|

|

|

|

|

|

|

|

This website contains information about recent changes mainly in GST laws. It also contains Articles on various topic in GST. Please visit the website and read more.

|

|

|

|

Dear Reader,

|

Please find newsletter for your reading and reference.

|

|

Newsletter no.98 dated 20.08.2023

|

|

|

Index of the Newsletter

- Recent updates

- GST in media

- GST Portal

- Lawgics by Ms. Nidhi Aggarwal

- GST notes by CMA Anil Sharma

|

|

|

|

|

|

|

The Ministry of Finance on Thursday extended the deadline by two months till December 31 for submitting claims to settle pending disputes relating to government contracts.

|

The Vivad se Vishwas II scheme was launched on July 15 to settle disputes in government contracts and the last date for submitting claims by contractors was October 31.

|

The scheme is applicable to all domestic contractual disputes where one of the parties is either the government of India or government undertakings.

|

The Department of Expenditure said “It has been decided that the claims under the Vivad se Vishwas II scheme can now be submitted till December 31, 2023.”

|

Under the scheme, for court awards passed on or before April 30, 2023 the settlement amount offered to the contractor will be up to 85 per cent of the net amount awarded/upheld by the court.

|

|

|

|

|

|

The Income-tax Rules,1962 is amended vide the Income tax (Eighteenth Amendment), Rules, 2023. They shall come into force with effect from the 1st day of September, 2023.

|

|

|

|

|

|

|

|

CBDT has issued a Notification no. G.S.R. 604(E) dated 16.08.2023 providing for the computation of income chargeable to tax under section 56(2)(xiii) of any sum received under a life insurance policy.

|

MINISTRY OF FINANCE

(Department Of Revenue)

(CENTRAL BOARD OF DIRECT TAXES)

NOTIFICATION

New Delhi, the 16th August, 2023

|

G.S.R. 604(E).—In exercise of the powers conferred by clause (xiii) of sub-section (2) of section 56, read with section 295 of the Income-tax Act, 1961 (43 of 1961), the Central Board of Direct taxes hereby makes the following rules further to amend the Income-tax Rules,1962, namely:─

|

1. Short title and commencement: - (1) These rules may be called the Income tax Amendment (Sixteenth Amendment), Rules, 2023.

|

(2) They shall come into force on the date of their publication in the Official Gazette.

|

2. In the Income-tax Rules, 1962, after rule 11UAC, the following rules shall be inserted, namely:—

|

“11UACA Computation of income chargeable to tax under clause (xiii) of sub-section (2) of section 56. - For the purpose of clause (xiii) of sub-section (2) of section 56, where any person receives at any time during any previous year any sum under a life insurance policy, then, the income chargeable to tax under the said clause during the previous year in which such sum is received shall be computed in the following manner, namely: —

|

(i) where the sum is received for the first time under the life insurance policy during the previous year (hereinafter referred to as first previous year), the income chargeable to tax in the first previous year shall be computed in accordance with the formula,—

|

A = the sum or aggregate of sum received under the life insurance policy during the first previous year; and

|

B = the aggregate of the premium paid during the term of the life insurance policy till the date of receipt of the sum in the first previous year that has not been claimed as deduction under any other provision of the Act;

|

(ii) where the sum is received under the life insurance policy during the previous year subsequent to the first previous year (hereinafter referred to as subsequent previous year), the income chargeable to tax in the subsequent previous year shall be computed in accordance to the formula,—

|

C = the sum or aggregate of sum received under the life insurance policy during the subsequent previous year; and

|

D = the aggregate of the premium paid during the term of the life insurance policy till the date of receipt of the sum in the subsequent previous year not being premium which –

|

(a) has been claimed as deduction under any other provision of the Act; or

|

(b) is included in amount ‘B’ or amount ‘D’ of this rule in any of the previous year or years

|

Explanation .– For the removal of doubts, it is clarified that the sum received under a life insurance policy would mean any amount, by whatever name called, received under such policy which is not to be excluded from the total income of the previous year in accordance with the provisions of clause (10D) of section 10, other than the sum–

|

(a) received under a unit linked insurance policy; or

|

(b) being the income referred to in clause (iv) of sub-section (2) of section 56.”.

|

SOURABH JAIN, Under Secy.

|

Note: The principal rules were published in the Gazette of India, Extraordinary, Part-II, Section 3, Sub-section (ii) vide notification number S.O. 969(E), dated the 26th March, 1962 and was last amended vide notification number G.S.R. 595 (E) dated 9th August, 2023.

|

|

|

|

|

|

|

|

GSTN has prepared an informative resource in the form of an e-invoice glossary and a step-by-step guide for your reference.

|

You can access and download the PDF document by clicking on the link below:

|

1. e-Invoicing: ‘e-Invoicing’ means reporting details of specified GST documents to a Government-notified portal i.e., Invoice Registration Portal (IRP) and obtaining an Invoice Reference Number (IRN). It doesn’t mean the generation of invoices by a Government portal.

|

2. IRP (Invoice Registration Portal): It is a government approved platform where notified persons upload or report invoices. Currently, six portals are authorised to generate IRN on reporting of invoices as per Rule 48(4) of the CGST Rules. Reporting invoices and generating Invoice Reference Numbers (IRN) on any of these portals is free of charge.

|

3. IRN (Invoice Reference Number): The unique identifier for every invoice reported on an IRP. It is based on the computation of a hash of the supplier's GSTIN, the financial year, the document type, and the document number.

|

4. AATO (Annual Aggregate Turnover): AATO (Annual Aggregate Turnover) for e-Invoicing is calculated based on the PAN of a taxpayer and the information provided in their GSTR-3B returns. It represents the total turnover of the taxpayer during a financial year and is used to determine the applicability of e-Invoice reporting requirements.

