|

onlinetaxupdate team wish to express sincere thanks to all the readers, authors, subscribers for the support extended to us. Please share your feedback at

|

taxupdate.otu@gmail.com or 7738647904

|

Newsletter 143 dated 11.11.2024

|

|

|

|

|

|

|

|

|

Dear Reader,

|

Please find newsletter for your reading and reference.

|

|

Index of the Newsletter

- Recent updates

- Portal updates

- Article

- Lawgics by Ms.Nidhi Aggarwal

- GST Notes by CMA Anil Sharma

- GST Daily by CA Pradeep Modi

- PPT/Handbook

- GST/IT/Customs in media

|

|

|

|

|

|

|

CBIC issued Notification No. 58/2026-Customs (N.T.) dated 22.06.2026 to hereby appoint the officer to exercise the powers and discharge the duties conferred on the officers for the purpose of adjudication of the show cause notices.

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Notification no. 12/2026-Customs (ADD) dated 19.06.2026 Seeking to continue anti-dumping duty on imports of Polyethylene Terephthalate resin having an intrinsic viscosity of 0.72 decilitres per gram or higher originating in or exported from China for a period of 5 years

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Circular no. 28/2026-Customs dated 15.06.2026 regarding testing of samples of export consignments

|

|

|

|

|

|

Press release ID 2279424 dated 30.06.26

|

The Government had earlier provided a full Customs Duty exemption on imports of critical petrochemical products till 30th June 2026, as a temporary and targeted relief in view of the conflict in West Asia and the consequent disruptions in global supply chains.

|

The exemption was provided to ensure sufficient availability of petrochemicals in the domestic market as Indian petroleum companies had been asked to concentrate on the production of LPG during this period. As the situation is gradually normalizing, to ensure a smooth and non-disruptive transition for the affected sectors, it has been decided to extend the said exemption by a further period of 15 days, that is, till 15th July 2026.The list of products covered remains the same as notified earlier.

|

The Government remains committed to supporting India's manufacturing sector. As before, the exemption is expected to benefit a wide range of sectors dependent on petrochemical feedstock and intermediates, including plastics, packaging, textiles, pharmaceuticals, chemicals, automotive components and other manufacturing segments. This will also provide relief to consumers of final products.

|

Link to previous press note issued:

|

|

|

|

|

|

|

|

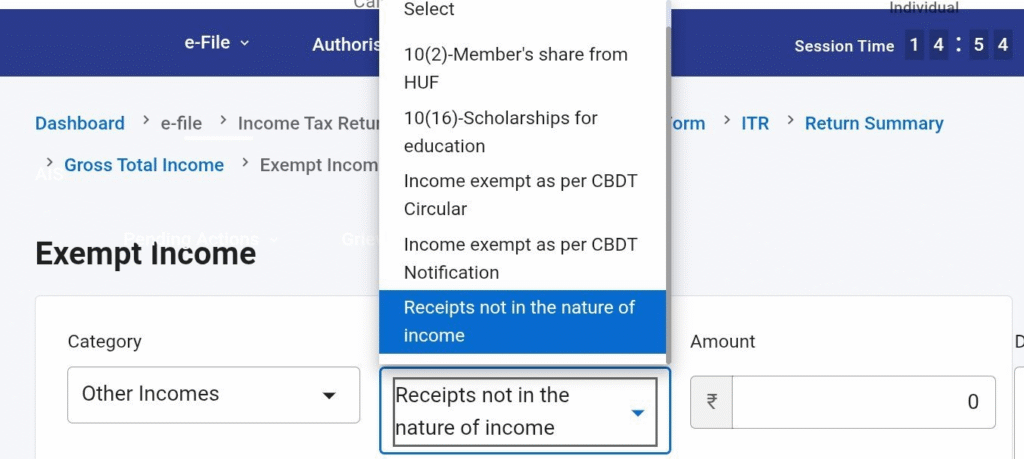

From AY 2026-27, the option to report 'Other Exempt Income' was removed.

|

Earlier, this was useful in situations such as:

|

- Sale of rural agricultural land/ Reporting of Gifts from Relatives - although disclosure was not required as same is not income .

|

The column of 'Other Income' under Exempt incomes has now been added.

