|

onlinetaxupdate team wish to express sincere thanks to all the readers, authors, subscribers for the support extended to us. Please share your feedback at

|

taxupdate.otu@gmail.com or 7738647904

|

Newsletter 138 dated 07.10.2024

|

|

|

|

|

|

|

|

|

Dear Reader,

|

Please find newsletter for your reading and reference.

|

|

Index of the Newsletter

- Recent updates

- Safari Retreats

- Article

- Lawgics by Ms.Nidhi Aggarwal

- GST Notes by CMA Anil Sharma

- GST Daily by CA Pradeep Modi

- PPT/Handbook

- GST/IT/Customs in media

- Latest Update - Recap

|

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Notification no. 02/2026 – Central Tax dated 07.05.2026.

|

GOVERNMENT OF INDIA

MINISTRY OF FINANCE

DEPARTMENT OF REVENUE

|

Notification No. 02/2026 – Central Tax dated 07.05.2026

|

S.O. 2286(E).— In exercise of the powers conferred by sub-section (1A) of section 101A of the Central Goods and Services Tax Act, 2017 (12 of 2017) (hereinafter referred to as the said Act), the Central Government, on the recommendations of the Council, hereby empowers the Principal Bench of the Appellate Tribunal, New Delhi constituted under sub-section (3) of section 109 of the said Act, to hear appeals made under section 101B of the said Act.

|

This notification shall be deemed to have come into force on the 1st day of April, 2026.

|

BALASUBRAMANIAN KRISHNAMURTHY,

Joint Secretary

|

|

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Notification no. 01/2026 – Central Tax dated 21.04.2026 that Seeks to extends the due date for furnishing the return in FORM GSTR-3B for the month of March, 2026 till the twenty-first day of April, 2026.

|

GOVERNMENT OF INDIA

MINISTRY OF FINANCE

DEPARTMENT OF REVENUE

CENTRAL BOARD OF INDIRECT TAXES AND CUSTOMS

Notification No. 01 /2026 Central Tax dated 21.04.2026

|

G.S.R (E)… ( In exercise of the powers conferred by sub section (6) of section 39 of the Central Goods and Services Tax Act, 2017 (12 of 2017), the Commissioner, on the recommendations of the GST Council, hereby extends the due date for furnishing the return in FORM GSTR 3B for the month of March, 2026 till the twenty first day of April, 2026, for the registered persons who are required to furnish return under sub section (1) of section 39 read with clause (i) of sub rule (1) of rule 61 of the Central Goods and Services Tax Rules, 2017.

|

2. This notification shall come into effect from 20th day of April, 2026.

|

(Kangale Shrunkhala Motiram)

Director

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Instruction no. 06/2025-GST dated 03.10.2025 regarding Provisional sanction of refund claims on the basis of identification and evaluation of risk by the system

|

File No.: CBIC-20006/4/2025-GST

Government of India

Ministry of Finance

Department of Revenue

Central Board Indirect Taxes & Customs

GST Policy Wing

|

Instruction No. 06/2025-GST dated 03.10.2025

|

All the Principal Chief Commissioners / Chief Commissioners of Central Tax

|

Subject: Provisional sanction of refund claims on the basis of identification and evaluation of risk by the system - reg.

|

The 56th meeting of the Goods and Services Tax Council held on 3rd September 2025, recommended amendment in rule 91(2) of CGST Rules, 2017 to provide for sanction of 90% of refund claimed on provisional basis by the proper officer on the basis of identification and evaluation of risk by the system. In addition, a proviso has been inserted in rule 91(2) to provide that, on case-by-case basis, where the proper officer is of the opinion that in a particular case, provisional refund should not be granted, he can, for reasons to be recorded in writing, instead of grant of refund on provisional basis, proceed with detailed examination of the application. Further, vide notification No. 14/2025-Central Tax dated 17.09.2025, category of registered persons has been notified under section 54(6) of the CGST Act, 2017, who shall not be allowed refund on provisional basis for zero rated supplies.

|

2. In order to ensure uniformity in the implementation of the provisions of the Act across field formations and to streamline the process of GST refunds, the Board, hereby issues the following instructions with respect to processing of refund claims, filed with the proper officer, on account of zero rated supply of goods or services or both.

|

3. Manner of processing refund applications:

|

3.1 While processing refund applications, the following may be ensured:

|

a. The refund application, consequent to its filing, shall continue to be processed as per extant guidelines till the issuance of FORM GST RFD-02 or FORM GST RFD-03, as the case may be. The extant timeline prescribed for the issuance of FORM GST RFD-02 or FORM GST RFD-03, as the case may be, should be strictly adhered to.

|

b. Categorization of refund applications as “low-risk” on the basis of risk score provided by the system shall be taken into account and 90% of the refund amount claimed shall be sanctioned on provisional basis in such cases.

|

c. It may be noted that once an acknowledgment has been issued in FORM GST RFD-02, scrutiny is not required to be done for low risk refund applications for sanctioning of refund on provisional basis unless the said refund application is covered under the first proviso to rule 91(2) of the CGST Rules, 2017, whereby the officer, for reasons to be recorded in writing, may proceed with the examination of the application in accordance with the provisions of rule 92, instead of grant of refund on provisional basis.

|

d. For refund applications, which are not categorised as “low-risk” by the system, refund shall not be sanctioned on provisional basis and in such cases, the proper officer shall proceed with detailed scrutiny of refund application and further action as per the extant guidelines.

|

3.2 The statutory conditions prescribed for grant of provisional refund, including non-eligibility of the notified category of registered persons under section 54(6) vide notification No. 14/2025-Central Tax dated 17.09.2025, the requirement under rule 91(1) regarding non-prosecution, shall continue to be applicable in these cases. Further, as no adjustment or withholding of refund, as provided under sub sections (10) and (11) of section 54 of the CGST Act, can be done in respect of the provisionally sanctioned amount, therefore, in such cases, the proper officer, instead of granting refund on provisional basis, may process and sanction refund on final basis at the earliest and recover the amount from the amount so sanctioned. Also, provisional refund may not be sanctioned where, in respect of any previous refund application filed by the claimant, the issue involved is pending in an appellate forum, or where a show cause notice is issued or where an order has been passed but matter has not attained finality.

|

3.3 It is clarified that as the said amendment has been made for trade facilitation, therefore the said proviso to rule 91(2) of the CGST Rules, 2017 may be used sparingly and on case-to-case basis, so that the provisional refund is not denied merely on the basis of presumptive reason(s), initiation of routine proceedings such as scrutiny etc.

|

3.4 It also needs to be noted that if, on detailed examination, it appears to the proper officer that the refund amount sanctioned provisionally is more than the refund amount finally found admissible, in such case, the proper officer shall issue a show cause notice to the applicant, in FORM GST RFD-08, under section 54 of the CGST Act, read with section 73 or 74 or 74A of the CGST Act, as is presently being done.

|

4. As the amendment in rule 91(2) of CGST Rules, 2017 has been notified vide notification No. 13/2025 Central Tax dated 17.09.2025 to come into effect from 01.10.2025, therefore the provisions related to risk based sanction of provisional refund shall be applicable for all refund applications filed on or after 01.10.2025.

|

5. It is worthwhile to note that the GST Council, in its 56th meeting, has also recommended amending Section 54(6) of the CGST Act, 2017, to provide for sanction of 90% of the refund amount claimed on provisional basis, in case of refund claims filed on account of inverted duty structure (IDS), similar to the provisions in place for zero-rated supplies. However, the said amendment to the Act will be incorporated through the forthcoming Finance Act and States will also be required to pass the corresponding amendments in their respective legislations, which will take time.

|

5.1 Therefore, as an interim measure of trade facilitation, it has been decided by the Central Government that till this amendment in the Act is effected, in case of refund applications filed on account of IDS, on or after 01.10.2025, 90% of the refund amount so claimed may be sanctioned on provisional basis in similar manner as is being sanctioned provisionally for refund claims filed on account of zero-rated supplies.

|

5.2 The manner for processing such refund applications shall be the same as specified in para 3.1 to para 3.4 above. Further, the statutory conditions prescribed for grant of provisional refund in case of zero rated supplies shall equally apply in these cases.

|

5.3 It is further stated that the functionality for issuance of provisional refund in such cases has been made available by GSTN, on lines similar to the provisional refund processing for refund applications filed on account of zero rated supply of goods or services or both.

|

6. The implementation of this instruction may be supervised by the jurisdictional Principal Commissioner/ Commissioner and a report in this regard may be sent to the jurisdictional Principal Chief Commissioner/ Chief Commissioner. Principal Chief Commissioner/ Chief Commissioner should ensure that the trade facilitation measures decided upon by the Government are implemented in letter and spirit and there is proper monitoring regarding the same.

