|

onlinetaxupdate team wish to express sincere thanks to all the readers, authors, subscribers for the support extended to us. Please share your feedback at

|

taxupdate.otu@gmail.com or 7738647904

|

Newsletter 130 dated 12.08.2024

|

|

|

|

|

|

|

|

|

Dear Reader,

|

Please find newsletter for your reading and reference.

|

|

Index of the Newsletter

- Recent updates

- Budget Posts

- Article

- Lawgics by Ms.Nidhi Aggarwal

- GST Notes by CMA Anil Sharma

- GST Daily by CA Pradeep Modi

- PPT/Handbook

- GST/IT/Customs in media

- Latest Update - Recap

|

|

|

|

|

|

|

Micro, Small and Medium Enterprises (MSMEs) are essential for India's economic growth, creation of employment and supporting large industries with cost-effective solutions. Over the years, the Goods and Services Tax (GST) has played a significant role and benefitted MSMEs by unifying the tax structure, easing logistical movement and in creating a transparent business environment.

|

Insights from Deloitte’s GST@7 survey

According to the survey, 78% of MSMEs now holds a favourable view of GST's 7-year journey, up from 66% in the GST@6 survey of 2023. 70% find quarterly return filing beneficial and expressed efficiencies in the supply chain as a key positive area. Around 69% of the respondents demonstrate robust support to tax compliance automation, e-invoicing etc as top performance areas of the Government.

|

Keeping in mind the industry sentiment, the much anticipated 53rd GST Council meeting convened on 22 June 2024, set the stage for more trade friendly measures to be adopted.

|

Recommendations of the recently concluded GST Council meeting

Some of the proposals made by the Council such as conditional waiver of interest and penalty not involving extended period of limitation, extension of time limit for availing of input tax credit (ITC) for invoices or debit notes, introduction of GSTR1A for amendment in GSTR1, rate rationalisation on specified products etc. would enable taxpayers including the MSMEs to experience a notable improvement in functioning of the business. To strengthen the registration process and combat fake ITC, biometric-based Aadhaar authentication of registration applicants has been proposed pan-India, in a phased manner which will further ease out the credit availability for the MSMEs.

|

The Council has also recommended reducing the Tax Collected at Source (TCS) rate for e-commerce operators from 1% to 0.5%. This particularly reflects a conscious effort by the Government to address the challenges being faced by small businesses like MSMEs and to help ease the working capital and financial burden on suppliers using these platforms.

|

GST 2.0 – Reforms to boost the MSMEs

While the Government has shown willingness to address the sector concerns, MSMEs are looking forward for additional focus on introducing transformative and progressive reforms for its growth and the economy at large.

|

The insight from the survey reveals that 88% of MSMEs expects further liberalisation of ITC by way of removal of restrictions on ITC which has been a universal challenge across businesses. The Government should permit small businesses to claim ITC based on the invoice received and without the requirement to match with the auto-generated GSTR 2B.

|

Further, 79% of the respondents expects more rationalisation of GST rates for the entire supply chain, 74% want a mechanism to unlock the working capital measures and 73% are looking forward for the Government to address the inverted duty structure in a holistic manner.

|

While the Government has been receptive on the challenges faced by e-commerce operators, the industry continues to hope that the Government will further make amendments as we move towards GST 2.0 to exempt GST TCS on e-commerce operators on facilitation of zero-rated supplies (ie, primarily exports), to help with the cash flow issue for exporters and facilitate the ease of compliances.

|

The survey also reveals that the industry continues to experience challenges by way of authorities' pro-revenue stance, aggressive audit techniques, prolonged proceedings and parallel proceedings being initiated by central and state authorities. The GST Council should aim to further streamline the document requirements for audits and assessments which would benefit all taxpayers, especially the MSME sector.

|

Presently, the GST law prescribes multiple conditions for a dealer to opt for the composition scheme such as no inter-state supply can be made, no ITC can be claimed on procurements, turnover capping at Rs 1.5 crores etc. The small businesses are unable to take advantage and register for the composition scheme, where interstate sales are sought to be made by below threshold or composition dealers. The Government should consider relaxing the conditions to enable small businesses to avail the benefit of the composition scheme.

|

Furthermore, the industry expects the Government to revise the Production Linked Incentive (PLI) schemes, expanding benefits to new sectors like apparel, textiles, and furniture, which are significant job creators driven by MSMEs.

|

As GST completes seven years, and we are moving towards GST 2.0, continued consistent policies promoting "Atmanirbhar Bharat" are expected, aiming to reduce operational costs, improve customer experience particularly for MSMEs and bolster India's economic growth.

|

The writer is Partner, Deloitte India

|

|

|

|

|

|

Haryana Excise & Taxation Department, issued an Instruction via memo no. 1217/GST-II daed 29.11.25 regrading taking up Suo-Moto Cases for Audit/ Scrutiny under the HGST Act, 2017.

|

Your attention is invited to the subject cited above. In this context, it is hereby directed that whenever any suo-moto case is proposed to be taken up for audit or scrutiny, the same shall be submitted with a clear, specific, and duly justified reasons and must also include the tentative quantum of tax evasion on the basis of available records, intelligence inputs, data analysis, or any other verifiable source of information.

|

Further, it is mandated that every such proposal for initiating suo-moto audit/scrutiny shall first be examined and recommended by the Deputy Excise and Taxation Commissioner (DETC) concerned and after the DETC's recommendations, the case file shall be forwarded to the Joint Excise and Taxation Commissioner (Range) for obtaining the necessary approval.

|

All field formations shall ensure strict compliance with these instructions. Any initiation of suo-moto action without adherence to the above-mentioned procedure shall be viewed seriously.

|

This issues with the approval of the competent authority.

|

|

|

|

|

|

|

|

Government of Assam, Guwahati issued Instruction no. 20/2025-GST dated 05.06.2025 prescribing Standard Operating Procedure on Road Vigilance.

|

No. CG/GST-40/2020/182 - To prevent tax evasion and protect government revenue, it is essential to establish a mechanism for monitoring the movement of goods and individuals engaged in transporting goods within Assam. Section 68 of the Assam Goods and Services Tax Act, 2017, grants the state government the authority to mandate specific documents that must be carried by the person in charge of a conveyance for any consignment of goods. Additionally, it empowers the proper officer to intercept such conveyances, verify the required documents, inspect the goods, and ensure compliance by the person in charge of the transport.

|

Rule 138 of the Assam Goods and Services Tax Rules, 2017 mandates the generation of an e-way bill and the electronic submission of relevant details on the common portal before initiating the movement of taxable goods valued at over fifty thousand rupees. Additionally, Rule 138A requires the person in charge of a conveyance to carry specific documents, including an invoice, bill of supply, delivery challan, and a copy of the e-way bill along with its number. Rule 138B authorizes the interception of conveyances for verification of documents and goods. Rule 138C stipulates that a summary report of every transit inspection must be recorded online by the proper officer within twenty-four hours, with a final report submitted within three days. Rule 138D further requires the online uploading of information related to vehicle detention.

|

To ensure the verification of e-way bills and necessary documents during the movement of goods by conveyance, as well as to conduct inspections aimed at preventing tax evasion, it has been deemed essential to implement random road vigilance at the following strategic locations:

|

(1) Srirampur (Dist-Kokrajhar) and (2) Chagolia (Dist. Dhubri)

|

For the purpose of such road vigilance the following guidelines are issued;

|

- Officers and staff will be deputed for road vigilance activities and each team will consist of one Superintendent of Taxes, two Inspector of Taxes and two Assistants respectively. Additionally, for all the teams a total of twenty assistants and grade-IV staff will be engaged for assistance.