|

|

|

|

|

|

|

|

|

|

|

Before applying for Income Tax registration, GST registration, ICEGATE, or DSC mapping, you can use the TRACES PAN Verification facility to check whether the name in the PAN database is correctly aligned with the PAN number.

|

Helps identify name mismatches in advance and avoid registration issues.

|

|

|

|

|

|

GSTN Advisory no. 666 dated 01.07.2026

|

It is informed that the Aggregate Annual Turnover (AATO) functionality is currently being upgraded to enable automatic updation of AATO as subsequent returns are filed post amendment window. As this enhanced functionality is being deployed from 1st July 2026, the window for amendment of AATO by taxpayers for FY 2025-26 has been revised on the GST Portal.

|

GSTN had earlier issued an advisory dated 02 May 2022 regarding the functionality for amendment of Aggregate Annual Turnover (AATO) on the GST Portal, which was applicable for AATO till FY 2024-25. Under the said advisory, taxpayers were provided the facility to amend their turnover during the month of May.

|

In continuation thereof, it is informed that the timelines for submission of amendment applications and verification of amended AATO details by Tax Officers, in respect of FY 2025-26, have been revised.

|

To ensure greater consistency, accuracy, and uniformity in the reporting of AATO across various modules of the GST Portal, certain system-level enhancements are being implemented. Consequently, the revised timelines for amendment of AATO for FY 2025-26 by the taxpayers and subsequent action by the tax officers are as under:

|

AATO Amendment Application window for FY 2025-26

01 July to 31 July 2026

|

Review by jurisdictional Tax officer

01 Aug to 15 Aug 2026

|

Accordingly, the facility for amendment of AATO, which was earlier available during May as per the previous advisory, shall now be made available from 01 July to 31 July 2026 for FY 2025-26. The amended AATO details will be available for review of Tax Officers from 01 Aug to 15 Aug.

|

All taxpayers are requested to take note of the revised timelines and carefully review the AATO details while submitting the amendment application and ensuring that the amended details are accurate before submission.

|

In case of any difficulty or concern, taxpayers are advised to raise a grievance through the Self-Service Portal available on the GST Portal, along with all relevant details, to facilitate prompt and effective resolution.

|

|

|

|

|

|

|

|

GSTN Advisory no. 665 dated 01.07.2026

|

Gross and Net GST revenue collections for the month of June, 2026

|

|

|

|

|

|

|

|

As per section 34 of CGST Act, 2017, any changes in the outward supply liability can be done in the return to be filed in the month of November. The return filed in November pertains to the period October. Thus, any credit note issued against invoices pertaining to FY 2023-24 can be corrected in the October 2024 month return viz. GSTR-1/3B.

|

GST Liability

- Outward GST Liability as per books to reconcile with liability furnished in GSTR-1/3B and if any liability is missed out to be reported in the return then the same has to be furnished in October month return.

- On the flip side if any outward GST Liability furnished in GSTR-1/3B but missed out to be accounted in books then the same has to be accounted in books.

- Compare the GST liability in GSTR-1 and GTR-3B and identify the difference, if any and pass necessary entry in books or if any liability not furnished in return then furnish the same. Or if the difference is genuine then keep reconciliation.

- Analyse the transaction recorded in ‘Miscellaneous Income’ at P&L credit side. If any GST liability is not accounted then account it in books and also consider in October month return.

- If there is no liability on transaction at above point 4 then keep proper write up or your stand as to why liability is not payable for future audit purpose. For e.g. liquidated damage recovered from your supplier.

- Any liability paid in GSTR-1/3B but missed to record the payment entry or utilisation entry in books then account the same.

- If any short payment or excess payment was done like 5% GST paid instead of 12% or vice-versa then account/reverse the difference in books. Also arrange to deposit or adjust in the October month return.

- Any capital asset sold but GST is not accounted then analyse whether GST is applicable or not. If applicable then account the liability in books. If not then keep calculation as to why GST is not payable in record for future audit purpose. E.g. like sale of car.

- Transfer of capital asset like laptop, car, machine parts etc. within company but outside state units need to be offered for GST. If not offered to tax then pass necessary entry to account the liability in book and consider it in October month GST return.

- Reconcile expense accounts/ ledgers like Freight, Legal consultancy, security service, rental income, director sitting fees, import of service etc. and ensure that applicable RCM is paid. If any liability is missed to be accounted then pass necessary entry and consider in October month return

- Raise Self invoice for RCM transaction and keep it on record.