|

7. Difficulty, if any, in implementation of this instruction may please be brought to the notice of the Board.

|

(Gaurav Singh)

Commissioner (GST)

|

Copy to: Additional Secretary, GST Council Secretariat with a request to circulate to State GST formations, which may, if deemed appropriate, issue similar instructions within their jurisdictions to ensure uniformity and effective implementation.

|

|

|

|

|

|

OFFICE OF THE COMMISSIONER OF STATE TAXMAHARASHTRA STATE, MUMBAI issued NOTIFICATION NO: - SGST/e-way bill/02/2025-26 dated 20.02.2026 Waiving off requirement of e-way bill for motor vehicles for road testing where goods are transported for reasons other than by way of supply under sub-rule (5) of rule 138A of MGST Rules, 2017.

|

M/s. Tata Motors Limited, having principal place of business at TATA MOTORS LIMITED, Nigadi Bhosari Road, Pimpri Chinchwad, Pune, Maharashtra, 411 018. (GSTIN: 27AALCT0864B1ZE) (hereinafter called as ‘taxpayer’), have made a representation vide their letter GST/MH/056 dated 13th November 2025. for waiving off requirement of e-way bill for motor vehicles for road testing where goods are transported for reasons other than by way of supply under sub-rule (5) of rule 138A of MGST Rules, 2017(hereinafter referred as MGST Rules, 2017).

|

Whereas I, Asheesh Sharma, Commissioner of State Tax. Maharashtra State, am of the opinion that the difficulties being faced by the ‘taxpayer’ are genuine and require due consideration. Now, therefore I, Asheesh Sharma, Commissioner of State Tax, Maharashtra State, in exercise of the powers conferred upon me under sub-rule (5) of rule 138A of the MGST Rules, 2017, am pleased to issue this notification for grant of permission to M/s. Tata Motors Limited. having principal place of business at TATA MOTORS LIMITED, Nigadi Bhosari Road, Pimpri Chinchwad, Pune, Maharashtra, 411 018 (GSTIN: 27AALCT0864B1ZE) to waive the requirement of e-way bill for motor vehicles to perform various road tests across India, subject to the following procedure and conditions as mentioned below.

|

(i) The ‘ taxpayer ’ shall execute a bond sufficient to cover the value of the motor vehicle being cleared for the purpose of road testing in a calendar month, with the Jurisdictional State Tax Officer, PIMPRI_702, Division - PUNE_SOUTH_EAST, Zone - PUNE_SOUTH_WEST, PUNE undertaking to follow all the conditions mentioned hereunder;

|

(ii) Motor vehicles shall be removed by the ‘taxpayer’ for the purpose of road test under a delivery challan, duly signed by the authorized signatory of the “taxpayer”;

|

(iii) The exemption to carry delivery challan instead of e-way bill is limited only to transportation of motor vehicles for reasons other than by way of supply and limited to road test of such motor vehicles;

|

(iv) The delivery challan shall be induplicate, pre-authenticated and having running serial number for every calendar year and printed format and shall contain the following information.

|

(a) The name and address of the “taxpayer”, it’s ‘GSTIN’

|

(b) Name of the jurisdictional officer, Division and Zone with whom the taxpayer is registered for the purpose of GST and notification number under which permission under sub-rule (5) of rule 138(A) of MGST Rules, 2017 for such removal has been given;

|

(c) The description, vehicle serial number/ engine number/ chassis number, as the case may be, to identify the vehicle which has been cleared for the purpose carrying out road test along with the value of such motor vehicle;

|

(d) The date of dispatch of such motor vehicle for road test and probable time line for return of the motor vehicles to its place of clearance;

|

(v) The Motor vehicle/ transport equipment will also carry trade plate as prescribed under Central Motor Vehicles Rules, 1989 or under any other law in force for the purpose of undertaking testing of such motor vehicle as the case may be;

|

(vi) The ‘taxpayer’ shall maintain proper records to correlate the dispatch and return of the motor vehicles sent for road testing. If at any point of time the value of the motor vehicles cleared for road test exceeds the amount for which the bond has been executed, the ‘taxpayer’ shall execute a separate bond of differential value with the concerned, before removal of the motor vehicle for testing purpose;

|

(vii) The taxpayer’ shall submit to the Jurisdictional State Tax Officer, PIMPRI_702, Division - PUNE_SOUTH_EAST, Zone - PUNE_SOUTH_ WEST, PUNE a monthly account containing the details of all motor vehicles sent and received back after road testing;

|

(viii) The ‘taxpayer’ shall furnish any additional relevant information pertaining to the instant subject matter which may be required by the Jurisdictional State Tax Officer, PIMPRI_702, Division-PUNE_SOUTH_EAST, Zone - PUNE_SOUTH_WEST, PUNE.

|

2. The ‘ taxpayer ’ shall be fully responsible and accountable for the taxable goods so removed without generation of e-way bill under sub-rule (5) of rule 138(A) of MGST Rules, 2017 as permitted under this notification.

|

3. If the above said conditions are not adhered to or are violated, the impugned permission shall be revoked/withdrawn without any prior intimation.

|

4. This notification is valid for financial year 2025-26, i.e. up to 31st March 2026

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Corrigendum on 12.06.2026 to Notification no. 45/2025 -Customs dated 24.10.2025 -

|

G.S.R…(E).- In the notification of the Government of India, Ministry of Finance (Department of Revenue) No. 45/2025-Customs, dated the 24th October, 2025, published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i), vide number G.S.R. 781(E), dated the 24th October, 2025, at page 291, in lines 12 and 14, for ‘1993’ read ‘1983’.

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Notification no. 03/2026 – Customs (CVD) dated 10.06.2026 to amend Notification no. 4/2021-Customs (CVD) dated 24.09.2021

|

Government of India

Ministry of Finance

(Department of Revenue)

|

Notification No. 3/2026-Customs (CVD) dated 10.06.2026

|

G.S.R…-(E).- In exercise of the powers conferred by sub-sections (1) and (6) of section 9 of the Customs

Tariff Act,1975 (51 of 1975), read with rules 20 and 24 of the Customs Tariff (Identification, Assessment and Collection of Countervailing Duty on Subsidized Articles and for Determination of Injury) Rules, 1995, the Central Government hereby makes the following amendment in the notification of the Government of India, in the Ministry of Finance (Department of Revenue) No. 4/2021-Customs (CVD), dated the 24th September, 2021, published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i), vide number G.S.R. 662(E), dated the 24th September, 2021, namely:-

|

In the said notification, after paragraph 2, the following paragraph shall be inserted, namely:-

|

“3. Notwithstanding anything contained in paragraph 2, the countervailing duty imposed under this

notification shall remain in force up to and inclusive of the 23rd March, 2027, unless revoked, superseded or amended earlier.”.

|

(Dheeraj Sharma)

Under Secretary

|

Note: The principal notification No. 4/2021-Customs (CVD) dated the 24th September, 2021, was published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i), vide number G.S.R. 662(E), dated the 24th September, 2021.

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Circular no. 28/2026-Customs dated 15.06.2026 regarding testing of samples of export consignments

|

|

|

|

|

|

Export consignments to West Asia will continue to receive enhanced insurance cover against payment defaults until September 30, the Directorate General of Foreign Trade (DGFT) said in a notification on Monday.

|

Earlier, the enhanced cover for exporters taking credit risk insurance from Export Credit Guarantee Corporation (ECGC) was available for shipments to West Asia sent between March 16 and June 15.

|

The enhanced risk cover announced on March 19 was part of the Resilience and Logistics Intervention for Export Facilitation (RELIEF) scheme under the Export Promotion Mission (EPM) to support exports to West Asia in view of the Iran war.

|

"The eligibility timelines under Component II of the EPM RELIEF intervention are extended up to September 30, 2026 to support Indian exporters and mitigate logistics challenges arising out of the continuing West Asia Crisis," the DGFT said.

