|

onlinetaxupdate team wish to express sincere thanks to all the readers, authors, subscribers for the support extended to us. Please share your feedback at

|

taxupdate.otu@gmail.com or 7738647904

|

Newsletter 136 dated 23.09.2024

|

|

|

|

|

|

|

|

|

Dear Reader,

|

Please find newsletter for your reading and reference.

|

|

Index of the Newsletter

- Recent updates

- GST Council - 54th meet proposed

- Article

- Lawgics by Ms.Nidhi Aggarwal

- GST Notes by CMA Anil Sharma

- GST Daily by CA Pradeep Modi

- PPT/Handbook

- GST/IT/Customs in media

- Latest Update - Recap

|

|

|

|

|

|

|

GSTN Advisory no. 666 dated 01.07.2026

|

It is informed that the Aggregate Annual Turnover (AATO) functionality is currently being upgraded to enable automatic updation of AATO as subsequent returns are filed post amendment window. As this enhanced functionality is being deployed from 1st July 2026, the window for amendment of AATO by taxpayers for FY 2025-26 has been revised on the GST Portal.

|

GSTN had earlier issued an advisory dated 02 May 2022 regarding the functionality for amendment of Aggregate Annual Turnover (AATO) on the GST Portal, which was applicable for AATO till FY 2024-25. Under the said advisory, taxpayers were provided the facility to amend their turnover during the month of May.

|

In continuation thereof, it is informed that the timelines for submission of amendment applications and verification of amended AATO details by Tax Officers, in respect of FY 2025-26, have been revised.

|

To ensure greater consistency, accuracy, and uniformity in the reporting of AATO across various modules of the GST Portal, certain system-level enhancements are being implemented. Consequently, the revised timelines for amendment of AATO for FY 2025-26 by the taxpayers and subsequent action by the tax officers are as under:

|

AATO Amendment Application window for FY 2025-26

01 July to 31 July 2026

|

Review by jurisdictional Tax officer

01 Aug to 15 Aug 2026

|

Accordingly, the facility for amendment of AATO, which was earlier available during May as per the previous advisory, shall now be made available from 01 July to 31 July 2026 for FY 2025-26. The amended AATO details will be available for review of Tax Officers from 01 Aug to 15 Aug.

|

All taxpayers are requested to take note of the revised timelines and carefully review the AATO details while submitting the amendment application and ensuring that the amended details are accurate before submission.

|

In case of any difficulty or concern, taxpayers are advised to raise a grievance through the Self-Service Portal available on the GST Portal, along with all relevant details, to facilitate prompt and effective resolution.

|

|

|

|

|

|

|

|

GSTN Advisory no. 665 dated 01.07.2026

|

Gross and Net GST revenue collections for the month of June, 2026

|

|

|

|

|

|

|

|

GSTN is taking downtime to enhance its services on the GST Portal on 27.06.2026 from 12:00 AM onwards until 2:30 am of 27.06.2026.

|

|

We shall be enhancing services on the GST portal on : 27th June’26 12:00 AM onwards. GST Portal services will not be available until 27th June’26 02:30 AM. The inconvenience caused is regretted.

|

|

|

|

|

|

|

|

|

CBIC issued Notification No. 58/2026-Customs (N.T.) dated 22.06.2026 to hereby appoint the officer to exercise the powers and discharge the duties conferred on the officers for the purpose of adjudication of the show cause notices.

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Circular no. 28/2026-Customs dated 15.06.2026 regarding testing of samples of export consignments

|

|

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Circular no. 27/2026-Customs dated 15.06.2026 regarding Exemption of Merchant Overtime Charges (MOT) on International Cruise passengers and baggage clearance at cruise ports.

|

|

|

|

|

|

Export consignments to West Asia will continue to receive enhanced insurance cover against payment defaults until September 30, the Directorate General of Foreign Trade (DGFT) said in a notification on Monday.

|

Earlier, the enhanced cover for exporters taking credit risk insurance from Export Credit Guarantee Corporation (ECGC) was available for shipments to West Asia sent between March 16 and June 15.

|

The enhanced risk cover announced on March 19 was part of the Resilience and Logistics Intervention for Export Facilitation (RELIEF) scheme under the Export Promotion Mission (EPM) to support exports to West Asia in view of the Iran war.

|

"The eligibility timelines under Component II of the EPM RELIEF intervention are extended up to September 30, 2026 to support Indian exporters and mitigate logistics challenges arising out of the continuing West Asia Crisis," the DGFT said.

|

Source: The Economic Times

|

|

|

|

|

|

|

|

Directorate General of Foreign Trade (DGFT) issued Public Notice No. 17/2026-27 dated 04.06.2026 regarding Enlistment under Appendix 2E of FTP, 2023-Agency Authorised to issue Certificate of Origin (Non-Preferential)

|

|

|

|

|

|

|

|

Directorate General of Foreign Trade (DGFT) issued Trade Notice 07/2026-27 dated 03.06.2026 regarding request for comments on alignment of Schedule-II (Export Policy) of ITC (HS), 2022 consequent to amendments introduced under the Finance Act, 2026

|

|

|

|

|

|

Central Board of Direct Taxes (CBDT) issued notification no. 72/2026 dated 25.06.2026 to hereby approves deductions under section 45(3)(a)(i) of the Income-tax Act, 2025 and rules 32 and 34 of the Income-tax Rules, 2026 to the Public Health Foundation of India, Delhi (PAN: AABAP4445L) for Scientific Research under the category of University, college or other institution.

|

|

|

|

|

|

|

|

Central Board of Direct Taxes (CBDT) issued notification no. 71/2026 dated 25.06.2026 to hereby approves deductions u/s 45(3)(a)(i) of the Income-tax Act, 2025 and rules 32 and 34 of the Income-tax Rules, 2026 to the University of Hyderabad (PAN: AAAAU8109M) for Scientific Research under the category of university, college or other institution.

|

|

|

|

|

|

Central Board of Direct Taxes issued Guidelines dated 13.06.2025 vide F. No. 225/37/2025/ITA-II, regarding compulsory selection of returns for Complete Scrutiny during the Financial Year 2025-26 - procedure for compulsory selection in such cases.

|

2. The parameters for compulsory selection of returns for Complete Scrutiny during Financial Year 2025-26 and procedure for compulsory selection in such cases are prescribed as under:

|

3. Clarification: It is clarified that where return has been furnished in response to notice u/s 142(1) of the Act and such notice u/s 142(1) of the Act was issued due to the information contained in NMS Cycle/AIS/Statement of Financial Transactions (SFT)/ CPC-TDS information / information received from Directorate of I&CI, such return will not be taken up for compulsory scrutiny. Selection of such cases for scrutiny will be done through the CASS cycle.

|

4. Issuance of notice u/s 143(2) in certain cases:

|

4.1 Jurisdictional Assessing Officers (JAOs) shall upload the underlying documents for access by NaFAC in the following cases which are to be completed by NaFAC on or before 31.03.2026 and Notice u/s 143(2)/142(1) of the Act calling for information shall be served on the assess through NaFAC in these caes:

|

(a) Cases (other than search & seizures/survey) in which notices u/s 148 of the Act have been issued where return is either furnished or not furnished in response to notice u/s 148 of the Act.