- Each day, the road vigilance teams are expected to collectively inspect approximately 200 vehicles.

- All vehicles checked shall invariably have to be entered in the e-way bill portal as required under the Assam Goods and Services Tax Rules, 2017.

- On detection of irregularities and detection of tax evasion by the road vigilance team, penalty shall be levied as per provision of section 68 and 129 of the Assam Goods and Services Tax Act, 2017 as deemed fit.

- All teams should maintain a "Log Book" as per proforma furnish below:

- Daily report will have to be furnished to Apex Office by 09:00 A.M of the following day as per the following proforma with an intimation to the concerning Deputy Commissioner of Taxes:

- CCTV cameras shall be installed at the area of inspection and body worn camera shall be used while carrying vigilance activities. The footage of the body worn camera and CCTV videos shall be analyzed randomly at Apex Office during and after drive is completed.

- The road vigilance teams shall strictly follow the procedure laid down in the Assam Goods and Services Tax Act, 2017 and rules made there under. They shall also adhere to all the orders, instruction and circulars issued or to be issued from time to time by Commissioner of Taxes, Assam.

- The road vigilance teams shall ensure that such vehicle checking causes minimal/less disruptions/ disturbance in regular traffic movement. Further, the officers hall also ensure that the inspection/ checking of vehicles undertaken by them does not create a false impression about extensive / indiscriminate checking. Road vigilance teams shall keep devising their own plan for interception and time for such interception shall be unpredictable /random.

- For Non-GST items which are exempted from the purview of e-way bill vide clause (f) of sub-rule (14) of rule 138 of the Assam Goods and Services Tax Rules, 2017, the officers are required to follow the provisions of the Assam Value Added Tax Act, 2003 and rules made thereunder. In such cases, it should be ensured that the person in charge of a conveyance carry specific documents such as Delivery Note or Road Permit or Transit Pass, as the case may be along with other relevant documents.

- Any departure from the aforementioned directives will be take seriously. Additionally, instances of misuse of power or non-adherence to rules by officers will be addressed with strict measures.

This Order is issued with the concurrence of the Government and shall come into force with immediate effect.

|

|

|

|

|

|

CBIC issued clarification via F. No. CBIC-20016/75/2025-GST dated 25.09.2025 on requirement of separate GST registration for importers storing goods in Warehouses in other States

|

|

|

|

|

|

Export consignments to West Asia will continue to receive enhanced insurance cover against payment defaults until September 30, the Directorate General of Foreign Trade (DGFT) said in a notification on Monday.

|

Earlier, the enhanced cover for exporters taking credit risk insurance from Export Credit Guarantee Corporation (ECGC) was available for shipments to West Asia sent between March 16 and June 15.

|

The enhanced risk cover announced on March 19 was part of the Resilience and Logistics Intervention for Export Facilitation (RELIEF) scheme under the Export Promotion Mission (EPM) to support exports to West Asia in view of the Iran war.

|

"The eligibility timelines under Component II of the EPM RELIEF intervention are extended up to September 30, 2026 to support Indian exporters and mitigate logistics challenges arising out of the continuing West Asia Crisis," the DGFT said.

|

Source: The Economic Times

|

|

|

|

|

|

Press release ID 2279424 dated 30.06.26

|

The Government had earlier provided a full Customs Duty exemption on imports of critical petrochemical products till 30th June 2026, as a temporary and targeted relief in view of the conflict in West Asia and the consequent disruptions in global supply chains.

|

The exemption was provided to ensure sufficient availability of petrochemicals in the domestic market as Indian petroleum companies had been asked to concentrate on the production of LPG during this period. As the situation is gradually normalizing, to ensure a smooth and non-disruptive transition for the affected sectors, it has been decided to extend the said exemption by a further period of 15 days, that is, till 15th July 2026.The list of products covered remains the same as notified earlier.

|

The Government remains committed to supporting India's manufacturing sector. As before, the exemption is expected to benefit a wide range of sectors dependent on petrochemical feedstock and intermediates, including plastics, packaging, textiles, pharmaceuticals, chemicals, automotive components and other manufacturing segments. This will also provide relief to consumers of final products.

|

Link to previous press note issued:

|

|

|

|

|

|

|

|

Press release ID 2279409 dated 30.06.2026

|

|

In a major operation the officers of the Directorate of Revenue Intelligence (DRI) successfully dismantled a trans-border gold smuggling syndicate and seized 15 kg foreign-origin smuggled gold, valued at approximately Rs. 21.40 crore, operating from Delhi.

|

|

|

DRI officers intercepted an international courier consignment originating from Thailand at Courier Terminal, Delhi. The consignment was in the name of a firm linked to a foreign national.

|

A meticulous examination of the consignment declared as "worn gear", led to the recovery of eight disc-shaped pieces of foreign-origin gold, each weighing 1.5 kg, ingeniously concealed inside gear parts. In total, 12 kg smuggled foreign-origin gold was recovered from the courier consignment.

|

Simultaneous searches conducted at the residence of the intended recipient and the alleged mastermind resulted in the recovery of two more identical disc-shaped pieces of foreign-origin gold, each weighing 1.5 kg.

|

Four persons, including the mastermind, who is a repeat offender, and a foreign national have been arrested in relation with the case.

|

Preliminary investigations also reveal that crypto-currency was being used to transfer the money across borders to finance the smuggling.