- Check if any goods sent for job work or capital asset sent for repair purpose is received within prescribed time period. If not received within timeline then create liability in books and consider payment through return.

- Ensure that Credit notes are actually issued to the customer. Also it is furnished in GSTR-1 so that the customer reverses the input tax credit claimed earlier based on underlying invoice.

- In case the customer has informed you about the discrepancy in the invoices appearing in his GSTR-2B which is a replica of the invoice uploaded by you then make necessary correction in returns.

- Send an email communication to all B2B customers alerting them to report any discrepancy in the invoice issued by you during FY 2023-24. Specifically inform that once the due date of 11th November is crossed then correction in the invoices /credit note pertaining to FY 2023-24 is not possible.

- Ensure all the liability ledgers viz. CGST Payable account, SGST payable account, IGST payable account, RCM CGST liability, RCM SGST liability, RCM IGST liability account are correct in books of account in the sense that only October month liability appear in these ledgers. If any previous period liability exists in these ledgers or unreconciled item is there then pass necessary entry and consider them in the compliance of October month return.

- Compare outward supply in GSTR-1/3B with E-way bill generated. In case you find any transaction for which e-way bill was generated but that particular transaction is not there in books of account then account it in October and consider them in October month GST compliance.

- Similarly, compare GSTR-1/3B outward supply with e-invoice details. Ideally there should not be any taxable supply which has not been reported to IRP (Invoice registration portal) and also not accounted in books. But still it can happen. So consider those missed transaction in books in the month of October.

- In case in the Cross charge the invoice on inter-company is missed to offer for tax. Consider those transaction and account GST liability on them.

- Common expenses borne by parent company for an event or conference where sister concerns employees had also attended, the cost need to be apportioned to respective company. GST is applicable on those recovery of expense from sister concerns. If GST is not accounted on the expenses then create and entry.

Input Tax Credit (ITC)

As per Section 16(4) the time limit to claim Input tax credit on invoices pertaining to FY 2023-24 is October 2024 month's return to be filed on or before 30.11.2024. According, following task need to be performed.

|

- Check the pending ITC pertaining to FY 2023-24 and in case any incorrect ITC is there in the open list then reverse that ITC by passing necessary entry in books. And, if any ITC is pending for claim then consider them while filing GSTR-3B.

- If any ITC not accounted due to invoice not found then check with concern department internally and then account the ITC.

- If the ITC is not appearing in GSTR-2B then inform the supplier to furnish it in his GSTR-1 to be filed for Oct24 on or before 11.11.2024

- Reconcile the ITC ledgers in books and the ITC claimed through GSTR-3B. Though monthly reconciliation would have been carried out by you, but for FY 2023-24 as a whole one reconciliation should be done.

- Compare the Electronic Credit Ledgers with the ITC taken through GSTR-3B. ideally the ITC balance in books should be same as the Electronic credit ledger. But still any open items is there, then reconcile it and close.

- Any ITC kept unclaimed due to doubt on its eligibility for credit then consult with advisor and take necessary action of claiming it or reversing it.

- Any reversal of ITC u/s 42 , 43 to be done for F.Y 23-24 considering turnover of fy 2023-24 then same need to be calculated to give impact in GSTR-3B.

Other liability

- Any interest paid for delay payment of GST, vide GSTR-3B, then pass necessary entry in books.

- Any penalty paid for vehicle detention case but entry not passed, account it in this October month.

- Any late fee for delay filing GST return then account necessary entry and also discharge the late fee.

Any task you think not included in the listing above kindly mention in the comment box below.

|

|

|

|

|

|

GST UPDATEZ ON 08-11-2024 by R.SRIVATSAN, IRS, NACIN, Chennai

|

The GSTN has launched a new form from 5th November 2024, GST DRC-03A, accessible on the GST portal.

|

This form allows taxpayers to adjust tax amounts already paid against specific GST demand orders.

|

For example, if you have a pending GST demand of ₹2,00,000/- and have already paid ₹50,000/- using the DRC-03 form, you can use the facilities in Form DRC-03A to adjust that ₹50,000/- against the demand, reducing your net tax liability to ₹1,50,000/-

|

The difficulties earlier was that if taxpayers did not utilize the designated payment methods to settle their dues, the GSTN system did not automatically apply those payments to outstanding tax demands.

