|

|

|

|

|

|

|

|

This website contains information about recent changes mainly in GST laws. It also contains Articles on various topic in GST. Please visit the website and read more.

|

|

|

|

Dear Reader,

|

Please find newsletter for your reading and reference.

|

|

Newsletter no. 89 dated 25.06.2023

|

|

|

Index of the Newsletter

- Recent updates

- GST in Media

- Press Release

- Article

- Lawgics by Ms.Nidhi Aggarwal

- GST notes by CMA Anil Sharma

- Book by CMA Anil Sharma

|

|

|

|

|

|

|

Income Tax, Income Tax misc

|

The Central Board of Indirect Taxes vide F. No.225/56/2026/ITA-II dated 04.06.2026 issued Guidelines for Compulsory Selection of returns for Complete Scrutiny during the financial year 2026-27 - procedure for compulsory selection in such cases.

|

The Guidelines for Compulsory Selection of returns filed during the financial year 2025-26 under the Income-tax, Act 1961 are hereby issued in pursuance of Section 536(2)(c) of the Income-tax Act, 2025. The parameters for compulsory selection of returns for complete scrutiny during Financial Year 2026-27 and procedure for compulsory selection in such cases are prescribed as under:

|

3. For Assessing Officers in International Taxation and Central charges: Cases may be selected for compulsory scrutiny by the International Taxation and Central Charges following the above prescribed parameters at Para 2 with prior administrative approval of Pr.CIT/Pr.DIT/CIT/DIT concerned and these selected cases shall continue to be handled by International Taxation and Central Circle charges respectively, as earlier. It is further clarified that communication to NaFAC for access and /or further action after selection for Compulsory Scrutiny will not apply to the International Taxation and Central charges.

|

4. Time limit: As per the proviso to section 143(2) of the Income tax Act, 1961 and in terms of section 536(2)(c) of the Income-tax Act, 2025, the time limit for service of notice u/s 143(2) of the Income-tax Act, 1961 for the ITRs filed in the Financial Year (FY) 2025-26 is 30.06.2026.

|

5. These instructions may be brought to the notice of all concerned for necessary compliance.

|

|

|

|

|

|

|

|

Notification giving effect to the Amending Protocol to the India–Brazil Double Taxation Avoidance Agreement (DTAA) under section 90(1) of the Income‑tax Act, 1961.

|

|

|

|

|

|

|

|

Income Tax, Income Tax misc

|

Form of Declaration under section 393(6) of the Income-tax Act, 2025 for receipt ofcertain incomes without deduction of tax