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Corrigendum on 12.06.2026 to Notification no. 45/2025 -Customs dated 24.10.2025 -

|

G.S.R…(E).- In the notification of the Government of India, Ministry of Finance (Department of Revenue) No. 45/2025-Customs, dated the 24th October, 2025, published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i), vide number G.S.R. 781(E), dated the 24th October, 2025, at page 291, in lines 12 and 14, for ‘1993’ read ‘1983’.

|

|

|

|

|

|

Central Board of Direct Taxes (CBDT) issued notification no. 72/2026 dated 25.06.2026 to hereby approves deductions under section 45(3)(a)(i) of the Income-tax Act, 2025 and rules 32 and 34 of the Income-tax Rules, 2026 to the Public Health Foundation of India, Delhi (PAN: AABAP4445L) for Scientific Research under the category of University, college or other institution.

|

|

|

|

|

|

|

|

Central Board of Direct Taxes (CBDT) issued notification no. 71/2026 dated 25.06.2026 to hereby approves deductions u/s 45(3)(a)(i) of the Income-tax Act, 2025 and rules 32 and 34 of the Income-tax Rules, 2026 to the University of Hyderabad (PAN: AAAAU8109M) for Scientific Research under the category of university, college or other institution.

|

|

|

|

|

|

|

|

Central Board of Direct Taxes (CBDT) issued notification no. 70/2026 dated 01.06.2026 to hereby specifies the business (other than the business specified in Note 5(d)(i) of the said Schedule), which is engaged in the infrastructure sub-sectors mentioned in the Updated Harmonised Master List of Infrastructure sub-sectors, in the notification of the Government of India in the Ministry of Finance, Department of Economic Affairs number F.No.13/1/2025-IPP, dated the 19th September, 2025, published in Gazette of India, Extraordinary, Part I, Section 1, as a business for the purposes of Schedule V of the said Act.

|

This notification shall come into force from the date of its publication in the Official Gazette.

|

|

|

|

|

|

|

|

Central Board of Direct Taxes (CBDT) issued notification no. 69/2026 dated 30.05.2026 to provide deduction u/s 45(3)(a)(i) of the Income-tax Act, 2025 and rules 32 and 34 of the Income-tax Rules, 2026 to the National Institute of Advanced Studies, Bangalore (PAN: AAATN2269A) for Scientific Research under the category of University, college or other institution, for the purposes of section 45(3)(a)(i) of the said Act of 2025 and rules 32 and 34 of the Income-tax Rules, 2026.

|

This notification shall be applicable to the National Institute of Advanced Studies, Bangalore for the tax years 2026-2027 to 2030-2031, subject to the conditions that it shall–

|

(i) comply with the conditions specified in rule 34 of the Income-tax Rules, 2026;

|

(ii) prepare statement under section 45(4)(a) of the Income-tax Act, 2025 for each tax year in Form No.15 and deliver or cause to be delivered to the Director General of Income-tax (Systems) or the person authorised by him on or before the 31st May, immediately following the tax year in which the donation is received, in accordance with rule 31 of the Income-tax Rules, 2026:

|

(iii) furnish to the donor, a certificate in Form No.16 specifying the amount of donation in accordance with rule 31 of the Income-tax Rules, 2026.

|

|

|

|

|

|

|

|

Central Board of Direct Taxes (CBDT) issued notification no. 68/2026 dated 30.05.2026 to provide deduction u/s 45(3)(a)(i) of the Income-tax Act, 2025 and rules 32 and 34 of the Income-tax Rules, 2026 to the S. Nijalingappa Sugar Institute, Belgaum (PAN: AAATK6236C) for Scientific Research under the category of University, college or other institution.

|

This notification shall be applicable to the S. Nijalingappa Sugar Institute, Belgaum for the tax years 2026-2027 to 2030-2031, subject to the conditions that it shall––

|

(i) comply with the conditions specified in rule 34 of the Income-tax Rules, 2026;

|

(ii) prepare statement under section 45(4)(a) of the Income-tax Act, 2025 for each tax year in Form No.15 and deliver or cause to be delivered to the Director General of Income-tax (Systems) or the person authorised by him on or before the 31st May, immediately following the tax year in which the donation is received, in accordance with rule 31 of the Income-tax Rules, 2026:

|

(iii) furnish to the donor, a certificate in Form No.16 specifying the amount of donation in accordance with rule 31 of the Income-tax Rules, 2026.

|

|

|

|

|

|

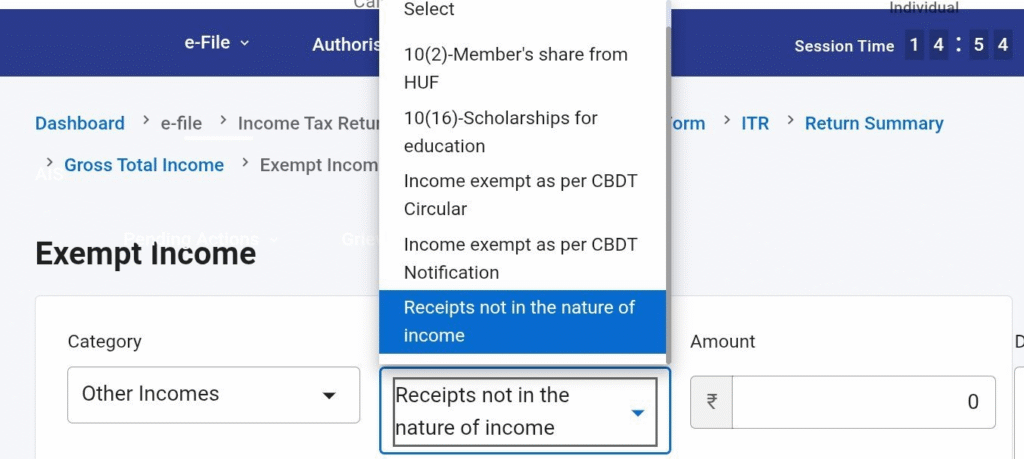

From AY 2026-27, the option to report 'Other Exempt Income' was removed.

|

Earlier, this was useful in situations such as:

|

- Sale of rural agricultural land/ Reporting of Gifts from Relatives - although disclosure was not required as same is not income .

|

The column of 'Other Income' under Exempt incomes has now been added.

|

|

|

|

|

|

|

|

|

|

|

|

|

No, the Honorable Madras High Court in Perfect Assayers (P.) Ltd. v. State Tax Officer (ST) (W.P. No.12083 of 2024 dated 03.06.2024] allowed the writ petition and set aside the Order-in-Original when reply filed by the taxpayer in response to the discrepancies raised in returns has not been taken into consideration. The Honorable Madras High Court noted that the Operative part of the impugned order is bereft of any proper reasoning as the explanation provided in relation to discrepancies as per the SCN by way of reply filed has not been taken into consideration and has not discussed properly the explanation and recorded the reason for rejecting the petitioner's explanation in the impugned order. The Honorable Court held that the impugned order is set aside and the matter is remanded back for reconsideration.

|

There is an urgent need to understand that the linear comparison of two different data sets is meaningless in GST. Yes, it may raise suspicion but no adverse inference can be made regarding non-payment, short-payment, or evasion of taxes.