|

Source: The Economic Times

|

|

|

|

|

|

|

|

Directorate General of Foreign Trade (DGFT) issued Public Notice No. 17/2026-27 dated 04.06.2026 regarding Enlistment under Appendix 2E of FTP, 2023-Agency Authorised to issue Certificate of Origin (Non-Preferential)

|

|

|

|

|

|

|

|

Directorate General of Foreign Trade (DGFT) issued Trade Notice 07/2026-27 dated 03.06.2026 regarding request for comments on alignment of Schedule-II (Export Policy) of ITC (HS), 2022 consequent to amendments introduced under the Finance Act, 2026

|

|

|

|

|

|

|

|

Directorate General of Foreign Trade (DGFT) issued Notification No. 20/2026-27 dated 02.06.2026 regarding Applicability of Quality Control Orders (QCOs)/ BIS requirements on imports by Special Economic Zone (SEZ) Units and Developers - Amendment in Para 2.03(A)(iii) of FTP 2023

|

|

|

|

|

|

|

|

Directorate General of Foreign Trade (DGFT) issued Notification No. 19/2026-27 dated 02.06.2026 regarding Amendment in import policy condition of specific ITC HS Codes covered under Chapter 71 of ITC (HS), 2022, Schedule - I (Import Policy)

|

|

|

|

|

|

Central Board of Direct Taxes (CBDT) issued notification no. 72/2026 dated 25.06.2026 to hereby approves deductions under section 45(3)(a)(i) of the Income-tax Act, 2025 and rules 32 and 34 of the Income-tax Rules, 2026 to the Public Health Foundation of India, Delhi (PAN: AABAP4445L) for Scientific Research under the category of University, college or other institution.

|

|

|

|

|

|

|

|

Central Board of Direct Taxes (CBDT) issued notification no. 71/2026 dated 25.06.2026 to hereby approves deductions u/s 45(3)(a)(i) of the Income-tax Act, 2025 and rules 32 and 34 of the Income-tax Rules, 2026 to the University of Hyderabad (PAN: AAAAU8109M) for Scientific Research under the category of university, college or other institution.

|

|

|

|

|

|

Central Board of Direct Taxes issued Circular no. 4 of 2026 dated 31.03.2026 regarding Document Identification Number (DIN).

|

|

|

|

|

|

GSTN is taking downtime to enhance its services on the GST Portal on 27.06.2026 from 12:00 AM onwards until 2:30 am of 27.06.2026.

|

|

We shall be enhancing services on the GST portal on : 27th June’26 12:00 AM onwards. GST Portal services will not be available until 27th June’26 02:30 AM. The inconvenience caused is regretted.

|

|

|

|

|

|

|

|

|

|

|

GSTN is taking downtime to enhance its services on the GST Portal on 12.06.2026 from 11:30 AM onwards until 7:30 am of 13.06.2026.

|

We shall be enhancing services on the GST portal on : 12th June’26 11:30 PM onwards. GST Portal services will not be available until 13th June’26 07:30 AM. The inconvenience caused is regretted.

|

|

|

|

|

|

|

|

GSTN Advisory no. 664 dated 17.06.2026

|

Reference is invited to the GSTN Advisory dated 20.05.2026 regarding enhancements in the e-Way Bill system, wherein it was informed that “Ship-to GSTIN” shall be mandatorily captured in Bill-to/Ship-to transactions. It was also clarified that where the consignee is an unregistered person, the value “URP” shall be entered in the Ship-to GSTIN field.

|

In this regard, representations have been received from trade, ERP vendors, GSPs, ASPs, private IRPs and other stakeholders seeking clarification on the applicability of the said requirement in cases where e-Way Bill is generated along with e-Invoice or by using IRN. Representations have also been received regarding the Voluntary Closure of e-Way Bill facility and its impact on portal-based and API-based operations.Accordingly, an advisory has been issued to apprise stakeholders of the corresponding changes introduced in the e-Invoice API, e-Way Bill by IRN API and EWB Closure API. It has also been informed that the aforesaid changes have been made available in the Sandbox environment for testing and system preparedness. The changes are scheduled to be implemented in the Production environment with effect from 1st August, 2026.

|

All concerned stakeholders may accordingly be advised to access the advisory through the link given below and undertake necessary testing, system changes and preparedness within the prescribed timeline.

|

|

|

|

|

|

|

|

GSTN Advisory no. 663 dated 09.06.2026

|

Reference is invited to the GSTN Advisory dated 20.05.2026, wherein it was informed that the following functionalities would be implemented in the E-Way Bill system with effect from 15th June, 2026:

|

- Mandatory capture of "Ship To GSTIN" in Bill-To/Ship-To transactions; and

- Voluntary Closure of E-Way Bill functionality.

Representations have been received from trade and industry seeking extension of the implementation timeline, citing the requirement of system changes, testing, API/ERP readiness and master data updation across the taxpayer ecosystem.

|

In view of the above, and to facilitate smooth transition and adequate preparedness by taxpayers, GSPs, ERP providers and other stakeholders, it has been decided to extend the implementation timeline for both the above functionalities.

|

Accordingly, the mandatory capture of "Ship To GSTIN" in Bill-To/Ship-To transactions and the Voluntary Closure of E-Way Bill functionality shall be implemented with effect from 1st August, 2026, instead of 15th June, 2026.

|

Taxpayers, GSPs, ERP providers and other stakeholders are advised to complete the necessary system changes, testing and operational preparedness before the revised implementation date.Thank you,

Team GSTN

|

|

|

|

|

|

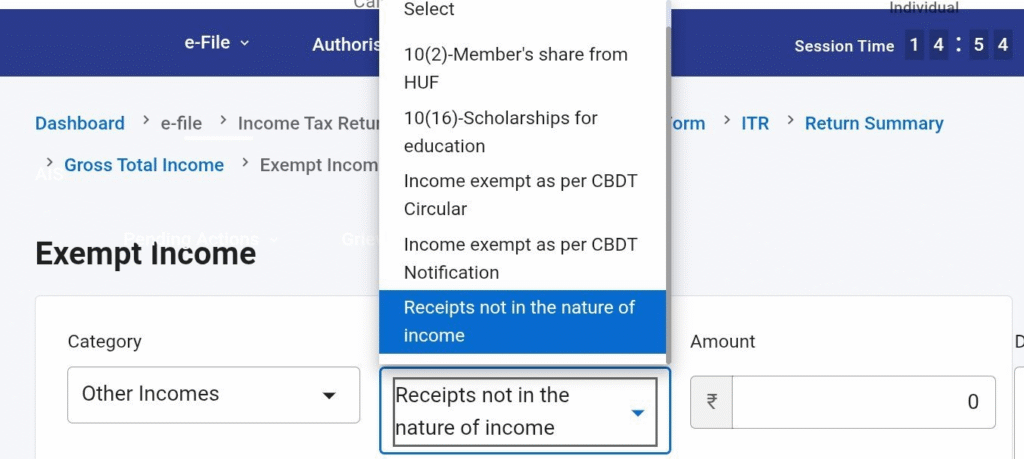

From AY 2026-27, the option to report 'Other Exempt Income' was removed.

|

Earlier, this was useful in situations such as:

|

- Sale of rural agricultural land/ Reporting of Gifts from Relatives - although disclosure was not required as same is not income .

|

The column of 'Other Income' under Exempt incomes has now been added.

|

|

|

|

|

|

|

|

|

|

|

Before applying for Income Tax registration, GST registration, ICEGATE, or DSC mapping, you can use the TRACES PAN Verification facility to check whether the name in the PAN database is correctly aligned with the PAN number.

|

Helps identify name mismatches in advance and avoid registration issues.

|

|

|

|

|

|

|

|

In a move that could foster greater investment in the commercial real estate sector, the Supreme Court on Thursday (October 3) provided relief to the industry by allowing the benefits of input tax credits (ITC) on construction costs for commercial buildings intended for leasing.

|

This ruling is expected to alleviate the financial burden of rents on tenants of commercial spaces.

|

Real estate players such as DLF, Max Estates, and Bharti Realty, among others, are likely to benefit, as buildings can now be classified as plant and machinery.

|

This benefit extends beyond commercial real estate, as rentals for commercial properties paid by various industries will also be eligible for ITC.

|

The ruling indicates that the benefit of ITC will be available retrospectively.

|

However, the industry is now seeking clarity from the government on whether similar relief should be extended to other sectors, including ports, airports, factories, warehousing, and data centers.

|

Background of the case

Safari Retreats filed a writ petition in the Odisha High Court, claiming eligibility for input tax credits on works contract services and other goods and services used in the construction of immovable property, excluding plant and machinery.

|

The Odisha High Court interpreted Section 17(5)(a) to allow for the availability of ITC.

|

Following this, the revenue department at the center filed a Special Leave Petition (SLP) in the Supreme Court, asserting that GST rules do not permit claiming ITC on immovable property.

|

Several petitioners subsequently approached the Supreme Court to challenge the constitutional validity of the provisions, as the Odisha High Court had not addressed this aspect.

|

In 2023, the Supreme Court concluded the matter but reserved its orders. Justice Abhay S. Oka and Justice Sanjay Karol pronounced the decision today.

|

The Supreme Court's ruling addressed three key questions. First, it examined whether the term “plant and machinery” in the explanation to Section 17(5) of the GST Act differs from “plant or machinery” referenced in Section 17(5)(d). Second, if these terms are indeed different, what should be understood by the term “plant”?