|

(b) Cases in which notices u/s 142(1) of the Act calling for return, have been issued & no returns have been furnished.

|

4.2 Cases, where notices u/s 148 of the Act have been issued pursuant to search & seizure/survey actions conducted on or after the 01.04.2021 but before 01.09.2024, if lying outside Central Charges,

|

(i) where return is furnished, the Jurisdictional Assessing Officer (JAO) concerned shall serve the Notice u/s 143(2) of the Act and Pr.CIT/Pr.DIT/CIT/DIT concerned shall ensure that such cases transfer these cases to central charges u/s 127 of the Act.

|

(ii) where return is not furnished, these cases shall be transferred to central charges for further necessary action.

|

4.3 During the course of Search & Seizure action, information relating to some other persons, who may have one-off/very few or limited financial transaction(s) with the main assessee group covered in the search u/s 132/ 132A of the Act, may be found. Such persons are not integrally connected with the core business of the main assessee searched and do not belong to the same business group. Often such persons are also not residing in the same city as that of the main assesssee. In such cases, the relevant information is generally passed on to the jurisdictional AO for assessing them u/s 148 (for searches conducted/requisition made after 01.04.2021) of the Income-tax Act, 1961. It is clarified that such non-search cases selected u/s 148 of the Act are not required to be transferred to the Central Charges unless covered by the Board's guidelines under F.No. 299/107/2013-IT (Inv.III)/1568 dated 25.04.2014.

|

5. For Assessing Officers in International Taxation and Central Circle charges:

|

5.1 The cases shall be selected for compulsory scrutiny by the International Taxation and Central Circle charges following the above prescribed parameter at Para 2 with prior administrative approval of Pr.CIT/Pr.DIT/CIT/DIT concerned and these selected cases for compulsory scrutiny shall continue to be handled by International Taxation and Central Circle charges respectively, as earlier.

|

5.2 It is further clarified that communication to NaFAC for access and/or further action after selection for Compulsory Scrutiny will not apply to the International taxation and Central charges.

|

6. Time limit: As per the proviso to section 143(2) of the Act, the time limit for service of notice u/s 143(2) of the Act for the ITRs filed in the Financial Year (FY) 2024-25 which are selected for Compulsory Scrutiny is 30.06.2025.

|

7. These instructions may be brought to the notice of all concerned for necessary compliance.

|

|

|

|

|

|

Central Board of Direct Taxes issued Circular no. 4 of 2026 dated 31.03.2026 regarding Document Identification Number (DIN).

|

|

|

|

|

|

Press release ID 2279424 dated 30.06.26

|

The Government had earlier provided a full Customs Duty exemption on imports of critical petrochemical products till 30th June 2026, as a temporary and targeted relief in view of the conflict in West Asia and the consequent disruptions in global supply chains.

|

The exemption was provided to ensure sufficient availability of petrochemicals in the domestic market as Indian petroleum companies had been asked to concentrate on the production of LPG during this period. As the situation is gradually normalizing, to ensure a smooth and non-disruptive transition for the affected sectors, it has been decided to extend the said exemption by a further period of 15 days, that is, till 15th July 2026.The list of products covered remains the same as notified earlier.

|

The Government remains committed to supporting India's manufacturing sector. As before, the exemption is expected to benefit a wide range of sectors dependent on petrochemical feedstock and intermediates, including plastics, packaging, textiles, pharmaceuticals, chemicals, automotive components and other manufacturing segments. This will also provide relief to consumers of final products.

|

Link to previous press note issued:

|

|

|

|

|

|

|

|

The GST Council on Sunday constituted a 13-member Group of Ministers (GoM) to suggest GST rate on premiums of various health and life insurance products and submit its report by October 30.

|

Bihar Deputy Chief Minister Samrat Choudhary is the convenor of the GoM. The members of the panel include members from Uttar Pradesh, Rajasthan, West Bengal, Karnataka, Kerala, Andhra Pradesh, Goa, Gujarat, Meghalaya, Punjab, Tamil Nadu and Telangana.

|

The 54th GST Council meeting on September 9 decided to set up a GoM to examine and review the present tax structure of GST on life and medical insurance. A final call by the Council on the taxation of insurance premiums is likely to be taken in the next meeting in November based on the GoM report.

|

Currently, 18 per cent of Goods and Services Tax (GST) is levied on insurance premiums.

|

The Terms of Reference (ToR) of the panel also include suggesting tax rate of health/medical insurance including individual, group, family floater and other medical insurance for various categories like senior citizens, middle class, persons with mental illness. Also, suggest tax rates on life insurance, including term insurance, life insurance with investment plans whether individual or group and re-insurance.

|

"The GoM is to submit its report by October 30," 2024," said the Office Memorandum issued by the GST Council Secretariat on the Constitution of GoM on Life and Health insurance.

|

Some opposition-ruled states, including West Bengal, had demanded complete exemption of GST on health and life insurance premiums, while some other states were in favour of lowering the tax to 5 per cent. Even Transport Minister Nitin Gadkari had in July written to Finance Miniter Nirmala Sitharaman on the issue saying "levying GST on life insurance premium amounts to levying tax on the uncertainties of life."

|

In 2023-24, the centre and states collected Rs 8,262.94 crore through GST on health insurance premiums, while Rs 1,484.36 crore was collected on account of GST on health reinsurance premiums.

|

Sitharaman in her reply to a discussion on the Finance Bill in the Lok Sabha in August had said that 75 per cent of the GST collected goes to states and the Opposition members should ask their state finance ministers to bring the proposal to the GST Council.

|

|

|

|

|

|

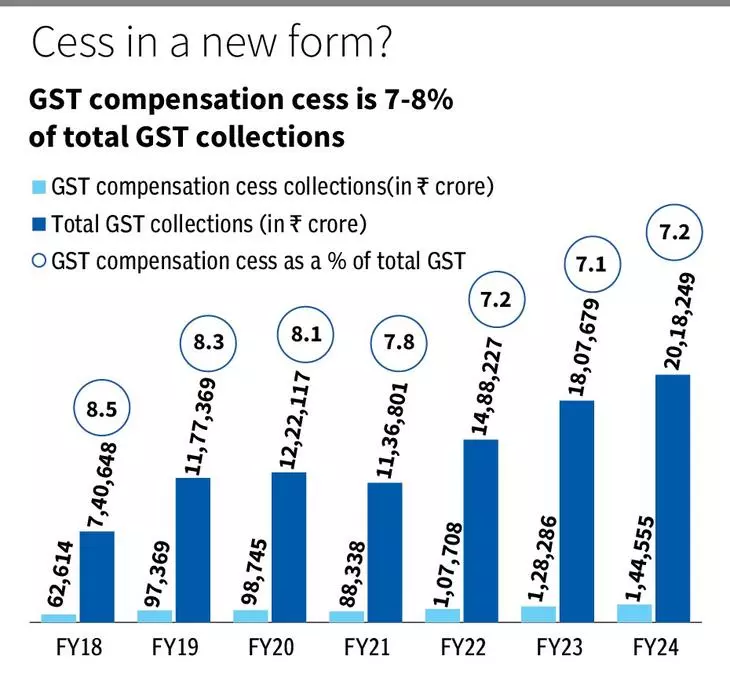

As the 54th GST Council Meeting last week formed a Group of Ministers (GoM) to decide the future of the GST compensation cess, data show that the tax component contributes substantially to the government coffers and merits continuation in new form once its levy ends in March 2026.