|

In this particular case, output tax (GSTR-1 not matching GSTR-3) is demand citing data differences without stating (i) the nature of supply (ii) the taxability of the same (iii) the HSN code (iv) the time of supply, and (v) the place of supply. Without these taxing ingredients, any demand for output tax is arbitrary and illegal.

|

This principle has been laid by the Honorable Apex Court in the case of Govind Saran Ganga Saran v. CST * Ors. AIR 1985 SC 1041, where it was held that four ingredients are required to be present in any proceedings to demand tax.

|

|

|

|

|

|

Recording of Statements:

Recording of statement is an important and integral part of any proceedings or investigation. In taxation matters also the statements of the taxpayers or witnesses are recorded on oath by the officers. Such statement may be recorded either during the search & seizure proceedings or during the summon proceedings or during the Survey proceedings etc. The relevant legal provision of recording statement under various taxation laws can be summarized as follows:

|

The confession or admission made in the statements serve as a material piece of evidence and has evidentiary value provided it is corroborated by some other independent evidences. It is settled law that admission by a person is a good piece of evidence though not conclusive and the same can be used against the person who makes it. Statement recorded during the investigation is only the starting point of the investigation and not the end. The Supreme Court in Kishori Lal v. Mt. Chaltibai AIR 1959 SC 504 considered the evidentiary value of an admission and the fact that an admission shifts the onus in terms of section 31 of the Evidence Act (now section 25 of the Bhartiya Sakshya Adhiniyam, 2023), held that:

|

“. . . the admissions shifted the onus on to the respondent on the principle that what a party himself admits to be true may reasonably be presumed to be so and until the presumption was rebutted, the fact admitted must be taken to be established….’’

|

So the statements are often used against the maker to establish certain factual and legal positions unless proven otherwise or contradicted or retracted. Thus ‘retraction’ is a significant tool in the hands of the assessee for correction of any wrong statement given.

|

Meaning of the term Statement, Admission & Retraction:

These terms are not prescribed under any of the taxing statutes stated above nor under the General Clauses Act, 1897. So to understand their meaning resort has to be made to the common parlance meaning or dictionary meaning only.

|

‘Statement’ means something to be stated. A statement is something that you say or write which gives information in a formal or definite way.

|

‘Admission’ means voluntarily acknowledgement of the existence or truth of a particular fact. Section 15-21 of The Bhartiya Sakshya Adhiniyam, 2023 (47 of 2023) (Corresponding provisions of Section 17-23 of erstwhile Indian Evidence Act, 1872) deals with Admission. But under the Bhartiya Sakshya Adhiniyam, 2023 ‘admission’ is defined in a narrower sense. According to section 15 of The Bhartiya Sakshya Adhiniyam, 2023, an admission is a statement oral or documentary or contained in electronic form which suggests an inference to any fact in issue or relevant fact.

|

‘Retraction’ means a request, offer, or statement to be withdrawn. It means to take back something previously stated. Thus the act of taking back an offer or statement, or admitting that a statement was false can be called as ‘retraction’. In legal sense retraction is used to describe an action in which an earlier action or statement is reversed, with the intent of restoring the original situation.

|

Reasons and need for Retraction:

In general, the key reasons or the need for retraction of the statement is felt necessary under the following circumstances:

|

- In case of incorrect or untrue statement made.

- Statement under misunderstanding of facts or misconception.

- Statement made involuntarily under pressure, threat, or coercion.

- Statement based on incomplete records or documents available.

- Statement given at odd hours and under mental stress or duress.

Once a retraction is made the burden is squarely shifted on the person who alleges that the statement was not made voluntarily to prove that it was involuntarily made or made under coercion or undue influence or that it was made under mistaken belief or was obtained by fraud or misrepresentation. The mere allegation will not suffice. The person seeking to retract has to prove by leading cogent and reliable evidence, the incorrect nature of the facts stated or confessed at the earliest possible opportunity.

|

Legality & Validity of Retraction:

Retraction may be considered as a remedy available to the person who wants to withdraw or correct mistaken statements made in a proceeding. Even if an admission is made in a statement, the same cannot be held to be conclusive in every case especially when the taxpayer or any other person whose statement has been recorded seeks to retract it and shows some honest and cogent reason. In Satinder Kumar (HUF) v. CIT 106 ITR 64(SC) it was held that:

|

“It is true that an admission made by an assessee constitutes a relevant piece of evidence but if the assessee contends that in making the admission he had proceeded on a mistaken understanding or on misconception of facts or on untrue facts such an admission cannot be relied upon without first considering the aforesaid contention”

|

Article 20(3) of the Constitution of India ensures that no person accused of an offense shall be compelled to be a witness against themselves. This means that an individual cannot be forced to provide evidence or testimony that may incriminate themselves. It is important to note, especially in the context of taxation laws, that statements recorded during a summons appearance, or a search proceeding are relevant only for the purpose of levy of duty or tax (which are civil proceedings by nature), and not to affix criminal liability.

|

Retraction is often viewed seriously by the tax department and there is always a tendency to negate such retractions. The retracted statement does not become null and void perse, but its validity is subject to further legal scrutiny. The tax department may seek cross-examination of the person who retracts his/her statement. So retraction is not so easy and there are challenges in the retractions.

|

Time Limit for Retraction:

There is no specific time frame prescribed under the law for the retraction. But to be fair and reasonable retraction should be planned as soon as possible and immediately after a statement is recorded. Inordinate delay in retracting the statements will create unnecessary doubts and presumption of afterthoughts is often taken by the tax department. It is a settled law that the retraction of a statement made after a lapse of ample time loses its significance and is viewed otherwise by the tax department.

|

In taxation matters, mostly the recorded statement is supplied by the tax department along with the final show cause notice or assessment order, etc. By this time a considerable time is elapsed. Further due to limited human memory, it is also sometimes not possible to remember each and every word of the recorded statement and apply for retraction. So in such cases, early retraction is generally not possible. So what is the way out to retract? The author feels that in such cases the assessee/concerned person should demand a copy of his statement from the tax department immediately after his/her statement is recorded. If it is supplied by the tax department, then retraction can be done based on it immediately. If it is not supplied and provided only at a later point, then retraction can be done as and when the copy of the statements is provided referring to the petition filed demanding copy of the statements recorded. This will be helpful in establishing the fact that the assessee was eager to correct his original statement recorded and also demanded a copy thereof but it is only due to non-supply/belated supply of the statements the assessee was precluded from retracting earlier.

|

Retraction by whom?