|

5. Enablement: The process of registering and enabling a taxpayer for e-Invoicing on the GST portal, allowing them to report e-Invoices on any of the six IRPs. Taxpayers are automatically enabled for e-Invoicing based on AATO but if not enabled they need to be self-enabled on the portal (https://einvoice.gst.gov.in).

|

6. GSTIN (Goods and Services Tax Identification Number): A unique identification number assigned to each registered taxpayer under the GST system.

|

7. GSTR-1: A monthly or quarterly return that taxpayers need to file, which contains details of outward supplies, including e-Invoice data.

|

8. Debit Note: A document used to record a reduction in the value of a previously issued invoice, typically issued by the seller.

|

9. Credit Note: A document used to record an increase in the value of a previously issued invoice, typically issued by the seller.

|

10. e-Invoice QR Code: A type of two-dimensional barcode that can be read by a digital device and provides information about the invoice. The QR code generated for e-Invoicing includes parameters such as the supplier's GSTIN, the recipient's GSTIN, invoice number, date of generation of the invoice, invoice value, IRN, etc..

|

11. e-Invoice QR Code Verifier App: A mobile application that allows users to scan and validate the QR codes on e-invoices.

|

12. e-Invoice FO (Front Office) Portal: The official web portal provided by GSTN where taxpayers can access various e-Invoice-related functionalities, including enablement status, e-Invoice generation, and searching for IRNs. It also provides links to all six IRPs, e-Invoice schema, master codes, enablement status, search IRN functionality, etc. (Link https://einvoice.gst.gov.in )

|

13. JSON Format: JSON (JavaScript Object Notation) is a standard data interchange format. For e-Invoicing, the invoice data must be uploaded in a predefined schema INV01 in JSON format.

|

14. API for e-Invoice Reporting: IRPs offer API-based functionality for reporting e-Invoices. API (Application Programming Interface) is a set of protocols for building and integrating software applications.

|

15. B2B Invoices: These are invoices issued in a business-tobusiness transaction. E-invoicing requirements in India currently apply to B2B invoices for certain taxpayers, based on their annual turnover

|

16. ERP System: Enterprise Resource Planning (ERP) system is a type of software used by companies to manage their day-to-day business activities. Taxpayers can continue to generate invoices from their current ERP system, but details of all such B2B invoices need to be uploaded or reported on an Invoice Registration Portal (IRP) in a notified format.

|

17. OTP: One-Time Password (OTP) is a password that is valid for only one login session or transaction. During the registration process on an IRP, an OTP is sent to the registered mobile number for verification.

|

18. Auto-population: This refers to the automatic filling in of data in a field. In the context of e-Invoicing, once an e-Invoice has been validated and has received an IRN, the data from the e-Invoice is auto-populated into the supplier's GSTR-1 form in the GST system.

|

19. e-Invoice schema: (INV-1 - Version 1.1) The e-Invoice schema is a predefined and standardised framework that defines the structure of the e-Invoice, including mandatory and optional fields, their format and rules for the generation of an e-Invoice.

|

20. Master codes: Master codes refer to a set of pre-defined codes used in the e-Invoicing system, such as HSN codes, country codes, currency codes, state codes, and others.

|

|

21. Signed e-Invoice: This refers to an e-Invoice that has been digitally signed by the Invoice Registration Portal (IRP) after validation. The signed e-invoice is provided with a unique IRN and QR code.

|

|

|

Disclaimer: The information provided above is intended for guidance and support purposes only. Taxpayers are advised to refer to the relevant sections of the GST Act and Rules for legal definitions and interpretation. The content shared does not constitute legal advice. Users are responsible for ensuring compliance with applicable laws and regulations.

|

Goods and Services Tax Network (GSTN)

(A Government Enterprise) (Dated 8 August 2023)

|

‘e-Invoicing’ means reporting details of specified GST documents to a Government-notified portal i.e., Invoice Registration Portal (IRP) and obtaining an invoice reference number. It doesn’t mean the generation of invoices by a Government portal.

|

In e-invoicing, taxpayers continue to create their GST invoices on their own Accounting/Billing/ERP Systems. These invoices are reported to any of the six authorized ‘Invoice Registration Portals (IRPs)’ in a standard format (called ‘Schema’ & notified as Form GST INV-1) and generating Invoice Reference Numbers (IRN) on any of these portals is free of charge.

|

B. To whom applicable/ who is eligible for e-Invoicing

|

Taxpayers whose aggregate turnover exceeds the notified limits (based on PAN) in any preceding financial year (since 2017-18) (as per the relevant notification) are required to comply with the e-invoicing regulations. Currently, the notified aggregate turnover is 5 crore and above is applicable from 1st August 2023.

|

C. Exemption from e-Invoice:

|

Certain taxpayers or entities are exempted from e-invoice reporting as per relevant notifications. Please refer to the respective notifications for detailed information.

|

D. Which documents/supplies covered:

|

GST invoices, Credit Notes and Debit Notes in respect of B2B Supplies, Supplies to SEZs (with and without payment), Exports (with and without payment) and Deemed Exports.

|

i. Taxpayers will continue to create their GST invoices on their own Accounting/Billing/ERP Systems.

|

ii. These invoices will be reported to any of the six authorized ‘Invoice Registration Portals (IRPs)’

|

iii. On reporting, IRP returns a signed e-Invoice with a unique ‘Invoice Reference Number (IRN)’ along with a QR Code

|

iv. Then, the Invoice (with QR Code) can be issued to the receiver. A GST invoice for B2B transaction will be valid only with a valid IRN.

|

F. Steps for E-invoice Reporting:

|

Step 1: Enablement for e-Invoicing:

|

i. All taxpayers who are eligible for the e-Invoicing, as per the Government notifications are automatically enabled for reporting of e-Invoices on any of the six authorized IRP portals.

|

- iv. Please note that the enablement status on the e-Invoice portal doesn’t automatically mean that a taxpayer is legally obligated to do e-Invoicing. The ‘enablement’ is primarily to ensure only the taxpayers having notified turnover limits are

- able to register and test/report invoices on IRPs.

