|

onlinetaxupdate team wish to express sincere thanks to all the readers, authors, subscribers for the support extended to us. Please share your feedback at

|

taxupdate.otu@gmail.com or 7738647904

|

Newsletter 148 dated 30.12.2024

|

|

|

|

|

|

|

|

|

Dear Reader,

|

Please find newsletter for your reading and reference.

|

|

|

Kindly share your suggestion on the 'GST Refund Course' in the Google form

|

|

|

|

Index of the Newsletter

- Recent updates

- GST

- Customs

- DGFT

- Income Tax

- Portal updates

- Article

- GST Notes

- by Ms.Nidhi Aggarwa

- by CMA Anil Sharma

- by CA Pradeep Modi

- PPT/Handbook

- Tax in Media

- GST

- Customs

- Income tax

- Other

|

|

|

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Notification no. 02/2026 – Central Tax dated 07.05.2026.

|

GOVERNMENT OF INDIA

MINISTRY OF FINANCE

DEPARTMENT OF REVENUE

|

Notification No. 02/2026 – Central Tax dated 07.05.2026

|

S.O. 2286(E).— In exercise of the powers conferred by sub-section (1A) of section 101A of the Central Goods and Services Tax Act, 2017 (12 of 2017) (hereinafter referred to as the said Act), the Central Government, on the recommendations of the Council, hereby empowers the Principal Bench of the Appellate Tribunal, New Delhi constituted under sub-section (3) of section 109 of the said Act, to hear appeals made under section 101B of the said Act.

|

This notification shall be deemed to have come into force on the 1st day of April, 2026.

|

BALASUBRAMANIAN KRISHNAMURTHY,

Joint Secretary

|

|

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Notification no. 01/2026 – Central Tax dated 21.04.2026 that Seeks to extends the due date for furnishing the return in FORM GSTR-3B for the month of March, 2026 till the twenty-first day of April, 2026.

|

GOVERNMENT OF INDIA

MINISTRY OF FINANCE

DEPARTMENT OF REVENUE

CENTRAL BOARD OF INDIRECT TAXES AND CUSTOMS

Notification No. 01 /2026 Central Tax dated 21.04.2026

|

G.S.R (E)… ( In exercise of the powers conferred by sub section (6) of section 39 of the Central Goods and Services Tax Act, 2017 (12 of 2017), the Commissioner, on the recommendations of the GST Council, hereby extends the due date for furnishing the return in FORM GSTR 3B for the month of March, 2026 till the twenty first day of April, 2026, for the registered persons who are required to furnish return under sub section (1) of section 39 read with clause (i) of sub rule (1) of rule 61 of the Central Goods and Services Tax Rules, 2017.

|

2. This notification shall come into effect from 20th day of April, 2026.

|

(Kangale Shrunkhala Motiram)

Director

|

|

|

|

|

|

OFFICE OF THE COMMISSIONER OF STATE TAXMAHARASHTRA STATE, MUMBAI issued NOTIFICATION NO: - SGST/e-way bill/02/2025-26 dated 20.02.2026 Waiving off requirement of e-way bill for motor vehicles for road testing where goods are transported for reasons other than by way of supply under sub-rule (5) of rule 138A of MGST Rules, 2017.

|

M/s. Tata Motors Limited, having principal place of business at TATA MOTORS LIMITED, Nigadi Bhosari Road, Pimpri Chinchwad, Pune, Maharashtra, 411 018. (GSTIN: 27AALCT0864B1ZE) (hereinafter called as ‘taxpayer’), have made a representation vide their letter GST/MH/056 dated 13th November 2025. for waiving off requirement of e-way bill for motor vehicles for road testing where goods are transported for reasons other than by way of supply under sub-rule (5) of rule 138A of MGST Rules, 2017(hereinafter referred as MGST Rules, 2017).

|

Whereas I, Asheesh Sharma, Commissioner of State Tax. Maharashtra State, am of the opinion that the difficulties being faced by the ‘taxpayer’ are genuine and require due consideration. Now, therefore I, Asheesh Sharma, Commissioner of State Tax, Maharashtra State, in exercise of the powers conferred upon me under sub-rule (5) of rule 138A of the MGST Rules, 2017, am pleased to issue this notification for grant of permission to M/s. Tata Motors Limited. having principal place of business at TATA MOTORS LIMITED, Nigadi Bhosari Road, Pimpri Chinchwad, Pune, Maharashtra, 411 018 (GSTIN: 27AALCT0864B1ZE) to waive the requirement of e-way bill for motor vehicles to perform various road tests across India, subject to the following procedure and conditions as mentioned below.