Retraction can be done only by the person who made the admission. No other person, including the legal representative of that person can retract the admission made by him. In case of Pullangode Rubber Produce Co., Limited V. State of Kerala- 1971 -TMI - 39985 - Supreme Court the Honorable Supreme Court held that an admission is extremely important piece of evidence but it cannot be said that it is conclusive. It is open to the person who made the admission to show that it is incorrect.

|

In case of Commissioner of Income Tax V. H.R. Basavaraj (late) by his legal representative-(2011) 339 ITR 63 (Karn) it was held that the admissions made cannot be retracted by the legal representatives of the person who made the admission. In this case the admissions made by the late Shri H.R. Basavaraj, cannot be retracted by the legal representatives on the various grounds that are sought to be urged. In view of the admissions made, the same become binding. It also binds legal representatives. Even though the admissions are sought to be retracted not by the person who made it but, by the legal representatives, it would still amount to an admission and would bind the legal representatives.

|

The Bombay High Court in the case of T. Lakhamshi Ladha & Co. v CIT 386 ITR 245 (Bom), held that in case there is a statement by a senior partner of anassessee firm, statement cannot be retracted by another partner of that firm in absence of any allegation of pressure and coercion by the department and there being no evidence to prove that original statement was incorrect.

|

Procedure for Retraction:

No specific mode and manner of retraction has been prescribed under the law. Based on the past judicial precedents the author has framed some points which are helpful in understanding the procedure of retraction.

|

- Retraction should be done only by the person whose statement was recorded.

- Retraction should be planned soon after the statement was recorded. Where retraction of statement recorded under section 132(4) and later confirmed in the statement recorded under section 131 had been made by the assessee after almost eight months, same was to be discarded. Retraction of a statement after a sufficiently long gap or point of time loses its significance and is an afterthought. Hence SLP filed by the assessee against the impugned order of the High Court was to be dismissed as the views of High Court were agreeable, and no case was made out to interfere with the impugned order. [Roshan Lal Sanchiti v. Principal Commissioner of Income-tax 150 taxmann.com 228 (SC)]

- Reasons for retraction are very important and of paramount importance. So the same should be clear, unambiguous, and explicitly supported by strong evidence. It has been observed by the Supreme Court in K.T.M.S. Mohd v. UOI - AIR 1992 SC 1831 that it is only for the maker of the statement who alleges inducement coercion, threat, etc., to establish that force was adopted which burden has not been discharged by the appellant for want of evidence.

- Retraction should be made in writing preferably through an Affidavit along with supporting evidence, if any. The entire matter should be explained in a detailed manner evidencing the facts and circumstances warranted for retraction negating the earlier statements made. An affidavit carries strong evidentiary value in a proceeding. An affidavit has to be considered as a piece of evidence. The importance and relevance of the averments made in the affidavit cannot be brushed aside without really having any material to contradict the same. It is a matter of common knowledge that even in Courts the affidavits are furnished and relied upon. Where pursuant to the search conducted at assessee's premises, his statement was recorded under section 132(4), however later assessee retracted the statement, but, had not adduced any evidence to substantiate his allegations to retract from his statements under section 132(4), the retraction was to be ignored and additions based on a statement originally recorded were justified. [ Kerala High Court in case of Nayyar Patel vs. Assistant Commissioner of Income-tax, (Inv) 137 taxmann.com 149 (Kerala)]

- Additional affidavit of the witnesses present during the recording of the statement may also be filed. This will strengthen the position of the assessee.

- An incorrect or false affidavit is a criminal offense. The Hon’ble Apex Court in the case of BabanSingh vs. Jagdish Singh AIR 1967 SC 68 held that where a false affidavit is sworn, the offense would fall u/s 191and 192 of the Indian Penal Code 1860 (now it would fall under sections 227& 228 of The Bhartiya Nyaya Sanhita,2023).

- Retraction should be made first before the authority who recorded the original statements instead of directly before the Court of law. In the case of Sidhharth Shankar Roy v. Commissioner of Customs, Mumbai 2013 (291) ELT 244 (Tri.) (Mumbai) (Order dated 30-8-2011), it was held that retraction of a confessional statement should be addressed to the same officer to whom the confessional statement was given u/s 108 of the Customs Act. In this case, the retraction was made before the Judicial Magistrate and not before the concerned officer of Customs (AIU).

- The authority before whom the retraction is made is empowered to cross-examine the person or witnesses who made the retraction. If no cross-examination is done by the authority, then the retracted statement becomes unchallengeable. Hon’ble Supreme Court in the case of Mehta Parikh & Co. vs.CIT 30 ITR 181 (SC) held that it would not be open to the revenue to challenge the statements made by the deponent in their affidavits later on if no cross-examination regarding the statements made in affidavits is done.

- A copy of the retracted statement should also be submitted to the higher authorities to establish the fact that the statement was recorded involuntarily and retraction is being filed by the assessee before the investigating authority.

- Once a statement is retracted the burden is on the department to disprove the retraction. The Hon’ble High Court of Delhi while relying upon Vinod Solanki’s SC case in the matter of DRI Vs. Mahendera Kumar Singhal 2016 (333) ELT (250) (Del.) held that the burden is on the department to show that the retraction made by the maker is the statement is not valid. The same principle was reiterated in the matter of Rakesh Kumar Garg Vs. CCE, 2016(331) ELT 321 (Del.)

- The legal position regarding admissibility of the retracted statement is well settled. Firstly, it loses its weight if it is retracted and secondly, it cannot be the sole basis of confirmation of duty demand or the prosecution of the accused. The statement recorded during the investigation if retracted then has to be corroborated by other independent sources and if not the same cannot be relied upon in judicial proceedings.

- The Hon’ble Madras High Court in case of Commissioner of Income-tax v. MAC Public Charitable Trust 144 taxmann.com 54 (Madras) has discussed the aspect of retraction as under:

61. In view of the law discussed above, it must be held that statement recorded under section 132(4) of the Act and later, confirmed in statement recorded under section 131 of the Act, cannot be discarded simply by observing that the assessees have retracted the same, because such retraction ought to have been generally made within a reasonable time or by filing complaint to superior authorities or otherwise brought to notice of the higher officials by filing duly sworn affidavit or statement supported by convincing evidence. Such a statement when recorded at two stages cannot be discarded summarily in cryptic manner by observing that the assessees in the belatedly filed affidavit have retracted from their statements. Such retraction is required to be made as soon as possible or immediately after the statement of the assessees was recorded. Duration of time when such retraction was made, assumes significance and in the present case, retraction has been made by the assessees after eight months to be precise, 237 days.

|

62. It is settled position of law that the admission though important is not conclusive. It is open to the assessee who made the admission to show that it is incorrect as held by the Hon'ble Supreme Court in Pullangode Rubber Produce Co. Ltd. v. State of Kerala 91 ITR 18. The onus falls on the person who had earlier admitted to prove it wrong. Therefore, the statements could form the basis of assessment.

