|

|

|

Newsletter no. 74 dated 06.03.2023

|

|

|

|

|

|

This website contains information about recent changes mainly in GST laws. It also contains Articles on various topic in GST. Please visit the website and read more.

|

|

|

|

Index

|

5. Book by CMA Anil Sharma

|

|

|

|

|

|

|

|

GSTN is taking downtime to enhance its services on the GST Portal on 27.06.2026 from 12:00 AM onwards until 2:30 am of 27.06.2026.

|

|

We shall be enhancing services on the GST portal on : 27th June’26 12:00 AM onwards. GST Portal services will not be available until 27th June’26 02:30 AM. The inconvenience caused is regretted.

|

|

|

|

|

|

|

|

|

|

|

Central Board of Direct Taxes (CBDT) issued notification no. 72/2026 dated 25.06.2026 to hereby approves deductions under section 45(3)(a)(i) of the Income-tax Act, 2025 and rules 32 and 34 of the Income-tax Rules, 2026 to the Public Health Foundation of India, Delhi (PAN: AABAP4445L) for Scientific Research under the category of University, college or other institution.

|

|

|

|

|

|

|

|

Central Board of Direct Taxes (CBDT) issued notification no. 71/2026 dated 25.06.2026 to hereby approves deductions u/s 45(3)(a)(i) of the Income-tax Act, 2025 and rules 32 and 34 of the Income-tax Rules, 2026 to the University of Hyderabad (PAN: AAAAU8109M) for Scientific Research under the category of university, college or other institution.

|

|

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Notification no. 02/2026 – Central Tax dated 07.05.2026.

|

GOVERNMENT OF INDIA

MINISTRY OF FINANCE

DEPARTMENT OF REVENUE

|

Notification No. 02/2026 – Central Tax dated 07.05.2026

|

S.O. 2286(E).— In exercise of the powers conferred by sub-section (1A) of section 101A of the Central Goods and Services Tax Act, 2017 (12 of 2017) (hereinafter referred to as the said Act), the Central Government, on the recommendations of the Council, hereby empowers the Principal Bench of the Appellate Tribunal, New Delhi constituted under sub-section (3) of section 109 of the said Act, to hear appeals made under section 101B of the said Act.

|

This notification shall be deemed to have come into force on the 1st day of April, 2026.

|

BALASUBRAMANIAN KRISHNAMURTHY,

Joint Secretary

|

|

|

|

|

|

|

|

Central Board of Direct Taxes (CBDT) issued notification no. 70/2026 dated 01.06.2026 to hereby specifies the business (other than the business specified in Note 5(d)(i) of the said Schedule), which is engaged in the infrastructure sub-sectors mentioned in the Updated Harmonised Master List of Infrastructure sub-sectors, in the notification of the Government of India in the Ministry of Finance, Department of Economic Affairs number F.No.13/1/2025-IPP, dated the 19th September, 2025, published in Gazette of India, Extraordinary, Part I, Section 1, as a business for the purposes of Schedule V of the said Act.

|

This notification shall come into force from the date of its publication in the Official Gazette.

|

|

|

|

|

|

|

|

Central Board of Direct Taxes (CBDT) issued notification no. 69/2026 dated 30.05.2026 to provide deduction u/s 45(3)(a)(i) of the Income-tax Act, 2025 and rules 32 and 34 of the Income-tax Rules, 2026 to the National Institute of Advanced Studies, Bangalore (PAN: AAATN2269A) for Scientific Research under the category of University, college or other institution, for the purposes of section 45(3)(a)(i) of the said Act of 2025 and rules 32 and 34 of the Income-tax Rules, 2026.

|

This notification shall be applicable to the National Institute of Advanced Studies, Bangalore for the tax years 2026-2027 to 2030-2031, subject to the conditions that it shall–

|

(i) comply with the conditions specified in rule 34 of the Income-tax Rules, 2026;

|

(ii) prepare statement under section 45(4)(a) of the Income-tax Act, 2025 for each tax year in Form No.15 and deliver or cause to be delivered to the Director General of Income-tax (Systems) or the person authorised by him on or before the 31st May, immediately following the tax year in which the donation is received, in accordance with rule 31 of the Income-tax Rules, 2026:

|

(iii) furnish to the donor, a certificate in Form No.16 specifying the amount of donation in accordance with rule 31 of the Income-tax Rules, 2026.

|

|

|

|

|

|

|

|

Central Board of Direct Taxes (CBDT) issued notification no. 68/2026 dated 30.05.2026 to provide deduction u/s 45(3)(a)(i) of the Income-tax Act, 2025 and rules 32 and 34 of the Income-tax Rules, 2026 to the S. Nijalingappa Sugar Institute, Belgaum (PAN: AAATK6236C) for Scientific Research under the category of University, college or other institution.

|

This notification shall be applicable to the S. Nijalingappa Sugar Institute, Belgaum for the tax years 2026-2027 to 2030-2031, subject to the conditions that it shall––

|

(i) comply with the conditions specified in rule 34 of the Income-tax Rules, 2026;

|

(ii) prepare statement under section 45(4)(a) of the Income-tax Act, 2025 for each tax year in Form No.15 and deliver or cause to be delivered to the Director General of Income-tax (Systems) or the person authorised by him on or before the 31st May, immediately following the tax year in which the donation is received, in accordance with rule 31 of the Income-tax Rules, 2026:

|

(iii) furnish to the donor, a certificate in Form No.16 specifying the amount of donation in accordance with rule 31 of the Income-tax Rules, 2026.

|

|

|

|

|

|

|

|

Central Board of Direct Taxes (CBDT) issued notification no. 67/2026 dated 30.05.2026 to provide deduction u/s 45(3)(a)(i) of the Income-tax Act, 2025 and rules 32 and 34 of the Income-tax Rules, 2026 to the Regional Centre for Biotechnology, Faridabad, Haryana (PAN: AAAAR9016J) for Scientific Research under the category of University, college or other institution.

|

This notification shall be applicable to the Regional Centre for Biotechnology, Faridabad, Haryana for the tax years 2026-2027 to 2030-2031, subject to the conditions that it shall––

|

(i) comply with the conditions specified in rule 34 of the Income-tax Rules, 2026;

|

(ii) prepare statement under section 45(4)(a) of the Income-tax Act, 2025 for each tax year in Form No.15 and deliver or cause to be delivered to the Director General of Income-tax (Systems) or the person authorised by him on or before the 31st May, immediately following the tax year in which the donation is received, in accordance with rule 31 of the Income-tax Rules, 2026:

|

(iii) furnish to the donor, a certificate in Form No.16 specifying the amount of donation in accordance with rule 31 of the Income-tax Rules, 2026.

|

|

|

|

|

|

|

|

Central Board of Direct Taxes (CBDT) issued notification no. 66/2026 dated 30.05.2026 to provide deduction u/s 45(3)(a)(i) of the Income-tax Act, 2025 and rules 32 and 34 of the Income-tax Rules, 2026 to the 'Ramakrishna Mission Vidyamandira' under the aegis of Ramakrishna Mission, Belur Math, Howrah (PAN: AAAAR1077P) for Scientific Research under the category of University, college or other institution.

|

This notification shall be applicable to the 'Ramakrishna Mission Vidyamandira' under the aegis of Ramakrishna Mission, Belur Math, Howrah for the tax years 2026-2027 to 2030-2031, subject to the conditions that it shall-

|

(i) comply with the conditions specified in rule 34 of the Income-tax Rules, 2026;

|

(ii) prepare statement under section 45(4)(a) of the Income-tax Act, 2025 for each tax year in Form No.15 and deliver or cause to be delivered to the Director General of Income-tax (Systems) or the person authorised by him on or before the 31st May, immediately following the tax year in which the donation is received, in accordance with rule 31 of the Income-tax Rules, 2026:

|

(iii) furnish to the donor, a certificate in Form No.16 specifying the amount of donation in accordance with rule 31 of the Income-tax Rules, 2026.