|

(i) The ‘ taxpayer ’ shall execute a bond sufficient to cover the value of the motor vehicle being cleared for the purpose of road testing in a calendar month, with the Jurisdictional State Tax Officer, PIMPRI_702, Division - PUNE_SOUTH_EAST, Zone - PUNE_SOUTH_WEST, PUNE undertaking to follow all the conditions mentioned hereunder;

|

(ii) Motor vehicles shall be removed by the ‘taxpayer’ for the purpose of road test under a delivery challan, duly signed by the authorized signatory of the “taxpayer”;

|

(iii) The exemption to carry delivery challan instead of e-way bill is limited only to transportation of motor vehicles for reasons other than by way of supply and limited to road test of such motor vehicles;

|

(iv) The delivery challan shall be induplicate, pre-authenticated and having running serial number for every calendar year and printed format and shall contain the following information.

|

(a) The name and address of the “taxpayer”, it’s ‘GSTIN’

|

(b) Name of the jurisdictional officer, Division and Zone with whom the taxpayer is registered for the purpose of GST and notification number under which permission under sub-rule (5) of rule 138(A) of MGST Rules, 2017 for such removal has been given;

|

(c) The description, vehicle serial number/ engine number/ chassis number, as the case may be, to identify the vehicle which has been cleared for the purpose carrying out road test along with the value of such motor vehicle;

|

(d) The date of dispatch of such motor vehicle for road test and probable time line for return of the motor vehicles to its place of clearance;

|

(v) The Motor vehicle/ transport equipment will also carry trade plate as prescribed under Central Motor Vehicles Rules, 1989 or under any other law in force for the purpose of undertaking testing of such motor vehicle as the case may be;

|

(vi) The ‘taxpayer’ shall maintain proper records to correlate the dispatch and return of the motor vehicles sent for road testing. If at any point of time the value of the motor vehicles cleared for road test exceeds the amount for which the bond has been executed, the ‘taxpayer’ shall execute a separate bond of differential value with the concerned, before removal of the motor vehicle for testing purpose;

|

(vii) The taxpayer’ shall submit to the Jurisdictional State Tax Officer, PIMPRI_702, Division - PUNE_SOUTH_EAST, Zone - PUNE_SOUTH_ WEST, PUNE a monthly account containing the details of all motor vehicles sent and received back after road testing;

|

(viii) The ‘taxpayer’ shall furnish any additional relevant information pertaining to the instant subject matter which may be required by the Jurisdictional State Tax Officer, PIMPRI_702, Division-PUNE_SOUTH_EAST, Zone - PUNE_SOUTH_WEST, PUNE.

|

2. The ‘ taxpayer ’ shall be fully responsible and accountable for the taxable goods so removed without generation of e-way bill under sub-rule (5) of rule 138(A) of MGST Rules, 2017 as permitted under this notification.

|

3. If the above said conditions are not adhered to or are violated, the impugned permission shall be revoked/withdrawn without any prior intimation.

|

4. This notification is valid for financial year 2025-26, i.e. up to 31st March 2026

|

|

|

|

|

|

|

Kolkata is likely to host the 57th meeting of the GST Council next month, sources said, although the Union Finance Ministry has not yet officially confirmed the venue or the schedule.

|

|

|

|

|

|

|

|

|

|

|

The four citizen-centric initiatives include revised Citizen's Charter, Revamped Citizen's Corner for complete tax related information, ‘Ease of Doing Business’ tab for making suggestions, and CBIC Archives for tax repository

|

|

|

|

|

|

|

|

|

In the year 2024, the Central Board of Direct Taxes (CBDT) and Central Board of Indirect taxes and Customs (CBIC), under the Department of Revenue, Ministry of Finance, have continued their citizen centric initiatives, driving significant reforms to enhance taxpayer experience...

|

|

|

|

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Corrigendum on 12.06.2026 to Notification no. 45/2025 -Customs dated 24.10.2025 -

|

G.S.R…(E).- In the notification of the Government of India, Ministry of Finance (Department of Revenue) No. 45/2025-Customs, dated the 24th October, 2025, published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i), vide number G.S.R. 781(E), dated the 24th October, 2025, at page 291, in lines 12 and 14, for ‘1993’ read ‘1983’.

|

|

|

|

|

|

CBIC issued Notification No. 58/2026-Customs (N.T.) dated 22.06.2026 to hereby appoint the officer to exercise the powers and discharge the duties conferred on the officers for the purpose of adjudication of the show cause notices.

|

|

|

|

|

|

|

|

CBIC issued Notification No. 57/2026-Customs (N.T.) dated 18.06.2026 to further amend Notification No. 27/2018-Customs (N.T.) dated 28.03.2018.

|

|

|

|

|

|

|

|

CBIC issued Notification No. 56/2026-Customs (N.T.) dated 16.06.2026 to make further amendment in Notification no. 21/2022-Customs (N.T.) dated 31.03.2022.