Step 2: Register on any of the six Invoice Registration Portals:

|

The Invoice Registration Portal (IRP) is the website for uploading/reporting invoices by the notified persons. Currently, six IRP portals have been notified for reporting the invoice. These six active Invoice Registration Portals (IRPs) offer services for reporting e-Invoices and generating Invoice Reference Numbers (IRN), free of charge.

|

The list of authorized portals is as follows:

|

https://einvoice1.gst.gov.in

|

https://einvoice2.gst.gov.in

|

https://einvoice3.gst.gov.in

|

https://einvoice4.gst.gov.in

|

https://einvoice5.gst.gov.in

|

https://einvoice6.gst.gov.in

|

Enabled taxpayers must register on any of the six IRPs before they can start reporting e-invoices. This onboarding process involves a one-time verification of the taxpayer's registered mobile number and email through an OTP.

|

Upon successful validation, login credentials for the IRP portal are created, and the taxpayer is ready to report e-invoices.

|

Step 3 & 4: Reporting and Auto-population of e-Invoice:

|

i) To receive an Invoice Reference Number (IRN) for theirI nvoices, taxpayers must report the data of e-invoices on the IRP portal using the predefined INV-01 schema in a JSON format.

|

ii) . Most IRPs provide functionalities for reporting e-Invoices via offline tool, online web tool, Mobile App and API-based methods.

|

iii) ]The schema and the portal have built-in validations to prevent duplicate reporting and other checks.

|

iv) Upon successful validation, a signed e-invoice, carrying a unique IRN and a QR code, is returned to the taxpayer.

|

v) A copy of this invoice is then shared with the GST system for auto-population in the supplier's GSTR-1 return.

|

vi. Issue e-Invoice with IRN details to buyer.

|

G. e-Invoice Verification:

|

To verify the IRN of an e-Invoice, taxpayers have multiple options.

|

i. First, taxpayers can utilize the GSTN e-Invoice QR Code Verifier app, which is available on the Google Play / App Store, to verify e-invoices reported on any of the IRPs.

|

H. e-Invoice Master FO Portal:

|

i. As the number of IRP portals has increased to six, GSTN has developed a comprehensive e-Invoice master information portal, which can be accessed at https://einvoice.gst.gov.in.

|

ii. This portal serves as a one-stop resource for all e-Invoicing related information. It offers access to master codes, the ability to check enablement status, search IRN functionality, information about all the IRPs along with links to their respective portals, the e-invoice schema, and more.

|

iii. In the near future, this portal is also expected to provide the functionality to download e-Invoices.

|

Disclaimer: The information provided above is intended for guidance and support purposes only. Taxpayers are advised to refer to the relevant sections of the GST Act and Rules for legal definitions and interpretation. The content shared does not constitute legal advice. Users are responsible for ensuring compliance with applicable laws and regulations.

|

|

|

|

|

|

|

|

CBIC published the notification no. 06/2023 -CTR dated 26.07.2023 to amend the notification no. 11/2017-Central Tax (Rate) dated 28.06.2017

|

MINISTRY OF FINANCE

(Department of Revenue)

NOTIFICATION No. 06/2023- Central Tax (Rate)

New Delhi, the 26th July, 2023

|

G.S.R. 537(E).—In exercise of the powers conferred by sub-section (1), sub-section (3) and sub-section (4) of section 9, sub-section (1) of section 11, sub-section (5) of section 15, sub-section (1) of section 16 and section 148 of the Central Goods and Services Tax Act, 2017 (12 of 2017), the Central Government, on being satisfied that it is necessary in the public interest so to do, on the recommendations of the Council, hereby makes the following further amendments in the notification of the Government of India, in the Ministry of Finance (Department of Revenue) No. 11/2017-Central Tax (Rate), dated the 28th June, 2017, published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i), vide number G.S.R. 690(E), dated the 28th June, 2017, namely:-

|

In the said notification, -

|

(i) against serial number 3, in column (3), in item (ie), following explanation shall be inserted, namely:-

|

"Explanation. –This item refers to sub-items of the item (iv), (v) and (vi), against serial number 3 of the Table as they existed in the notification prior to their omission vide notification No. 03/2022- Central Tax (Rate) dated the 13th July,2022.‖;

|

(ii) against serial number 9, in column (3), in item (iii), in sub-item (b), in the entries under column (5), in condition (2), -

|

(a)for the words, figures and letters ―on or before the 15th March of the preceding Financial Year‖, the words, figures and letters ―on or after the 1st January of the preceding Financial Year but not later than 31st March of the preceding Financial Year‖ shall be substituted;

|

(b) after the fourth proviso, the following proviso shall be inserted, namely:- ―

|

"Provided also that the option exercised by GTA to itself pay GST on the services supplied by it during a Financial Year shall be deemed to have been exercised for the next and future financial years unless the GTA files a declaration in Annexure VI to revert under reverse charge mechanism on or after the 1st January of the preceding Financial Year but not later than 31st March of the preceding Financial Year."

|

(iii) against serial number 24, in column (3), in item (i), in the Explanation, in clause(i) , sub-clause(h) shall be omitted.

|

(i) in para 2, for the words ―end of the financial year for which it is exercised‖, the words and figures ―the start of the financial year for which I exercise option to revert under reverse charge mechanism by filing Annexure VI on or before the due date‖ shall be substituted;

|

(ii) in note to the Annexure, for the words, figures and letters ―The last date for exercising the above option for any financial year is the 15th March of the preceding financial year‖, the words, figures and letters ―The above option for any Financial Year shall be exercised on or after 1st January of the preceding Financial Year but not later than 31st March of the preceding Financial Year‖ shall be substituted;

|

(C) after Annexure V, the following Annexure shall be inserted, namely:-

|

{RAJEEV RANJAN, Under Secy

|

Form for exercising option by a Goods Transport Agency intending to revert under reverse charge mechanism to be filed before the commencement of any financial year to be submitted before the jurisdictional GST Authority.