|

|

|

|

|

|

|

|

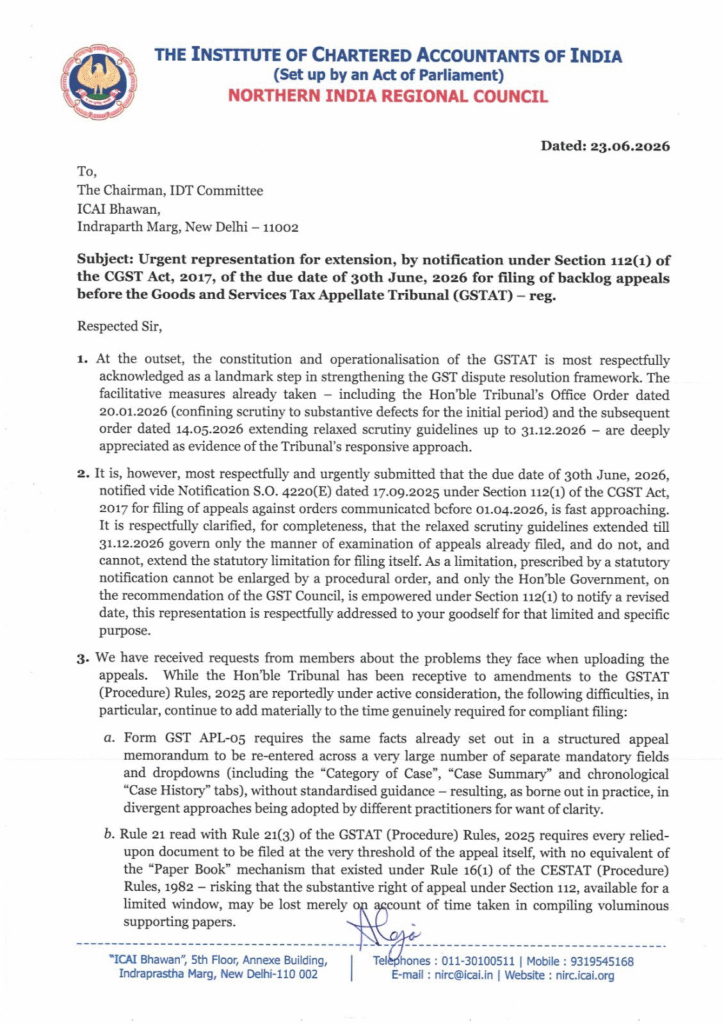

Centre has extended the last date for filing appeals before the Goods and Services Tax Appellate Tribunal (GSTAT) to July 31, 2026, giving taxpayers an additional month to submit their cases after a surge in filings led to technical difficulties on the GSTAT portal.

|

The extension applies to appeals filed under Section 112(1) read with Section 112(3) of the Goods and Services Tax (GST) law.

|

The revised deadline replaces the earlier cut-off of June 30, 2026, which had been notified by the government on September 17, 2025.

|

The decision follows recent representations from various stakeholders who flagged technical issues arising from a rush of appeals being filed on the GSTAT portal ahead of the deadline.

|

While noting that the original due date had been notified well in advance in September 2025, the government said filing activity had intensified sharply in recent weeks. It said 30,000 appeals were filed in the last 15 days alone, with daily filings touching a peak of 5,500 appeals.

|

Advising against eleventh-hour filings, the government urged taxpayers to complete their appeal submissions well in advance to ease pressure on the GSTAT portal.

|

The GST Appellate Tribunal serves as the first judicial appellate forum for taxpayers seeking to challenge orders issued by GST authorities after the disposal of their first appeals.

|

Source: The Economic Times

|

|

|

|

|

|

|

|

|

GST & IDT Committee has requested the Chairman, IDT Committee, ICAI, New Delhi to urgently represent before the respective forums for the date extension of GSTAT, i.e., 30-Jun-2026.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Tata Steel Limited said tax authorities have filed an appeal seeking restoration of penalties worth Rs. 368.72 crore that were earlier dropped in a GST adjudication order, even as proceedings on the underlying demand remain stayed by the Jharkhand High Court, according to a stock exchange filing.

|

"One June 16, 2026, the Assistant Commissioner, Division-I, CGST & Central Excise , Jamshedpur, Jharkhand filed an appeal before the Commissioner (Appeals) of CGST & Central Excise, Ranchi against the above-mentioned Adjudication Order dated December 18, 2026, to the extend that the Adjudicating Authority has dropped the penalty amounting to Rs. 3,68,72,21,158/-," Tata Steel said in its exchange filing.

|

The appeal, filed on June 16 by the Assistant Commissioner, CGST & Central Excise, Jamshedpur, challenges the December 18, 2025, adjudication order to the extent it waived the penalty.

|

The original show-cause notice, issued in June 2025, proposed disallowance of input tax credit for FY 2018-19 to FY 2022-23, with an aggregate GST demand of about Rs. 1,007.55 crore. Of this, Tata Steel said it has already paid Rs. 514.19 crore in the normal course, leaving an alleged exposure of Rs. 493.35 crore.

|

In December 2025, the adjudicating authority confirmed the tax demand of Rs. 493.35 crore, imposed a penalty of Rs. 638.83 crore and applicable interested, while dropping an earlier proposed penalty of Rs. 368.72 crore. Tata Steel subsequently moved the Jharkhand High Court, which granted a stay on all further proceedings in March 2026.

|

"This matter is, inter-alia, contingent upon the final adjudication of the issue concerning the issuance of show cause notices for multiple periods, which is presently sub judice before the High Court," Tata Steel said.

|

Tata Steel added that it has a good case on merit and hence will contest the same before the Appellate Authority within the statutory timelines, noting that the development has no impact on its financial or operational position, arising from the said appeal.