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Notification no. 12/2026-Customs (ADD) dated 19.06.2026 Seeking to continue anti-dumping duty on imports of Polyethylene Terephthalate resin having an intrinsic viscosity of 0.72 decilitres per gram or higher originating in or exported from China for a period of 5 years

|

|

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Notification no. 11/2026-Customs (ADD) dated 19.06.2026 Seeking to impose anti-dumping duty on imports of Sulphenamides Accelerators originating in or exported from China for a period of 5 years

|

|

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Notification no. 10/2026-Customs (ADD) dated 10.06.2026 to amend the Notification no. 51/2021-Customs (ADD) dated 16.09.2021

|

Government of India

Ministry of Finance

(Department of Revenue)

|

Notification No. 10/2026-Customs (ADD) dated 10.06.2026

|

G.S.R…-(E). - In exercise of the powers conferred by sub-sections (1) and (5) of section 9A of the Customs Tariff Act, 1975 (51 of 1975) read with rules 18 and 23 of the Customs Tariff (Identification, Assessment and Collection of Anti-dumping Duty on Dumped Articles and for Determination of Injury) Rules, 1995, the Central Government hereby makes the following amendment in the notification of the Government of India, in the Ministry of Finance (Department of Revenue) No. 51/2021-Customs(ADD), dated the 16th September, 2021, published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i), vide number G.S.R. 637(E), dated the 16th September, 2021, namely:-

|

In the said notification, after paragraph 2 and before Explanation, the following paragraph shall be inserted, namely:-

|

“3. Notwithstanding anything contained in paragraph 2, the anti-dumping duty imposed under this notification shall remain in force up to and inclusive of the 15th December, 2026, unless revoked, superseded or amended earlier.”.

|

(Dheeraj Sharma)

Under Secretary

|

Note: The principal notification No. 51/2021-Customs (ADD), dated the 16th September, 2021 was published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i), vide number G.S.R. 637(E), dated the 16th September, 2021.

|

|

|

|

|

|

OFFICE OF THE PRINCIPAL COMMISSIONER OF CUSTOMS (AIR CARGO), AIR CARGO COMPLEX, MEENAMBAKKAM, CHENNAI 600 016 issued PUBLIC NOTICE No : 15/2025 dated 29.07.2025 regarding Enablement of Voluntary Payment electronically on ICEGATE e-Payment Platform

|

Attention of all the Importers, Exporters, General Trade, Other stakeholders, members of trade and Officers of Air Cargo Commissionerate, Chennai is invited to CBIC's circular No. 27/2024- customs dated 23.12.2024 on above mentioned subject.

|

2. In line with Government's commitment to digitize all the services and to make it paperless, ICEGATE e-Payment Platform has been enabled with electronic collection of Voluntary/Self-Initiated Payments (SIP).

|

3. This new functionality has been envisaged to replace the existing TR6 payments which are currently being done manually at various Customs Stations. This functionality shall enable the users to generate a self-initiated challan for voluntary payments and then make payments through the ICEGATE e-payment platform without any further approval by officers of Customs.

|

4. While using the voluntary payment Facility at ICEGATE, the users may take note of the below-mentioned aspects:

|

- a. The Voluntary Payment module will be accessible as a post login functionality. Users must be registered on ICEGATE to access this feature;

- b. This facility is enabled with payments which are primarily meant for imports/exports cleared in the past. In other words, the facility is not a replacement for challans generated by ICES/ECCS/SEZ online/ACES applications. Therefore, it should not be used for payment of customs duties for clearance of any live consignments;

- c. The various purposes, for which the payment can be made are provided in Annexure-A, wherein, it is advised to select the same carefully while making payment.