|

Third, the Court assessed the constitutional validity of the provisions in Sections 17(5)(c) and (d).

|

In a clear and detailed judgment, the Court ruled that the phrase “plant and machinery” in the explanation to Section 17(5) is distinct from the phrase “plant or machinery” in Section 17(5)(d). Consequently, the Court stated that it is essential to establish guiding principles to define what constitutes “plant.” While upholding the constitutional validity of Sections 17(5)(c) and (d), the Court emphasized that eligibility for ITC must be determined on a case-by-case basis.

|

According to the judgment, several factors must be considered when determining eligibility, including the nature of the taxpayer’s business, the role of the building or structure in delivering output services, and the functionality test—assessing whether the building contributes to the operational capabilities of the business. The Court clarified that these factors will help determine whether a building qualifies as a “plant” and, consequently, whether ITC should be allowed under Clauses (c) or (d).

|

Importantly, the Court upheld the taxpayer's submissions regarding Clause (d). Experts believe that lower adjudicating authorities will now decide ITC eligibility based on the specific facts and circumstances of each case.

|

This nuanced, fact-based approach is expected to guide future determinations on the subject.

|

To summarise, ITC was previously unavailable for the construction of commercial properties meant for leasing, as these were classified as immovable property.

|

Therefore, tenants could not claim ITC on the rents paid. Until now, leasing income attracted 18% GST without ITC.

|

Industry reaction

“The eligibility of input tax credit (ITC) will be determined based on the functionality and essentiality tests,” explained Abhishek A. Rastogi, founder of Rastogi Chambers, who represented multiple petitioners in the Supreme Court case.

|

“The essentiality test requires that the procurement of goods or services be directly essential to the business’s operations, while the functionality test assesses whether the inputs are functionally integral to the performance or output of the business. Therefore, unless it can be demonstrated that the claimed credits do not meet these criteria, the denial of credit would not be justified under the law," he said.

|

Rastogi emphasised that the judgment significantly narrows the circumstances under which ITC can be denied.

|

He noted that the Court’s approach provides greater clarity and fairness to businesses by ensuring that credit is denied only when the inputs are not integral to the functioning or operations of the business.

|

This ruling is expected to have a impact on how ITC claims are handled, especially concerning construction and immovable property, where the interpretation of what constitutes a “plant” or an essential business input has been contentious.

|

Rastogi concluded that this decision provides much-needed guidance for future cases and will likely serve as a key reference point for lower courts and adjudicating authorities in interpreting Section 17(5).

|

"The Supreme Court has upheld the Orissa High Court's judgment in Safari Retreat, allowing the availment of input tax credit for construction-related expenses when the immovable property is used for business purposes or for the construction of plant or machinery," Onkar Sharma, Partner, Khaitan & Co cheered.

|

This judgment is expected to have a major impact on the real estate and manufacturing sectors, depending on the factual scenario in each case, he emphasised.

|

Saurabh Agarwal, a Tax Partner at EY, noted that while the Revenue Department's appeal was allowed, the Court's acknowledgment that malls could, in certain situations, be classified as Plant and Machinery indicates a more adaptable interpretation of the law.

|

This ruling presents new opportunities for businesses, particularly in the real estate and commercial leasing sectors, to assess their eligibility for ITC on construction-related expenses.

|

Although the constitutional challenge was dismissed, the Court’s acceptance of the taxpayer’s arguments under Section 17(5)(d) is seen as a positive development. This outcome could reduce the financial burden on developers and encourage increased investment in commercial real estate.

|

Agarwal emphasised the need for the real estate industry to carefully analyze the implications of this ruling concerning ITC eligibility for outward supplies related to rental income.

|

He suggested that, in light of the Supreme Court's decision, the GST Council should provide clarifications that would enable real estate players to claim ITC on rental income.

|

Moreover, the ruling is expected to lower rental costs, as ITC would no longer represent a financial strain for the industry. It is essential to note that the ruling applies retrospectively from the inception of the GST; however, the deadline for claiming ITC for the period up to 2022-23 has already passed.

|

Nonetheless, industry participants can still claim ITC for FY 2023-24 until November 30.

|

|

|

|

|

|

The Supreme Court on Thursday declared that real estate companies can claim Input Tax Credits (ITC) under the Goods and Services Tax (GST) regime, on costs of construction for commercial structures intended for renting or leasing purposes.

|

The judgment by a Bench headed by Justice A.S. Oka would give a fillip to the real estate sector by lowering their investment costs. “If a building qualifies to be a plant, ITC can be availed against the supply of services in the form of renting or leasing the building or premises, provided the other terms and conditions of the CGST Act and Rules framed are fulfilled,” Justice Oka held.

|

The court, however, noted that if the construction of a building by the recipient of service was for his own use, the “chain would break and ITC would not be available”.

|

“Under the CGST Act, renting or leasing immovable property is deemed to be a supply of service, and it can be taxed as output supply. Therefore, if the building in which the premises are situated qualifies for the definition of plant, ITC can be allowed on goods and services used in setting up the immovable property, which is a plant,” Justice Oka reasoned.

|

The court said the question whether or not a mall, warehouse or any building other than a hotel or a cinema theatre could be classified as a ‘plant’ within the meaning of the expression “plant or machinery” in Section 17(5)(d) of the Central Goods and Services Tax Act, 2017 was a factual question.

|

This has to be determined keeping in mind the business of the registered person and the role that building plays in the business. “Functionality test will have to be applied to decide whether a building is a plant,” the judgment noted.

|

“ITC eligibility will be determined based on the functionality and essentiality tests,” explained Abhishek A. Rastogi, founder of Rastogi Chambers, who represented multiple petitioners in the case before the court. “In essence, the Court has effectively read down the provisions of Section 17(5)(c) and (d) of the GST Act. ITC can only be denied in situations where the nature of the taxpayer’s business and the claimed credits fail to satisfy these two critical tests,” he stressed.

|

|

|

|

|

|

The Supreme Court on October 3 made a landmark ruling that allows property owners to claim input tax credit, or ITC, on construction costs for rental buildings. This ruling is a major win for thousands of taxpayers who have faced legal challenges from GST departments. Watch the video with TNIE's Monika Yadav to take a dive into the details!

|

|

|

|

|

|

|

|

Adv. Pawan Arora, Partner of Athena Law Associates shares his viewpoint on the recent judgment of Hon'ble Supreme Court's in M/s. Safari Retreats Private Limited on the issue of eligibility of Input Tax Credit (ITC) on inputs used in the construction of shopping mall constructed for giving the units in it for rental purpose.

|

A. Outcomes of the Judgment

1. Summary of the Principles laid down by the Hon’ble Apex Court

|

i. A Building can be said to be a ‘plant’ for availment of ITC, if the construction of the said building is essential for carrying out the activity of supplying services such as renting or giving on lease or other transactions in respect of the building or a part thereof.

|

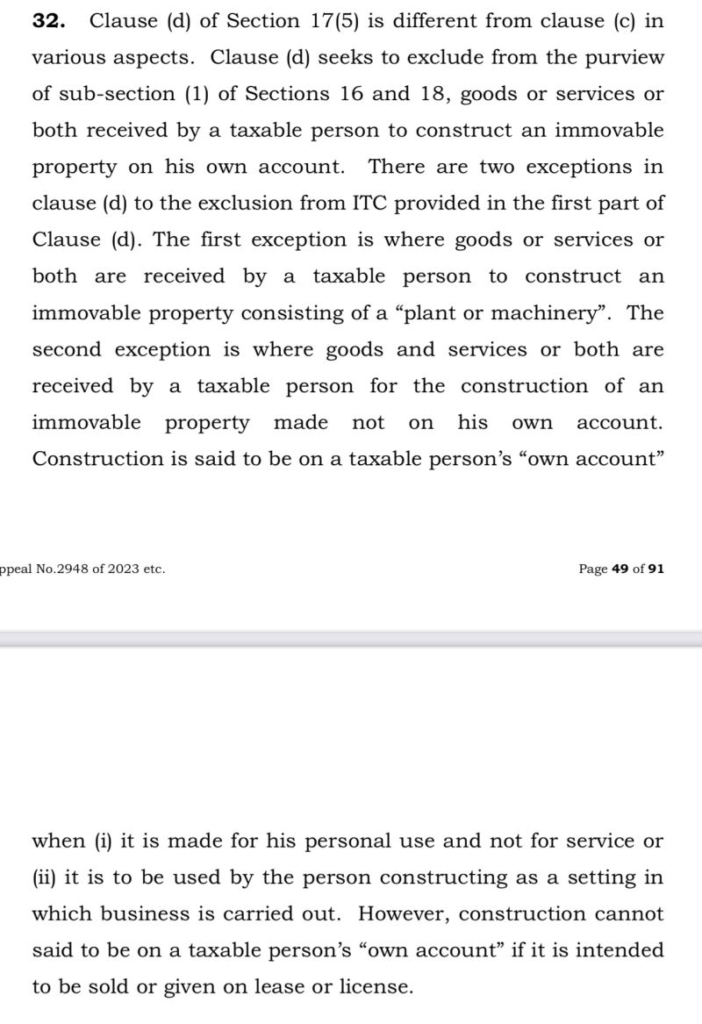

ii. Construction cannot be said to be on a taxable person’s “own account” if it is intended to be sold or given on lease or license.