|

Source: The Economic Times

|

|

|

|

|

|

|

|

With the June 30 deadline for filing legacy appeals before the Goods and Services Tax Appellate Tribunal (GSTAT) fast approaching , tax professionals, chartered accountants and industry bodies have urged the Finance Ministry to extend the filing window, warning that persistent technical glitches on the GSTAT portal could prevent thousands of taxpayers from filing their appeals before the deadline.

|

The demand comes as taxpayers seek to file appeals arising from nearly nine years of litigation accumulated during the period when the Tribunal remained non-operational. Experts said the combination of a massive backlog, voluminous documentation and continuing portal-related issues has significantly constrained taxpayers' ability to meet the deadline.

|

According to Aditya Singhania, Founder of Trackase, the backlog is estimated at nearly four lakh to 4.5 lakh legacy appeals, while only around 36,929 appeals have been filed nationalwide so far.

|

"The ground reality is deeply concerning. Against an anticipated backlog of nearly four to four and a half lakh appeals accumulated over nine years of the Tribunal's non-operationality, only around 36,929 appeals have been filed nationally as of now," Singhania said.

|

He attributed the slow pace of filings to the teething troubles of the newly launched e-filing portal, including server time-outs, authentication challenges, payment gateway reconciliation issues and a filing structure that requires considerable time and effort to navigate.

|

Experts cite portal hurdles, record backlog

According to experts and representations submitted to the Finance Ministry, taxpayers continue to face multiple technical issues on the GSTAT portal, including session expiry, repeated login failures., Aadhaar authentication problems, Digital Signature Certificate (DSC) validation failures, payment reconciliation delays and incomplete integration between the Goods and Services Tax Network (GSTN) and the GSTAT portal.

|

Experts said taxpayers are also required to retrieve and compile extensive records accumulated over several years, including adjudication orders, invoices, reconciliations, e-way bills, ledger extracts and other supporting documents, making the filing process particularly time-consuming.

|

CA Nitin Bansal, State-President, BJP CA Cell Haryana, said the Finance Ministry has received several representations highlighting the practical challenges taxpayers are facing in filing appeals before the Tribunal.

|

"With the Tribunal becoming operational after nearly nine years, taxpayers must now prepare and file a substantial backlog of appeals within a limited window, many involving voluminous, multi-year records, even as the GSTAT e-filing portal continues to stabilise," Bansal said.

|

He added that extending the deadline would be revenue-neutral as the mandatory pre-deposit and other conditions would remain unchanged while ensuring genuine taxpayers are not denied their appellate remedy because of circumstances beyond their control.

|

Over-time extension sought

CA Sonu Goel, Chairman, Panipat Branch of the Institute of Chartered Accountants of India (ICAI), said a one-time extension would ensure disputes are decided on their merits rather than procedural constrints.

|

"One-time extension would safeguard taxpayers' right to appeal, uphold the principles of natural justice, and ensure that dispute are decided on merits rather than being defeated by procedural or technological constraints. This pragmatic relief would further reinforce the Government's commitment to ease of doing business while maintaining certainty and confidence in the GST ecosystem," Goel said.

|

Parag Mehta, Partner at N.A. Shah Associates LLP, said the portal continues to experience issues ranging from login failures and incorrect fee calculations to disappearing data.

|

"Considering the fact that the portal is not fully supporting the filing process and the number of appeals filed remains significantly lower than expected, the deadline should be extended. GSTAT is an important appellate remedy and taxpayers should not be deprived of that opportunity," Mehta said.

|

Bas association flags nationwide concerns

The Sales Tax Bar Association has also written to the Finance Ministry seeking an extension of the filing deadline, stating that taxpayers and tax professional across the country continue to face significant practical and technical difficulties while filing appeals through the GSTAT portal.

|

In its representation, the association said the present limitation period covers appellate orders accumulated over nearly nine years when the Tribunal remained non-functional, requiring taxpayers to retrieve historical records and prepare detailed documentation within a limited period.

|

The association highlighted recurring issues including server interruptions, repeated Aadhaar authentication and DSC validation failures, payment gateway reconciliation delays, manual duplication of information already available on the GSTN portal and challenges in uploading voluminous records.