- d. The proof of payment may be submitted to the concerned sections/field formations for taking further action,

- The officer may verify the payment details using https://foservices.icegate.gov.in/#/epayment/enquiry

5.1 Currently, ICEGATE users can make voluntary payments as a debit from the Electronic Cash Ledger (only available for IEC holders and Customs Brokers).

|

5.2 In case, users wish to initiate challan-wise payment, the ICEGATE platform also allows user to make transaction-wise payment on the platform, whereby the systems design takes care of routing the payment instantaneously through Electronic Cash Ledger before accounting for duty payment. On completion of testing for voluntary payment acceptance, at present, following modes are enabled for such challan wise payments:

|

- a. Nine (9) banks under internet banking through authorized bank mode, as per Annexure-B

- b. NEFT/RTGS through RBI

- Payment Aggregator mode

5.3 Remaining banks shall be enabled as and when the testing is complete. In all other modes, users already have an option to deposit the amount in the Electronic Cash Ledger through remaining authorized modes and use the same for making voluntary payment using Electronic Cash Ledger

|

6. Since the above facility is aimed at replacing the current procedure of making Over The-Counter (OTC) payment using TR-6 Challan, all the officers in Air Cargo Complex, Chennai are not to accept any payments through manual TR-6 challan after 19 JULY, 2025, unless the same is approved by the concerned Pr. Commissioner/Commissioner of Customs. The approval must clearly spell out the reasons for resorting to the manual method of payment. The field officers can view the voluntary challans through 'Payment Status - Voluntary Payment' option available in 'Service' section of ICEGATE portal (http://www.icegate.gov.in)

|

7. An user manual on the Voluntary/Self-Initiated Payment (SIP) facility to handhold and onboard the users has been uploaded (http://www.icegate.gov.in/guidelines/voluntary-payment) on the ICEGATE platform

|

8. Difficulties faced, if any, may be brought to the notice of Joint Commissioner/Additional Commissioner designated as Systems manager in Air Cargo Complex Chennai for necessary action or e-mail the difficulties faced to the following e-mail ID, pcommr7acc-cuschn@gov.in.

|

9. All the stakeholders including the trade and concerned associations are requested to take note of the above. All officers to treat this as Standing instruction.

|

This is issued with the approval of Principal Commissioner of Customs, Air Cargo Commissionerate

|

To,

All Concerned

Copy submitted to:

The Principal Chief Commissioner of Customs,

Chennai Customs Zone .

Copy to:

|

- The Principal Commissioner/Commissioner of Chennai Customs ZoneChennai- I/Chennai–II/ Chennai-III/Chennai-IV/ Chennai Audit.

- The Additional / Joint Commissioners of Customs, Chennai VII

Commissionerate

- All Dy. /Asst Commissioners of Customs, Chennai VII Commissionerate.

- The D.C. (EDI), ACC, Chennai, for uploading on website of Chennai–VII

Commissionerate.

- The Supdt. CHS for notice board display purpose

- Hindi Cell

Annexure-A

One of the following purposes to be selected while using Voluntary

Payment Facility at ICEGATE:

|

- i. Payment pursuant to an Investigation:

- ii. Payment pursuant to Audit;

- iii. Payment pursuant to Internal Compliance; EPCG (Payment of Duty,

- interest. penalty);

- iv. EODC (Payment of Duty, interest, penalty);

- v. Advanced License/Authorization (Payment of Duty):

- vi. IGCR (Payment of Duty, interest, penalty);

- vii. Payment at the time of Pre-Notice Consultation;

- viii. Payment for notices under section 28(2) and 28(4) of Customs Act,

- 1962;

- ix. Payment for closure of proceedings in terms of section 28(5) of the

- Customs Act. 1962:

- x. Payment of interest:

- xi. Payment of penalty:

- xii. Pre-Deposit against appeals:

- xiii. Amounts arising out of proceedings before Settlement Commission:

- xiv. Fines imposed by any order;

- xv. Payment of outstanding demands/ Arrear payments:

- xvi. Amounts arising out of disposal of Uncleared/Unclaimed Goods:

- xvii. Amounts arising out of disposal of seized goods;

- xviii. Amounts arising out of disposal of confiscated goods:

- xix. Amounts arising out of Court Attachment orders;

- xx. Advance ruling (CAAR) fees;

- xxi. Cost recovery charges;

- xxii. Transshipment fees;

- xxiii. Merchant overtime charges;

- xxiv. Bill of Entry (BE) amendment fees;

- xxv. Shipping Bill (SB) amendment fees;

- xxvi. Payments not mentioned above;

- Punjab National Bank (PNB)

- Kotak Mahindra Bank

- IDBI Bank

- Karnataka Bank

- Canara Bank

- Karur Vysya Bank (KVB)

- South Indian Bank (SIB)