|

However, the introduction of DRC-03A simplifies this process, enabling taxpayers to align their payments with their obligations more easily.

|

There are instances where some taxpayers have inadvertently paid amounts via

DRC-07/DRC-08/MOV-09/MOV-11/APL-04 through DRC-03 instead of using the ‘Payment towards demand’ feature on the GST portal. This has resulted in situations where payments have been made but the corresponding demands remain open in the electronic liability register.

|

The government has now addressed this with the new form, GST DRC-03A.

|

In order to access this facility,

|

Step:1

Log in to the GST portal, navigate to ‘User Services,’ and select ‘My Applications.’

|

Step:2

The GST DRC-03A form will be visible.

|

Step:3

Enter the DRC-03 form number and click ‘Search.’

|

Step:4

Once located, fill in the details linking with Demand Orders and other details.

|

Step:5

After submitting the DRC-03A form and the adjustment is completed, the updates will be automatically reflected in the taxpayer’s liability ledger.

|

There are several taxpayers who may find the DRC-03A form particularly useful.

|

1.Taxpayers who have made partial payments on any GST demand and wish to adjust those against specific orders.

|

2.Taxpayers who have made payments on an ad-hoc basis without citing a demand order and now seek to align those payments with specific orders.

|

3.Taxpayers facing unfavorable tax orders who wish to appeal to the GST tribunal and avoid recovery actions from GST officials.

|

Since the GST appellate tribunal (GSTAT) yet to be established, taxpayers who have lost appeals against tax demand orders cannot pursue further appeals in the GST tribunal.

|

In such cases, GST officials may initiate recovery for any outstanding amounts.

|

To illustrate,

if a taxpayer faces a demand of ₹1,00,000

and files an appeal, they must pre-deposit 10% of that amount.

|

If the appeal fails, recovery proceedings may commence for the remaining ₹90,000/-.

|

Filing the DRC-03A can temporarily prevent such recoveries until GSTAT issues further directives.

|

One more progressive facility. ……….

|

|

|

|

|

|

No, the Honorable Karnataka High Court in the case of Kolvekar Logistics v. Joint Commissioner of Commercial taxes (Appeals), Hubbali , quashed the orders and held that in the light of the Rule 138-A of the State Goods and Services Tax Act and Section 68 of the Central Goods and Services Tax Act and Rule 48 of the Central Goods and Services Rules, 2017 and as per Rule 48(1)(b) of the CGST, it is only the duplicate copy which is meant for transporter and the triplicate copy is meant for supplier as per clause (c). Therefore, held that the transporter is not required to carry the original tax invoice, but the law mandates him to carry the duplicate copy.

|

The Honorable Court noted that the Petitioner was penalized, and faced an additional tax demand because the original tax invoice was not carried by the transporter, only a xerox copy was presented. The Honorable Karnataka High Court relying upon the judgement of Divya Jyothi Petrochemicals Co. v. Joint Commissioner of Commercial Taxes (Appeals) , wherein it was held that rule 48 of the CGST Rules, deals with the manner of issuing the Invoice. Accordingly, the Invoice shall be prepared in triplicate in case of supply of goods. The original copy marked as such is meant for the recipient or the purchaser and therefore, the same will not be carried by the transporter. As per rule 48(1)(b) of the CGST Act, it is only the duplicate copy is meant for the transporter and the triplicate copy is for the supplier as per clause (c) of rule 48(1) of the CGST Act.

|

The Honorable Court held that the transporter is not required to carry the original tax invoice, but as per rule 48(1)(b) of the CGST Act, transporters are mandatorily required to carry the duplicate copy. Thus, the court quashed the Impugned Orders and directed the Respondent to refund the tax, and the penalty amounts paid by the Petitioner within three months.

|

Author’s Comment

“Due Process” of law demands, the exercise of specific powers conferred to the Proper officer within specific boundaries of the law. Passion to protect the interest of revenue does not authorize by-passing of the law. The Revenue Department has to understand that this kind of approach renders the “due process” laid down in the statute “Superfluous, unnecessary and nugatory”, which is impermissible in the law. Intercepting officers fueled by their past experiences are lured into passing such perverse orders. But, First Appellate authorities are expected to bear the ‘Creatures of Statute’ effect and justify their Quasi judicial role to overcome trust deficiencies with the taxpayers and to quash such orders of over passionate adjudicating authorities.