|

It warned that if the deadline is not extended, thousands of taxpayers could lose the opportunity to pursue their statutory appeals because of technological and procedural constraints, potentially leading to avoidable litigation before various High Courts.

|

Prabhat Ranjan, Senior Director at Nexdigm, said extending the filing deadline has become "the need of the hour".

|

"The appellate process should be about the actual merits of the issues between both parties and not technical questions of delay. This is a taxpayer-friendly measure that will make GST dispute resolution processes more fair and credible," he said.

|

As of publication, the government has not announced any extension of the June 30 deadline for filing legacy GSTAT appeals. While the GSTAT has extended the period for relaxed scrutiny of filed appeals until December 31, 2026 , tax professionals, industry experts and representative bodies continue to seek a one-time extension of the filing deadline, arguing that additional time would enable taxpayers to exercise their statutory right of appeal without affecting revenue, as the mandatory pre-deposit requirements would continue to apply.

|

Source: The Economic Times

|

|

|

|

|

|

|

|

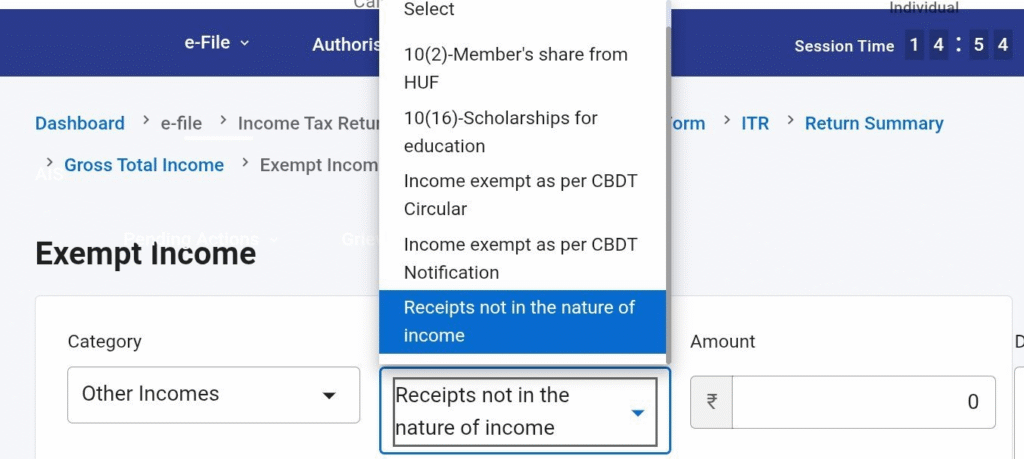

From AY 2026-27, the option to report 'Other Exempt Income' was removed.

|

Earlier, this was useful in situations such as:

|

- Sale of rural agricultural land/ Reporting of Gifts from Relatives - although disclosure was not required as same is not income .

|

The column of 'Other Income' under Exempt incomes has now been added.

|

|

|

|

|

|

|

|

|

|

|

The Hon’ble Supreme Court of India in the case of Commissioner of Central Goods and Service Tax, Navi Mumbai v. Hindustan Construction Company disposed of the case and held that the Court did not find any good ground and reason to interfere with the CESTAT Judgment, where it was held that no service tax should be charged on reimbursement of expenses because no service element is involved.

|

M/s. Hindustan Construction Company (“the Respondent”) was engaged in the business of providing taxable services under the head of ‘construction and other services’. For provision of such services, the Respondents were initially registered with the Service Tax department w.e.f. September, 2004 and subsequently, obtained the centralized registration w.e.f. May, 2007.

|

The Respondents incurred certain expenditure such as insurance premium, advance tax payment, stamp paper/duty, hotel expenses etc. on behalf of their group companies. The said expenses did not relate to any supplies made to the Respondents. Incurrence of such expenses were used to be reimbursed by the group companies at actual.

|

The Respondents also shared cost of common expenditure that has been incurred by them, with their group companies in accordance with company’s group policy. To recover the said expenses, the Respondents issued debit notes in favour of their group companies. The Respondents did not pay any service tax on the transactions made by them with their group companies, owing to the reason that there is no provision of any taxable service between them and it was mere arrangement of accounting such reimbursable expenditure.

|

During the course of audit of the books of accounts, the officers of the service tax department (“the Petitioner”) observed that the Respondents had recovered amounts from their related party by raising debit notes on two broad heads viz.,

|

- debit notes raised for reimbursement of various revenue expenses; and

- debit note raised for reimbursement of expenses incurred on behalf of group companies.