|

|

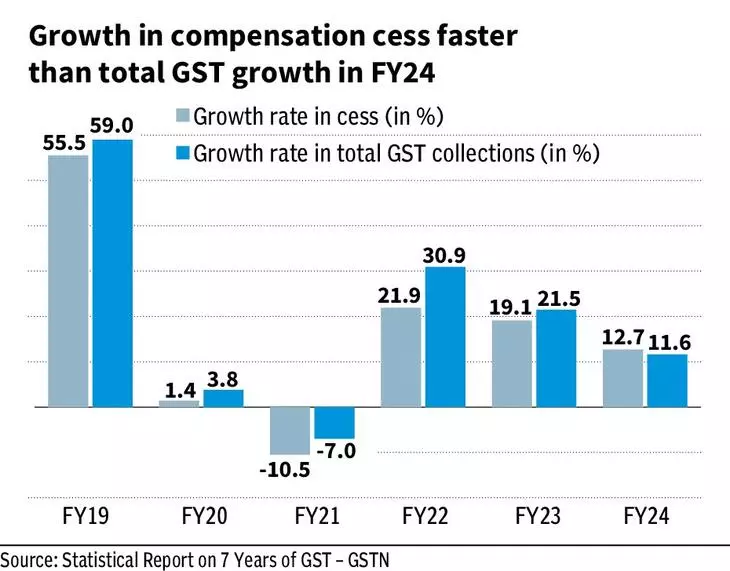

businessline analysis of the annual GST compensation cess collections from FY18 to FY24 shows that the tax contributed average 8 per cent to the total GST collections during the said years, and has been growing at almost the same rate as rise in overall GST collections. In fact, in FY24, the growth in cess outpaced that of total GST collections.

|

|

|

The GST compensation cess grew around 22 per cent in FY22 at ₹1.07 lakh crore, 19 per cent in FY23 to come in at ₹1.28 lakh crore, and 12.7 per cent in FY24 (₹1.44 lakh crore). Overall GST collections grew at 31 per cent, 21.5 per cent and 11.6 per cent during the same post-Covid years. The growth rate in Central Goods and Services Tax (CGST) is at 29 per cent, 19.7 per cent and 16 per cent in the period.

|

The cess is levied on supply of select so-called sin goods, luxury products and those with adverse environmental or health impacts. The list includes items such as tobacco, Pan Masala, carbonated beverages and also on products such as motor vehicles beyond certain capacity and coal products. It is also chargeable on certain goods imported to India.

|

|

“Industries like automobile, aerated beverages and others affected by the compensation levy were hoping for its discontinuation after the five-year period and then again after its extension for covering up the previous shortfall,” Abhishek Jain, Indirect Tax Head & Partner, KPMG, said. “The GoM is faced with a tough balancing act between industry expectations and the government’s interest in maintaining this key revenue source in some form,” he added.

|

|

|

While the levy on tobacco and related products helps in influencing consumer behaviour towards purchase of such goods, analysts also note that given the rising demand for large motor vehicles and redefinition of luxury goods, the GoM should also review items on which the cess is currently levied and rationalise it.

|

GST compensation cess was brought in as a measure by the Centre to meet its promise to the States to offer a 14 per cent CAGR in tax revenue for five years from the date of GST rollout. The payout to States ended in June 2022, but subsequently it was extended till March 2026, to repay the loan of around ₹2.7 lakh crore that the Centre borrowed during the pandemic period to meet the deficit.

|

Finance Minister Nirmala Sitharaman at the 54th Council meet said that government will likely clear the back-to-back loan and the interest thereon by January 2026 itself, and thus two months of compensation cess collections (February and March 2026) totalling to roughly ₹40,000 crore is likely to be surplus. “It shall no longer be ‘compensation cess’ post March 2026, but what is to be done with it, it will be decided by the GoM,” she said.

|

|

|

|

|

|

|

|

Author: R.SRIVATSAN, IRS, NACIN, Chennai

|

Automobile dealers using demonstration vehicles or demo cars for promoting sales can claim input tax credit (ITC) under the GST law.

|

However, no ITC would be available if demo cars are used by dealers for their own purpose during the course of the business.

|

The Central Board of Indirect Taxes and Customs (CBIC) said authorised dealers are required to maintain demo vehicles at their sales outlet as per dealership norms which are used for providing trial runs and for demonstrating features of the vehicle to the potential buyers.

|

These vehicles are purchased by the authorised dealers from the vehicle manufacturers against tax invoices and are typically reflected as capital assets in books of account of the authorized dealers.

|

As per dealership norms, these vehicles may be required to be held by the authorized dealers as demo vehicles for certain mandatory period and may, thereafter, be sold by the dealer at a written down value and applicable tax is payable at that point of time.

|

The demo vehicles are actually used by the authorized dealers to promote further sale of motor vehicles of the similar type and therefore, such vehicles appear to be used in the course or furtherance of business of the authorized dealers.

|

Obviously these vehicles should not be used for transportation of its employees or other passengers or for personal use.

|

Where such vehicles are capitalized in the books of accounts by the authorized dealer, the said vehicle falls in the definition of 'capital goods. ITC is available when no depreciation is claimed under Income Tax.

|

R.SRIVATSAN, IRS

NACIN, Chennai

|

|

|

|

|

|

Author: R.SRIVATSAN, IRS, NACIN, Chennai

|

The 54th GST Council meeting has recommended rectification processes related to the ITC for demands under section 73, 74, 107 and 108 of the CGST Act, 2017.

|

The Council recommended that section 118 and 150 of the Finance (No.2) Act, 2024, which provides for insertion of sub-section (5) and sub-section (6) in Section 16 of CGST 2017 retrospectively w.e.f 01.07.2017 may be notified at the earliest.

|

Issues related to wrong availment of Input Tax Credit (ITC) by the taxpayers.

|

Special procedure for rectification of orders u/s 148 of the CGST Act, 2017 will be followed by the class of taxable persons, against whom any order u/s 73 or 74 or section 107 or 108 of CGST Act has been issued confirming demand for wrong availment of ITC on account of contravention of provisions of sub-section (4) of section 16 of the CGST Act, but where such ITC is now available as per newly inserted provisions of sub-section (5) or sub-section (6) of section 16 of CGST Act 2017.

|

The wrong availment of ITC due to non-filing of returns by the sellers has caused a lot of trouble for the buyers.

|

In fact, section 16(4), CGST Act 2017 has succeeded in reducing these issues in related to the availment of ITC to an extent but still in many cases recipient of supply were being issued with the notice u/s 73, 74, 107 and 108 of CGST Act 2017, for no fault of them.

|

Therefore, the introduction of 16(5) and 16(6) of CGST Act, 2017 will resolve the issues on availment of ITC.