- Federal Bank

- IndusInd Bank

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Circular no. 28/2026-Customs dated 15.06.2026 regarding testing of samples of export consignments

|

|

|

|

|

|

|

The Government of India has taken various initiatives to provide the income tax relief to cooperative societies. Details are as under:

|

|

|

|

|

|

|

|

|

The Central Board of Direct Taxes (CBDT) has launched an electronic campaign to assist taxpayers in resolving mismatches between the income and transactions reported in the Annual Information Statement (AIS) and those disclosed in Income Tax Returns (ITRs) for the financial years 2023-24 and 2021-22.

|

|

|

|

|

|

|

|

|

|

Directorate General of Foreign Trade (DGFT) issued Notification No. 20/2026-27 dated 02.06.2026 regarding Applicability of Quality Control Orders (QCOs)/ BIS requirements on imports by Special Economic Zone (SEZ) Units and Developers - Amendment in Para 2.03(A)(iii) of FTP 2023

|

|

|

|

|

|

|

|

Directorate General of Foreign Trade (DGFT) issued Notification No. 19/2026-27 dated 02.06.2026 regarding Amendment in import policy condition of specific ITC HS Codes covered under Chapter 71 of ITC (HS), 2022, Schedule - I (Import Policy)

|

|

|

|

|

|

|

|

Directorate General of Foreign Trade (DGFT) issued Notification No. 18/2026-27 dated 02.06.2026 regarding Nomination of Non-official Members of the Board of Trade

|

|

|

|

|

|

Directorate General of Foreign Trade (DGFT) issued Policy Circular no. 01/2026-27 dated 15.04.2026 regarding Clarification on Eligibility of New ECGC Whole Turnover Policy under Component II of the Resilience & Logistics Intervention for Export Facilitation (RELIEF) under Export Promotion Mission (EPM)

|

|

|

|

|

|

|

|

Directorate General of Foreign Trade (DGFT) issued Policy Circular no. 10/2025-26 dated 26.02.2026 regarding EPCG Scheme - Relief in Average EO in terms of the para 5.17(a) of Hand Book of procedures (HBP) of FTP, 2023,

|

Government of lndia

Ministry of Commerce and lndustry

(Directorate General of Foreign Trade)

Vanijya Bhawan, New Delhi

Web Site: http://dgft.gov.in

|

Policy Circular No. 10/2025-26 dated 26.02.2026

|

To,

All Regional Authorities of DGFT/

All Customs Authorities

|

Subject: EPCG Scheme - Relief in Average EO in terms of the para 5.17(a) of Hand Book of procedures (HBP) of FTP,2023,

|

The para 5.17 of the HBP of the FTP, 2023 envisages that to provide relief to exporters of those sectors where total exports in that sector/product group has declined by more than 5% as compared to the previous year, the Average Export obligation (EO) for the year may be reduced proportionate to reduction in exports of that particular sector/product group during the relevant year as against the preceding year. This implies that the sector/product group that witnessed such decline in 2024-25 as compared to 2023-24 would be entitled for such relief.

|

2. A list of product groups showing the percentage decline in exports during 2024-25 as compared to 2023-24 is Annexed.

|

3. All Regional Authorities are requested to re-fix the Annual Average EO for EPCG Authorizations for the year 2024- 25 accordingly. The reduction, if any, in the EO should be appropriately endorsed in the license file of the Office of Regional Authority and also in the amendment sheet to be issued to the EPCG Authorisation holder.

|

4. Regional Offices while considering requests of discharge of EO will ensure that in case of shortfall in EO fulfilment, Policy Circulars issued earlier in terms of Para 5.11.2 of HBP 2009-14, Para 5.19 of HBP of FTP 2015-20 and para 5.17 of FTP, 2023 are also considered before issuance of demand notice, EODC etc. This stipulation should be part of Check-Sheet for the purpose of EODC.

|

5. This issues with the approval of Director General of Foreign Trade.

|

Enclosures: As mentioned above.

|

(Randheep Thakur)

Joint Director General of Foreign Trade

Tel. No.011-2303 8731

E-mail: randheep.thakur@gov.in

|

(lssued from F. No. 18/43/AM-26/P-5)

|

|

|

|

|

|

Directorate General of Foreign Trade (DGFT) issued Public Notice No. 17/2026-27 dated 04.06.2026 regarding Enlistment under Appendix 2E of FTP, 2023-Agency Authorised to issue Certificate of Origin (Non-Preferential)

|

|

|

|

|

|

|

|

Directorate General of Foreign Trade (DGFT) issued Public Notice No. 16/2026-27 dated 02.06.2026 regarding Amendment in Para 2.88 of Handbook of Procedures

|

|

|

|

|

|

|

|

Directorate General of Foreign Trade (DGFT) issued Public Notice No. 15/2026-27 dated 02.06.2026 regarding Amendment of Appendix 2B [List of Agencies Authorised to issue Certificate of Origin (Preferential) of Foreign Trade Policy , 2023.

