filed with pre deposit, the appeal shall not be dismissed on limitation.

|

|

|

|

|

|

5. GST Notes by CMA Anil Sharma

1) New slides on GST Circulars is added in the Notes section titled as "Capsules".

|

- Total 25 slides in capsule-01 is added

|

|

|

|

|

|

|

|

6. GST Daily by CA Pradeep Modi

CA Pradeep Modi is presenting judgment analysis under title 'GST Daily - Stay yourself updated'

|

|

|

|

|

|

THE HON'BLE ALLAHABAD HIGH COURT IN THE CASE OF Vibhuti Tyres V/s State of U.P., decided on 7-5-2025

|

✔️ Is it justified that GST order with higher demand than show-cause notice?

|

👉 The Hon'ble High Court Judgement:-

|

✔️ Where in show-cause notice amount representing tax, interest and penalty was indicated as Rs. 8,81,080, but in order, much higher demand was raised at Rs. 32,97,336, same was in violation of section 75(7); matter was to be remanded back.

|

Section 75 of Central Goods and Services Tax Act, 2017

|

|

|

|

|

|

|

|

THE HON'BLE JHARKHAND HIGH COURT IN THE CASE OF Sadanand Prasad Barnwal V/s State of Jharkhand, decided on 8-5-2025

|

✔️ Is it valid if SCN and order under section 73 for lack of digital signature of issuing authority?

|

👉 The Hon'ble High Court Judgement:-

|

✔️ Where both summary of SCN in Form GST DRC-01 and order under section 73 did not bear digital signature of concerned authority, both SCN and order were to be quashed.

|

Section 161, read with section 73 of Central Goods and Services Tax Act, 2017

|

|

|

|

|

|

|

|

THE HON'BLE CALCUTTA HIGH COURT IN THE CASE OF Edelweiss Rural & corporate Services Ltd. V/s Deputy Commissioner of Revenue, decided on 5-5-2025

|

✔️ What would be Refund if business stood closed and registration was cancelled?

|

👉 The Hon'ble High Court Judgement:-

|

✔️ Where Refund sanction order had itself observed that assessees business was closed down, its registration was cancelled and it had no tax dues refund claim was already allowed, direction to credit refund amount to credit ledger instead of bank account of assessee was self-contradictory since there was no business for assessee to take benefit of refund credited to assessees credit ledger.

|

Section 54 of Central Goods and Services Tax Act, 2017

|

|

|

|

|

|

|

|

THE HON'BLE JHARKHAND HIGH COURT IN THE CASE OF Sri Ram Stone Works V/s State of Jharkhand, decided on 9-5-2025

|

✔️ Can GST Notice would be issued under Section 61 of CGST Act merely on the basis of difference between sale price and market price?

|

👉 TheHon'ble High Court Judgement:- ✔️ Clear objective of section 61 is to enable an Assessing Officer to point out discrepancies and errors which are occurring in return filed by a registered person with that of related particulars; notice under section 61 cannot be issued comparing particulars at which assessee has sold its goods with that of prevalent market price.

|

|

|

|

|

|

|

|

THE HON'BLE ALLAHABAD HIGH COURT IN THE CASE OF Gopal Trading Company V/s State of U.P., decided on 7-5-2025

|

✔️ Can excess stock during search warrants proceedings would be confiscation under section 130 of CGST?

|

👉 The Hon'ble High Court Judgement:-

|

✔️ Where in search at premises of assessee, excess stock was found, Act specifically contemplates that proceedings under section 73/74 should be pressed; proceedings under section 130 could not have been pressed.Section 67, read with sections 73, 74 and 130, of Central Goods and Services Tax Act, 2017

|

|

|

|

|

|

|

|

THE HIGH COURT AT CALCUTTA Anmol Stainless Pvt. Ltd. V/s Deputy Commissioner of State Tax, Serampore Charge

|

✔️ Can any demand order would be stayed on as SCN issued under extended Section 73(9) timeline citing lack of force majeure?

|

👉 The Hon'ble High Court Judgement:-

|

✔️ Where show cause cum demand notice was issued in respect of period April, 2019 to March, 2020 as late as on 30-4-2024 in view of Notification Nos. 9/2023-CT and 56/2023-CT by which time limit for issuance of order under section 73(9) was extended while assessee challenged same on ground that there was no force majeure prevailing at relevant time and, hence, respondents could not have relied on these Notifications, there was prima facie case; affidavit-in-opposition to writ petition was to be filed and demand was to be stayed.