|

|

|

|

|

|

Yes, the Honorable Madras High Court in the case of Chandhrasekaran Anand v. Deputy Commissioner (ST) , allowed the writ petition filed against the order dismissing the appeal filed beyond the condonable period due to Accountant’s illness and thereby, directed the Appellant to consider the appeal filed on merits without going into the question of limitation. The Honorable Court noted that the petitioner has placed on the record evidence that an accountant engaged to handle GST matters was hospitalized during the relevant period evident from the discharge summary submitted. There is a delay of 25 days beyond the condonable period. In the facts and circumstances outlined above, the interest of justice warrants that the petitioner's appeal be received and disposed of on merits.

|

Author’s Comments

If the appeal is filed after the period of condonation permitted in Section 107(4) (3+1 months), the Appellate authority does not have statutory authority to condone the delay, not even if the reasons are ample and deserve to be entertained. The appeal must be dismissed for being fatally belated because the Legislature has allowed Appellate authority this much authority and not more.

|

The Honorable Supreme Court has decided in Singh Enterprises v. CCE 2008 (221) ELT 163 that where the period of limitation is specifically provided in the statute, admitting appeals albeit for ‘sufficient cause’ would render statutory provisions impossible. And Appellate Authority thus being the denuded of authority to condone (due to lapse of maximum time permitted) is barred from examining the cause and condone the delays even for a “good and sufficient” reason.

|

The Honorable Allahabad High Court in the case of M/s. Yadav Steels v. Additional Commissioner and Anr. and in the case of M/s. Abhishek Trading Corporation. Commissioner (Appeals) and Anr. has decided that the Central Goods and Services Tax Act, 2017 is a special statute and a self-contained code in itself and section 5 of the Limitation Act is not applicable to give power to First Appellate authority to condone the delay beyond statutory time limit allowed.

|

|

|

|

|

|

4. Lawgics by Ms.Nidhi Aggarwal

|

Ms. Nidhi Aggarwal is delighted to present judgment with a great vision to spread complex GST law in a simple manner amongst the taxpayers, tax professionals, students and knowledge seeker.

|

|

Recently added notes are listed below:

|

|

|

|

|

|

Synopsis: The Delhi High Court dismissed the writ petition involving fraudulent ITC claims, directing the petitioner to pursue appellate remedy u/s 107 of the CGST Act.

|

Caste name: Banson Enterprises & Anr. vs Assistant Commissioner CGST & Ors.

|

Citation: W.P. (C) 6503/2025 dated 15.05.2025

|

Authority: Delhi High Court

|

The petition challenges the Order-in-Original dated 02.02.2025 based on a Show Cause Notice (SCN) dated 03.08.2024 A search was conducted, and statements were recorded including that of one Director admitting to the issuance of fake invoices during the Central Excise period. It was alleged that the Petitioner issued goods-less invoices to enable fraudulent Input Tax Credit (ITC) claims amounting to Rs. 1.85 crore.

|

Contentions of the Petitioner:

|

SCN was issued by unauthorized officer, thus, violates Rule 142(1)(a) of CGST Rules. No pre-consultation as required under Rule 142(1A) of CGST Rules was issued. Consolidated SCN for multiple financial years was issued and challenge to such consolidated action is pending in a separate matter (Quest Infotech case).

|

Contentions of the Department:

The impugned order is appealable, hence writ is not maintainable. The Petitioner’s Director admitted to allegations. Natural justice was followed as the Petitioner received the SCN, filed a reply, and availed of personal hearing. Reliance must be made on SC judgments and Allahabad HC rulings emphasizing alternate remedy u/s 107 CGST Act.

|

Findings and Decision of the Court:

The Court refused to interfere under writ jurisdiction, citing:

|

- No breach of fundamental rights or principles of natural justice.

- Availability of a statutory remedy (appeal) under Section 107 CGST Act.