|

According to Section 16(5) and 16(6) CGST Act :

|

Notwithstanding anything contained in sub-section (4), in respect of an invoice or debit note for supply of goods or services or both pertaining to the Financial Years 2017-18, 2018-19, 2019-20 and 2020-21, the registered person shall be entitled to take input tax credit in any return under section 39 which is filed up to the thirtieth day of November, 2021.

|

Where registration of a registered person is canceled under section 29 and subsequently the cancellation of registration is revoked by any order, either under section 30 or pursuant to any order made by the Appellate Authority or the Appellate Tribunal or court and where availment of input tax credit in respect of an invoice or debit note was not restricted under sub-section (4) on the date of order of cancellation of registration, the said person shall be entitled to take the input tax credit in respect of such invoice or debit note for supply of goods or services or both, in a return under section 39,– (i) filed up to thirtieth day of November following the financial year to which such invoice or debit note pertains or furnishing of the relevant annual return, whichever is earlier; or (ii) for the period from the date of cancellation of registration or the effective date of cancellation of registration, as the case may be, till the date of order of revocation of cancellation of registration, where such return is filed within thirty days from the date of order of revocation of cancellation of registration, whichever is later.] The Council also recommended issuance of a circular to clarify the procedure and issues related to the implementation of the provision of 16(5) and 16(6) of CGST Act, 2017.

|

Lot of disputes, appeals, refunds and pre-deposit, refund of pre-deposits and similar obligations causing financial stresses on the business and procedural compliances by tax administration will get resolved by this progressive move.

|

|

|

|

|

|

Author: R.SRIVATSAN, IRS, NACIN, Chennai

|

by R.SRIVATSAN, IRS, NACIN, Chennai

|

RCM on Commercial Rent refers to the Reverse Charge Mechanism, where the recipient (tenant) is liable to pay GST on commercial rent.

|

Here is a comprehensive analysis of how RCM impacts commercial rent for discharging GST liabilities, taking case by case.

|

A: For Registered Landlords:-

|

If the landlord is registered under GST, they charge GST on the rent to the tenant and the tenant pays the GST to the landlord along with the rent, while the registered landlord discharges the GST liability.

|

B: For Unregistered Landlords:-

|

If the landlord is not registered under GST, the RCM applies, and the tenant (if registered) is responsible for paying the GST directly to the government.

|

C: Tenant Composition Optee:-

|

If the tenant is a GST composition taxpayer, the RCM will apply on the registered tenant liability becomes an extra cost because they cannot claim Input Tax Credit (ITC).

|

If the tenant is a GST regular taxpayer, they can claim the RCM liability as ITC reducing their tax burden.

|

RCM liability must be paid in cash only. ITC adjustment is not permissible.

|

The FCM does not apply to small landlords whose aggregate turnover is below the GST registration threshold (₹20 lakhs for most states, ₹10 lakhs for some special category states).

|

Additionally, if the tenant is unregistered under GST, RCM does not apply, and no GST is payable on the rent.

|

E: ITC (Input Tax Credit) for Tenants:-

|

Tenants paying GST under RCM can avail of Input Tax Credit (ITC) on the GST paid under RCM, provided they are using the property in the course or furtherance of business purposes.

|

Tax Rate on Commercial Rent

GST on commercial rent is currently taxed at 18% on the rent amount under the services category. This applies in all cases whether GST is paid by the landlord or under RCM by the tenant under direct charge.

|

The SAC code for renting of immovable property is 997212. This SAC code also applies to all forms of rental agreements such as long-term leases and short-term rentals.

|

The application of RCM on commercial rent has broad implications for tenants, landlords, and the overall real estate sector. While it shifts the tax burden from landlords to tenants, it ensures that GST is collected on rental transactions, even when landlords are unregistered.

|

For tenants, especially businesses, RCM means added responsibilities in terms of compliance and cash flow management, but the availability of ITC can help offset the GST paid under RCM.

|

|

The table summarises the essence of RCM on commercial renting.

|

|

|

|

|

|

|

|

|

Author: R.SRIVATSAN, IRS, NACIN, Chennai

|

The Hon'ble Guwahati High Court has quashed the validity of Notification No. 56/2023, CT, dt:23-12-2023, in the case of Shree Shyam Steel Vs UOI regarding the extension of time for passing orders under Section 73(9) of the CGST Act for the financial years 2018-19 and 2019-20.

|

The Government, exercising its authority under section 168A of the CGST Act, 2017, in conjunction with IGST Act 2017 has through Notification 56/2023 specifically extend the time limits as outlined below:

|

For the Financial Year 2018-19:

|

The deadline to issue orders related to tax recovery for this fiscal year was extended until April 30, 2024.

|

For the Financial Year 2019-20:

|

The deadline for orders regarding tax recovery in this fiscal year was extended until August 31, 2024.

|

This order of the Honourable Guwahati High court has answered several critical issues in terms of statutory interpretation, constitutional principles, and GST governance.

|

The bench noted that prima facie the notification bearing No. 56/2023 does not align with the provisions of Section 168(A) of the Central GST Act, 2017.

|

Section 168A, with its non-obstante clause grants the government overriding authority to extend due dates for completing proceedings and taking measures.

|

But without a proposal/ recommendation from GSTC, the government cannot issue the notification for extending the period u/s 168A of the CGST Act, 2017 and as such, the notification bearing No. 56/2023 on 28.12.2023 is ultra vires without legislative validity.

|

The notification cannot stand the scrutiny of law because the power to notify u/s 168A is granted exclusively when there is a force majeure.

|

The Court’s declaration that the notification is ultra vires Section 168A signifies that the Central Government exceeded its powers under this section.

|

Section 168A was introduced as a special provision to deal with extraordinary situations such as force majeure (e.g., COVID-19) and allows the Government to extend statutory time limits.

|

However, it must be based on recommendations from the GST Council.

|

In fact, in the 49th Meeting of the GST Council, the GSTC made a recommendation for extending the time limit for passing the order u/s 73(9) of the CGST Act, 2017 for the

|

FY 2017-2018 up to 31.12.2023

|

FY 2018-2019 up to 31.03.2024

|

FY 2019-2020 up to 30.06.2024.

|

According to the recommendation of the GST Council, a notification bearing No. 9/2023-CE was issued dated 31.03.2023 by the Central Board of Indirect Taxes and Customs.

|

However, GST Council has not made any proposal to date, and despite that, the CBIC has issued a Notification bearing No. 56/2023-CE on 28.12.2023 by extending the period to pass the order Under Section 73(9) of the CGST Act, 2017 for the Financial Year 2018-2019 and for the FY 2019-2020 which has been held unlawful.

|

The judgment emphasizes that executive decisions cannot supersede statutory requirements, especially in the absence of GST Council's recommendations.

|

This ruling is a direct reaffirmation of the importance of the GST Council's role as a constitutional body that balances federal interests in GST matters.

|

Section 168A stipulates that any relaxation of timelines must be in consonance with the recommendations of the GST Council.

|

The judgment thus underscores the principle that executive discretion is not absolute in GST matters and must be subject to the constitutional framework, wherein the GST Council plays a pivotal role in shaping policy.

|

This decision will obviously have significant implications for taxpayers who were caught in the disputes under Section 73(9) for the financial years 2018-19 & 2019&20.