On the basis of such observation, the audit wing had alleged that the amount so recovered by the Respondents should be considered as a taxable service under the category of ‘business support service’, defined under Section 65 (104c) of the Finance Act, 1994 (“the Finance Act”).

|

Based on the audit report, the Department had issued periodical Show Cause Notices (“SCNs”) dated April 21, 2014, March 24, 2015 and February 19, 2016, proposing for recovery of the service tax demand for the period October, 2008 to March, 2015. The said SCNs were adjudicated vide Order-in-Original dated April 28, 2017, in confirming the proposed demands against the Respondents. On appeal against the said adjudication order dated April 28, 2017, this Tribunal vide Final Order dated September 24, 2021 had set aside the adjudication order and allowed the appeals in favour of the Respondent.

|

In continuation to the earlier show cause proceedings, the Department had issued another SCN dated March 09, 2018, proposing for recovery of service tax demand for the period April 01, 2015 to March 31, 2017. The said SCN was adjudicated by Commissioner, CGST & Central Excise vide Order-in-Original dated March 30, 2019 (‘the Impugned Order’), in confirming service tax demand of Rs.11,71,17,556/- along with interest. Besides, the Impugned Order has also imposed penalties of Rs. 1,17,11,756/- and Rs. 10,000/- under Section 76 the Finance Act and 77 the Finance Act, respectively.

|

Hence, aggrieved with the Impugned Order, the Respondent filed an Appeal before the Customs, Excise & Service Tax Appellate Tribunal (“CESTAT”).

|

Whether Service Tax is chargeable on reimbursement of expenses?

|

The CESTAT, Mumbai in 87430 of 2019 held as under:

|

- Observed that, in order to have the cost effectiveness, the Respondents incur various expenses for and on behalf of their group companies and cost of such services were recovered as reimbursement by way of raising debit notes. The service tax demands raised for the earlier period viz., October, 2008 to March, 2015 were set aside vide Final Order dated October 24, 2021, by relying upon the judgement of the Hon’ble Supreme Court in the case of Intercontinental Consultants and Technocrats Pvt. Ltd. .

- Noted that, the period involved in the present dispute is from April 01, 2015 to March 31, 2017. The phrase ‘service’ has been defined in Section 65B to mean ‘any activity carried out by a person for another for consideration, and includes a declared service…..’. On reading of the said definition clause, it transpires that in order to constitute a service, there must be involvement of more than one person i.e., a service provider and a service receiver; and that there must be ‘consideration’ for provision of such service. The phrase ‘consideration’ explained in the Explanation, appended to Section 67 has provided that ‘consideration’ includes any amount that is payable for the taxable services provided or to be provided. The said explanation clause, providing the meaning of the phrase ‘consideration’ was substituted by the Finance Act, 2015, dated May 14, 2015.

- Opined that, clause (ii) in the Explanation is relevant, which provides that any reimbursable expenditure or cost incurred by the service provider for provision of the taxable service is to be considered as ‘consideration’, for the purpose of levy of service tax thereon. In the present case, the Respondent herein have not provided any taxable service to their group companies, which is evident from both the SCN and the Impugned Order. The nature of activities undertaken by the Respondents were discussed by the original authority in the Impugned Order.