|

63. The statements given to the Assessing officer under section 132 (4) have legal force. Unless the retractions are made within a short span of time, supported by affidavit swearing that the contents are incorrect and it was obtained under force, coercion and by lodging a complaint with higher officials, the same cannot be treated as retracted. This position laid down in catena of decisions by the various High Courts in Lekh Raj Dhunna (supra), Bachittar Singh (supra), Rameshchandra & Co. v. CIT 35 Taxman 153/168 ITR 375 (Bom.), Dr. S.C. Gupta (supra), CIT v. Hotel Meriya 195 Taxman 459/ 332 ITR 537 (Ker.), O. Abdul Razak (supra).

|

13. The Hon’ble Kolkata CESTAT in case of Super Forgings & Steel Ltd. v. Commissioner of Central Excise 161 taxmann.com 284 (Kolkata - CESTAT) held that in respect of clandestine removal, statement of Commercial Manager of Factory which was heavily relied on by Revenue was retracted subsequently and Revenue authorities failed to discharge burden of proving serious charge of clandestine clearance; demand was not sustainable.

|

Similar view was taken by Mumbai CESTAT in case of Narshinha Alloys (P.) Ltd. v. Commissioner of Central Excise and Service Tax 161 taxmann.com 59 (Mumbai - CESTAT). Confessional statement subsequently retracted without any recovery of unaccounted goods cannot be used to substantiate allegation of clandestine removal of goods.

|

14. Once alleged statement made by assessee was retracted on next day itself with allegations of force and duress, onus to prove that said statement was voluntary shifted upon department and in absence of any such proof from department, confessional statement is not evidence to levy penalty. [Vinod Kumar Sahadev v. Union of India 49 taxmann.com 380 (Delhi)]

|

Conclusion:

Retraction is an important aspect of any proceedings. In genuine and honest cases retraction acts as a savior. So the right of retraction should be exercised with proper care and due diligence. There should not be any casual approach while retracting a statement. It should be well grounded, reasoned, and supported by clinching evidence to prove that what was recorded earlier was incorrect and under misbelief. Retraction without proper reason and supporting evidence will prove fatal to the proceedings. Hence it is advisable to exercise the retraction option in exceptional circumstances and under the proper guidance of a legal expert.

|

Disclaimer: The above views are compiled by the author based on the study of various Court cases, judicial pronouncements etc. There may some other views also on this subject matter. So, the readers are requested to refer to relevant provisions of the statute, latest judicial pronouncements, circulars, clarifications, etc. of the respective law and obtain legal opinion before acting on the above write up. The author is a practicing Chartered Accountant at Guwahati and can be reached at: manoj_nahata2003@yahoo.co.in.

|

|

|

|

|

|

The ongoing protests over legalising the Minimum Support Price (MSP) have brought attention to the challenge of determining a fair price for farmers’ produce.

|

While the government currently provides MSP for 23 crops, the remuneration is not enough to make farming profitable.

|

Agriculture and market experts suggest that the Commission for Agricultural Costs and Prices (CACP) must rethink how it measures the cost of agricultural produce in order to ensure a fair price to farmers without worsening the already rising food inflation. They also emphasise the need to align MSP with the country's macroeconomic goals and climate variations.

|

Anil Sharma, former chairperson, Institute of Cost Accountants of India, Kolkata told Down To Earth (DTE) that MSP should include all farming costs. Below is a summary of what he told DTE:

|

While calculating MSP for different crops, CACP considers only A2 and FL costs. Costs of capital, lease rent for own land, own machinery and post-harvesting costs are ignored. In his 2004-06 reports, M S Swaminathan recommended a comprehensive cost (C2) structure, which includes all costs, to determine MSP for different crops. However, for various reasons, costs other than A2 and FL continue to be overlooked.

|

In contrast, when calculating the costs of products manufactured in industry, all types of costs are considered to determine the actual cost of production. Even the notional value of items available at no cost is included in the total cost. In industry, accrual-based accounting is practiced, where expenses or costs, even if not paid at the time, are added to the total cost of a product. Decision-making processes in the industry also consider opportunity costs to reach final conclusions.

|

Indian accounting standards (Ind AS), cost accounting standards and Cost Records Rules-2014 under the Companies Act 2013 and Income Tax Act 1961 prescribe methodologies for recording business transactions to ensure accountability and transparency while determining the actual cost and margin for manufactured or traded products. These standards also help in determining the tax liability of businesses.

|

As India progresses towards a US $10 trillion economy, it is time to treat agriculture as a complete business proposition and adopt a formal costing and accounting mechanism. This would ensure greater transparency in determining MSP and calculating the actual costs and margins of agricultural produce.

|

To accurately calculate the cost of agricultural produce, A2, FL, and all other incurred costs must be considered. An indicative list of such costs includes: seeds, fertiliser, pesticides, etc, irrigation, labour, fuel, electricity, hired machinery, land rent, interest on own capital, rental value for land, farm equipment and other consumables, depreciation on machinery and other assets, repair and maintenance of machinery, insurance of crops and farm equipment, packing material, treatment of residues such as husk, stubble, taxes, transportation, storage, and stacking and restacking, commissions to agents, and others.

|

By recording all these, we can determine the per-hectare or per-quintal cost of produce and per-quintal cost of quantity sold. Additionally, factors related to the environment, seasonality, supply and demand, nutritional values, natural calamities, irrigation systems, soil conditions, infrastructure and subsidies should also be considered.

|

The ultimate objective of any business and trade is to achieve reasonable returns on invested money for a respectable livelihood.

|

|

|

|

|

|

4. Lawgics by Ms.Nidhi Aggarwal

|

Ms. Nidhi Aggarwal is delighted to present judgment with a great vision to spread complex GST law in a simple manner amongst the taxpayers, tax professionals, students and knowledge seeker.

|

|

Recently added notes are listed below:

|

|

|

|

|

|

Synopsis: The Delhi High Court dismissed the writ petition involving fraudulent ITC claims, directing the petitioner to pursue appellate remedy u/s 107 of the CGST Act.

|

Caste name: Banson Enterprises & Anr. vs Assistant Commissioner CGST & Ors.

|

Citation: W.P. (C) 6503/2025 dated 15.05.2025

|

Authority: Delhi High Court

|

The petition challenges the Order-in-Original dated 02.02.2025 based on a Show Cause Notice (SCN) dated 03.08.2024 A search was conducted, and statements were recorded including that of one Director admitting to the issuance of fake invoices during the Central Excise period. It was alleged that the Petitioner issued goods-less invoices to enable fraudulent Input Tax Credit (ITC) claims amounting to Rs. 1.85 crore.

|

Contentions of the Petitioner:

|

SCN was issued by unauthorized officer, thus, violates Rule 142(1)(a) of CGST Rules. No pre-consultation as required under Rule 142(1A) of CGST Rules was issued. Consolidated SCN for multiple financial years was issued and challenge to such consolidated action is pending in a separate matter (Quest Infotech case).

|

Contentions of the Department:

The impugned order is appealable, hence writ is not maintainable. The Petitioner’s Director admitted to allegations. Natural justice was followed as the Petitioner received the SCN, filed a reply, and availed of personal hearing. Reliance must be made on SC judgments and Allahabad HC rulings emphasizing alternate remedy u/s 107 CGST Act.

|

Findings and Decision of the Court:

The Court refused to interfere under writ jurisdiction, citing:

|

- No breach of fundamental rights or principles of natural justice.