|

Section 73, read with section 168A, of Central Goods and Services Tax Act, 2017

|

|

|

|

|

|

|

|

THE HON'BLE MADRAS HIGH COURT IN THE CASE OF Union of India V/s Flemingo Duty Free Shop Pvt. Ltd. , decided on 29-4-2025

|

✔️ Is it justified for Revenue to examine if tax impact was revenue neutral or resulted in loss of revenue before taking any action?

|

👉 TheHon'ble High Court Judgement:-

|

✔️ Where petitioner entered into concession agreement with Airport Authority of India for operation of Duty Free Shop at International Airport and paid minimum guarantee/revenue share, revenue Authorities should examine as to whether tax effect was in fact revenue neutral or there was any loss of revenue and thereafter proceed in accordance with law.

|

|

|

|

|

|

|

|

THE HON'BLE ALLAHABAD HIGH COURT IN THE CASE OF

|

Arena Superstructures Pvt. Ltd. V/s Union of India, decided on 22-4-2025

|

✔️ Can department would be create any demand if Once resolution plan approved?

|

👉 The Hon'ble High Court Judgement:-

|

✔️ Assessee submitted that once resolution plan had been approved by NCLT, GST department could not create further dues by way of passing orders.

|

✔️ The HON'BLE Supreme Court in the case of Vaibhav Goel v. Deputy Commissioner of Income-tax 172 taxmann.com 601 (SC), held that successful resolution applicant cannot be faced with "undecided" claims after resolution plan had been accepted.

|

✔️ In view of same, it was clear that once resolution plan was approved by NCLT, all other creditors were barred from raising claims subsequently - Accordingly, impugned assessment order was to be set aside.

|

Section 74 of Central Goods and Services Tax Act, 2017

|

|

|

|

|

|

|

|

THE HON'BLE GUJARAT HIGH COURT IN THE CASE OF BVM Pharma V/s Union of India, decided on 27-3-2025

|

✔️ Can GST would be levied on assignment of leasehold rights in land and building?

|

👉 The Hon'ble High Court Judgement:-

|

✔️ Where assessee-lessee transferred leasehold rights of its industrial plot to third party-assignee by transfer order and thus, third party-assignee would now become lessee, assignment of leasehold rights of land and building by assessee would not be subject to levy of GST.

|

✔️ In Gujarat Chamber of Commerce and Industry v. Union of India 2025 it was held that provisions of section 7(1)(a) providing for scope of supply read with clause 5(b) of Schedule II and Clause 5 of Schedule III would not be applicable to such transaction of assignment of leasehold rights of land and building and same would not be subject to levy of GST.

|

|

|

|

|

|

|

|

THE HON'BLE DELHI HIGH COURT IN THE CASE OF Gurudas Mallik Thakur V/s Commissioner of Central Goods and Service Tax, decided on 23-4-2025

|

✔️ Can Filing of appeal under section 107 would be available to either taxable persons or any aggrieved person too?

|

👉 The Hon'ble High Court Judgement:-

|

✔️ Where petitioner-director of a company filed writ petition challenging levy of penalty on him on ground of ITC fraud and took stand that he had already resigned at relevant time, since matter required closer scrutiny on facts as to who was responsible for running company, petitioners should avail appellate remedy.

|

✔️ Filing of appeal under section 107 is permissible by any person and not merely by a taxable person.

|

|

|

|

|

|

|

|

THE HON'BLE MADRAS HIGH COURT IN THE CASE OF Tvl. Arun Traders V/s Union of India, decided on 8-4-2025

|

✔️ Can pre-deposit would be paid later on if it is inadvertently not deposited at time of filing appeal?

|

👉 The Hon'ble High Court Judgement:-

|

✔️ Where 10 per cent of pre-deposit amount was not paid to department at time of filing appeal due to inadvertence, in interest of justice, assessee should deposit required pre-deposit amount and Appellate Authority should restore appeal.

|

Section 107 of Central Goods and Services Tax Act, 2017

|

|

|

|

|

|

|

|

THE HON'BLE KARNATAKA HIGH COURT IN THE CASE OF Indian Oil Corporation Ltd. V/s Assistant Commissioner of Central Tax, decided on 20-8-2024

|

✔️ Can Refund under inverted duty structure would be denied merely due to the same rate on principal input and output?

|

👉 The Hon'ble High Court Judgement:-

|

✔️ Where accumulated ITC results from any inputs being taxed at higher rates than output supplies, refund under Section 54(3)(ii) cannot be denied merely because principal input and output attract same tax rate.