|

|

|

|

|

|

|

|

Directorate General of Foreign Trade (DGFT) issued Public Notice No. 14/2026-27 dated 01.06.2026 regarding Fixation of Six New Standard Input Output Norms (SIONs) at SION No. A-3702, A-3703, A-3704, A-3705, A-3706 & A-3707 under "Chemical and Allied Product" (Product Code-'A')

|

|

|

|

|

|

Directorate General of Foreign Trade (DGFT) issued Trade Notice 07/2026-27 dated 03.06.2026 regarding request for comments on alignment of Schedule-II (Export Policy) of ITC (HS), 2022 consequent to amendments introduced under the Finance Act, 2026

|

|

|

|

|

|

|

|

Central Board of Direct Taxes (CBDT) issued notification no. 72/2026 dated 25.06.2026 to hereby approves deductions under section 45(3)(a)(i) of the Income-tax Act, 2025 and rules 32 and 34 of the Income-tax Rules, 2026 to the Public Health Foundation of India, Delhi (PAN: AABAP4445L) for Scientific Research under the category of University, college or other institution.

|

|

|

|

|

|

|

|

Central Board of Direct Taxes (CBDT) issued notification no. 71/2026 dated 25.06.2026 to hereby approves deductions u/s 45(3)(a)(i) of the Income-tax Act, 2025 and rules 32 and 34 of the Income-tax Rules, 2026 to the University of Hyderabad (PAN: AAAAU8109M) for Scientific Research under the category of university, college or other institution.

|

|

|

|

|

|

|

|

Central Board of Direct Taxes (CBDT) issued notification no. 70/2026 dated 01.06.2026 to hereby specifies the business (other than the business specified in Note 5(d)(i) of the said Schedule), which is engaged in the infrastructure sub-sectors mentioned in the Updated Harmonised Master List of Infrastructure sub-sectors, in the notification of the Government of India in the Ministry of Finance, Department of Economic Affairs number F.No.13/1/2025-IPP, dated the 19th September, 2025, published in Gazette of India, Extraordinary, Part I, Section 1, as a business for the purposes of Schedule V of the said Act.

|

This notification shall come into force from the date of its publication in the Official Gazette.

|

|

|

|

|

|

Central Board of Direct Taxes issued Circular no. 4 of 2026 dated 31.03.2026 regarding Document Identification Number (DIN).

|

|

|

|

|

|

|

|

|

It is informed that the Aggregate Annual Turnover (AATO) functionality is currently being upgraded to enable automatic updation of AATO

|

|

|

|

|

|

|

|

|

|

|

Gross and Net GST revenue collections for the month of June, 2026

|

|

|

|

|

|

|

|

|

|

|

GSTN is taking downtime to enhance its services on the GST Portal on 27.06.2026 from 12:00 AM onwards until 2:30 am of 27.06.2026.

|

|

|

|

|

|

|

|

|

|

|

GSTN is taking downtime to enhance its services on the GST Portal on 12.06.2026 from 11:30 AM onwards until 7:30 am of 13.06.2026. We shall be enhancing services on the GST portal on : 12th June’26 11:30 PM onwards. GST Portal services will not be available until 13th June’26 07:30 AM. The inconvenience caused is regretted.

|

|

|

|

|

|

|

|

|

|

|

Reference is invited to the GSTN Advisory dated 20.05.2026 regarding enhancements in the e-Way Bill system, wherein it was informed that “Ship-to GSTIN” shall be mandatorily captured in Bill-to/Ship-to transactions.

|

|

|

|

|

|

|

|

|

|

|

Representations have been received from trade and industry seeking extension of the implementation timeline, citing the requirement of system changes, testing, API/ERP readiness and master data updation across the taxpayer ecosystem.

|

|

|

|

|

|

|

|

|

|

|

GSTN is taking downtime to enhance its services on the GST Portal on 06.06.2026 from 01:30 AM onwards until 3:30 am of 06.06.2026.

|

|

|

|

|

|

|

|

|

|

|

From AY 2026-27, the option to report 'Other Exempt Income' was removed. Now it is being restored.

|

|

|

|

|

|

|

|

|

|

|

Helps identify name mismatches in advance and avoid registration issues.