|

The quashing of the notification implies that the statutory limitation periods for passing orders may not stand extended leaving the fate of numerous cases in uncertainty, a potential relief for taxpayers too, as any delay in proceedings beyond the statutory limits could invalidate the actions of tax officers.

|

This judgment could serve as a precedent/guidance for future litigation surrounding notifications or executive actions that seek to bypass statutory procedures or constitutional mandates under the GST regime.

|

|

|

|

|

|

Yes, the Honorable High Court of Madras in the case of Global Hardware vs. The State Tax Officer (W.P. (MD) No. 13164 of 2024 dated 21.06.2024) granted liberty to the Petitioner to file a statutory appeal before the Deputy Commissioner (GST-Appeal) within 30 days from the receipt of the court's order. The Honorable Court noted that the petitioner received an order dated 01.12.2023 for the assessment year 2022-23 and has approached WRIT Court long after the expiry of the Time limit for filing an Appeal u/s 107. The Honorable Court provided a procedural remedy while not addressing the substantive arguments, focusing on facilitating the appeal process despite the lapse in the statutory timeline. The Respondent was further directed to consider and dispose of the appeal on its merits within three months.

|

If the appeal is filed after the period of condonation permitted in section 107(4) (3+1 months), the Appellate Authority does not have statutory authority to condone the delay, not even if the reasons are ample and deserve to be entertained. The appeal must be dismissed for being fatally belated because the legislature has allowed Appellate authority this much authority and not more.

|

The Honorable Supreme Court has decided in Singh Enterprises v. CCE 2008 (221) ELT 163 that where the period of limitation is specifically provided in the statute, admitting appeals albeit for 'sufficient cause' would render statutory provisions impossible. And Appellate Authority thus being the denuded of authority to condone (due to lapse of maximum time permitted) is barred from examining the cause and condone the delays even for a 'good and sufficient' reason.

|

The Honorable Allahabad High Court in the case of M/s. Yadav Steels v. Additional Commissioner and Anr. and in the case of M/s. Abhishek Trading Corporation v. Commissioner (Appeals) and Anr. has decided that the Central Goods and Services Tax Act, 2017 is a special statute and a self-contained code in itself and Section 5 of the Limitation Act is no applicable to give power to First Appellate authority to condone the delay beyond statutory time limit allowed.

|

|

|

|

|

|

No, the Honorable Madras High Court in the case of Murugan Metals vs. The State Officer (ST) (W.P.No.16582 of 2024 dated 25.06.2024) set aside the impugned assessment order dated 28.12.2023 on the condition that the petitioner remits 5% of the disputed tax demand within two weeks from the date of receipt of a copy of the order. The Honorable Court observed that the petitioner's reply dated 11.01.2023 included the GSTR-3B returns for the assessment period 2017-18, along with a comparison statement between the GSTR-2A and GSTR-3B returns. However, the assessing officer did not appear to have considered these documents while confirming the tax proposal. Additionally, the petitioner failed to participate in subsequent proceedings or file the reconciliation statement in GSTR-9C. Considering these circumstances, the Honorable Court deemed it necessary to reconsider the case but also to impose conditions on the petitioner. The Honorable Court directed the respondent to provide the petitioner a reasonable opportunity, including hearing, and to issue a fresh order within three months from the date of receipt of the remittance. Consequently, the bank statement was raised.

|

Whether to celebrate such an order that remands back the case to the Proper Officer for another round of adjudication (re-adjudication) is a matter of choice and strategy. In the author's considered opinion, such orders are unable to fetch the desired relief because SCN is not vacated, only a short-term relief (at a cost) is provided in this long battle. The petitioner could have disputed the cause of action (2A v 3B) invoked, and the burden to proof would have been on the revenue to prove their case. Important to mention that mismatch/linear comparison of two data sets (GSTR-2A whose authorship is not with taxpayer v GSTR-3B) is meaningless in GST. Yes, it could raise suspicion, but without evidence, it is impossible to bring home the allegations levelled against the taxpayer.

|

|

|

|

|

|

Yes, the Honorable High Court of Allahabad in case of M/s. Anil Rice Mill vs. State of UP and 2 Others (WRIT TAX No. - 886 of 2023 dated 14.08.2024) dismissed the writ petition filed by the petitioner stating that the primary responsibility of claiming the benefit is upon the dealer to provide and establish the actual physical movement of goods, genuineness of transactions, etc. and if the dealer fails to prove the actual physical movement of goods, the benefit of ITC cannot be granted. The Honorable Court relied on the judgment of the Honorable Supreme Court in the case of State of Karnataka vs. M/s Ecom Gill Coffee Trading Private Limited (2023), which reinforces the principle that the burden of proving the legitimacy of an ITC claim lies with the purchasing dealer. The Honorable Court observed that the petitioner has only brought on record the tax invoices, e-way bills, and payment through the banking channel, but no such details such as payment of freight charges, acknowledgment of taking delivery of goods, toll receipts and payment thereof has been provided. Thus in the absence of these documents, the actual physical movements of goods and genuineness of transportation as well as the transaction cannot be established and in such circumstances, further no proof of filing of GSTR-2A has been brought on record, consequently, the authorities rightly initiated proceedings against the petitioner. In view of the facts as stated above, no interference is called for by this Court in the impugned orders.

|

Where self-assessment is challenged, the burden rests on the Revenue making the allegation and not on the registered person-suffering the allegation. The Burden of proof is not discharged by making the allegation. The Burden of proof is discharged only when a mountain of evidence commensurate with the nature of the allegation made is produced and appended to notice. Allegations of severe wrong-doing require proportionately substantial evidence. Evidence is not extracted of books of accounts or statements taken on-oath. Evidence is that proves something. Section 155 of the CGST Act places the burden to prove regarding "eligibility to credit" only on the taxpayer. Once, it is shown that all the conditions of section 16 are fulfilled, the taxpayer's burden is discharged and onus shifts on the department to prove their case

|

In the instance case, the petitioner could have disputed the allegation stating that being a trader, if the outward supplies are accepted to be genuine then inward supplies have to be genuine. And if inward supplies are in genuine and outward supplies are accepted to be genuine, then the allegation is deeply rooted in incomplete investigation, surmise and conjecture only. The Revenue cannot approbate and reprobate on the same issue. The taxpayer must have allowed the revenue to prove their case and in the absence of evidence in support of allegations, allegations are self-defeating.

|

This is classic case of poor strategy by the petitioner and in coming times, other taxpayers will have to face the heat of this order.

|

|

|

|

|

|

Recently, the Hon'ble Supreme Court directed the disposal of around 199 appeals based on monetary limits prescribed by the Revenue as a step towards reducing litigation.

|

This initiative will undoubtedly bring much-needed relief to both taxpayers and the department. But why stop there?

|

— Expanding the Initiative:

The same exercise should be carried out for all pending cases before High Courts, CESTAT, and the soon-to-be-constituted GSTAT to multiply the benefits.

|

— Identifying Covered Cases:

It's also worth identifying all cases where the point of law has been settled by the Hon’ble Supreme Court. Both the department and taxpayers can proactively withdraw such appeals, freeing up judicial resources to focus on new and unresolved issues and saving legal costs for all parties involved.