|

1. I/We______________ (name of Person), authorized representative of M/s……………………. had exercised option to pay GST on the services of GTA in relation to transportation of goods supplied by us during, the financial year……………under forward charge by filing Annexure V on ………………..;

|

2. I hereby declare that I want to revert to reverse charge mechanism for Financial Year………;

|

3. I understand that this option once exercised shall not be allowed to be changed within a period of one year from the date of exercising the option and will remain valid till the end of the financial year for which it is exercised.

|

Legal Name: -

GSTIN: -

PAN No.

Signature of Authorized representative:

Name Authorized Signatory :

Full Address of GTA:

(Dated Acknowledgment of jurisdictional GST Authority)

Note: The above option for any Financial Year shall be exercised on or after 1st January of the preceding Financial

Year but not later than 31st March of the preceding Financial Year."

|

2. This notification shall come into force with effect from 27th July, 2023.

|

The principal notification number 11/2017 -Central Tax (Rate), dated the 28th June, 2017 was published in the Gazette of India, Extraordinary, vide number G.S.R. 690 (E), dated the 28th June, 2017 and last amended vide notification number 05/2023-Central Tax (Rate), dated the 9th May, 2023 published in the official gazette vide number G.S.R. 348(E), dated the 9th May, 2023.

|

|

|

|

|

|

|

|

Centre has extended the last date for filing appeals before the Goods and Services Tax Appellate Tribunal (GSTAT) to July 31, 2026, giving taxpayers an additional month to submit their cases after a surge in filings led to technical difficulties on the GSTAT portal.

|

The extension applies to appeals filed under Section 112(1) read with Section 112(3) of the Goods and Services Tax (GST) law.

|

The revised deadline replaces the earlier cut-off of June 30, 2026, which had been notified by the government on September 17, 2025.

|

The decision follows recent representations from various stakeholders who flagged technical issues arising from a rush of appeals being filed on the GSTAT portal ahead of the deadline.

|

While noting that the original due date had been notified well in advance in September 2025, the government said filing activity had intensified sharply in recent weeks. It said 30,000 appeals were filed in the last 15 days alone, with daily filings touching a peak of 5,500 appeals.

|

Advising against eleventh-hour filings, the government urged taxpayers to complete their appeal submissions well in advance to ease pressure on the GSTAT portal.

|

The GST Appellate Tribunal serves as the first judicial appellate forum for taxpayers seeking to challenge orders issued by GST authorities after the disposal of their first appeals.