|

|

|

|

|

|

|

|

Central Board of Direct Taxes issued Notification No. 06/2026 dated 12.05.2026 - Order under clause (iia) of sub-section (1) of section 35 of the Income tax Act, 1961, read with Rule 5F of the Income tax Rules, 1962.

|

In exercise of the powers conferred by clause (iia) of sub-section (1) of section 35 of the Income Tax Act, 1961, read with Rule 5F of the Income Tax Rules 1962, the Pr. Chief Commissioner of Income Tax (Exemptions), Delhi hereby accords approval to the company M/s Shree Hari Arogyam Foundation, (PAN: ABGCS1785A), having registered office at Sector 3, Gandhinagar Sector 23, S.O. Gandhinagar, Gujarat, India - 382024 for 'Scientific Research' for the purpose of the said clause.

|

This Notification shall be applicable for five Assessment years from AY 2026-27 to AY 2030-31.

|

|

|

|

|

|

|

|

Directorate of Income -tax (Systems) issued Order vide reference F. No. ADG(S)-1/PAN/M/3699/2026-AD-DD SYSTEMS 1-5 DELHI dated 01st April, 2026.

|

Subject: - Order for specifying Forms and procedures in relation to furnishing Application for PAN Correction under Ruic 158(12) oflncomc -tax Rules, 2026 read with Section 262( 4) of Income-tax Act, 2025

|

ln exercise of the powers conferred by Rule 158( I 2) of the Income-tax Rules, 2026, the Director General of Income-tax (Systems), specifies the following Application Forms in respect of correction of PAN alongwith related procedure and guidelines, as under:-

|

a) PAN holders are required to fill the following Forms for Changes or Correction in PAN D

|

i. PAN CR-0 I: Request For Changes or Correction in PAN Data

|

ii. PAN CR-02: Request For Changes or Correction in PAN Data

|

b) The PDF format of the Forms for Changes or Correction in PAN Data, along with the related guidelines, is attached at Annexure-1.

c) The Forms can be submitted physically in the PAN Centres of Mis UTUTSL/ Mis Protean eGov or on line through their websites

|

2. This order shall apply with effect from 0 1.04.2026.

|

Manu Malik, Director General of Income-tax (Systems) ,Delhi

|

|

|

|

|

|

|

|

Central Board of Direct Taxes (CBDT) issued notification no. 64/2026 dated 10.04.2026 ..

|

|

|

|

|

|

|

|

CBIC -

To commemorate nine years of the Goods and Services Tax (GST), the Central Board of Indirect Taxes and Customs (CBIC) organized a special celebration at CSOI, New Delhi, on 1 July 2026. The event was held under the theme, ‘सुगम कर व्यवस्था, सशक्त भारत’, highlighting GST's

|

GST Indore -

The 9th #GSTDay was celebrated with great enthusiasm at CGST & Central Excise Commissionerate, Indore under the theme "सुगम कर व्यवस्था, सशक्त भारत".

|

GST Samvad an interaction among officers, taxpayers, trade & industry representatives, and tax professionals was organised on 30.06.2026 to commemorate nine years of GST as a transformative reform. The programme highlighted taxpayer facilitation initiatives, digital services, policy updates, and the importance of timely and voluntary compliance.

|

9 Years of GST! The CGST Indore Commissionerate celebrated the 9th anniversary of the Goods and Services Tax. The event marked nearly a decade of economic transformation and a unified national market.

|

Recognizing Excellence: The Department felicitated leading revenue contributors-Bharat Petroleum( @BPCLimited), HDFC Limited(@HDFCLTD), and MRF Limited(@MRF_Corporate)-for their exemplary tax compliance.10 dedicated departmental officers and a meritorious student were also honored

|

Taxpayer First: CGST Indore Commissioner Shri Peeyoush Bhati highlighted GST’s role in nation-building and announced that the Commissionerate will now regularly host monthly meetings with taxpayers to address grievances and ensure a transparent, efficient regime.

|

GST Aurangabad Commissionerate -

CGST AURANGABAD building lit up to kick in early 9th GST day celebrations

|

CGST Mumbai West -

As part of the #GSTPakhwada on occasion of upcoming 9th GST Day, on this year’s theme "सुगम कर व्यवस्था, सशक्त भारत” (Easy Tax System, Empowered India), CGST Mumbai West Commissionerate organised an Essay Writing Competition for officers and staff.

|

The winners and participants were felicitated by the Hon’ble Commissioner, CGST&C.Ex. Mumbai West appreciating their enthusiasm and insightful contributions.

|

WIRC of The Institute of Cost Accountants of India

Celebrating one of India’s landmark tax reforms that strengthened transparency, unity and the vision of One Nation, One Tax, One Market.

|

DGTPS MUMBAI CBIC

9वें GST दिवस के उपलक्ष्य में DGTS MZU & AZU द्वारा "Nine Years of GST: Perspective from Taxpayers" विषय पर Kendriya Vidyalayas के विद्यार्थियों हेतु एक वेबिनार आयोजित किया गया।

|

इस सत्र के माध्यम से GST के प्रति जागरूकता, वित्तीय साक्षरता को बढ़ावा दिया गया तथा विद्यार्थियों को राष्ट्र निर्माण में कराधान की भूमिका से अवगत कराया गया।

|

CGST Thane -

CGST Thane organized a 'Hindi & Marathi Essay Competition' for officers & staff

|

The Commissioner honored winners with certificates for outstanding performance

|

Celebrating language, awareness & commitment to GST

|

CGST MUMBAI EAST

As part of the 9th GST Day celebrations, CGST & Central Excise, Mumbai East Commissionerate organised Essay Writing and Drawing Competitions for students of Sandesh Vidyalaya & Junior College, Vikhroli (East), on 30.06.2026, with enthusiastic participation from young students.

|

The essay competition focused on GST and citizens’ responsibility towards tax compliance, while the drawing competition encouraged students to express ideas creatively. Prizes were awarded to winners, promoting taxation awareness and responsible citizenship among young minds.

|

As part of the 9th Anniversary celebrations of GST, CGST & Central Excise, Mumbai East Commissionerate organised GST "SAMVAD" and interactive session with members of trade and tax professionals on 29 June 2026 at Vikhroli to mark the occasion with active participation.

|

The session witnessed enthusiastic participation. Queries on filing of appeals, GST returns and other GST-related issues were addressed by officers, making it a valuable platform for knowledge sharing, constructive dialogue and promoting voluntary tax compliance across sectors.

|

CGST & Customs Thiruvananthapuram Zone

On the occasion of International Day Against Drug Abuse & Illicit Trafficking, the officers and staff of CGST & Customs Thiruvananthapuram Zone took a solemn pledge under the #NashaMuktBharatAbhiyan to build a society free from the menace of drugs.

|

DGTS AHMEDABAD CBIC

30.06.2026 को,DGTS AZU और MZU ने JG University के साथ मिलकर GST Awareness & Overview पर एक हाइब्रिड सेमिनार आयोजित किया।DGTS के Pr. ADG,श्री सुमित कुमार ने उद्घाटन भाषण दिया। CBIC के रिटायर्ड सुपरिटेंडेंट श्री जॉन क्रिश्चियन मुख्य वक्ता थे। #DGTS #GST #GSTDAY2026 #CBIC

|

Article Writing Competition 2026

To commemorate 9th Year of GST, Online Tax Update (OTU) launched 'Article Writing Competition 2026'. Registration starts today 1st July 2026 and ends on 15th July 2026. Article submission till 31st July 2026 and Winner Announcement in August, 2026. Cash Award + Certificate of Participation. Participation fees Rs. 300/- Read more

|

|

|

|

|

|

|

|

Centre has extended the last date for filing appeals before the Goods and Services Tax Appellate Tribunal (GSTAT) to July 31, 2026, giving taxpayers an additional month to submit their cases after a surge in filings led to technical difficulties on the GSTAT portal.