|

Ref. C.C.E. AND S.T., SURAT I vs BILFINDER NEO STRUCTO CONSTRUCTION LTD.

|

|

|

|

|

|

Blessed, that the recent ruling by Hon’ble Kerala High Court in the case of M/S. MUTHOOT FINANCE LIMITED ruled on 03.09.2024 aligns closely with the views I expressed in my article long ago (see screen shot below).

|

The court has reiterated that the Education Cess (EC), Secondary and Higher Education Cess (SHEC), and Krishi Kalyan Cess (KKC) can only be utilized for their specific purposes and not for any other tax payments. This decision also confirms that there cannot be any transitioning of these cesses under the CGST Act.

|

The court’s decision underscores that cesses, while levied similarly to taxes, are not given the same treatment.

|

|

Let’s wait for the final law on this!!

|

|

|

|

|

|

|

|

|

4. Lawgics by Ms.Nidhi Aggarwal

|

Ms. Nidhi Aggarwal is delighted to present judgment with a great vision to spread complex GST law in a simple manner amongst the taxpayers, tax professionals, students and knowledge seeker.

|

|

Recently added notes are listed below:

|

|

|

|

|

|

Synopsis: The Delhi High Court dismissed the writ petition involving fraudulent ITC claims, directing the petitioner to pursue appellate remedy u/s 107 of the CGST Act.

|

Caste name: Banson Enterprises & Anr. vs Assistant Commissioner CGST & Ors.

|

Citation: W.P. (C) 6503/2025 dated 15.05.2025

|

Authority: Delhi High Court

|

The petition challenges the Order-in-Original dated 02.02.2025 based on a Show Cause Notice (SCN) dated 03.08.2024 A search was conducted, and statements were recorded including that of one Director admitting to the issuance of fake invoices during the Central Excise period. It was alleged that the Petitioner issued goods-less invoices to enable fraudulent Input Tax Credit (ITC) claims amounting to Rs. 1.85 crore.

|

Contentions of the Petitioner:

|

SCN was issued by unauthorized officer, thus, violates Rule 142(1)(a) of CGST Rules. No pre-consultation as required under Rule 142(1A) of CGST Rules was issued. Consolidated SCN for multiple financial years was issued and challenge to such consolidated action is pending in a separate matter (Quest Infotech case).

|

Contentions of the Department:

The impugned order is appealable, hence writ is not maintainable. The Petitioner’s Director admitted to allegations. Natural justice was followed as the Petitioner received the SCN, filed a reply, and availed of personal hearing. Reliance must be made on SC judgments and Allahabad HC rulings emphasizing alternate remedy u/s 107 CGST Act.

|

Findings and Decision of the Court:

The Court refused to interfere under writ jurisdiction, citing:

|

- No breach of fundamental rights or principles of natural justice.

- Availability of a statutory remedy (appeal) under Section 107 CGST Act.

The Court noted that the Allegations involve serious misuse of ITC, requiring fact-based adjudication, not suited for writ jurisdiction. Thus, the Petitioner was granted liberty to file appeal, and if filed with pre deposit, the appeal shall not be dismissed on limitation.

|

|

|

|

|

|

|

|

Synopsis: GST RC cancellation is not justified as petitioner was not given fair opportunity to respond.

|

Case Name: M/s. Genius Orthos Industries VS Union of India & Ors.

|

Citation: WRIT TAX No. 542 of 2023 dated 24.04.2025

|

Authority: Allahabad High Court

|

The petitioner was engaged in the business of surgical goods and its GST registration was cancelled on 19.12.2022 after a physical verification of its premises allegedly found no inputs, finished goods, or workers. A show cause notice was issued prior to cancellation, but the petitioner claimed they were not informed of the specific material findings leading to the cancellation. The appeal against the cancellation was also dismissed.

|

Contentions of the Petitioner:

|

The principles of natural justice were violated, as no proper notice of the specific material against them was given. Cancellation was based on vague grounds, and the watchman at the premises had confirmed that business activities were conducted, albeit irregularly. Rule 25 of the CGST Rules and Form GST REG 30 was not referenced in actual SCN.

|

Contentions of the Department:

|

The petitioner had due knowledge of the discrepancies found during physical verification and failed to provide a satisfactory explanation. Claimed that the cancellation order was justified due to absence of business activity at the registered premises.

|

Findings and Decision of the Court:

|

The High Court found that the cancellation was done without due process, especially considering that:

|

- The material used for cancellation was never properly shared with the petitioner.

- The statement of the watchman indicating occasional business activity was ignored.

- The physical verification report (GST REG-30) was not referenced in the show cause notice.

Thus, impugned cancellation and appellate orders were quashed and the matter was remanded to the proper authority for fresh adjudication within three months, ensuring that a reasoned and speaking order is passed after an Opportunity of hearing is granted. The petitioner may submit relevant evidence.

|

|

|

|

|

|

|

|

Synopsis: Rejection of appeal on ground that appeal was not filed electronically under Rule 108 of CGST Rules, 2017 is invalid in case of non availability of order–in–original on GST portal and Appeal being filed manually.

|

Case Name: M/s Appolo Sesame Industries & Anr. VS Assistant Commissioner of CGST, Division X, Nadiad & Ors

|

Citation: R/Special Civil Application No. 571 of 2025 dated 24.04.2025

|

Authority: Gujarat High Court

|

The petitioners challenged the rejection of their appeal against an Order-in-Original dated 30.10.2023. They had filed the appeal manually in Form GST APL-01, as the order was not available on the GST portal, making electronic filing impossible. Despite this, the Appellate Authority rejected the appeal on 27.09.2024, stating it was not filed electronically, as required under Rule 108(1) of the CGST Rules, 2017.

|

Contentions of the Petitioner:

|

The order-in-original was not available on the portal, so manual filing was the only viable option. A pre-deposit of 10% of the disputed dues was paid. The Appellate Authority ignored the proviso to Rule 108(1), which allows manual filing if the order is unavailable electronically. The Appellate Authority failed to issue the mandatory provisional acknowledgment, despite receiving the appeal.

|

Contentions of the Department:

|

The appeal was filed offline without fulfilling electronic filing requirements. The Appellate Authority argued that procedural rules were not followed, hence the rejection was valid.

|

Findings and Decision of the Court:

|

The High Court found that the Appellate Authority failed to apply its mind to the facts. It held that the rejection of the appeal violated Rule 108(1) of the CGST Rules, as manual filing is permitted when the order is not available on the portal. The impugned rejection order was set aside and the matter was remanded to the Appellate Authority to hear and decide the appeal on merits.

|

|

|

|

|

|

|

|

Synopsis: The demand order was quashed on the ground that the hearing notices must not be merely uploaded on portal but also e-mailed to petitioner.

|

Case Name: Shri Krishna Sales VS Commissioner of Delhi Goods and Service Tax & Ors.

|

Citation: W.P. (C) 5524/2025 dated 29th April, 2025

|

Authority: Delhi High Court

|

Brief facts of the case:

The petitioner challenged the Show Cause Notice (SCN) dated 26.09.2023 and demand order dated 25.12.2023, issued by the Delhi GST authorities. The challenge also extended to Notification No. 09/2023 Central Tax dated 31.03.2023, which extended the time limits for adjudication under Section 73 of the CGST Act. The SCN was only uploaded under the "Additional Notices and Orders" tab on the GST portal and did not come to the petitioner’s notice. The petitioner filed a rectification application, which was considered time-barred.

|

Contentions of the Petitioner:

The SCN and subsequent hearing notices were not properly served, being uploaded in a location on the portal that made them easy to miss. The notification extending limitation was issued improperly under Section 168A without valid GST Council approval and is under challenge before the Supreme Court (SLP No. 4240/2025).The demand order was passed ex parte without giving a fair opportunity to respond.

|

Contentions of the Department:

The SCN was uploaded properly as per current GST portal functionality. The notification extending time limits is valid and backed by GST Council recommendation (in some cases), with related petitions already under consideration in the Supreme Court. The petitioner’s application for rectification was rightly rejected due to limitation bar.

|

Findings and Decision of the Court:

The demand order dated 25.12.2023 was set aside. The Court allowed the petitioner to file a reply to the SCN within 30 days. The hearing notice must be communicated not just through the portal but also via email. The adjudication order shall be passed afresh, after granting a personal hearing. The outcome of this case will be subject to the final decision of the Supreme Court in the pending SLP on the validity of the notifications.

|

|

|

|

|

|

|

|

Synopsis: Notification dated 11.03.2022 & 25.11.2024 confers power to Principal Commissioner Delhi North and Delhi West to issue notices under Section 73 & 74 of CGST Act, 2017.

|

The petitioner challenged a Show Cause Notice (SCN) dated 24.07.2024 and Order-in-Original dated 02.02.2025, issued for alleged fraudulent availment of Input Tax Credit (ITC) through fictitious and non existent firms. The case was based on an extensive investigation involving over 87 entities, and a criminal complaint was also filed under Section 132(1)(b) of the CGST Act, 2017. The petitioner participated in the proceedings and submitted a reply to the SCN but later objected to the jurisdiction of the adjudicating authority.

|

Contentions of the Petitioner:

The personal hearing was improper, and the order was passed without following due process. The authority that adjudicated the matter (CGST Commissionerate Delhi North) lacked jurisdiction. The correct authority was claimed to be CGST Delhi West. A Corrigendum, issued on 28.01.2025 (after the hearing), was alleged to be backdated and manipulated to rectify the jurisdiction issue.

|

Contentions of the Department:

|

The department cited two notifications: Notification dated 11.03.2022 granted jurisdiction to Principal Commissioner, Delhi North and Notification dated 25.11.2024 extended jurisdiction to both Delhi North and Delhi West. The department argued that the adjudicating authority had valid jurisdiction and that due opportunity of hearing was provided to the petitioner. Petitioner’s challenge to jurisdiction was unfounded, and their remedy lies in filing an appeal under Section 107 of the CGST Act.

|

Findings and Decision of the Court:

The High Court held that jurisdiction was validly established via the cited notifications. The petitioner was directed to file an appeal before the Appellate Authority under Section 107. The court clarified that if the appeal is filed within 30 days, along with mandatory pre-deposit, it shall not be dismissed on limitation grounds and shall be heard on merits.

|

|

|

|

|

|

5. GST Notes by CMA Anil Sharma

1) New slides on GST Circulars is added in the Notes section titled as "Capsules".

|

- Total 25 slides in capsule-01 is added

|

|

|

|

|

|

|

|

6. GST Daily by CA Pradeep Modi

CA Pradeep Modi is presenting judgment analysis under title 'GST Daily - Stay yourself updated'

|

|

|

|

|

|

THE HON'BLE ALLAHABAD HIGH COURT IN THE CASE OF Vibhuti Tyres V/s State of U.P., decided on 7-5-2025

|

✔️ Is it justified that GST order with higher demand than show-cause notice?

|

👉 The Hon'ble High Court Judgement:-

|

✔️ Where in show-cause notice amount representing tax, interest and penalty was indicated as Rs. 8,81,080, but in order, much higher demand was raised at Rs. 32,97,336, same was in violation of section 75(7); matter was to be remanded back.

|

Section 75 of Central Goods and Services Tax Act, 2017

|

|

|

|

|

|

7. PPT/Handbook on GST

|

|

|

|

8. GST/Income Tax in Media

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Recap of Latest updates posted on 01.07.2026

|

From AY 2026-27, the option to report 'Other Exempt Income' was removed. Now it is being restored.

|

To commemorate nine years of the Goods and Services Tax (GST), the Central Board of Indirect Taxes and Customs (CBIC) organized a special celebration ..

|

Gross and Net GST revenue collections for the month of June, 2026

|

It is informed that the Aggregate Annual Turnover (AATO) functionality is currently being upgraded to enable automatic updation of AATO

|

Goods & Services Tax Appellate Tribunal (GSTAT) issued clarification on the Form of dresses or robes to be worn by members.

|

In a dramatic twist, the Central Bureau of Investigation (CBI) on Tuesday arrested senior IAS officer Pardeep Kumar on the very day he retired, tightening its grip on the massive Rs 593-crore Haryana government funds scam.

|

When the Goods and Services Tax (GST) was implemented on July 1, 2017, one of its central promises was to eliminate tax cascading and allow seamless flow of input tax credit (ITC) across the value chain.

|

Now that the income tax return filing time is here you can start the process by first preparing your tax return information and data.

|

|

|

|

|

|

|

|

|

Recap of Latest updates posted on 30.06.2026

|

Complete CGST, IGST, and Compensation Cess Acts & All Rules and GSTAT Rules

|

The government has extended the due date for filing of appeal before the Goods and Services Tax Appellate Tribunal (GSTAT) under section 112(1) read with section 112(3) to 31.07.2026.

|

Centre has extended the last date for filing appeals before the Goods and Services Tax Appellate Tribunal (GSTAT) to July 31, 2026, giving taxpayers an additional month to submit their cases after a surge in filings led to technical difficulties on the GSTAT portal.

|

GST & IDT Committee has requested the Chairman, IDT Committee, ICAI, New Delhi to urgently represent before the respective forums for the date extension of GSTAT, i.e., 30-Jun-2026.

|

The Union government on Tuesday granted a six-month extension to the tenure of Central Board of Direct Taxes (CBDT) Chairman Ravi Agrawal till December 2026.

|

The central government is working on a scheme to bear 90 per cent of the CBAM compliance costs for MSMEs as exporters grapple with the European Union's new carbon border tax that came into force this year..

|

In a major operation the officers of the Directorate of Revenue Intelligence (DRI) successfully dismantled a trans-border gold smuggling syndicate and seized 15 kg foreign-origin smuggled gold, valued at approximately Rs. 21.40 crore, operating from Delhi.

|

The Government had earlier provided a full Customs Duty exemption on imports of critical petrochemical products till 30th June 2026…

|

Export consignments to West Asia will continue to receive enhanced insurance cover against payment defaults until September 30, the Directorate General of Foreign Trade (DGFT) said in a notification on Monday.