|

|

|

|

|

|

|

|

|

|

|

No, the Honorable Madras High Court in the case of M/s. SS Traders vs. Joint Commissioner (ST) (Intelligence) set aside the order and remanded back to pass a fresh order. The Honorable Court noted that the petitioner is mulct with huge tax liability vide Assessment Order and on the date of hearing, 105 pages’ order was passed which was technically impossible.

|

|

|

|

|

|

|

|

|

The recent judgment of the Madras High Court in the case of Tvl. Skanthaguru Innovations Private Limited has sparked a new debate as to whether the revenue department can make the balance of ECL negative by exercising the power of Rule 86A of the CGST Rules.

|

|

|

|

|

|

|

|

|

The Free Trade Warehousing Zones FTWZ is considered as a special category of Special Economic Zone wherein the activities of trading, warehousing, labeling, packing, or re-packing without any processing are permitted.

|

|

|

|

|

|

|

|

4. GST Notes

by Ms.Nidhi Aggarwal

|

Ms. Nidhi Aggarwal is delighted to present judgment with a great vision to spread complex GST law in a simple manner amongst the taxpayers, tax professionals, students and knowledge seeker.

|

|

Recently added notes are listed below:

|

|

|

|

|

|

Synopsis: The Delhi High Court dismissed the writ petition involving fraudulent ITC claims, directing the petitioner to pursue appellate remedy u/s 107 of the CGST Act.

|

Caste name: Banson Enterprises & Anr. vs Assistant Commissioner CGST & Ors.

|

Citation: W.P. (C) 6503/2025 dated 15.05.2025

|

Authority: Delhi High Court

|

The petition challenges the Order-in-Original dated 02.02.2025 based on a Show Cause Notice (SCN) dated 03.08.2024 A search was conducted, and statements were recorded including that of one Director admitting to the issuance of fake invoices during the Central Excise period. It was alleged that the Petitioner issued goods-less invoices to enable fraudulent Input Tax Credit (ITC) claims amounting to Rs. 1.85 crore.

|

Contentions of the Petitioner:

|

SCN was issued by unauthorized officer, thus, violates Rule 142(1)(a) of CGST Rules. No pre-consultation as required under Rule 142(1A) of CGST Rules was issued. Consolidated SCN for multiple financial years was issued and challenge to such consolidated action is pending in a separate matter (Quest Infotech case).

|

Contentions of the Department:

The impugned order is appealable, hence writ is not maintainable. The Petitioner’s Director admitted to allegations. Natural justice was followed as the Petitioner received the SCN, filed a reply, and availed of personal hearing. Reliance must be made on SC judgments and Allahabad HC rulings emphasizing alternate remedy u/s 107 CGST Act.

|

Findings and Decision of the Court:

The Court refused to interfere under writ jurisdiction, citing:

|

- No breach of fundamental rights or principles of natural justice.

- Availability of a statutory remedy (appeal) under Section 107 CGST Act.

The Court noted that the Allegations involve serious misuse of ITC, requiring fact-based adjudication, not suited for writ jurisdiction. Thus, the Petitioner was granted liberty to file appeal, and if filed with pre deposit, the appeal shall not be dismissed on limitation.

|

|

|

|

|

|

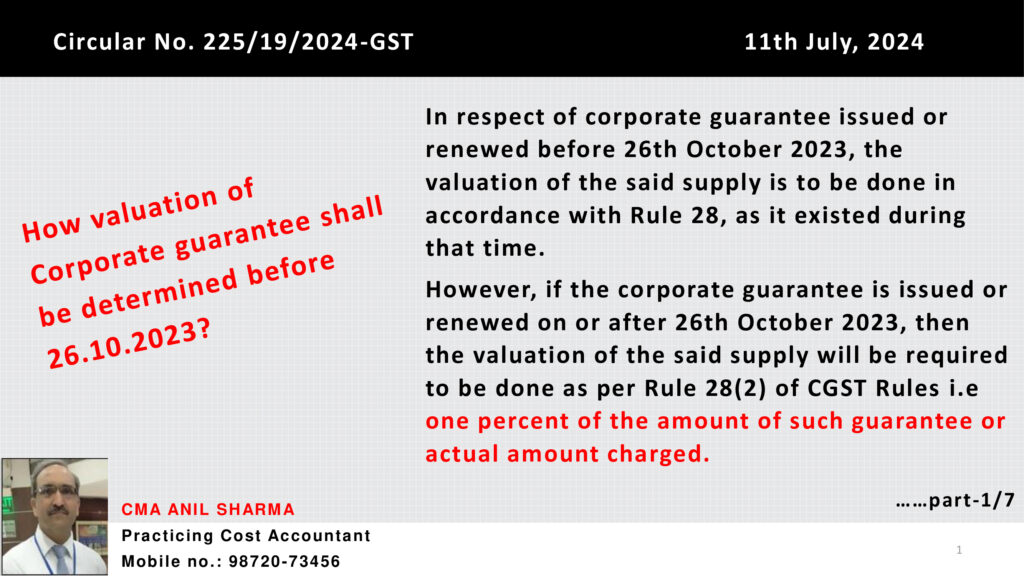

by CMA Anil Sharma

1) New series title "Capsule" is added in the Notes section.