|

Source: The Economic Times

|

|

|

|

|

|

|

|

|

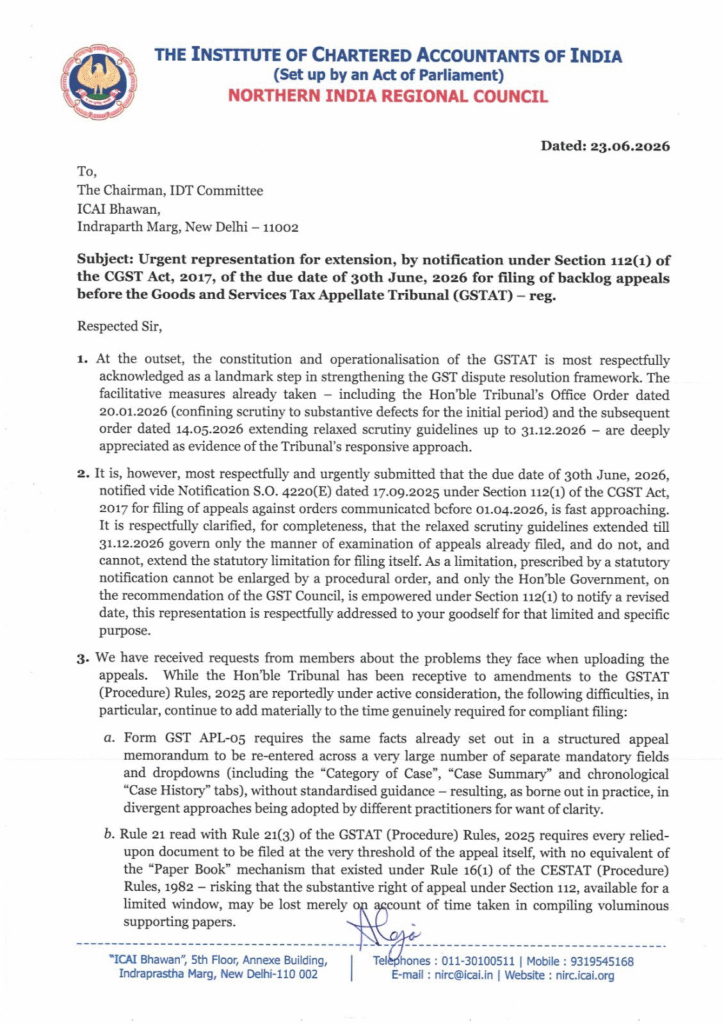

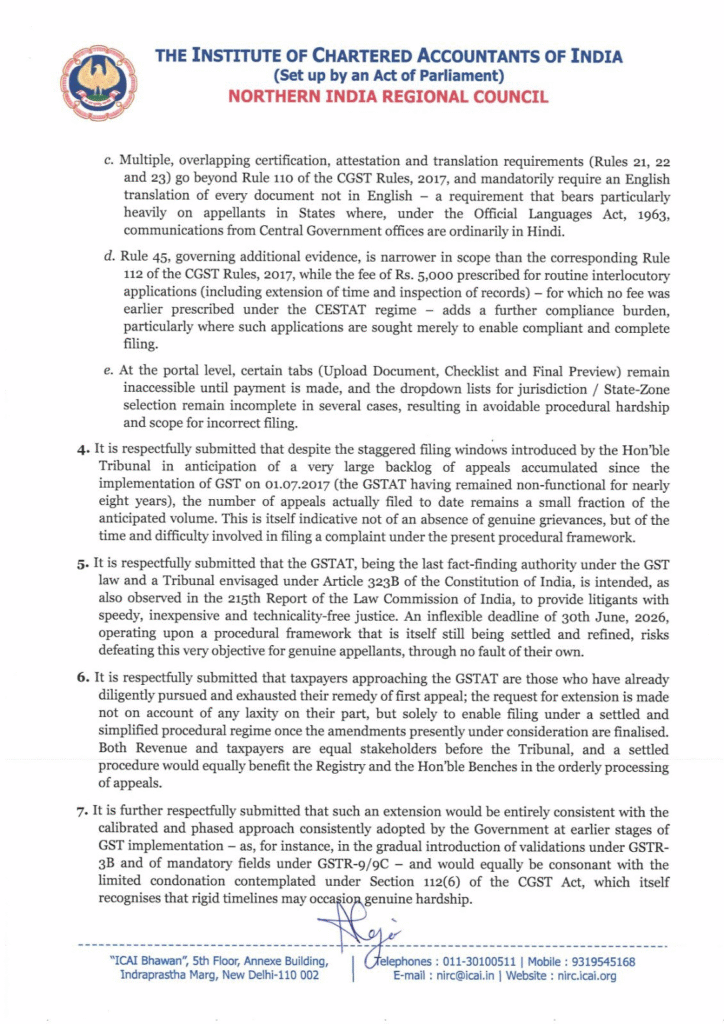

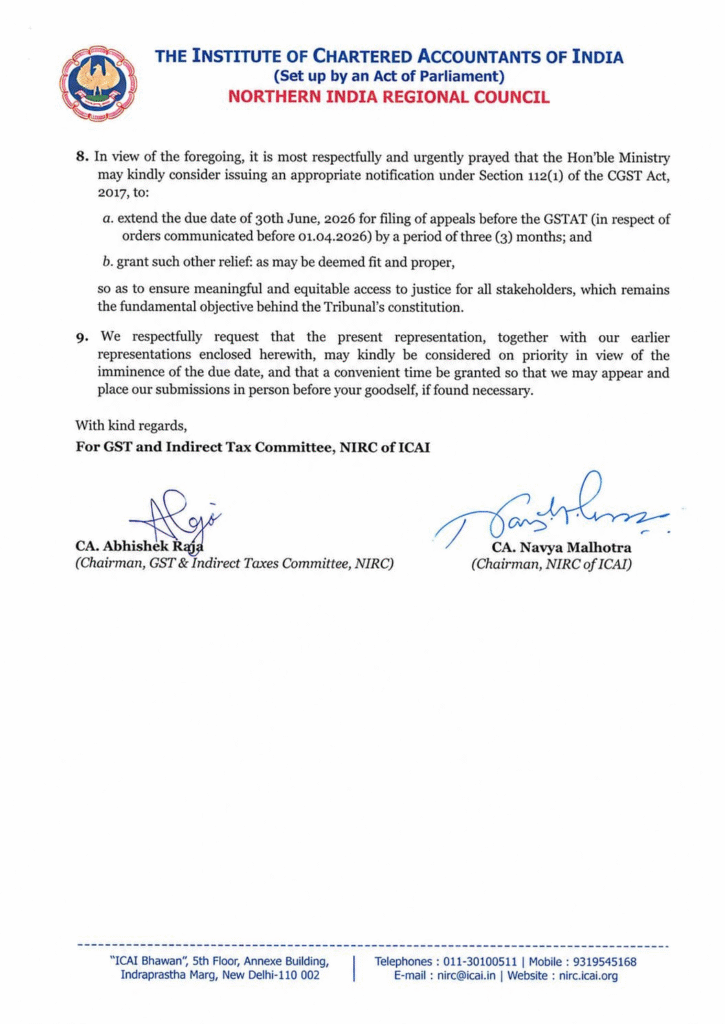

GST & IDT Committee has requested the Chairman, IDT Committee, ICAI, New Delhi to urgently represent before the respective forums for the date extension of GSTAT, i.e., 30-Jun-2026.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Tata Steel Limited said tax authorities have filed an appeal seeking restoration of penalties worth Rs. 368.72 crore that were earlier dropped in a GST adjudication order, even as proceedings on the underlying demand remain stayed by the Jharkhand High Court, according to a stock exchange filing.

|

"One June 16, 2026, the Assistant Commissioner, Division-I, CGST & Central Excise , Jamshedpur, Jharkhand filed an appeal before the Commissioner (Appeals) of CGST & Central Excise, Ranchi against the above-mentioned Adjudication Order dated December 18, 2026, to the extend that the Adjudicating Authority has dropped the penalty amounting to Rs. 3,68,72,21,158/-," Tata Steel said in its exchange filing.

|

The appeal, filed on June 16 by the Assistant Commissioner, CGST & Central Excise, Jamshedpur, challenges the December 18, 2025, adjudication order to the extent it waived the penalty.

|

The original show-cause notice, issued in June 2025, proposed disallowance of input tax credit for FY 2018-19 to FY 2022-23, with an aggregate GST demand of about Rs. 1,007.55 crore. Of this, Tata Steel said it has already paid Rs. 514.19 crore in the normal course, leaving an alleged exposure of Rs. 493.35 crore.