|

iii. Functionality test will have to be applied to decide whether the construction of an immovable property is a “plant” in the facts of each case.

|

iv. A mall, warehouse or any building other than a hotel or a cinema theatre can be classified as a ‘plant’ within the meaning of the expression “plant or machinery” used in clause (d) of Section 17(5) by considering-

|

a. factual position in each case,

|

b. business of the registered person, and

|

c. the role of the mall/warehouse/building in the said business.

|

B. Detailed Analysis of the Judgment

i. Interpretation of the term “plant OR machinery” used in clause (d) of sub-section (5) of Section 17.

|

ii. Meaning of the word "plant".

|

iii. Constitutional Validity of Section 17(5) (c) & (d) and Section 16(4) of CGST Act.

|

i. The first respondent is engaged in construction of a shopping mall for the purpose of letting out premises in malls to different tenants. Vast quantities of material, inputs and services are required for construction of malls in the form of cement, sand, steel, aluminium, wires, plywood, paint, lifts, escalators, air-conditioning plants, electrical equipment, transformers, building automation systems etc., along with consultancy services, architectural services, legal and other professional services, engineering services and other services including the services of a special team of international designers specialised in the construction of malls.

|

ii. The letting out of units in the shopping mall by the first respondent attracts GST based on the rent received by the first respondent since it amounts to the supply of service under CGST Act.

|

iii. Therefore, the first respondent was desirous of availing the Input Tax Credit (ITC) accumulated against the rental income received on letting out the mall premises.

|

4. Analysis of Clauses (c) and (d) of Section 17(5) by the Hon’ble Apex Court

|

I. Interpretation of the term “Plant OR Machinery” used in clause (d)

|

i. There is hardly any similarity between clauses (c) and (d) of Section 17(5). The only similarity is that, both apply to construction of an immovable property.

|

ii. Clause (c) uses the expression “plant and machinery”, which is specifically defined in the explanation whereas Clause (d) uses the expression “plant or machinery”, which is not specifically defined.

|

iii. The legislature has intentionally used the expression “plant or machinery” in clause (d) as distinguished from the expression “plant and machinery” used in several places.

|

iv. The expression “plant and machinery” and “plant or machinery” cannot be given the same meaning.

|

v. When the legislature uses the expression “plant and machinery,” only a plant will not be covered by the definition unless there is an element of machinery or vice versa. This expression cannot be read as “plant or machinery”.

|

vi. The expression “plant or machinery” has a different connotation. It can either be a Plant or Machinery.

|

vii. The very fact that the expression “immovable property other than plant or machinery” is used, shows that there could be a plant that is an immovable property.

|

viii. As the word ‘plant’ has not been defined under the CGST Act or the rules framed thereunder, its ordinary meaning in commercial terms will have to be attached to it.

|

ix. The Court has earlier-

|

-

-

- laid down the functionality test.

- held that whether a building is a plant, is a question of fact.

- held that if it is found on facts that a building has been so planned and constructed as to serve an assessee’s special technical requirements, it will qualify to be treated as a plant for the purposes of investment allowance.

x. The word ‘plant’ used in a bracketed portion of Section 17(5)(d) cannot be given the restricted meaning provided in the definition of “plant and machinery”, which excludes land, buildings or any other civil structures. Therefore, in a given case, a building can also be treated as a plant, which is excluded from the purview of the exception carved out by Section 17(5)(d) as it will be covered by the expression “plant or machinery”.

|

xi. To give a plain interpretation to clause (d) of Section 17(5), the word “plant” will have to be interpreted by taking recourse to the functionality test. Therefore, if a building qualifies to be a plant, ITC can be availed against the supply of services in the form of renting or leasing the building or premises.

|

xii. Renting or leasing immovable property is deemed to be a supply of service, and it can be taxed as output supply. Therefore, if the building in which the premises are situated qualifies for the definition of plant, ITC can be allowed on goods and services used in setting up the immovable property, which is a plant.

|

xiii. A developer may construct a mall predominantly to sell the premises therein, after obtaining an occupation certificate. Therefore, it will be out of the purview of clause 5(b) of Schedule II. Each case will have to be tested on merits as the question whether an immovable property or a building is a ‘plant’, is a factual question to be decided.

|

xiv. Functionality test will have to be applied to decide whether a building is a plant. Therefore, by using the functionality test, in each case, on facts, in the light of what the Court has held earlier, it will have to be decided whether the construction of an immovable property is a “plant” for the purposes of clause (d) of Section 17(5).

|

xv. The matter has been remanded back for the limited purpose to decide on facts, whether the mall in question satisfies the functionality test so that it can be termed as a ‘plant’ within the meaning of bracketed portion in Section 17(5)(d). The same applies to warehouses or other buildings except hotels and cinema theatres.

|

xvi. While deciding these cases, no final adjudication has been made on the question whether the construction of immovable property carried out by the petitioners in Writ Petitions amounts to ‘plant’, and each case will have to be decided on its merit by applying the functionality test in terms of this judgment. The issue must be decided in appropriate proceedings in which adjudication can be made on facts. The petitioners are free to adopt appropriate proceedings or raise the issue in appropriate proceedings.

|

II. Interpretation of term “on his own account” used in clause (d)

|

i. Construction is said to be on a taxable person’s “own account” when it is,

|

a. made for his personal use and not for service; or

|

b. to be used by the person constructing it, as a setting to carry out its business.

|

ii. However, construction cannot be said to be on a taxable person’s “own account” if it is intended to be sold or given on lease or license.

|

i. There is no scope to give any other meaning to clause (c) of Section 17(5), than its plain and natural meaning.

|

ii. The expression “plant and machinery” has been specifically defined in the explanation to Section 17.

|

iii. The Court cannot add or subtract anything from clause (c).

|

iv. ITC is a creation of legislature. Therefore, legislature can exclude specific categories of goods or services from ITC.

|

v. Exclusion of the category of works contracts by clause (c) will not per se defeat the object of the CGST Act.

|

5. Constitutional Validity

|

i. The Hon’ble Apex Court has held that the challenge to the constitutional validity of clauses (c) & (d) of Section 17(5) and Section 16(4) of the CGST Act is not established.

|

C. INTERPRETATION OF TAXING STATUTES

6. Principles governing the Interpretation of Taxation Statutes as summarised by the Hon’ble Apex Court in para 25 of the Judgment

|

i. A taxing statute must be read ‘as it is’ with no additions and no subtractions on the grounds of legislative intendment or otherwise;

|

ii. If the language of a taxing provision is plain and the consequence of giving effect to it may lead to some absurd result, it is not a factor to be considered when interpreting the provisions. It is for the legislature to step in and remove the absurdity;

|

iii. While dealing with a taxing provision, the principle of strict interpretation should be applied;

|

iv. If two interpretations of a statutory provision are possible, the Court ordinarily would interpret the provision in favour of a taxpayer and against the revenue;

|

v. In interpreting a taxing statute, equitable considerations are entirely out of place;

|

vi. A taxing provision cannot be interpreted on any presumption or assumption;

|

vii. A taxing statute has to be interpreted in the light of what is clearly expressed. The Court cannot imply anything which is not expressed. Moreover, the Court cannot import provisions in the statute to supply any deficiency;

|

viii. There is nothing unjust in the taxpayer escaping, if the letter of the law fails to catch him on account of the legislature’s failure to express itself clearly;

|

ix. If literal interpretation is manifestly unjust, which produces a result not intended by the legislature, only in such a case can the Court modify the language;

|

x. Equity and taxation are strangers. But if construction results in equity rather than injustice, such construction should be preferred;

|

xi. It is not a function of the Court in the fiscal arena to compel the Parliament to go further and do more;

xii. When a word used in a taxing statute is to be construed and has not been specifically defined, it should not be interpreted in accordance with its definition in another statute that does not deal with a cognate subject. It should be understood in its commercial sense. Unless defined in the statute itself, the words and expressions in a taxing statute have to be construed in the sense in which the persons dealing with them understand it, i.e., as per the trade understanding, commercial and technical practice and usage.