|

- Total 62 slides in capsule-01 & capsule 02 Part 1 & 2 and capsule 03 part 1 is added

|

|

|

|

|

|

|

|

by CA Pradeep Modi

CA Pradeep Modi is presenting judgment analysis under title 'GST Daily - Stay yourself updated'

|

|

|

|

|

|

THE HON'BLE ALLAHABAD HIGH COURT IN THE CASE OF Vibhuti Tyres V/s State of U.P., decided on 7-5-2025

|

✔️ Is it justified that GST order with higher demand than show-cause notice?

|

👉 The Hon'ble High Court Judgement:-

|

✔️ Where in show-cause notice amount representing tax, interest and penalty was indicated as Rs. 8,81,080, but in order, much higher demand was raised at Rs. 32,97,336, same was in violation of section 75(7); matter was to be remanded back.

|

Section 75 of Central Goods and Services Tax Act, 2017

|

|

|

|

|

|

|

|

THE HON'BLE JHARKHAND HIGH COURT IN THE CASE OF Sadanand Prasad Barnwal V/s State of Jharkhand, decided on 8-5-2025

|

✔️ Is it valid if SCN and order under section 73 for lack of digital signature of issuing authority?

|

👉 The Hon'ble High Court Judgement:-

|

✔️ Where both summary of SCN in Form GST DRC-01 and order under section 73 did not bear digital signature of concerned authority, both SCN and order were to be quashed.

|

Section 161, read with section 73 of Central Goods and Services Tax Act, 2017

|

|

|

|

|

|

|

|

THE HON'BLE CALCUTTA HIGH COURT IN THE CASE OF Edelweiss Rural & corporate Services Ltd. V/s Deputy Commissioner of Revenue, decided on 5-5-2025

|

✔️ What would be Refund if business stood closed and registration was cancelled?

|

👉 The Hon'ble High Court Judgement:-

|

✔️ Where Refund sanction order had itself observed that assessees business was closed down, its registration was cancelled and it had no tax dues refund claim was already allowed, direction to credit refund amount to credit ledger instead of bank account of assessee was self-contradictory since there was no business for assessee to take benefit of refund credited to assessees credit ledger.

|

Section 54 of Central Goods and Services Tax Act, 2017

|

|

|

|

|

|

|

|

THE HON'BLE JHARKHAND HIGH COURT IN THE CASE OF Sri Ram Stone Works V/s State of Jharkhand, decided on 9-5-2025

|

✔️ Can GST Notice would be issued under Section 61 of CGST Act merely on the basis of difference between sale price and market price?

|

👉 TheHon'ble High Court Judgement:- ✔️ Clear objective of section 61 is to enable an Assessing Officer to point out discrepancies and errors which are occurring in return filed by a registered person with that of related particulars; notice under section 61 cannot be issued comparing particulars at which assessee has sold its goods with that of prevalent market price.

|

|

|

|

|

|

|

|

THE HON'BLE ALLAHABAD HIGH COURT IN THE CASE OF Gopal Trading Company V/s State of U.P., decided on 7-5-2025

|

✔️ Can excess stock during search warrants proceedings would be confiscation under section 130 of CGST?

|

👉 The Hon'ble High Court Judgement:-

|

✔️ Where in search at premises of assessee, excess stock was found, Act specifically contemplates that proceedings under section 73/74 should be pressed; proceedings under section 130 could not have been pressed.Section 67, read with sections 73, 74 and 130, of Central Goods and Services Tax Act, 2017

|

|

|

|

|

|

5. PPT/Handbook on GST

|

|

|

|

6. Tax in Media

|

GST

|

|

|

|

|

|

|

|

|

|

|

|

|

We hope the above updates are of use to you.

Kindly share your feedback at taxupdate.otu@gmail.com

|

|

|

|

Visit our website

|

OTU provides you

|

- Articles on various topics

|

|

- Media - GST, Income Tax & Press R.

|

|

|

|

|