|

In December 2025, the adjudicating authority confirmed the tax demand of Rs. 493.35 crore, imposed a penalty of Rs. 638.83 crore and applicable interested, while dropping an earlier proposed penalty of Rs. 368.72 crore. Tata Steel subsequently moved the Jharkhand High Court, which granted a stay on all further proceedings in March 2026.

|

"This matter is, inter-alia, contingent upon the final adjudication of the issue concerning the issuance of show cause notices for multiple periods, which is presently sub judice before the High Court," Tata Steel said.

|

Tata Steel added that it has a good case on merit and hence will contest the same before the Appellate Authority within the statutory timelines, noting that the development has no impact on its financial or operational position, arising from the said appeal.

|

Source: The Economic Times

|

|

|

|

|

|

|

|

With the June 30 deadline for filing legacy appeals before the Goods and Services Tax Appellate Tribunal (GSTAT) fast approaching , tax professionals, chartered accountants and industry bodies have urged the Finance Ministry to extend the filing window, warning that persistent technical glitches on the GSTAT portal could prevent thousands of taxpayers from filing their appeals before the deadline.

|

The demand comes as taxpayers seek to file appeals arising from nearly nine years of litigation accumulated during the period when the Tribunal remained non-operational. Experts said the combination of a massive backlog, voluminous documentation and continuing portal-related issues has significantly constrained taxpayers' ability to meet the deadline.

|

According to Aditya Singhania, Founder of Trackase, the backlog is estimated at nearly four lakh to 4.5 lakh legacy appeals, while only around 36,929 appeals have been filed nationalwide so far.

|

"The ground reality is deeply concerning. Against an anticipated backlog of nearly four to four and a half lakh appeals accumulated over nine years of the Tribunal's non-operationality, only around 36,929 appeals have been filed nationally as of now," Singhania said.

|

He attributed the slow pace of filings to the teething troubles of the newly launched e-filing portal, including server time-outs, authentication challenges, payment gateway reconciliation issues and a filing structure that requires considerable time and effort to navigate.

|

Experts cite portal hurdles, record backlog

According to experts and representations submitted to the Finance Ministry, taxpayers continue to face multiple technical issues on the GSTAT portal, including session expiry, repeated login failures., Aadhaar authentication problems, Digital Signature Certificate (DSC) validation failures, payment reconciliation delays and incomplete integration between the Goods and Services Tax Network (GSTN) and the GSTAT portal.

|

Experts said taxpayers are also required to retrieve and compile extensive records accumulated over several years, including adjudication orders, invoices, reconciliations, e-way bills, ledger extracts and other supporting documents, making the filing process particularly time-consuming.

|

CA Nitin Bansal, State-President, BJP CA Cell Haryana, said the Finance Ministry has received several representations highlighting the practical challenges taxpayers are facing in filing appeals before the Tribunal.

|

"With the Tribunal becoming operational after nearly nine years, taxpayers must now prepare and file a substantial backlog of appeals within a limited window, many involving voluminous, multi-year records, even as the GSTAT e-filing portal continues to stabilise," Bansal said.

|

He added that extending the deadline would be revenue-neutral as the mandatory pre-deposit and other conditions would remain unchanged while ensuring genuine taxpayers are not denied their appellate remedy because of circumstances beyond their control.

|

Over-time extension sought

CA Sonu Goel, Chairman, Panipat Branch of the Institute of Chartered Accountants of India (ICAI), said a one-time extension would ensure disputes are decided on their merits rather than procedural constrints.

|

"One-time extension would safeguard taxpayers' right to appeal, uphold the principles of natural justice, and ensure that dispute are decided on merits rather than being defeated by procedural or technological constraints. This pragmatic relief would further reinforce the Government's commitment to ease of doing business while maintaining certainty and confidence in the GST ecosystem," Goel said.

|

Parag Mehta, Partner at N.A. Shah Associates LLP, said the portal continues to experience issues ranging from login failures and incorrect fee calculations to disappearing data.

|

"Considering the fact that the portal is not fully supporting the filing process and the number of appeals filed remains significantly lower than expected, the deadline should be extended. GSTAT is an important appellate remedy and taxpayers should not be deprived of that opportunity," Mehta said.

|

Bas association flags nationwide concerns

The Sales Tax Bar Association has also written to the Finance Ministry seeking an extension of the filing deadline, stating that taxpayers and tax professional across the country continue to face significant practical and technical difficulties while filing appeals through the GSTAT portal.

|

In its representation, the association said the present limitation period covers appellate orders accumulated over nearly nine years when the Tribunal remained non-functional, requiring taxpayers to retrieve historical records and prepare detailed documentation within a limited period.

|

The association highlighted recurring issues including server interruptions, repeated Aadhaar authentication and DSC validation failures, payment gateway reconciliation delays, manual duplication of information already available on the GSTN portal and challenges in uploading voluminous records.

|

It warned that if the deadline is not extended, thousands of taxpayers could lose the opportunity to pursue their statutory appeals because of technological and procedural constraints, potentially leading to avoidable litigation before various High Courts.

|

Prabhat Ranjan, Senior Director at Nexdigm, said extending the filing deadline has become "the need of the hour".

|

"The appellate process should be about the actual merits of the issues between both parties and not technical questions of delay. This is a taxpayer-friendly measure that will make GST dispute resolution processes more fair and credible," he said.

|

As of publication, the government has not announced any extension of the June 30 deadline for filing legacy GSTAT appeals. While the GSTAT has extended the period for relaxed scrutiny of filed appeals until December 31, 2026 , tax professionals, industry experts and representative bodies continue to seek a one-time extension of the filing deadline, arguing that additional time would enable taxpayers to exercise their statutory right of appeal without affecting revenue, as the mandatory pre-deposit requirements would continue to apply.