The Court noted that the Allegations involve serious misuse of ITC, requiring fact-based adjudication, not suited for writ jurisdiction. Thus, the Petitioner was granted liberty to file appeal, and if filed with pre deposit, the appeal shall not be dismissed on limitation.

|

|

|

|

|

|

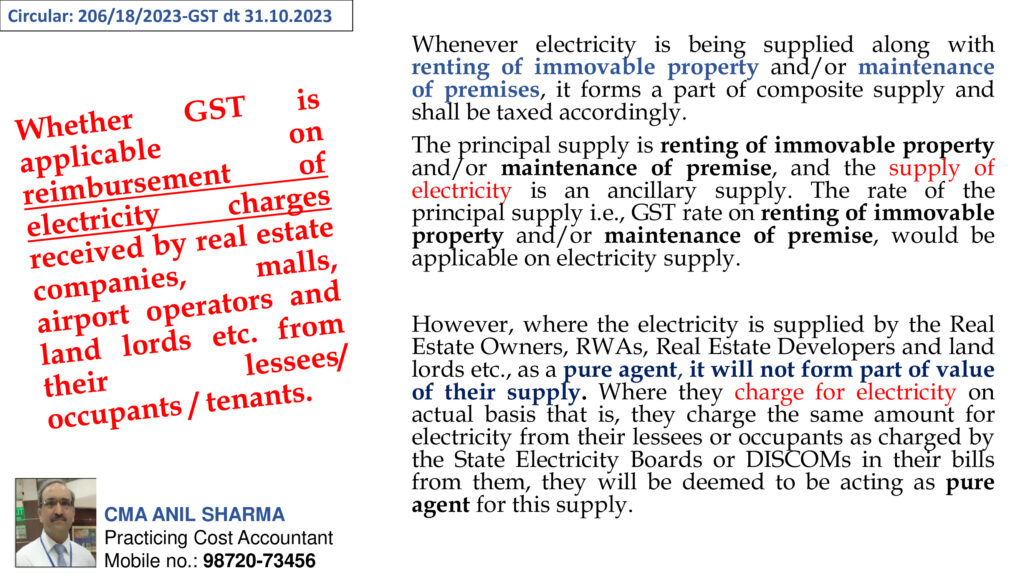

5. GST Notes by CMA Anil Sharma

1) New slides on GST Circulars is added in the Notes section titled as "Capsules".

|

- Total 25 slides in capsule-01 is added

|

|

|

|

|

|

|

|

6. GST Daily by CA Pradeep Modi

CA Pradeep Modi is presenting judgment analysis under title 'GST Daily - Stay yourself updated'

|

|

|

|

|

|

THE HON'BLE ALLAHABAD HIGH COURT IN THE CASE OF Vibhuti Tyres V/s State of U.P., decided on 7-5-2025

|

✔️ Is it justified that GST order with higher demand than show-cause notice?

|

👉 The Hon'ble High Court Judgement:-

|

✔️ Where in show-cause notice amount representing tax, interest and penalty was indicated as Rs. 8,81,080, but in order, much higher demand was raised at Rs. 32,97,336, same was in violation of section 75(7); matter was to be remanded back.

|

Section 75 of Central Goods and Services Tax Act, 2017

|

|

|

|

|

|

7. PPT/Handbook on GST

|

|

|

|

8. GST/Income Tax in Media

|

|

|

|

|

|

|

|

|

|

|

|

|

|

🔔 Topic: Intricacies in RCM Compliance w.r.t New Amendment & Overview of IMS 👍

|

🗓 Date: 14.11.2024 (Thursday)

⏰ Time: 2:00 to 3:00 pm.

🎤 Speaker: CA Saradha Hariharan

▶ Medium: English

🤝 Fees: Rs. 100/-

🔖 Recording - Yes

|

|

|

|

|

|

|

|

We are happy to introduce -

👉 GST Litigation Course 🥳🎊🎉

|

🗓 3 (three) days Course, 2 hours each

🎙 Best Industry Speaker

📚 From SCN, Adjudicating to Appeal level training - detailed procedure and practical aspects covered e.g. how to read SCN, drafting technique, adjudicating strategy, appeal order reading, appeal preparation, filing - pratical case discussion.

🔖 Notes will be given

🎥 Recording given

|

|

Tentative date for course launch is Nov 2024

|

|

|

|

|

|

|

|

|

Hope the above updates is of use to you. Please share your input and feedback at taxupdate.otu@gmail.com

|

|

|

|

|

|

|

|

|

Visit our website

|

OTU provides you

|

- Articles on various topics

|

|

- Media - GST, Income Tax & Press R.

|

|

|

|

|