|

Section 54 of Central Goods and Services Tax Act, 2017

|

|

|

|

|

|

|

|

THE HON'BLE ALLAHABAD HIGH COURT IN THE CASE OF Simla Gomti Pan Products Pvt. Ltd. V/s Commissioner of State Tax, ,decided on 10-4-2025

|

✔️ Can it would be relaxed in limitation period if time spend by assessee before High Court and Supreme Court?

|

👉 The Hon'ble High Court Judgement:-

|

✔️ Where appeal filed by assessee against assessment order was dismissed as barred by limitation and while passing said order, time spend by assessee before High Court and Supreme Court in challenge to said order was not considered by appellate authority, order dismissing appeal was to be quashed and matter was to be remanded to pass fresh orders.

|

Section 107 of Central Goods and Services Tax Act, 2017

|

|

|

|

|

|

|

|

BEFORE THE AUTHORITY FOR ADVANCE RULING UNDER GST, GUJARAT

|

re :Inox Air Products Pvt. Ltd., decided on 25-3-2025

|

👉 The AUTHORITY FOR ADVANCE RULING Judgement:-

|

✔️ In terms of section 17(5)(h) applicant is required to reverse ITC involved in inputs used in outward supply which was in transit.

|

|

|

|

|

|

7. PPT/Handbook on GST

|

|

|

|

8. GST/Income Tax in Media

|

|

|

- Govt extends GST Appellate Tribunal appeal filing deadline to July 31 after portal rush

- Representation seeking extension of the last date for filing appeals before GSTAT by ICAI-NIRC

- Tax authorities appeal to reinstate ₹368.72 crore GST penalty on Tata Steel

- Portal glitches put thousands of GST appeals at risk; experts seek deadline extension

- Firm moved to a new GST jurisdiction? CBIC issues clarity on how pending cases will be handled

- Certificate of Meritorious Service (CBIC-CMS)

- Representation seeking extension of the last date for filing appeals before GSTAT by MCTC

- Will former RBI governor Shaktikanta Das replace Nirmala Sitharaman as finance minister?

- 57th GST Council meeting next month

- Representation seeking extension of the last date for filing appeals before GSTAT by KSCAA

- Businesses embrace GST, but seek more reforms: Deloitte survey

- Kanpur man wins tax battle after losing Rs 1.95 crore through wife's trading account: 'Income generated from…'

- UPERC recognises GST cut on renewable energy equipment as ‘Change in Law’ event

- Representation seeking extension of the last date for filing appeals before GSTAT by STBA

- Representation seeking extension of the last date for filing appeals before GSTAT by GSTAT Bar Association, Delhi

- Representation seeking extension of the last date for filing appeals before GSTAT by Taxation Bar Association, Agra

- Representation seeking extension of the last date for filing appeals before GSTAT by ADVOCATES’ TAX BAR ASSOCIATION

- Office Order No. 88/2026 — Officers In & Out (Zones + Directorates)

- GST fraud network busted in Lucknow, key accused arrested

- GST has improved transparency, but simpler rules needed: CMDR study

- Bharat Metal Exchange Ltd requested Circular clarifying GST Refund mechanism for statutory pre-deposit

- Five booked in Rs 3,000-crore fake GST invoice racket using shell firms in Punjab

- TG-Press Note: Arrest under GST

- Cestat ruling: Stock brokers may get clarity on delayed payment charges

- GST inspector in Maharashtra in Rs.10k graft case

- CGST officer chargesheeted in Rs. 10 lakh bribery case

- Delhi launches 2-week GST training programme to strengthen tax system

- Despite the introduction of GST audit department, there are serious lapses in Ernakulam, which receives the highest tax rate.

- Shah Batteries Director Held for GST Fraud

- Flipkart moves Kolkata HC for GST exemption on delivery charges after appellate ruling setback

- Next GST Council meeting to focus on 'process reforms', inverted duty structure fixes

- E-way bill generation post GST rollout fouth-highest in May 2026

- Zomato gets Rs 9.6 crore GST demand from Andhra Pradesh tax authorities

- Maharashtra cabinet clears amendments to GST law to align state with Centre, eases compliance for businesses

|

|

|

|

|

|

|

|

|

|

GST Litigation Course by OTU:

|

|

onlinetaxupdate.com is conducting a GST Litigation Course with 3 sessions of 2 hours each by Best Industry speaker tentatively in November 2024

|

|

|

|

|

|

|

Hope the above updates is of use to you. Please share your input and feedback at taxupdate.otu@gmail.com

|

|

|

|

|

|

|

|

|

Visit our website

|

OTU provides you

|

- Articles on various topics

|

|

- Media - GST, Income Tax & Press R.

|

|

|

|

|