|

The extension applies to appeals filed under Section 112(1) read with Section 112(3) of the Goods and Services Tax (GST) law.

|

The revised deadline replaces the earlier cut-off of June 30, 2026, which had been notified by the government on September 17, 2025.

|

The decision follows recent representations from various stakeholders who flagged technical issues arising from a rush of appeals being filed on the GSTAT portal ahead of the deadline.

|

While noting that the original due date had been notified well in advance in September 2025, the government said filing activity had intensified sharply in recent weeks. It said 30,000 appeals were filed in the last 15 days alone, with daily filings touching a peak of 5,500 appeals.

|

Advising against eleventh-hour filings, the government urged taxpayers to complete their appeal submissions well in advance to ease pressure on the GSTAT portal.

|

The GST Appellate Tribunal serves as the first judicial appellate forum for taxpayers seeking to challenge orders issued by GST authorities after the disposal of their first appeals.

|

Source: The Economic Times

|

|

|

|

|

|

|

|

|

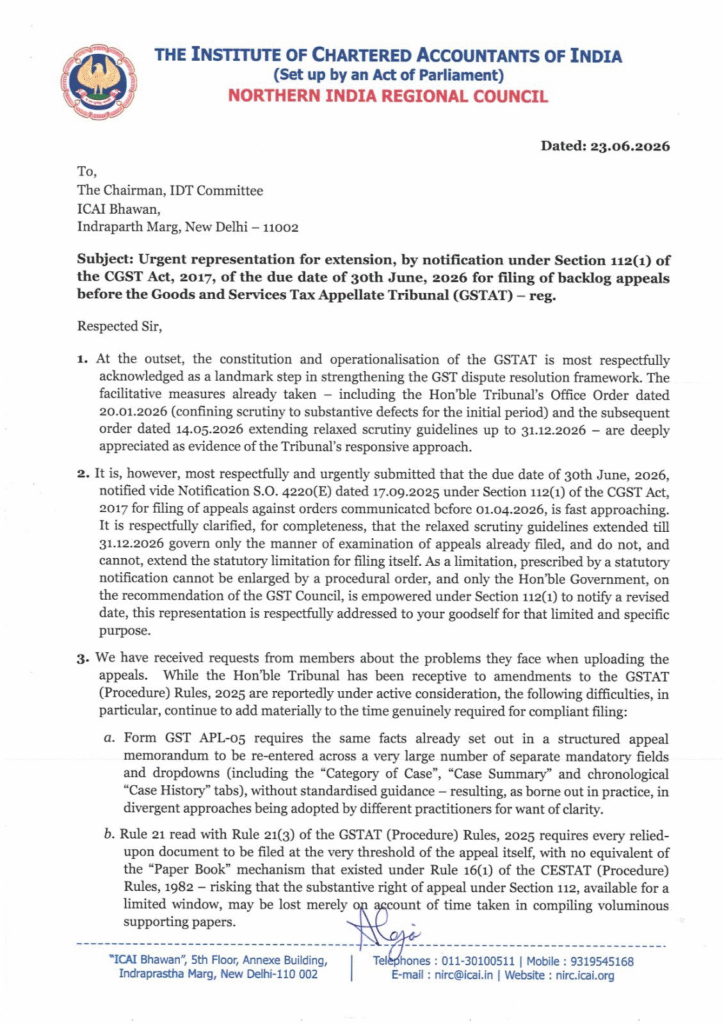

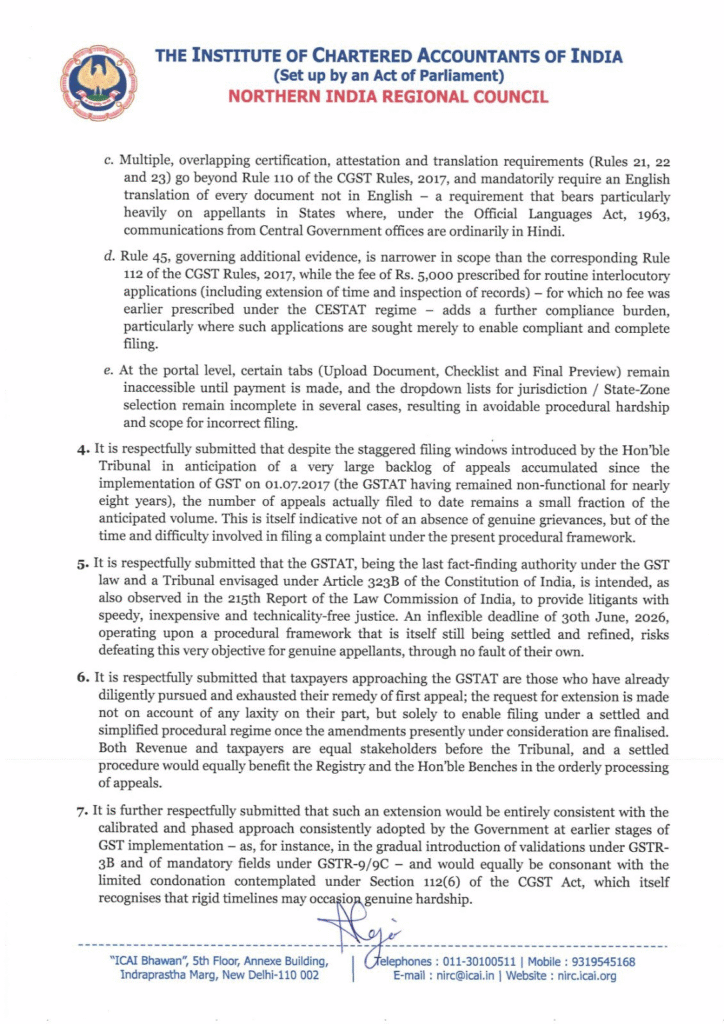

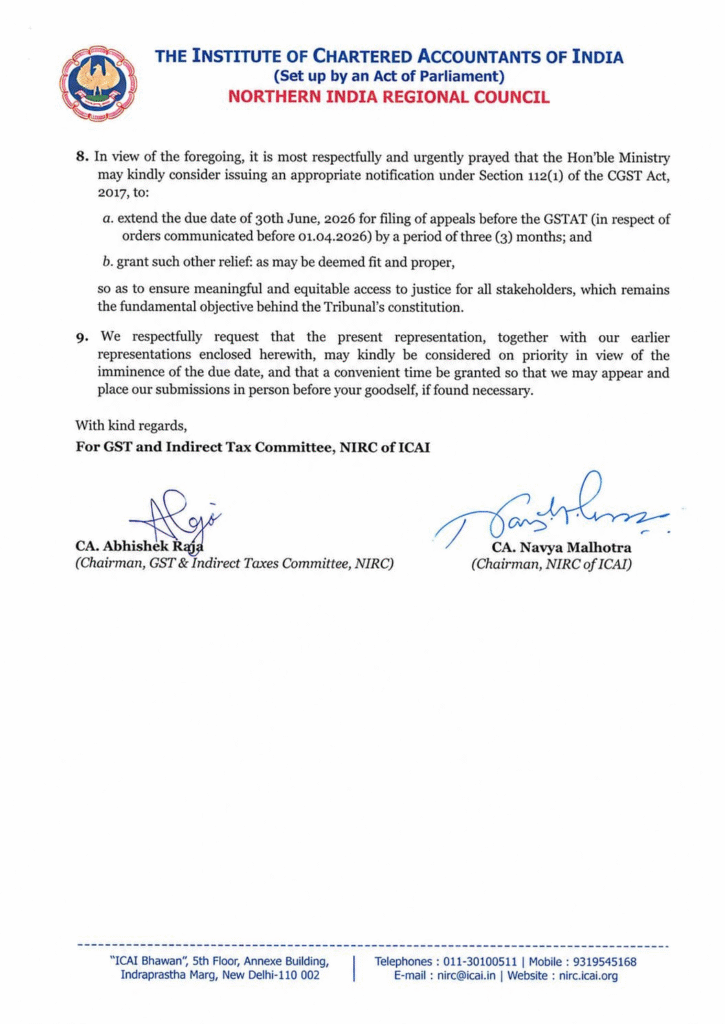

GST & IDT Committee has requested the Chairman, IDT Committee, ICAI, New Delhi to urgently represent before the respective forums for the date extension of GSTAT, i.e., 30-Jun-2026.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