- Held that, the Impugned Order has not specifically discussed as to how and which particular services were provided by the Respondents to their group companies. Though, the original authority stated that the act of sourcing of the service for the group companies would be categorized under ‘business support service’, but has not dealt with the vital aspect regarding the manner of provision of a service, that too a taxable service. Rather, the facts of the case indicate that the mode of operation undertaken by the Respondents in making payment for the services and getting the same reimbursed are not for provision of any service, but are only reimbursement for the services procured for their group companies. Thus, the reimbursement of the cost/expenses incurred by the Respondents as per actual, cannot be regarded as consideration, flowing to the Respondents towards the taxable services provided by them. In other words, the amount claimed in the debit notes are for the simple reimbursement of the cost/expenses incurred by the Respondents in terms of the cost sharing arrangements with the group entities, with the only purpose of cost effectiveness, having no service element involved therein. in absence of any provision of service by the Respondents to their group companies, mere claim of reimbursement of actual cost and expenses should not form a part of provision of any taxable service, for payment of service tax thereon. Hence, the Impugned Order was set aside.

The Petitioner filed writ application before the Hon’ble Supreme Court in Civil Appeal Diary No. 53372/2024 which was disposed of because the Court did not find any good ground and reason to interfere with the CESTAT Judgment.

|

DISCLAIMER: The views expressed are strictly of the author and A2Z Taxcorp LLP. The contents of this article are solely for informational purpose and for the reader’s personal non-commercial use. It does not constitute professional advice or recommendation of firm. Neither the author nor firm and its affiliates accepts any liabilities for any loss or damage of any kind arising out of any information in this article nor for any actions taken in reliance thereon. Further, no portion of our article or newsletter should be used for any purpose(s) unless authorized in writing and we reserve a legal right for any infringement on usage of our article or newsletter without prior permission.

|

|

|

|

|

|

5. Lawgics by Ms.Nidhi Aggarwal

|

|

Ms. Nidhi Aggarwal is delighted to present GST Notes/Law in a simplified manner under the title “ Lawgics ”. The note is prepared in a series of PDFs encompassing GST Law and the interpretations thereof in simple manner. The author with a great vision to spread complex GST law in a simple manner amongst the taxpayers, tax professionals, students and knowledge seeker is presenting the Lawgics in piecemeal at regular interval.