- Availability of a statutory remedy (appeal) under Section 107 CGST Act.

The Court noted that the Allegations involve serious misuse of ITC, requiring fact-based adjudication, not suited for writ jurisdiction. Thus, the Petitioner was granted liberty to file appeal, and if filed with pre deposit, the appeal shall not be dismissed on limitation.

|

|

|

|

|

|

|

|

Synopsis: GST RC cancellation is not justified as petitioner was not given fair opportunity to respond.

|

Case Name: M/s. Genius Orthos Industries VS Union of India & Ors.

|

Citation: WRIT TAX No. 542 of 2023 dated 24.04.2025

|

Authority: Allahabad High Court

|

The petitioner was engaged in the business of surgical goods and its GST registration was cancelled on 19.12.2022 after a physical verification of its premises allegedly found no inputs, finished goods, or workers. A show cause notice was issued prior to cancellation, but the petitioner claimed they were not informed of the specific material findings leading to the cancellation. The appeal against the cancellation was also dismissed.

|

Contentions of the Petitioner:

|

The principles of natural justice were violated, as no proper notice of the specific material against them was given. Cancellation was based on vague grounds, and the watchman at the premises had confirmed that business activities were conducted, albeit irregularly. Rule 25 of the CGST Rules and Form GST REG 30 was not referenced in actual SCN.

|

Contentions of the Department:

|

The petitioner had due knowledge of the discrepancies found during physical verification and failed to provide a satisfactory explanation. Claimed that the cancellation order was justified due to absence of business activity at the registered premises.

|

Findings and Decision of the Court:

|

The High Court found that the cancellation was done without due process, especially considering that:

|

- The material used for cancellation was never properly shared with the petitioner.

- The statement of the watchman indicating occasional business activity was ignored.

- The physical verification report (GST REG-30) was not referenced in the show cause notice.

Thus, impugned cancellation and appellate orders were quashed and the matter was remanded to the proper authority for fresh adjudication within three months, ensuring that a reasoned and speaking order is passed after an Opportunity of hearing is granted. The petitioner may submit relevant evidence.

|

|

|

|

|

|

|

|

Synopsis: Rejection of appeal on ground that appeal was not filed electronically under Rule 108 of CGST Rules, 2017 is invalid in case of non availability of order–in–original on GST portal and Appeal being filed manually.

|

Case Name: M/s Appolo Sesame Industries & Anr. VS Assistant Commissioner of CGST, Division X, Nadiad & Ors

|

Citation: R/Special Civil Application No. 571 of 2025 dated 24.04.2025

|

Authority: Gujarat High Court

|

The petitioners challenged the rejection of their appeal against an Order-in-Original dated 30.10.2023. They had filed the appeal manually in Form GST APL-01, as the order was not available on the GST portal, making electronic filing impossible. Despite this, the Appellate Authority rejected the appeal on 27.09.2024, stating it was not filed electronically, as required under Rule 108(1) of the CGST Rules, 2017.

|

Contentions of the Petitioner:

|

The order-in-original was not available on the portal, so manual filing was the only viable option. A pre-deposit of 10% of the disputed dues was paid. The Appellate Authority ignored the proviso to Rule 108(1), which allows manual filing if the order is unavailable electronically. The Appellate Authority failed to issue the mandatory provisional acknowledgment, despite receiving the appeal.

|

Contentions of the Department:

|

The appeal was filed offline without fulfilling electronic filing requirements. The Appellate Authority argued that procedural rules were not followed, hence the rejection was valid.

|

Findings and Decision of the Court:

|

The High Court found that the Appellate Authority failed to apply its mind to the facts. It held that the rejection of the appeal violated Rule 108(1) of the CGST Rules, as manual filing is permitted when the order is not available on the portal. The impugned rejection order was set aside and the matter was remanded to the Appellate Authority to hear and decide the appeal on merits.

|

|

|

|

|

|

|

|

Synopsis: The demand order was quashed on the ground that the hearing notices must not be merely uploaded on portal but also e-mailed to petitioner.

|

Case Name: Shri Krishna Sales VS Commissioner of Delhi Goods and Service Tax & Ors.

|

Citation: W.P. (C) 5524/2025 dated 29th April, 2025

|

Authority: Delhi High Court

|

Brief facts of the case:

The petitioner challenged the Show Cause Notice (SCN) dated 26.09.2023 and demand order dated 25.12.2023, issued by the Delhi GST authorities. The challenge also extended to Notification No. 09/2023 Central Tax dated 31.03.2023, which extended the time limits for adjudication under Section 73 of the CGST Act. The SCN was only uploaded under the "Additional Notices and Orders" tab on the GST portal and did not come to the petitioner’s notice. The petitioner filed a rectification application, which was considered time-barred.

|

Contentions of the Petitioner:

The SCN and subsequent hearing notices were not properly served, being uploaded in a location on the portal that made them easy to miss. The notification extending limitation was issued improperly under Section 168A without valid GST Council approval and is under challenge before the Supreme Court (SLP No. 4240/2025).The demand order was passed ex parte without giving a fair opportunity to respond.

|

Contentions of the Department:

The SCN was uploaded properly as per current GST portal functionality. The notification extending time limits is valid and backed by GST Council recommendation (in some cases), with related petitions already under consideration in the Supreme Court. The petitioner’s application for rectification was rightly rejected due to limitation bar.

|

Findings and Decision of the Court:

The demand order dated 25.12.2023 was set aside. The Court allowed the petitioner to file a reply to the SCN within 30 days. The hearing notice must be communicated not just through the portal but also via email. The adjudication order shall be passed afresh, after granting a personal hearing. The outcome of this case will be subject to the final decision of the Supreme Court in the pending SLP on the validity of the notifications.

|

|

|

|

|

|

|

|

Synopsis: Notification dated 11.03.2022 & 25.11.2024 confers power to Principal Commissioner Delhi North and Delhi West to issue notices under Section 73 & 74 of CGST Act, 2017.

|

The petitioner challenged a Show Cause Notice (SCN) dated 24.07.2024 and Order-in-Original dated 02.02.2025, issued for alleged fraudulent availment of Input Tax Credit (ITC) through fictitious and non existent firms. The case was based on an extensive investigation involving over 87 entities, and a criminal complaint was also filed under Section 132(1)(b) of the CGST Act, 2017. The petitioner participated in the proceedings and submitted a reply to the SCN but later objected to the jurisdiction of the adjudicating authority.