The Hon’ble Delhi High Court in M/s. Spinns International v. Pr. Commissioner of Goods and Service Tax, has set aside the Show Cause Notice (“SCN”) and the consequential order for cancellation of GST Registration of the assessee, on the grounds that the SCN was bereft of any reasons and was issued in a mechanical manner without any application of mind. Held that, the purpose of a SCN is to enable the noticee to meet the allegations, on the basis of which an adverse action is proposed. Further, the procedure adopted by the Revenue Department is flawed and the order for cancellation of GST Registration of the assessee was passed in violation of principles of natural justice.

|

M/s. Spinns International (“the Petitioner”) had applied for the amendment of certain particulars in the GST Registration, which were accepted by the Revenue Department (“the Respondent”) dated May 27, 2022. A SCN dated September 29, 2022 (“the Impugned SCN”) was issued by the Respondent proposing to cancel the Petitioner’s Registration and called upon the Petitioner to appear before it.

|

The Petitioner stated that the Impugned SCN did not specify any reasons and was incapable of being responded to. Consequently, the Petitioner’s GST Registration was cancelled vide the order dated October 11, 2022 (“the Impugned Order”) on the grounds that the Petitioner had neither appeared for a personal hearing nor submitted any reply.

|

The Petitioner, then filed an application seeking the revocation of the Impugned Order, which is pending, but the Respondent stated that a NOC from Anti-Evasion Head-Quarter must be obtained in order to proceed with the revocation application.

|

Being aggrieved this Petition has been filed.

|

Whether the Impugned SCN and the Impugned Order passed for cancellation of GST Registration without specifying the reasons is maintainable?

|

The Hon’ble Delhi High Court in W.P.(C) 1989/2023 held as under:

|

- Noted that, it is settled law that the purpose of a SCN is to enable the noticee to meet the allegations on the basis of which an adverse action is proposed.

- Observed that, the Impugned SCN did not specify any allegation, which was capable of being responded to and was issued in a mechanical manner without any application of mind.

- Opined that, the Impugned SCN cannot be considered as a SCN at all.

- Noted that, there is no statutory provision that requires a taxpayer to seek a NOC from any authority for moving an application for revocation of cancellation of its GST Registration.

- Stated that, the procedure adopted by the Respondent for cancellation of the GST Registration is flawed.

- Held that, the Impugned Order has been passed in violation of principles of natural justice.

- Set aside the Impugned SCN and the Impugned Order.

- Permitted the Respondent to initiate any fresh action in accordance with law.

Section 29 of the Central Goods and Services Tax Act, 2017 (“the CGST Act”):

|

“Cancellation or suspension of registration.

|

29. (1) The proper officer may, either on his own motion or on an application filed by the registered person or by his legal heirs, in case of death of such person, cancel the registration, in such manner and within such period as may be prescribed, having regard to the circumstances where,––

|

(a) the business has been discontinued, transferred fully for any reason including death of the proprietor, amalgamated with other legal entity, demerged or otherwise disposed of; or

|

(b) there is any change in the constitution of the business; or

|

(c) the taxable person is no longer liable to be registered under section 22 or section 24 or intends to optout of the registration voluntarily made under sub-section (3) of section 25:

|

Provided that during pendency of the proceedings relating to cancellation of registration filed by the registered person, the registration may be suspended for such period and in such manner as may be prescribed.

|

(2) The proper officer may cancel the registration of a person from such date, including any retrospective date, as he may deem fit, where,––

|

(a) a registered person has contravened such provisions of the Act or the rules made thereunder as may be prescribed; or

|

(b) a person paying tax under section 10 has not furnished the return for a financial year beyond three months from the due date of furnishing the said return; or

|

(c) any registered person, other than a person specified in clause (b), has not furnished returns for such continuous tax period as may be prescribed; or

|

(d) any person who has taken voluntary registration under sub-section (3) of section 25 has not commenced business within six months from the date of registration; or

|

(e) registration has been obtained by means of fraud, wilful misstatement or suppression of facts:

|

Provided that the proper officer shall not cancel the registration without giving the person an opportunity of being heard.

|

Provided further that during pendency of the proceedings relating to cancellation of registration, the proper officer may suspend the registration for such period and in such manner as may be prescribed.

|

(3) The cancellation of registration under this section shall not affect the liability of the person to pay tax and other dues under this Act or to discharge any obligation under this Act or the rules made thereunder for any period prior to the date of cancellation whether or not such tax and other dues are determined before or after the date of cancellation.

|

(4) The cancellation of registration under the State Goods and Services Tax Act or the Union Territory Goods and Services Tax Act, as the case may be, shall be deemed to be a cancellation of registration under this Act.

|

(5) Every registered person whose registration is cancelled shall pay an amount, by way of debit in the electronic credit ledger or electronic cash ledger, equivalent to the credit of input tax in respect of inputs held in stock and inputs contained in semi-finished or finished goods held in stock or capital goods or plant and machinery on the day immediately preceding the date of such cancellation or the output tax payable on such goods, whichever is higher, calculated in such manner as may be prescribed:

|

Provided that in case of capital goods or plant and machinery, the taxable person shall pay an amount equal to the input tax credit taken on the said capital goods or plant and machinery, reduced by such percentage points as may be prescribed or the tax on the transaction value of such capital goods or plant and machinery under section 15, whichever is higher.

|

(6) The amount payable under sub-section (5) shall be calculated in such manner as may be prescribed.”

|

DISCLAIMER: The views expressed are strictly of the author and A2Z Taxcorp LLP. The contents of this article are solely for informational purpose and for the reader’s personal non-commercial use. It does not constitute professional advice or recommendation of firm. Neither the author nor firm and its affiliates accepts any liabilities for any loss or damage of any kind arising out of any information in this article nor for any actions taken in reliance thereon. Further, no portion of our article or newsletter should be used for any purpose(s) unless authorized in writing and we reserve a legal right for any infringement on usage of our article or newsletter without prior permission.

|

|

|

|

|

|

|

|

The Hon’ble Madras Court in M/s. Engineering Aids v. State Tax Officer and Ors. has quashed the demand order passed by the Revenue Department, on the grounds that the reply filed by the assessee to the Show Cause Notice (“SCN”) was not considered even though the same was received by the Revenue Department. Remanded the matter back for fresh consideration on merits and in accordance with the law. Further, directed the Revenue Department to pass final orders, after adhering to the principles of natural justice and providing the opportunity of hearing to assessee.

|

This petition has been filed by M/s. Engineering Aids (“the Petitioner”) challenging the summary order in Form GST DRC-07 dated April 5, 2022 (“the Impugned Order”) passed by the Revenue Department (“the Respondent”) under Section 74 of the Central Goods and Services Tax Act, 2017 (“the CGST Act”) for demand and recovery of tax, on the grounds of violation of principles of natural justice, contending that only the Impugned Order was served and not the detailed order nor has it been uploaded on the GST portal. Further, the reply in Form GST DRC-06 dated February 25, 2022 (“the Reply”) to the SCN issued in Form GST DRC-01 dated February 17, 2022 (“the SCN”) was not considered by the Respondent while passing the Impugned Order.

|

Whether the Impugned Order can be passed without considering the Reply to the SCN?

|

The Hon’ble Madras High Court in W.P. No.28124 of 2022 held as under:

|

- Noted that, the Petitioner has also filed Form GST DRC-06, dated February 25, 2022 which confirms that the Reply sent by the Petitioner was received by the Respondent.