|

Source: The Economic Times

|

|

|

|

|

|

|

|

|

|

The Goods and Services Tax (GST) Council’s fitment committee, composed of revenue officials from both the Centre and states, is expected to provide an explanation of the “ground clearance” criterion and its implementation in the context of utility vehicles (UVs) for purposes of taxation.

|

A ground clearance (also known as ride height) of above 170 millimetres (mm) is one of the three key parameters for categorising a UV and attracting a 22 per cent compensation cess.

|

|

|

|

|

|

|

|

|

|

|

|

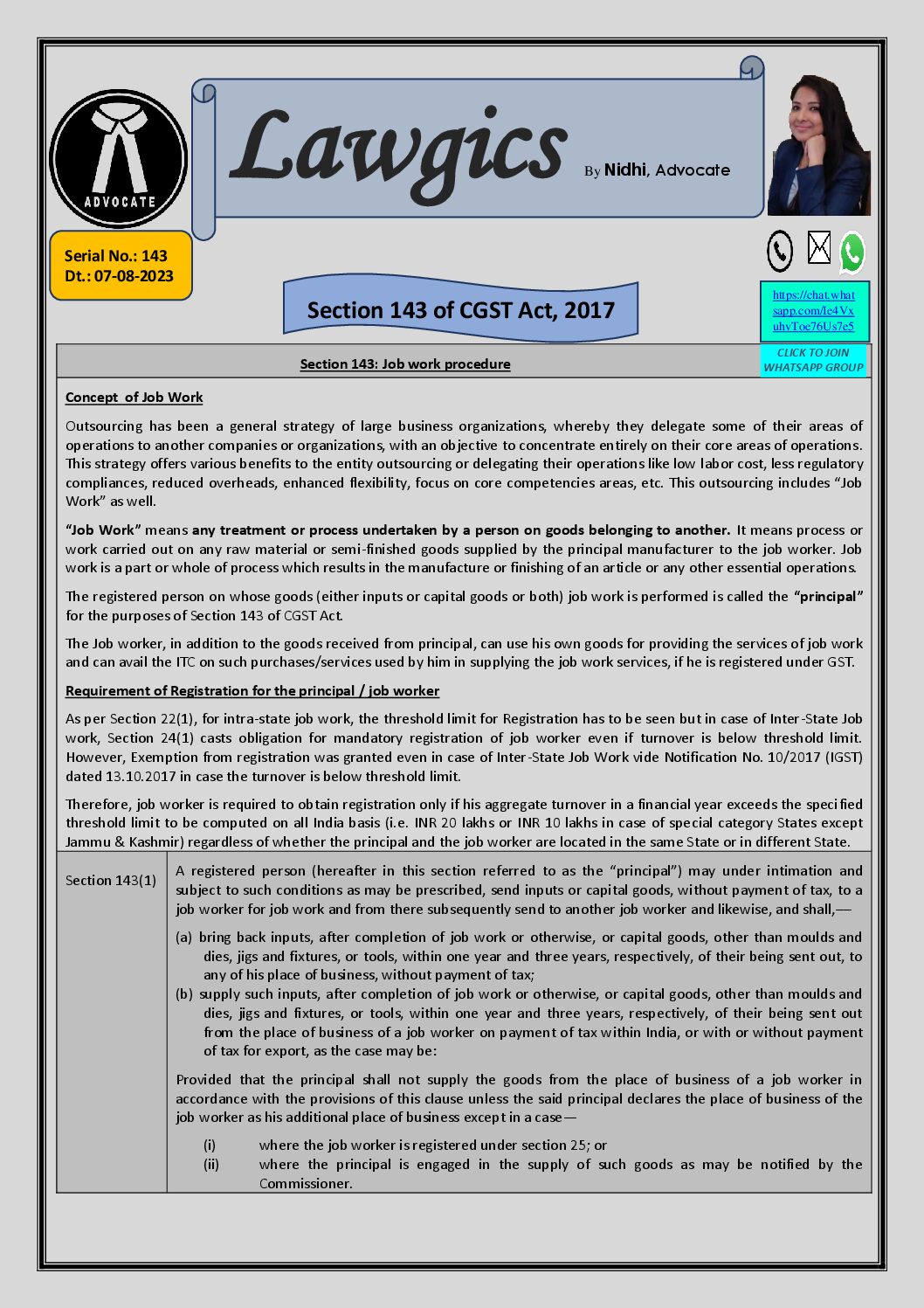

4 Lawgics by Ms.Nidhi Aggarwal

|

Ms. Nidhi Aggarwal is delighted to present GST Notes/Law in a simplified manner under the title “ Lawgics ”. The note is prepared in a series of PDFs encompassing GST Law and the interpretations thereof in simple manner. The author with a great vision to spread complex GST law in a simple manner amongst the taxpayers, tax professionals, students and knowledge seeker is presenting the Lawgics in piecemeal at regular interval.