|

D. Words of wisdom by the Hon'ble Apex Court for Good Advocacy

i. Brevity is the hallmark of good advocacy.

|

ii. The Judges and lawyers are humans and sometimes, bulky compilations & submissions can be counterproductive.

|

|

|

|

|

|

No, the Honorable High Court of Allahabad in the case of M/s Vijay Trading Company vs. Additional Commissioner Grade 2 and Another (Writ Tax no.1278 of 2024 dated 20.08.2024) quashed the assessment order stating that the law is clear on the subject that the proceedings under section 130 of the GST Act cannot be put to service if excess stock is found at the time of the survey.

|

The Honorable Court observed after carefully reviewing the arguments and the relevant legal provisions, it is evident that the petitioner's contentions hold merit. It is not disputed that the survey conducted on 11.05.2022 did result in a finding of excess stock. However, this Court has consistently held that when such findings are made, the appropriate legal recourse is to initiate proceedings under Sections 73/74 of the GST Act. These sections provide a structured process for determining and rectifying discrepancies in tax filings or stock records, ensuring that the taxpayer is given a fair opportunity to respond and rectify any issues. Section 130, on the other hand, is intended for more serious cases where there is evidence of fraudulent intent or gross negligence in tax matters. This position was reaffirmed in the recent judgment of this Court in Dinesh Kumar Pradeep Kumar, where it was clearly stated that proceedings under Section 130 should not be invoked for mere discrepancies in stock. The Honorable Court emphasized that the tax authorities must follow the procedures laid out in Sections 73/74 for assessing and resolving such matters. The Honorable Court stated that given these findings, the impugned orders dated 03.04.2024 and 24.01.2023 cannot be sustained in law. The failure to follow the appropriate legal procedures under the GST Act, combined with the questionable method of stock assessment, renders these orders legally unsound. As a result, the orders are hereby quashed.

|

Author’s Comments

“Due Process” of law demands, the exercise of specific powers conferred to the Proper officer within specific boundaries of the law. Passion to protect the interest of revenue does not authorize the by-passing of the law.

|

Section 35(6) of the CGST Act, 2017 covers the situation of shortage of stock. In the considered opinion of the Author, there is no provision under the law to cover the situation of excess stock is found. In case of excess stock found, Section 130 of the CGST Act cannot be invoked as decided in this case. Further, there is no cause-of-action to invoke section 74 of the CGST Act. In case of Excess stock, it can be alleged that goods are received without invoice, in such a situation; action can be taken against the supplier only for contravention of the provisions of this law and not against the recipient. Necessary ingredients to establish levy are not attracted in case of excess stock found, to demand tax under section 74 of the Act.

|

|

|

|

|

|

Yes, the Honorable High Court of Calcutta in the case of Limton Metals Ltd. v. Superintendent dated 25 June 2024 dismissed the writ petition challenging orders for cancellation of registration. The petitioner argued that the notice did not comply with section 29 provisions, as it did not specify the reasons for the cancellation and the notice mentioned "Others" under the reasons column, which the petitioner claimed was insufficient disclosure. The Honorable Court observed that the petitioners have advanced arguments that the show cause notice did not identify and/or specify the reasons, it would however, transpire from the show cause, that it referred to certain supportive documents which that were also made available to the petitioner along with the aforesaid show cause notice indicating that the petitioner was suspected of being a fake entity used to pass on irregular Input Tax Credit (ITC) without actual supply. However, mere disclosure of reasons does not satisfy the requirement of the provisions contained in Rule 25 of the CGST Rules, 2017. However since the petitioner is reluctant to cooperate with further inspection, it raises serious doubts regarding the bona fide of the petitioners.

|

The Honorable Court stated that although the procedure adopted by the respondents to cancel the petitioner's registration under the said Act may not be strictly as per the procedure laid down, however, the same cannot be said to be per se illegal or without any basis. The writ petition was dismissed, as the court concluded that the petitioner had been informed of the reasons for the cancellation.

|

Author’s Comments

It is common to find that demand in a notice is arbitrary. It is important to note that allegations in support of a demand may lack some essential ingredients and that may offer grounds to assail the notice on the ground of ‘arbitrariness’. Now section 160(1) can be relied upon in adjudication to overcome this allegation. Not everything that is vague or difficult to comprehend can be called as arbitrary. Arbitrariness demands a certain minimum level of understanding of the subject before capable of declaring something to be arbitrary. A Defense that relies upon arbitrariness bears the burden to demonstrate the exact level of the unintelligibility of the allegation in the notice that goes to the root of the demand and destroys it completely.

|

Arbitrariness must be advanced as a defense with great circumspection because faced with arbitrariness, there remains nothing more to be said by way of defense and arbitrariness ends any further defense. Other ground in addition to arbitrariness is a contradiction-of-sorts.

|

|

|

|

|

|

In the case of Shree Shyam Steel v. Union of India (WP(C)/3838/2024), the Honorable Gauhati High Court admitted the challenge to Notification No. 56/2023-CE issued by the Central Board of Indirect Taxes and Customs (CBIC). The notification extended the deadline for passing orders under Section 73(9) of the CGST Act, 2017 for the financial years. 2018-2019 and 2019-2020. The Honorable Court provided interim protection to the petitioners, prohibiting any coercive action based on the notification. The petitioner contended that the notification was issued without the mandatory recommendation of the GST Council, as required under Section 168A of the CGST Act, 2017.

|

Although the GST Council had previously made a recommendation for extending deadlines, reflected in Notification No. 9/2023-CE dated 31.03.2023, however, no such recommendation was made for the extensions in Notification No. 56/2023-CE. The Honorable Court further noted that the petitioner has argued that there is no corresponding notification issued by the Assam GST department for extending timelines. The Honorable Gauhati High Court held that Notification No. 56/2023-CE was prima facie not in consonance with Section 168A of the CGST Act, 2017. The Honorable Court found that the notification could not stand the scrutiny of law due to the absence of the necessary recommendation from the GST Council. Further directed the respondents to file affidavits.

|

At many instances, there is no recommendation of the GST Council, yet CBIC rolls out the notifications and then recommendation are ratified by the GST Council at a later stage. The Argument that there is no recommendation of the GST Council to extend the timelines might not hold the ground tightly to declare such notifications ultra-vires the law. Further, section 11(4) of the state GST Act gives the power to states that notification issued by the Central Government will be deemed to be issued under the State Act also. Thereby, there is no need for separate notifications to be issued by the State.

|

|

|

|

|

|

Mr. B. Venkateswaran I.R.S, Assistant Commissioner, Central GST (Retired) presented his note on the Circular no. 212/6/2024 dated 26.06.2024 as below.

|

This circular clarifies the conditions under which discounts provided by suppliers via tax credit notes after supply should not be included in the taxable value. It also provides a mechanism for verifying the reversal of Input Tax Credit (ITC) by recipients. The goal is to ensure uniform implementation of Section 15(3)(b)(ii) across tax departments until a permanent system functionality is introduced.

|

When suppliers provide discounts via tax credit notes after a supply has been made, these discounts may be excluded from the taxable value, but specific conditions must be met.

|

Conditions for Discount Exclusion:

|

- Pre-existing Agreement: The discount must be established in an agreement made at or before the time of supply.

- Linking to Invoices: The discount should be directly linked to specific invoices to ensure traceability.

- Reversal of ITC: The recipient must reverse the proportionate ITC related to the discount to ensure that the ITC claimed on the original supply is adjusted in line with the discounted value.

Verification and Compliance Mechanism:

|

Currently, there is no functionality on the GST common portal for suppliers or tax officers to verify the recipient's ITC reversal. This has caused issues in the field, and the circular proposes a temporary solution:

|

For Total Tax Exceeding ₹5 Lakhs:

|

When the combined CGST, SGST, and IGST on discounts in a financial year exceed ₹5,00,000, suppliers must obtain a certificate from the recipient, issued by a Chartered Accountant (CA) or Cost Accountant (CMA). The certificate must certify that the recipient has reversed the required proportionate ITC.

|

The certificate must include:

|

- Credit notes and invoice details.

- Amount of ITC reversed for each credit note.

- Document reference confirming the reversal (e.g., FORM GST DRC-03 or return).