|

|

|

|

|

|

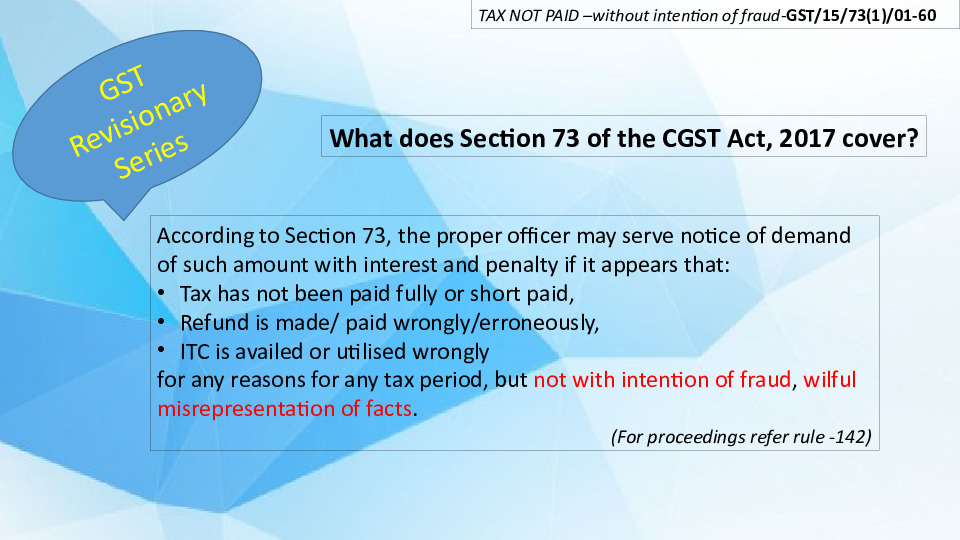

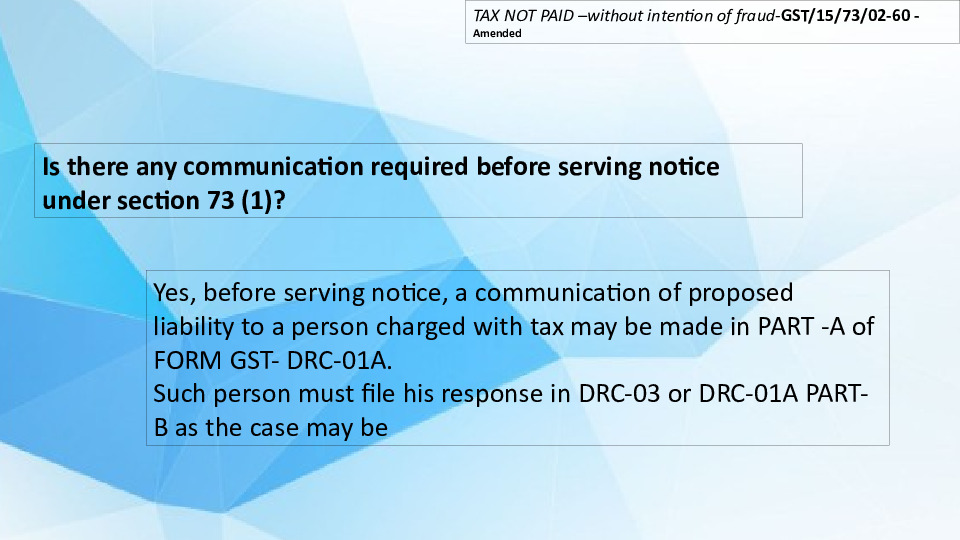

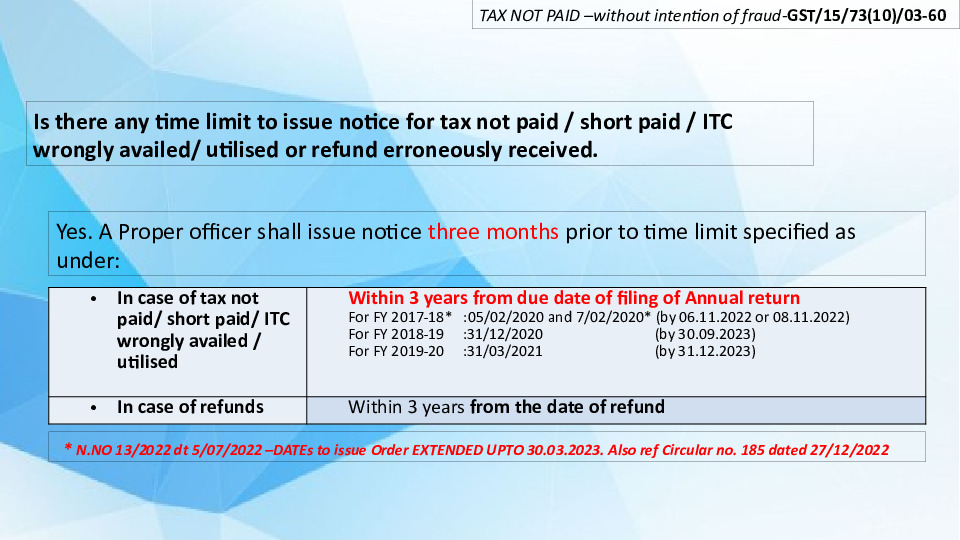

6. GST Notes by CMA Anil Sharma

1) Shri CMA Anil Sharma, Shri CMA Gurdev Singh Saini and Smt. CMA Bhawna Sharma posted Chapter-15 containing CGST Act in simple language in PPT format. This is to make dealers, professionals, academicians, students etc. understand the basics of GST laws. Each Chapter in CGST Act, 2017 is explained in the form of Slides as given below for easy understanding of the Act:

|

Chapter-15 slides given below:-

|

|

|

|

|

|

|

|

|

|

|

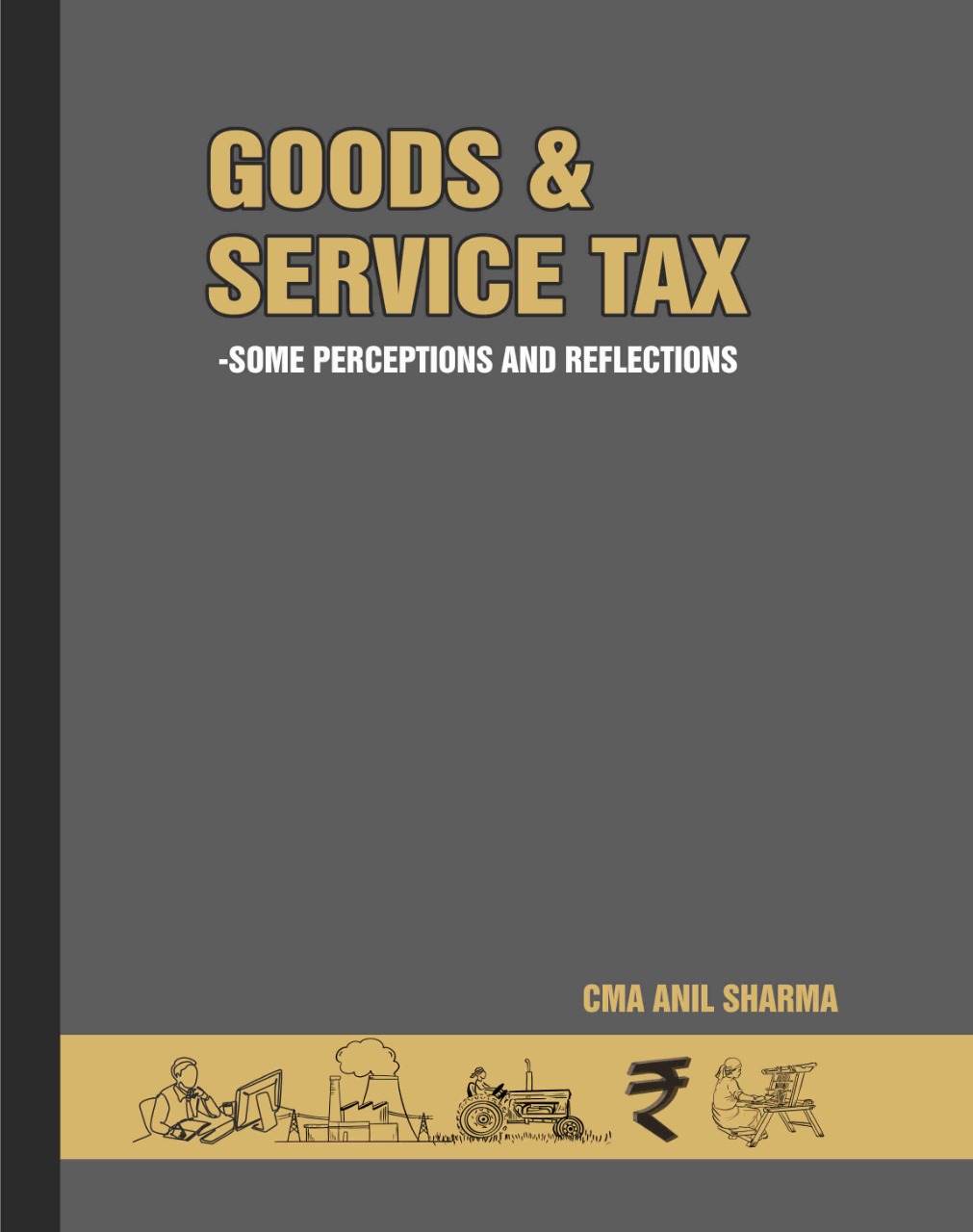

7) Book by CMA Anil Sharma

|

Book by CMA Anil Sharma, B.Com (Honrs), M.Com, FCMA co-author of the book "Handbook on GST Audit by Tax Authorities" has authored yet another book title Goods & Service Tax – Some Perceptions and Reflections. Buy now at Price Rs. 240- (Rs.300/- minus 20% Discount).

|

|

|

|

|

|

|

You wish to publish your Article?

|

If you wish to share your article with maximum readers then please send the article at taxupdate.otu@gmail.com. We shall publish it with all due credit to you.

|

|

|

|

|

|

|

Hope the above updates is of use to you. Please share your input and feedback at taxupdate.otu@gmail.com

|

|

|

|

|

|

|

Visit our website

|

OTU provides you

|

- Articles on various topics

|

|

- Media - GST, Income Tax & Press R.

|

|

- Notes / Newsletter etc.

|

|

|

|

|