- Observed that, there was no reference of the Reply in the Impugned Order and the Reply was not considered by the Respondent while passing the Impugned Order.

- Held that, the respondents have not considered the Reply even though the same was received by them hence the Impugned Order has to be quashed.

- Quashed the Impugned Order.

- Remanded the matter back to the Respondent for fresh consideration on merits and in accordance with the law.

- Directed the Respondent to pass final orders within 12 weeks, after adhering to the principles of natural justice and providing the opportunity of hearing to the Petitioner.

DISCLAIMER: The views expressed are strictly of the author and A2Z Taxcorp LLP. The contents of this article are solely for informational purpose and for the reader’s personal non-commercial use. It does not constitute professional advice or recommendation of firm. Neither the author nor firm and its affiliates accepts any liabilities for any loss or damage of any kind arising out of any information in this article nor for any actions taken in reliance thereon. Further, no portion of our article or newsletter should be used for any purpose(s) unless authorized in writing and we reserve a legal right for any infringement on usage of our article or newsletter without prior permission.

|

|

|

|

|

|

|

|

The AAR, West Bengal in the matter of Shopinshop Franchise Pvt. Ltd. has ruled that ‘Bouquets’ made with dry parts of plants, foliage, flower buds, grasses, and branches of plants which dried, bleached, dyed, and coloured and sold with plastic foil packaging will be classifiable under Tariff Item No. 06039000 or 06049900 of the Customs Tariff Act, 1975 (“the Customs Tariff Act”), and would be exempted from GST as per the SI No. 34 of the Notification No. 02/2017-Central Tax (Rate) dated June 28, 2017 (“the Goods Exemption Notification”).

|

Shopinshop Franchise Pvt. Ltd. (“the Applicant”) is a company engaged in manufacturing and processing of dry parts of plants, foliage, flower buds, grasses and branches of plant which are dried, bleached, dyed and coloured for decorative and ornamental purposes and sold as ‘Bouquets’ made with dried parts of plants and packed in plastic foil packaging (“the Impugned Product”).

|

The Applicant submitted that the Impugned Product will be classified under HSN Code 0604 as per Chapter 6 of the First Schedule of the Customs Tariff Act and is exempted from GST as per SI No. 34 of the Goods Exemption Notification.

|

The Applicant filed this application seeking the classification and applicable GST rates on the Impugned Product.

|

Whether the supply of the Impugned Product will be classified under HSN Code 0604 as per Chapter 6 of the First Schedule of the Customs Tariff Act and covered under the SI. No 34 of the Goods Exemption Notification?

|

The AAR, West Bengal in 27/WBAAR/2022-23 held as under:

|

- Observed that, the raw materials used in making the Impugned Product are plant products and they undergo some sort of processing before packing with a simple plastic foil packaging.

- Noted that, the Bouquet, made with “Dried and/or Dyed” flower buds will be classifiable as “Other” under Tariff Item No. 06039000 and Bouquet, made with “Dried and/or Dyed” parts of plants, foliage, grasses and branches of plant, will be classifiable as “Other” under Tariff Item No. 06049000.

- Further noted that, as per SI. No. 34 of the Goods Exemption Notification, the whole of Chapter 6 of the Customs Tariff Act which deals with “Live trees and other plants; bulbs, roots and the like; cut flowers and ornamental foliage” is exempted from GST.

- Held that, the Impugned Product will be classifiable under Tariff Item Nos. 06039000 or 06049900, whether individually or in combination, and supply of the Impugned Product is exempted from payment of tax vide SI. No. 34 of Goods Exemption Notification.

SI. No. 34 of the Goods Rate Notification:

|

DISCLAIMER: The views expressed are strictly of the author and A2Z Taxcorp LLP. The contents of this article are solely for informational purpose and for the reader’s personal non-commercial use. It does not constitute professional advice or recommendation of firm. Neither the author nor firm and its affiliates accepts any liabilities for any loss or damage of any kind arising out of any information in this article nor for any actions taken in reliance thereon. Further, no portion of our article or newsletter should be used for any purpose(s) unless authorized in writing and we reserve a legal right for any infringement on usage of our article or newsletter without prior permission.

|

|

|

|

|

|

|

|

The Hon’ble Allahabad High Court in M/s. Radha Fragnance v. Union of India and Others affirmed the order of detention of goods and imposition of tax and penalty, on the grounds that the assessee was transporting huge quantity of goods without e-way bill by reducing the value of goods below the threshold limit. Held that, it is only to protect small trade where the value is minimal that the necessity of downloading e-way bill is dispensed, however, the same does not allow the assessee to undervalue goods so as to escape it from bringing to the notice of the Revenue Department by uploading the same on the Web-Portal.

|

M/s. Radha Fragnance(“the Petitioner”) is in the business of manufacturing and sale of Pan Masala and Chewing Tobacco (“the Goods”), who had received orders for supply of the Goods from two registered dealers namely M/s ASP Enterprises and M/s Alliance Trading Company and was sending the goods through four tax invoices.

|

The goods in transit from State of Haryana to Jharkhand were intercepted on February 4, 2019 by Revenue Department (“the Respondent”) wherein, the tax invoices were produced by the driver of the vehicle for the Goods and during verification it was found that goods were not accompanied with E-way Bill as per Rule 138 of the Central Goods and Services Tax Rules, 2017 (“the CGST Rules”), as the value of goods were claimed to be below INR 50,000/. The Respondent, on inspection, found that the total value of the Goods came to INR 15,36,000/- and after allowing discount of 25% and excluding tax and Cess, the basic value came to INR 6,12,766/- while the value on both the invoices was declared collectively INR 69,600/-.

|

Subsequently, a Show Cause Notice in Form MOV-07 was issued on February 6, 2019 (“the Impugned SCN”), for which a reply was filed on February 13, 2019 mentioning that, tax invoices in respect of tobacco were misplaced by the driver and could not be produced at the time of interception of goods. However, an Order-in-Original dated February 14, 2019 (“the OIO”) under Section 129 of the Central Goods and Services Tax Act, 2017 (“the CGST Act”) read with Section 20 of the Integrated Goods and Services Tax Act, 2017 (“the IGST Act”) was passed, rejecting the explanation submitted by the Petitioner and directed the Petitioner to deposit Integrated Goods and Services Tax (“IGST”) to the extent of Rs.7,27,235/- and penalty of the same amount. Consequently, the Petitioner filed an appeal wherein, the OIO was confirmed vide Order-in-Appeal dated March 2, 2019 (“the OIA”).

|

Being aggrieved, this petition has been filed.

|

Whether in the garb of certain protection given under Rule 138 dispensing requirement of E-Way bill for goods valuing below Rs.50,000/-, a dealer who is a manufacturer, can be allowed to send his goods to different consignees undervaluing the goods and the Tax Authorities not to proceed taking action under the Act?

|

The Hon’ble Allahabad High Court in Writ Tax No. 427 of 2019 held as under:

|

- Observed that, the Respondent, on fair valuation, found that the Goods, which were in transit accounted for INR 7,12,766/- while the proper disclosure was not made by the Petitioner and it was on this undervaluation of goods that the Respondent proceeded and imposed IGST and penalty.