|

Contentions of the Petitioner:

The personal hearing was improper, and the order was passed without following due process. The authority that adjudicated the matter (CGST Commissionerate Delhi North) lacked jurisdiction. The correct authority was claimed to be CGST Delhi West. A Corrigendum, issued on 28.01.2025 (after the hearing), was alleged to be backdated and manipulated to rectify the jurisdiction issue.

|

Contentions of the Department:

|

The department cited two notifications: Notification dated 11.03.2022 granted jurisdiction to Principal Commissioner, Delhi North and Notification dated 25.11.2024 extended jurisdiction to both Delhi North and Delhi West. The department argued that the adjudicating authority had valid jurisdiction and that due opportunity of hearing was provided to the petitioner. Petitioner’s challenge to jurisdiction was unfounded, and their remedy lies in filing an appeal under Section 107 of the CGST Act.

|

Findings and Decision of the Court:

The High Court held that jurisdiction was validly established via the cited notifications. The petitioner was directed to file an appeal before the Appellate Authority under Section 107. The court clarified that if the appeal is filed within 30 days, along with mandatory pre-deposit, it shall not be dismissed on limitation grounds and shall be heard on merits.

|

|

|

|

|

|

5. GST Notes by CMA Anil Sharma

|

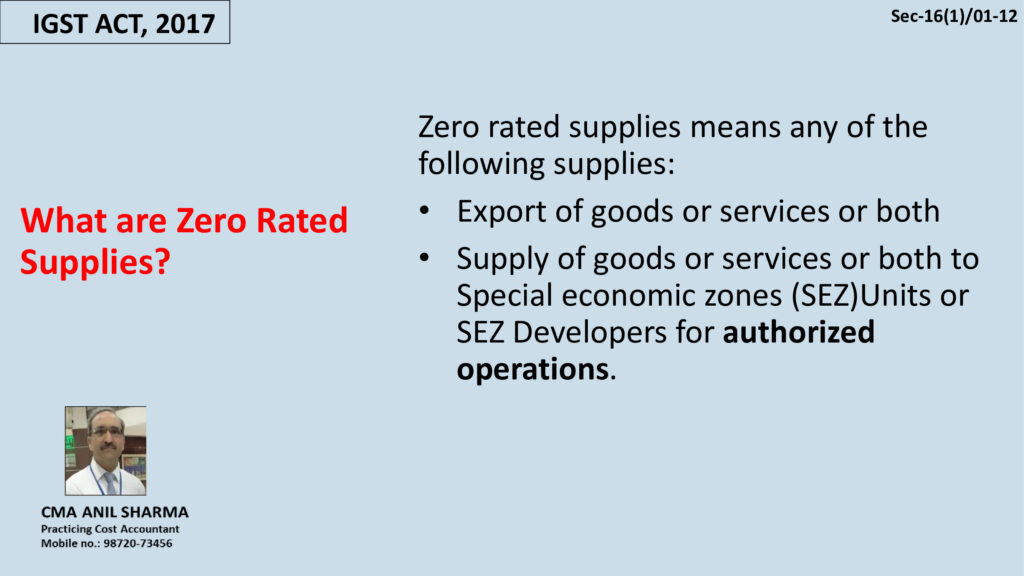

1) Chapter-7 of IGST Act containing 12 slides is added in the Notes section'. It covers POS for inter state transactions including export.

|

Authored by CMA Anil Sharma Sir, with a vision to simply the complex GST Law for taxpayer, professional, taxmen etc.

|

|

|

|

|

|

|

|

|

6. GST Daily by CA Pradeep Modi

CA Pradeep Modi is presenting judgment analysis under title 'GST Daily - Stay yourself updated'

|

|

|

|

|

|

THE HON'BLE ALLAHABAD HIGH COURT IN THE CASE OF Vibhuti Tyres V/s State of U.P., decided on 7-5-2025

|

✔️ Is it justified that GST order with higher demand than show-cause notice?

|

👉 The Hon'ble High Court Judgement:-

|

✔️ Where in show-cause notice amount representing tax, interest and penalty was indicated as Rs. 8,81,080, but in order, much higher demand was raised at Rs. 32,97,336, same was in violation of section 75(7); matter was to be remanded back.

|

Section 75 of Central Goods and Services Tax Act, 2017

|

|

|

|

|

|

|

|

THE HON'BLE JHARKHAND HIGH COURT IN THE CASE OF Sadanand Prasad Barnwal V/s State of Jharkhand, decided on 8-5-2025

|

✔️ Is it valid if SCN and order under section 73 for lack of digital signature of issuing authority?

|

👉 The Hon'ble High Court Judgement:-

|

✔️ Where both summary of SCN in Form GST DRC-01 and order under section 73 did not bear digital signature of concerned authority, both SCN and order were to be quashed.

|

Section 161, read with section 73 of Central Goods and Services Tax Act, 2017

|

|

|

|

|

|

|

|

THE HON'BLE CALCUTTA HIGH COURT IN THE CASE OF Edelweiss Rural & corporate Services Ltd. V/s Deputy Commissioner of Revenue, decided on 5-5-2025

|

✔️ What would be Refund if business stood closed and registration was cancelled?

|

👉 The Hon'ble High Court Judgement:-

|

✔️ Where Refund sanction order had itself observed that assessees business was closed down, its registration was cancelled and it had no tax dues refund claim was already allowed, direction to credit refund amount to credit ledger instead of bank account of assessee was self-contradictory since there was no business for assessee to take benefit of refund credited to assessees credit ledger.

|

Section 54 of Central Goods and Services Tax Act, 2017

|

|

|

|

|

|

|

|

THE HON'BLE JHARKHAND HIGH COURT IN THE CASE OF Sri Ram Stone Works V/s State of Jharkhand, decided on 9-5-2025

|

✔️ Can GST Notice would be issued under Section 61 of CGST Act merely on the basis of difference between sale price and market price?

|

👉 TheHon'ble High Court Judgement:- ✔️ Clear objective of section 61 is to enable an Assessing Officer to point out discrepancies and errors which are occurring in return filed by a registered person with that of related particulars; notice under section 61 cannot be issued comparing particulars at which assessee has sold its goods with that of prevalent market price.

|

|

|

|

|

|

7. PPT/Handbook on GST

|

|

|

|

8. GST/Income Tax in Media

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Hope the above updates is of use to you. Please share your input and feedback at taxupdate.otu@gmail.com

|

|

|

|

|

|

|

|

|

Visit our website

|

OTU provides you

|

- Articles on various topics

|

|

- Media - GST, Income Tax & Press R.

|

|

|

|

|