For Total Tax Below ₹5 Lakhs:

|

If the total tax on discounts in a financial year does not exceed ₹5,00,000, suppliers can obtain an undertaking or certificate directly from the recipient, without needing CA/CMA certification. This certificate should also detail the ITC reversal.

|

These certificates or undertakings will serve as valid evidence of compliance with Section 15(3)(b)(ii) and should be presented during audits or investigations.

|

This mechanism can also be applied retroactively to past transactions. Suppliers may obtain the required certificates or undertakings as evidence for previous periods if needed by the tax authorities.

|

PLEASE SCROLL DOWN TO SEE SUGGEST FOMAT.

|

Suggested Sample Certificate Formats:

|

Certificate Format 1: For Tax Exceeding ₹5 Lakhs

|

CERTIFICATE OF INPUT TAX CREDIT REVERSAL

|

(Under Section 15(3)(b)(ii) of the CGST Act 2017) As per Circular No. 212/6/2024-GST dated 26-06-2024

|

Subject: Certificate of Reversal of Input Tax Credit (ITC) on Discounts Provided Through Credit Notes for Financial Year

|

I/We,…………………………………. , a practicing Chartered Accountant/Cost Accountant (Membership No………………………… ), having office at , certify that M/s………………………………………. and holder of GSTN NO……………………. (GSTIN: ) has duly reversed the Input Tax Credit (ITC) related to discounts provided through credit notes for Financial Year , amounting to Rs. (IGST: Rs. , CGST: Rs. , SGST: Rs. ). As details in the enclosed Annexure.

|

2. I/We confirm that this information is true to the best of my/our knowledge. This certificate is issued in accordance with Circular No. 212/6/2024-GST dated 26th June 2024 to serve as evidence of compliance with Section 15(3)(b)(ii) of the CGST Act 2017.

|

Membership No.:

UDIN No.:

Date:

|

Certificate Format 2: For Tax Below ₹5 Lakhs

|

CERTIFICATE OF INPUT TAX CREDIT REVERSAL

(Under Section 15(3)(b)(ii) of the CGST Act 2017)

|

As per Circular No. 212/6/2024-GST dated 26-06-2024

|

Subject: Certificate of Reversal of Input Tax Credit (ITC) on Discounts Provided Through Credit Notes for Financial Year

|

I/We, ………………………….., having principal place of business at………………………… , with GSTIN………………………… , certify that we have duly reversed the Input Tax Credit (ITC) related to the discounts provided via credit notes for Financial Year , amounting to Rs. (IGST: Rs. , CGST: Rs. , SGST: Rs. ) as per the details re provided in the enclosed Annexure.

|

2. I/We confirm that this information is true to the best of my/our knowledge. This certificate is issued in accordance with Circular No. 212/6/2024-GST dated 26th June 2024 to serve as evidence of compliance with Section 15(3)(b)(ii) of the CGST Act 2017.

|

This certificate format and the accompanying content are provided solely for informational purposes and to assist with compliance under Circular No. 212/6/2024-GST dated 26-06-2024. The use of this format should be done in consultation with a qualified professional, such as a Chartered Accountant (CA) or Cost Accountant (CMA).

|

This document does not constitute legal or financial advice, and the applicability of the content may vary based on specific circumstances. Users are advised to seek professional advice to ensure full compliance with the Central Goods and Services Tax Act, 2017, and any other relevant legislation.

|

|

|

|

|

|

With due respect to the Hon’ble Supreme Court ruling, my personal takeaway is that the ruling seems to have overlooked some crucial aspects (as apparent from para 32) and therefore, a review could be essential. Here are a few points:

|

1. Interpretation of "own account";

|

- The ruling defines "own account" as situations where construction is made for personal use and not for service.

- It is intended for use by the person constructing as the setting for their business operations.

|

It’s important to note that any input tax credit for personal use is already restricted under Section 17(1) of the CGST Act. Hence, the same interpretation should not be applied under Section 17(5)(d) while using the term "own account”

|

2. Incomplete articulation of Section 17(5)(d);

|

- The ruling partially addresses Section 17(5)(d), with no discussion on the latter part that includes the phrase “including when such goods or services or both are used in the course or furtherance of business”

- A complete articulation might have led to a different outcome

|

3. Expressions 'course' and 'furtherance':

|

- The expressions "course" and "furtherance" are pivotal. While "course" may indicate the regular conduct of business, "furtherance" implies the advancement or promotion of business.

- These terms significantly impact the interpretation of "own account" and could have altered the ruling’s implications

|

|

Let’s see how this unfolds…

|

|

|

|

|

|

|

|

|

4. Lawgics by Ms.Nidhi Aggarwal

|

Ms. Nidhi Aggarwal is delighted to present judgment with a great vision to spread complex GST law in a simple manner amongst the taxpayers, tax professionals, students and knowledge seeker.

|

|

Recently added notes are listed below:

|

|

|

|

|

|

Synopsis: The Delhi High Court dismissed the writ petition involving fraudulent ITC claims, directing the petitioner to pursue appellate remedy u/s 107 of the CGST Act.

|

Caste name: Banson Enterprises & Anr. vs Assistant Commissioner CGST & Ors.

|

Citation: W.P. (C) 6503/2025 dated 15.05.2025

|

Authority: Delhi High Court

|

The petition challenges the Order-in-Original dated 02.02.2025 based on a Show Cause Notice (SCN) dated 03.08.2024 A search was conducted, and statements were recorded including that of one Director admitting to the issuance of fake invoices during the Central Excise period. It was alleged that the Petitioner issued goods-less invoices to enable fraudulent Input Tax Credit (ITC) claims amounting to Rs. 1.85 crore.

|

Contentions of the Petitioner:

|

SCN was issued by unauthorized officer, thus, violates Rule 142(1)(a) of CGST Rules. No pre-consultation as required under Rule 142(1A) of CGST Rules was issued. Consolidated SCN for multiple financial years was issued and challenge to such consolidated action is pending in a separate matter (Quest Infotech case).

|

Contentions of the Department:

The impugned order is appealable, hence writ is not maintainable. The Petitioner’s Director admitted to allegations. Natural justice was followed as the Petitioner received the SCN, filed a reply, and availed of personal hearing. Reliance must be made on SC judgments and Allahabad HC rulings emphasizing alternate remedy u/s 107 CGST Act.

|

Findings and Decision of the Court:

The Court refused to interfere under writ jurisdiction, citing:

|

- No breach of fundamental rights or principles of natural justice.

- Availability of a statutory remedy (appeal) under Section 107 CGST Act.

The Court noted that the Allegations involve serious misuse of ITC, requiring fact-based adjudication, not suited for writ jurisdiction. Thus, the Petitioner was granted liberty to file appeal, and if filed with pre deposit, the appeal shall not be dismissed on limitation.

|

|

|

|

|

|

5. GST Notes by CMA Anil Sharma

1) New slides on GST Circulars is added in the Notes section titled as "Capsules".

|

- Total 25 slides in capsule-01 is added

|

|

|

|

|

|

|

|

6. GST Daily by CA Pradeep Modi

CA Pradeep Modi is presenting judgment analysis under title 'GST Daily - Stay yourself updated'

|

|

|

|

|

|

THE HON'BLE ALLAHABAD HIGH COURT IN THE CASE OF Vibhuti Tyres V/s State of U.P., decided on 7-5-2025

|

✔️ Is it justified that GST order with higher demand than show-cause notice?

|

👉 The Hon'ble High Court Judgement:-

|

✔️ Where in show-cause notice amount representing tax, interest and penalty was indicated as Rs. 8,81,080, but in order, much higher demand was raised at Rs. 32,97,336, same was in violation of section 75(7); matter was to be remanded back.

|

Section 75 of Central Goods and Services Tax Act, 2017

|

|

|

|

|

|

7. PPT/Handbook on GST

|

|

|

|

8. GST/Income Tax in Media

|

|

|

|

|

|

|

|

|

|

|

|

Recap of Latest updates posted on 30.06.2026

|

Complete CGST, IGST, and Compensation Cess Acts & All Rules and GSTAT Rules

|

The government has extended the due date for filing of appeal before the Goods and Services Tax Appellate Tribunal (GSTAT) under section 112(1) read with section 112(3) to 31.07.2026.

|

Centre has extended the last date for filing appeals before the Goods and Services Tax Appellate Tribunal (GSTAT) to July 31, 2026, giving taxpayers an additional month to submit their cases after a surge in filings led to technical difficulties on the GSTAT portal.

|

GST & IDT Committee has requested the Chairman, IDT Committee, ICAI, New Delhi to urgently represent before the respective forums for the date extension of GSTAT, i.e., 30-Jun-2026.

|

The Union government on Tuesday granted a six-month extension to the tenure of Central Board of Direct Taxes (CBDT) Chairman Ravi Agrawal till December 2026.

|

The central government is working on a scheme to bear 90 per cent of the CBAM compliance costs for MSMEs as exporters grapple with the European Union's new carbon border tax that came into force this year..