- Stated that, the very purpose of downloading e-way bill is that every goods, which are in transit, is recorded in the Web Portal and the Respondent has a clear picture of the goods which are manufactured and sold by the dealers either Inter-State or Intra-State.

- Further stated that, it is only to protect small trade where the value is minimal that the necessity of downloading e-way bill is dispensed, however, the same does not allow the Petitioner to undervalue goods, so as to escape it from bringing to the notice of the Respondent by uploading the same on the Web-Portal.

- Noted that, the Petitioner had started its business in 2018, and had carried 11 transactions and none of the transactions were ever reported on the Web Portal and no E-Way bill was downloaded. Meaning thereby that all the transactions made by the Petitioner was below INR 50,000/-.

- Opined that, if the Petitioner is permitted, it will harm the business world and lead to a parallel economy and the very purpose of enactment of GST would be frustrated.

- Further noted that, one of the consignee of the Petitioner was actually registered as ‘Works Contract and Suppliers of Services’ and not in the business of trading. In the garb of technicalities, no benefit can be given to a dealer who has intentionally undervalued its goods to escape from the eyes of law.

- Held that, the Petitioner had grossly undervalued the Goods to avoid downloading e-way bill and bringing the transaction on record so as to escape payment of due tax.

- Further held that, the actions of the Respondent in detaining the Goods and imposing tax and penalty, needed no interference as the Petitioner cannot be permitted to take shelter of the fact that no e-way bill is required in case of goods valued less than INR 50,000/-.

Section 129 of the CGST Act:

|

“Detention, seizure and release of goods and conveyances in transit-

|

(1) Notwithstanding anything contained in this Act, where any person transports any goods or stores any goods while they are in transit in contravention of the provisions of this Act or the rules made thereunder, all such goods and conveyance used as a means of transport for carrying the said goods and documents relating to such goods and conveyance shall be liable to detention or seizure and after detention or seizure, shall be released,––

|

(a) on payment of penalty equal to two hundred per cent. of the tax payable on such goods and, in case of exempted goods, on payment of an amount equal to two per cent. of the value of goods or twenty-five thousand rupees, whichever is less, where the owner of the goods comes forward for payment of such penalty;

|

(b) on payment of penalty equal to fifty per cent. of the value of the goods or two hundred per cent. of the tax payable on such goods, whichever is higher, and in case of exempted goods, on payment of an amount equal to five per cent. of the value of goods or twenty-five thousand rupees, whichever is less, where the owner of the goods does not come forward for payment of such penalty;

|

(c) upon furnishing a security equivalent to the amount payable under clause (a) or clause (b) in such form and manner as may be prescribed:

|

Provided that no such goods or conveyance shall be detained or seized without serving an order of detention or seizure on the person transporting the goods.

|

(3) The proper officer detaining or seizing goods or conveyance shall issue a notice within seven days of such detention or seizure, specifying the penalty payable, and thereafter, pass an order within a period of seven days from the date of service of such notice, for payment of penalty under clause (a) or clause (b) of sub-section (1).

|

(4) No penalty shall be determined under sub-section (3) without giving the person concerned an opportunity of being heard.

|

(5) On payment of amount referred in sub-section (1), all proceedings in respect of the notice specified in sub-section (3) shall be deemed to be concluded.

|

(6) Where the person transporting any goods or the owner of such goods fails to pay the amount of penalty under sub-section (1) within fifteen days from the date of receipt of the copy of the order passed under sub-section (3), the goods or conveyance so detained or seized shall be liable to be sold or disposed of otherwise, in such manner and within such time as may be prescribed, to recover the penalty payable under sub-section (3):

|

Provided that the conveyance shall be released on payment by the transporter of penalty under sub-section (3) or one lakh rupees, whichever is less:

|

Provided further that where the detained or seized goods are perishable or hazardous in nature or are likely to depreciate in value with passage of time, the said period of fifteen days may be reduced by the proper officer.”

|

Rule 138(1) of the CGST Rules:

|

“138. Information to be furnished prior to commencement of movement of goods and generation of e-way bill.-

|

(1) Every registered person who causes movement of goods of consignment value exceeding fifty thousand rupees-

|

(i) in relation to a supply; or

|

(ii) for reasons other than supply; or

|

(iii) due to inward supply from an unregistered person,

|

shall, before commencement of such movement, furnish information relating to the said goods as specified in Part A of FORM GST EWB-01, electronically, on the common portal along with such other information as may be required on the common portal and a unique number will be generated on the said portal:

|

Provided that the transporter, on an authorization received from the registered person, may furnish information in Part A of FORM GST EWB-01, electronically, on the common portal along with such other information as may be required on the common portal and a unique number will be generated on the said portal:

|

Provided further that where the goods to be transported are supplied through an ecommerce operator or a courier agency, on an authorization received from the consignor, the information in Part A of FORM GST EWB-01 may be furnished by such e-commerce operator or courier agency and a unique number will be generated on the said portal:

|

Provided also that where goods are sent by a principal located in one State or Union territory to a job worker located in any other State or Union territory, the e-way bill shall be generated either by the principal or the job worker, if registered, irrespective of the value of the consignment:

|

Provided also that where handicraft goods are transported from one State or Union territory to another State or Union territory by a person who has been exempted from the requirement of obtaining registration under clauses (i) and (ii) of section 24, the e-way bill shall be generated by the said person irrespective of the value of the consignment.

|

Explanation 1. – For the purposes of this rule, the expression “handicraft goods” has the meaning as assigned to it in the Government of India, Ministry of Finance, notification No. 56/2018-Central Tax, dated the 23rd October, 2018, published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i), vide number G.S.R 1056 (E), dated the 23rd October, 2018 as amended from time to time.

|

Explanation 2.- For the purposes of this rule, the consignment value of goods shall be the value, determined in accordance with the provisions of section 15, declared in an invoice, a bill of supply or a delivery challan, as the case may be, issued in respect of the said consignment and also includes the central tax, State or Union territory tax, integrated tax and cess charged, if any, in the document and shall exclude the value of exempt supply of goods where the invoice is issued in respect of both exempt and taxable supply of goods.”

|

DISCLAIMER: The views expressed are strictly of the author and A2Z Taxcorp LLP. The contents of this article are solely for informational purpose and for the reader’s personal non-commercial use. It does not constitute professional advice or recommendation of firm. Neither the author nor firm and its affiliates accepts any liabilities for any loss or damage of any kind arising out of any information in this article nor for any actions taken in reliance thereon. Further, no portion of our article or newsletter should be used for any purpose(s) unless authorized in writing and we reserve a legal right for any infringement on usage of our article or newsletter without prior permission.

|

|

|

|

|

|

|

|

The Hon’ble Orissa High Court in M/s. Y. B. Constructions Pvt. Ltd. v. Union of India and others has permitted the assessee to rectify the error of mentioning B2C instead of B2B in Form GSTR-1 at the time of filing of returns, holding that the assessee would be prejudiced if it is not allowed to avail the benefits of Input Tax Credit (“ITC”). Directed the Respondent to receive the corrected Form GSTR-1 manually and upload the details on the web portal within 4 weeks.

|

M/s. Y. B. Constructions Pvt. Ltd. (“the Petitioner”) had committed a mistake while filing the GST Return under Form GSTR-1 for the period 2017-18 dated October 16, 2017 and November 25, 2017 and for the period 2018-19 dated January 30, 2018 and March 30, 2019, wherein, B2C instead of B2B was mentioned. The Petitioner sought to correct the error in order to receive the ITC benefit from the principal contractor. The last date for rectifying the return was April 13, 2019. The Revenue Department (“the Respondent”) stated that once the deadline for rectification of the Forms was crossed, then no further indulgence would be granted to the Petitioner.

|

Being aggrieved, this Petition has been filed.

|

The Petitioner contended that the error came to be noticed when the principal contractor held up the legitimate running bill amount of the Petitioner by informing it about the above error and thereafter it has been making requests to the Respondent to permit it to make the corrections.

|

Whether the Petitioner be allowed to rectify the error committed in Form GSTR-1?

|

The Hon’ble Orrisa High Court in W.P.(C) No.12232 of 2021 held as under:

|

- Noted that, allowing the Petitioner to rectify the mistake in its GST Returns will not cause any loss to the Respondent, as there will be no escapement of tax, however, denying the request will prejudice the Petitioner, who is entitled to receive the ITC benefit.