|

|

Lawgics 143 to 146 is added for your reading

|

|

|

|

|

|

|

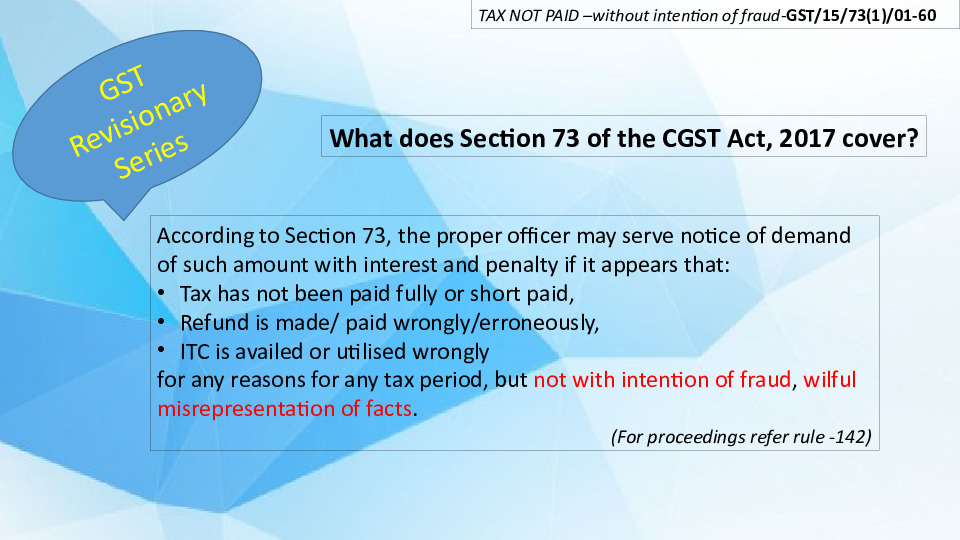

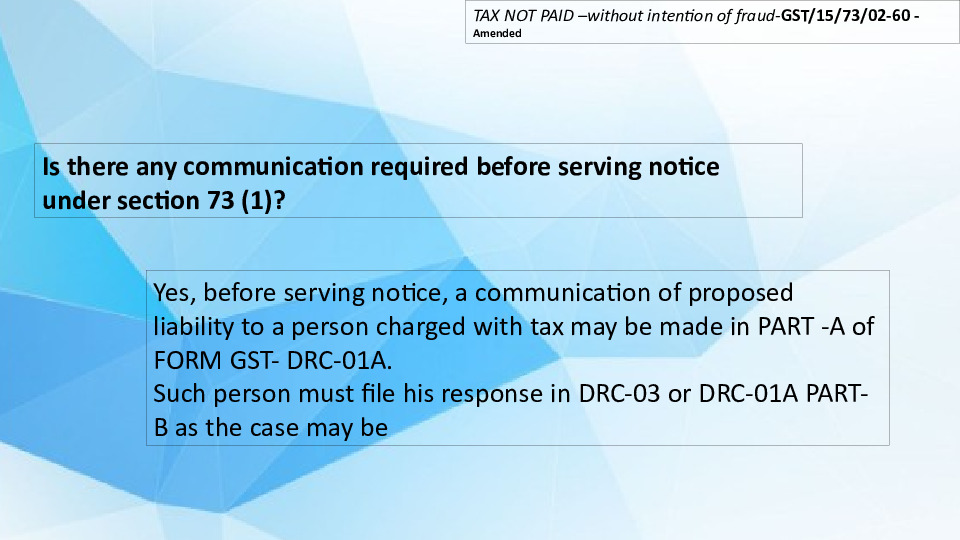

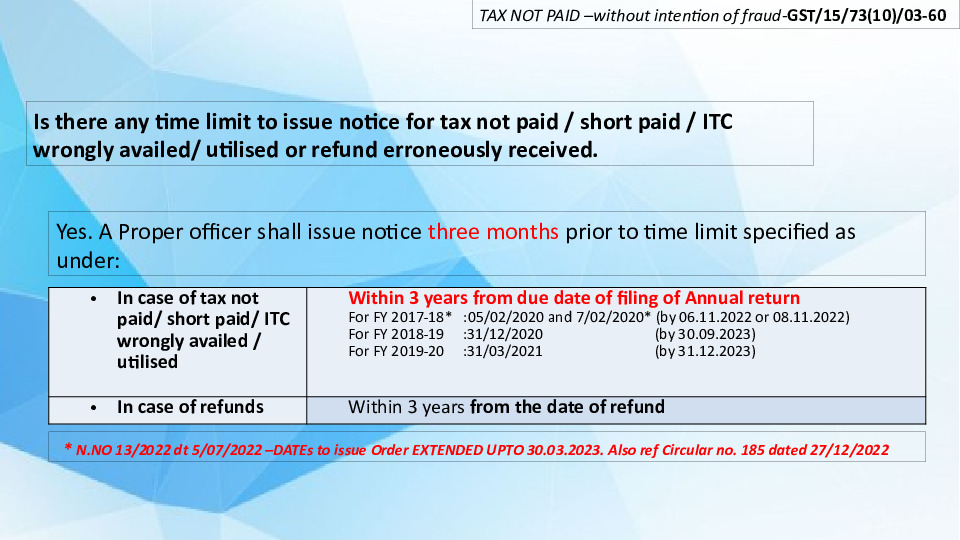

5. GST Notes by CMA Anil Sharma

1) Shri CMA Anil Sharma, Shri CMA Gurdev Singh Saini and Smt. CMA Bhawna Sharma posted Chapter-1 to 15 containing CGST Act in simple language in PPT format. This is to make dealers, professionals, academicians, students etc. understand the basics of GST laws. Each Chapter in CGST Act, 2017 is explained in the form of Slides as given below for easy understanding of the Act:

|

Chapter-15th slide is given below.

|

|

|

|

|

|

|

|

|

|

|

Do you wish to publish your Article?

If you wish to share your article with maximum readers then please send it at taxupdate.otu@gmail.com. We shall publish it with all due credit to you.

|

|

The topic can be on GST, Income Tax, Pre-GST laws, PPT, Notes etc. The article may contain 500 words to 1500 words or it may be more than that if the article demands.

|

|

|

|

|

|

|

If you wish to subscribe to weekly Newsletter at Rs. 149/- for one year, please subscribe. We shall send you the updates weekly.

|

|

|

|

|

|

|

Hope the above updates is of use to you. Please share your input and feedback at taxupdate.otu@gmail.com

|

|

|

|

|

|

|

Visit our website

|

OTU provides you

|

- Articles on various topics

|

|

- Media - GST, Income Tax & Press R.

|

|

- Notes / Newsletter at 149/ p.a.

|

|

|

|

|