|

In a major operation the officers of the Directorate of Revenue Intelligence (DRI) successfully dismantled a trans-border gold smuggling syndicate and seized 15 kg foreign-origin smuggled gold, valued at approximately Rs. 21.40 crore, operating from Delhi.

|

The Government had earlier provided a full Customs Duty exemption on imports of critical petrochemical products till 30th June 2026…

|

Export consignments to West Asia will continue to receive enhanced insurance cover against payment defaults until September 30, the Directorate General of Foreign Trade (DGFT) said in a notification on Monday.

|

The Hon'ble Madras High Court pronounced on 08.06.2026 in the case of M/s. Fastenex Private Limited that GST Notices u/s 74 Cannot Fail Solely Because Multiple Financial Years Are Covered.

|

|

|

|

|

|

|

|

|

Recap of Latest updates posted on 29.06.2026

|

MCTC made a representation to FM Smt. Nirmala Sitharaman, on 26.06.2026 requesting an extension of the deadline for filing GSTAT appeals from 30th June 2026 to 31st December 2026.

|

Tax professionals, chartered accountants and industry bodies have urged the Finance Ministry to extend the filing window, warning that persistent technical glitches on the GSTAT portal could prevent thousands of taxpayers from filing their appeals before the deadline.

|

On the occasion of 9th GST Day to be celebrated on 1st July, 2026 the CBIC has decided to grant Certificate of Meritorious Service (CBIC-CMS) to the following officers:

|

Businesses shifting their principal place of business to a new GST jurisdiction will not have to restart pending tax proceedings..

|

Commerce ministry has convened a meeting of stakeholders on June 30 to discuss issues related to SEZs, including reforms aimed at harmonising export promotion schemes and easing business operations in the enclaves.

|

Tata Steel Limited said tax authorities have filed an appeal seeking restoration of penalties worth Rs. 368.72 crore that were earlier dropped in a GST adjudication order

|

GSTAT , Vijayawada Bench, Andhra Pradesh will be functioning from its new premises at Mangalagiri, Guntur from 01.07.2026

|

The Hon’ble Madras High Court in P. Baskaran set aside the order imposing interest and penalty u/s 74 of CGST Act and remanded the matter for fresh consideration on the applicability of Section 74

|

The Hon’ble Madras High Court (Madurai Bench) in Tvl. Manickavasagam S. set aside the assessment order passed under Section 74 of the TNGST Act pertaining to levy of GST on seigniorage fees

|

The Hon’ble Gauhati High Court in M/s Metal Syndicate and Another set aside the OIO and the OIA confirming GST demand of Rs. 78,70,952/- along with interest and equivalent penalty, and held that a bona fide purchasing dealer cannot be denied ITC merely on account of the supplier’s failure to deposit the tax collected with the Government.

|

The Hon’ble Allahabad High Court in Ashish Tyagi allowed the habeas corpus petition and declared the arrest and consequent detention of the assessee under Section 132 of the CGST Act as illegal

|

|

|

|

|

|

|

|

|

Recap of Latest updates posted on 28.06.2026

|

CBDT issued notification no. 71/2026 dated 25.06.2026 to hereby approves deductions to the University of Hyderabad for Scientific Research under the category of university, college or other institution.

|

CBDT issued notification no. 72/2026 dated 25.06.2026 to hereby approves deductions under section 45(3)(a)(i) of the Income-tax Act, 2025 to the Public Health Foundation of India, Delhi for Scientific Research under the category of University, college or other institution.

|

Indian enterprises are rapidly advancing in artificial intelligence (AI) adoption and a growing cohort has embedded AI into the core of operations.

|

Several important financial changes are set to take effect on July 1, 2026. These changes could impact taxpayers, bank customers, credit card users, passport applicants and Aadhaar card holders.

|

DRI has successfully unearthed and dismantled a highly organised gold smuggling syndicate operating through Mumbai Airport.

|

|

|

|

|

|

|

|

|

Recap of Latest updates posted on 27.06.2026

|

All officers and staff of GSTAT, Ranchi Bench, are hereby directed to remain available on 28.06.2026 (Sunday) and extend all necessary assistance for resolving any last-minute difficulties…

|

KSCAA has submitted a representation highlighting practical and procedural issues faced by taxpayers and professionals in relation to GSTAT…

|

Kolkata is likely to host the 57th meeting of the GST Council next month, sources said, although the Union Finance Ministry has not yet officially confirmed the venue or the schedule.

|

Sources indicated that Das is being considered for the post of Union finance minister, while the incumbent , Nirmala Sitharaman, is expected to be shifted to the human resource development (HRD) ministry.

|

Mr. S.K. Rahman, Member (Technical), GST Appellate Tribunal, Chennai Bench address audience at BCAS 20th Residential Study Course on GST held at ITC Grand Chola, Chennai on 26th, June, 2026.

|

Adv. Ashu Dalmia of ADA Law Chambers, prepared this PPT on topic "GST Litigation - Key issues & Case laws".

|

Author: Abhishek Goyal M.Com, FCS, LLB | Edition: 1st Ed. 2026 | Publisher: Bharat Law House

|

|

|

|

|

|

|

|

|

Recap of Latest updates posted on 26.06.2026

|

EPFO has announced that its member portal, employer portal and UMANG app services will be temporarily unavailable due to scheduled system migration from June 26 to 30.

|

CBIC issued Circular no. 255/01/2026-GST dated 25.06.2026 to provide Clarification regarding jurisdiction in cases involving migration/ transfer of …

|

GSTN is taking downtime to enhance its services on the GST Portal on 27.06.2026 from 12:00 AM onwards until 2:30 am of 27.06.2026.

|

Residents living along Punjab’s State boundary with Himachal Pradesh, including traders, truck operators and taxi drivers, have united under the banner of the ‘Sangarsh Morcha’ to oppose Himachal Pradesh’s vehicle entry tax.

|

US Treasury Secretary Scott Bessent said tariff rates could return to their previous levels if ongoing Section 301 investigations conclude successfully, signaling the Trump administration intends to preserve much of its tariff framework even after shifting away from emergency powers.

|

Many market participants believe that the South Korean market has also been weighted down by the government's new proposal to tax unrealised gains.

|

Author: Abhishek Goyal M.Com, FCS, LLB | Edition: 1st Ed. 2026 | Publisher: Bharat Law House

|

|

|

|

|

|

|

|

|

Sales Tax Bar Association (Regd.) (STBA) made representation for extension of the time limit for filing appeals before the Goods and Services Tax Appellate Tribunal (GSTAT) vide letter reference STBA/2026/25 dated 25.06.2026

|

Madanapalle police in Annamayya district arrested two interstate accused for allegedly cheating a Bengaluru-based techie from Tirupati district.

|

Exporters flagged delays in EPCG and Advance Authorisation approvals, difficulties in updating Importer-Exporter Code profiles, customs clearance backlogs, digital signatures on online portals, and pending Integrated Goods and Services Tax (IGST) refunds.

|

The Uttar Pradesh Electricity Regulatory Commission (UPERC) has ruled that the reduction in GST on renewable energy equipment from 12% to 5% will be treated as a “Change in Law” event under power purchase agreements signed under the PM-KUSUM Component-C2 scheme.

|

A Kanpur man is making headlines after he received relief from the Income Tax Appellate Tribunal (ITAT) in a case involving a Rs 1.95 crore trading loss incurred through his wife’s account.

|

|

|

|

|

|

|

|

|

Taxation Bar Association, Agra represented by General Secretary Adv. Akhilesh Bhatnagar made representation to Hon'ble Smt. Nirmala Sitharaman vide Letter dated 22.06.2026.

|

GSTAT Bar Association, Delhi made a representation before CBIC vide Letter dated 20.06.2026 seeking extension of the last date for filing appeals before GSTAT.

|

whether partners of a partnership firm could be personally penalized under Section 122(1A) of the CGST Act, 2017 for tax evasion committed by the firm ?

|

The Hon’ble Punjab and Haryana High Court in the case of Hudson Insurance Brokers Private Limited held that an order passed without assigning any reasons and without considering the reply of the assessee is a non-speaking order and violative of principles of natural justice, and therefore liable to be set aside.

|

The Hon’ble Bombay High Court in the case of Rika Global Impex Limited held that benefit under the RoDTEP Scheme cannot be denied to exporters of sugar merely because the export was categorized as ‘restricted’, ..

|

The question is this: Will the government extend the filing date? There is no clarity. While many feel that the government is in no mood to extend the deadline

|

|

|

|

|

Hope the above updates is of use to you. Please share your input and feedback at taxupdate.otu@gmail.com

|

|

|

|

|

|

|

|

|

Visit our website

|

OTU provides you

|

- Articles on various topics

|

|

- Media - GST, Income Tax & Press R.

|

|

|

|

|