- Relied on the judgment of the Hon’ble Madras High Court in the matter of M/s. Sun Dye Chem v. The Assistant Commissioner ST , wherein, the plea of the assessee was accepted and it was permitted to file the corrected Form.

- Permitted the Petitioner to resubmit the corrected Form GSTR-1.

- Directed the Respondent to receive the corrected Form GSTR-1 manually and facilitate the uploading of the details on the web portal within 4 weeks.

The above judgment brings up a significant issue concerning whether the assessee would be allowed to rectify the error while filing its Form GSTR-1.

|

In this regard, recently, in a similar matter, the Hon’ble Orissa High Court in M/s. Shiva Jyoti Construction v. The Chairperson, Central Board of Excise &Customs and others had permitted the assessee to rectify its Form GSTR-1 filed for the months of September 2017 and March 2018, in order to claim ITC benefit by the recipient, wherein B2C was erroneously mentioned, instead of B2B. It was held that, the assessee will be unnecessarily prejudiced if it is not allowed to avail the benefits of ITC.

|

To know more, kindly watch our video “Legal Jurisprudence: B2B Supply wrongly shown as B2C - Credit denied to Buyers” || CA (Adv) Bimal Jain - https://youtu.be/MuYeNW510E8

|

Further, the Hon’ble Karnataka High Court in M/s. Wipro Limited India v. the Assistant Commissioner of Central Taxes and Ors. had allowed the assessee to rectify the errors committed at the time of filing of Forms and submitting GST Returns for FY 2017-2020. It was held that, the error committed by the assessee in showing the wrong Goods and Services Tax Identification Number (“GSTIN”) in the invoices, which was carried forward in the relevant forms is a bonafide error, which has occurred due to bonafide reasons, unavoidable circumstances and sufficient cause. Hence, Circular No. 183/15/2022-GST dated December 27, 2022 (“the Circular”), which allows rectification of such bonafide and inadvertent mistakes, would be directly and squarely applicable.

|

To know more, kindly watch our video “Karnataka HC: Relevance of Circular on Difference of Credit in GSTR 2A vs. GSTR 3B” || CA (Adv) Bimal Jain - https://youtu.be/cl0Isfns-Oo

|

DISCLAIMER: The views expressed are strictly of the author and A2Z Taxcorp LLP. The contents of this article are solely for informational purpose and for the reader’s personal non-commercial use. It does not constitute professional advice or recommendation of firm. Neither the author nor firm and its affiliates accepts any liabilities for any loss or damage of any kind arising out of any information in this article nor for any actions taken in reliance thereon. Further, no portion of our article or newsletter should be used for any purpose(s) unless authorized in writing and we reserve a legal right for any infringement on usage of our article or newsletter without prior permission.

|

|

|

|

|

|

|

|

The Hon’ble Gujarat High Court in M/s. Devi Products v. State of Gujarat has set aside the Show Cause Notice (“SCN”) issued to the assessee and the consequential order for cancellation of GST Registration, on the grounds that they were passed without recording any reasons and without determining the tax demand and thus, are cryptic in nature. Held that, cancellation of GST Registration without any determination of the amount payable by the assessee is not valid and sustainable.

|

M/s Devi Products (“the Petitioner”) is a sole proprietor engaged in the business of trading of brass articles. The Petitioner had filed its return till June, 2020, however due to prevalent circumstances during Covid-19 pandemic the Petitioner had no business subsequent to June, 2020 and due to the financial hardship suffered, the Petitioner was of bonafide belief that there was no requirement to file GST returns.

|

Subsequently, a SCN dated March 15, 2021 (“the Impugned SCN”) was issued by the Revenue Department (“the Respondent”) under Rule 22(1) of the Central Goods and Services Tax Rules, 2017 (“the CGST Rules”) read with Section 29 of the Central Goods and Services Tax Act, 2017 (“the CGST Act”) whereby, the Petitioner was informed that its GST Registration was liable to be cancelled for not filing returns for a continuous period of six months. The GST Registration of the Petitioner was also suspended on March 15, 2021 under Rule 21A of the CGST Rules without recording any reasons. Thereafter, the GST Registration of the Petitioner was cancelled by the Respondent with effect from July 1, 2017 vide Order dated March 24, 2021 (“the Impugned Order”) without recording any particulars or the reasons or the grounds for cancellation and without determining the tax demand.

|

Being aggrieved, this petition has been filed.

|

Whether Impugned SCN and the Impugned Order without recording the grounds for cancellation of GST Registration and without determining the tax demand are sustainable?

|

The Hon’ble Gujarat High Court in R/Special Civil Application No. 2288 of 2023 held as under:

|

- Relied on the judgment of the Hon’ble Supreme Court in Krani Associates vs. Masood Ahmed wherein, it was held that recording of reasons is meant to serve the vital principle that justice must not only be done but it must also appear to be done and it would also operate as valid restraint on any possible arbitrary exercise of judicial and quasi-judicial or even administrative power. Further, it reassures that discretion has been exercised by the decision maker on relevant grounds and by disregarding extraneous considerations and facilitates the process of judicial review by the superior Court.

- Noted that, the Respondent ought to have at least incorporated the specific details of the contents of the Impugned SCN which any prudent person can respond to as otherwise it would fail to respond to such SCN which is bereft of details thereby making the mechanism of issuing SCN only a formality.

- Stated that, the very nature of the Impugned SCN and the Impugned Order was cryptic and unsustainable under law, as while cancelling the GST Registration, the Respondent had not even determined the amount payable pursuant to such cancellation.

- Held that, cancellation of GST Registration without any determination of the amount payable by the Petitioner is hardly sustainable and such action cannot be ratified in any manner.

- Quashed the Impugned SCN and the Impugned Order.

- Permitted the Respondent to issue fresh SCN with the particular reasons incorporating the details and directed to provide reasonable opportunity of hearing to the Petitioner.