|

The Hon'ble Madras High Court pronounced on 08.06.2026 in the case of M/s. Fastenex Private Limited that GST Notices u/s 74 Cannot Fail Solely Because Multiple Financial Years Are Covered.

|

|

|

|

|

|

|

|

|

Recap of Latest updates posted on 29.06.2026

|

MCTC made a representation to FM Smt. Nirmala Sitharaman, on 26.06.2026 requesting an extension of the deadline for filing GSTAT appeals from 30th June 2026 to 31st December 2026.

|

Tax professionals, chartered accountants and industry bodies have urged the Finance Ministry to extend the filing window, warning that persistent technical glitches on the GSTAT portal could prevent thousands of taxpayers from filing their appeals before the deadline.

|

On the occasion of 9th GST Day to be celebrated on 1st July, 2026 the CBIC has decided to grant Certificate of Meritorious Service (CBIC-CMS) to the following officers:

|

Businesses shifting their principal place of business to a new GST jurisdiction will not have to restart pending tax proceedings..

|

Commerce ministry has convened a meeting of stakeholders on June 30 to discuss issues related to SEZs, including reforms aimed at harmonising export promotion schemes and easing business operations in the enclaves.

|

Tata Steel Limited said tax authorities have filed an appeal seeking restoration of penalties worth Rs. 368.72 crore that were earlier dropped in a GST adjudication order

|

GSTAT , Vijayawada Bench, Andhra Pradesh will be functioning from its new premises at Mangalagiri, Guntur from 01.07.2026

|

The Hon’ble Madras High Court in P. Baskaran set aside the order imposing interest and penalty u/s 74 of CGST Act and remanded the matter for fresh consideration on the applicability of Section 74

|

The Hon’ble Madras High Court (Madurai Bench) in Tvl. Manickavasagam S. set aside the assessment order passed under Section 74 of the TNGST Act pertaining to levy of GST on seigniorage fees

|

The Hon’ble Gauhati High Court in M/s Metal Syndicate and Another set aside the OIO and the OIA confirming GST demand of Rs. 78,70,952/- along with interest and equivalent penalty, and held that a bona fide purchasing dealer cannot be denied ITC merely on account of the supplier’s failure to deposit the tax collected with the Government.

|

The Hon’ble Allahabad High Court in Ashish Tyagi allowed the habeas corpus petition and declared the arrest and consequent detention of the assessee under Section 132 of the CGST Act as illegal

|

|

|

|

|

|

|

|

|

Recap of Latest updates posted on 28.06.2026

|

CBDT issued notification no. 71/2026 dated 25.06.2026 to hereby approves deductions to the University of Hyderabad for Scientific Research under the category of university, college or other institution.

|

CBDT issued notification no. 72/2026 dated 25.06.2026 to hereby approves deductions under section 45(3)(a)(i) of the Income-tax Act, 2025 to the Public Health Foundation of India, Delhi for Scientific Research under the category of University, college or other institution.

|

Indian enterprises are rapidly advancing in artificial intelligence (AI) adoption and a growing cohort has embedded AI into the core of operations.

|

Several important financial changes are set to take effect on July 1, 2026. These changes could impact taxpayers, bank customers, credit card users, passport applicants and Aadhaar card holders.

|

DRI has successfully unearthed and dismantled a highly organised gold smuggling syndicate operating through Mumbai Airport.

|

|

|

|

|

|

|

|

|

Recap of Latest updates posted on 27.06.2026

|

All officers and staff of GSTAT, Ranchi Bench, are hereby directed to remain available on 28.06.2026 (Sunday) and extend all necessary assistance for resolving any last-minute difficulties…

|

KSCAA has submitted a representation highlighting practical and procedural issues faced by taxpayers and professionals in relation to GSTAT…

|

Kolkata is likely to host the 57th meeting of the GST Council next month, sources said, although the Union Finance Ministry has not yet officially confirmed the venue or the schedule.

|

Sources indicated that Das is being considered for the post of Union finance minister, while the incumbent , Nirmala Sitharaman, is expected to be shifted to the human resource development (HRD) ministry.

|

Mr. S.K. Rahman, Member (Technical), GST Appellate Tribunal, Chennai Bench address audience at BCAS 20th Residential Study Course on GST held at ITC Grand Chola, Chennai on 26th, June, 2026.

|

Adv. Ashu Dalmia of ADA Law Chambers, prepared this PPT on topic "GST Litigation - Key issues & Case laws".

|

Author: Abhishek Goyal M.Com, FCS, LLB | Edition: 1st Ed. 2026 | Publisher: Bharat Law House

|

|

|

|

|

|

|

|

|

Recap of Latest updates posted on 26.06.2026

|

EPFO has announced that its member portal, employer portal and UMANG app services will be temporarily unavailable due to scheduled system migration from June 26 to 30.

|

CBIC issued Circular no. 255/01/2026-GST dated 25.06.2026 to provide Clarification regarding jurisdiction in cases involving migration/ transfer of …

|

GSTN is taking downtime to enhance its services on the GST Portal on 27.06.2026 from 12:00 AM onwards until 2:30 am of 27.06.2026.

|

Residents living along Punjab’s State boundary with Himachal Pradesh, including traders, truck operators and taxi drivers, have united under the banner of the ‘Sangarsh Morcha’ to oppose Himachal Pradesh’s vehicle entry tax.

|

US Treasury Secretary Scott Bessent said tariff rates could return to their previous levels if ongoing Section 301 investigations conclude successfully, signaling the Trump administration intends to preserve much of its tariff framework even after shifting away from emergency powers.

|

Many market participants believe that the South Korean market has also been weighted down by the government's new proposal to tax unrealised gains.

|

Author: Abhishek Goyal M.Com, FCS, LLB | Edition: 1st Ed. 2026 | Publisher: Bharat Law House

|

|

|

|

|

|

|

|

|

Sales Tax Bar Association (Regd.) (STBA) made representation for extension of the time limit for filing appeals before the Goods and Services Tax Appellate Tribunal (GSTAT) vide letter reference STBA/2026/25 dated 25.06.2026

|

Madanapalle police in Annamayya district arrested two interstate accused for allegedly cheating a Bengaluru-based techie from Tirupati district.

|

Exporters flagged delays in EPCG and Advance Authorisation approvals, difficulties in updating Importer-Exporter Code profiles, customs clearance backlogs, digital signatures on online portals, and pending Integrated Goods and Services Tax (IGST) refunds.

|

The Uttar Pradesh Electricity Regulatory Commission (UPERC) has ruled that the reduction in GST on renewable energy equipment from 12% to 5% will be treated as a “Change in Law” event under power purchase agreements signed under the PM-KUSUM Component-C2 scheme.

|

A Kanpur man is making headlines after he received relief from the Income Tax Appellate Tribunal (ITAT) in a case involving a Rs 1.95 crore trading loss incurred through his wife’s account.

|

|

|

|

|

Hope the above updates is of use to you. Please share your input and feedback at taxupdate.otu@gmail.com

|

|

|

|

|

|

|

|

|

Visit our website

|

OTU provides you

|

- Articles on various topics

|

|

- Media - GST, Income Tax & Press R.

|

|

|

|

|