Section 29 of the CGST Act:

|

“Cancellation or suspension of registration.

|

29. (1) The proper officer may, either on his own motion or on an application filed by the registered person or by his legal heirs, in case of death of such person, cancel the registration, in such manner and within such period as may be prescribed, having regard to the circumstances where,––

|

(a) the business has been discontinued, transferred fully for any reason including death of the proprietor, amalgamated with other legal entity, demerged or otherwise disposed of; or

|

(b) there is any change in the constitution of the business; or

|

(c) the taxable person is no longer liable to be registered under section 22 or section 24 or intends to optout of the registration voluntarily made under sub-section (3) of section 25:

|

Provided that during pendency of the proceedings relating to cancellation of registration filed by the registered person, the registration may be suspended for such period and in such manner as may be prescribed.

|

(2) The proper officer may cancel the registration of a person from such date, including any retrospective date, as he may deem fit, where,––

|

(a) a registered person has contravened such provisions of the Act or the rules made thereunder as may be prescribed; or

|

(b) a person paying tax under section 10 has not furnished 5; or

|

(c) any registered person, other than a person specified in clause (b), has not furnished returns for 6; or

|

(d) any person who has taken voluntary registration under sub-section (3) of section 25 has not commenced business within six months from the date of registration; or

|

(e) registration has been obtained by means of fraud, wilful misstatement or suppression of facts:

|

Provided that the proper officer shall not cancel the registration without giving the person an opportunity of being heard.

|

Provided further that during pendency of the proceedings relating to cancellation of registration, the proper officer may suspend the registration for such period and in such manner as may be prescribed.

|

(3) The cancellation of registration under this section shall not affect the liability of the person to pay tax and other dues under this Act or to discharge any obligation under this Act or the rules made thereunder for any period prior to the date of cancellation whether or not such tax and other dues are determined before or after the date of cancellation.

|

(4) The cancellation of registration under the State Goods and Services Tax Act or the Union Territory Goods and Services Tax Act, as the case may be, shall be deemed to be a cancellation of registration under this Act.

|

(5) Every registered person whose registration is cancelled shall pay an amount, by way of debit in the electronic credit ledger or electronic cash ledger, equivalent to the credit of input tax in respect of inputs held in stock and inputs contained in semi-finished or finished goods held in stock or capital goods or plant and machinery on the day immediately preceding the date of such cancellation or the output tax payable on such goods, whichever is higher, calculated in such manner as may be prescribed:

|

Provided that in case of capital goods or plant and machinery, the taxable person shall pay an amount equal to the input tax credit taken on the said capital goods or plant and machinery, reduced by such percentage points as may be prescribed or the tax on the transaction value of such capital goods or plant and machinery under section 15, whichever is higher.

|

(6) The amount payable under sub-section (5) shall be calculated in such manner as may be prescribed.”

|

DISCLAIMER: The views expressed are strictly of the author and A2Z Taxcorp LLP. The contents of this article are solely for informational purpose and for the reader’s personal non-commercial use. It does not constitute professional advice or recommendation of firm. Neither the author nor firm and its affiliates accepts any liabilities for any loss or damage of any kind arising out of any information in this article nor for any actions taken in reliance thereon. Further, no portion of our article or newsletter should be used for any purpose(s) unless authorized in writing and we reserve a legal right for any infringement on usage of our article or newsletter without prior permission.

|

|

|

|

|

|

|

|

The Hon’ble Bombay High Court in Survival Technologies Pvt. Ltd. v. the Deputy Commissioner of Income Tax has set aside the notice issued under Section 148 of the Income Tax Act (“the IT Act”) seeking to reopen the assessment of the assessee and the consequential order rejecting the objections of the assessee for reopening such assessment proceedings, on the grounds that the notice was issued without any tangible material with the Revenue Department. Held that, mere change of opinion does not provide jurisdiction to the Revenue Department to re-open assessment.

|

Survival Technologies Pvt. Ltd. (“the Petitioner”) filed its return of income for the Assessment Year (“A.Y.”) 2015-16 which was subsequently selected for scrutiny assessment and notices were issued under Section 143(2) of the IT Act on March 17, 2016 and under Section 142(1) of the IT Act on January 23, 2017 by the Revenue Department (“the Respondent”). The Petitioner furnished necessary information and details pursuant to such notices including its claim for deduction under Section 35(2AB) of the IT Act.

|

Subsequently, an order of assessment dated June 13, 2017 was passed under Section 143(3) of the IT Act, assessing the total income at INR 8,48,00,190/-, by disallowing INR 32,70,724/- being excess deduction claimed under Section 35(2AB) of the IT Act. However, the disallowance was reduced to INR 16,35,262/- as per rectification order dated June 23, 2017 passed under Section 154 of the IT Act.

|

Thereafter, a Notice dated March 30, 2021 (“the Impugned Notice”) was issued under Section 148 of the IT Act seeking to reopen assessment for the A.Y. 2015-16 on the ground that income chargeable to tax had escaped assessment. The Petitioner objected such proposed reopening of assessment but the objections were rejected vide Order dated February 21, 2022 (“the Impugned Order”).

|

Being aggrieved, this petition has been filed.

|

Whether the reassessment proceedings could be initiated on account of change of opinion, after the expiry of period of four years unless any income chargeable to tax has escaped assessment?

|

The Hon’ble Bombay High Court in Writ Petition No. 3035 of 2022 held as under:

|

- Analyzed Section 147 of the IT Act which empowers the Assessing Officer (“AO”) to assess or re-assess an income if it has reasons to believe that such income has escaped assessment, however, no action shall be taken after the expiry of period of four years from the end of the relevant assessment year unless any income chargeable to tax has escaped assessment.

- Observed that, since this is a case of reopening beyond the period of four years, the Respondent had to satisfy the jurisdictional conditions on both counts, i.e. ‘reason to believe’ and ‘failure to disclose fully and truly the material facts’. Further, it is a settled principle of law that the jurisdiction exercised under Section 147 of the IT Act by an AO has to be tested on the touchstone of the reasons recorded, which can neither be improved subsequently nor added in the reply or in the subsequent pleadings.

- Relied on the earlier judgment in Hindustan Lever Ltd. v. Rb. Wadkar, Assistant Commissioner of Income-Tax and Others wherein, the AO was obliged to disclose as to which fact or material was not disclosed by the assessee fully and truly, for the purposes of assessment of that A.Y., so as to establish a vital linkage between the reasons and the evidence while noting that, the jurisdictional condition has not been satisfied by the Respondent, except having made a bald statement that the material facts were not disclosed fully and truly.

- Opined that, the Respondent has failed to establish that there was any failure on the part of the Petitioner to disclose fully and truly any material fact.

- Further observed that, the Impugned Notice has been issued without there being any tangible material with the Respondent as he clearly relied upon the material which was already on record.

- Relied on the judgment of Hon’ble Delhi High Court in Jindal Photo Films Ltd. v. Deputy Commissioner of Income-Tax and Another wherein, it was held that, if materials for reason to believe is available, the writ court will not exercise its power of judicial review to go into the sufficiency or adequacy of the material available.

- Held that, mere ‘change of opinion’ does not provide jurisdiction to the Respondent to initiate proceedings under Section 147 of the IT Act.

- Set aside the Impugned Notice and Impugned Order.

The above judgment brings up a significant issue concerning whether the assessment proceedings could be initiated merely on the ground of change of opinion.

|

Recently, a similar view was taken up by the Hon’ble Bombay High Court in Court inthe matter of Punia Capital Pvt. Ltd. v. the Assistant Commissioner of Income Tax and Ors. wherein, it was held that, the Revenue Department could only re-open an assessment beyond four years, if there was a failure on the part of the assessee to disclose material facts fully and truly and not on the basis of “reason to believe” without satisfying the jurisdictional condition required under the provisions of Section 147 of the IT Act.

|

Section 147 of the IT Act:

|

“Income escaping assessment.

|

If any income chargeable to tax, in the case of an assessee, has escaped assessment for any assessment year, the Assessing Officer may, subject to the provisions of sections 148 to 153, assess or reassess such income or recompute the loss or the depreciation allowance or any other allowance or deduction for such assessment year (hereafter in this section and in sections 148 to 153 referred to as the relevant assessment year).

|

Explanation-For the purposes of assessment or reassessment or re-computation under this section, the Assessing Officer may assess or reassess the income in respect of any issue, which has escaped assessment, and such issue comes to his notice subsequently in the course of the proceedings under this section, irrespective of the fact that the provisions of section 148A have not been complied with.”

|

DISCLAIMER: The views expressed are strictly of the author and A2Z Taxcorp LLP. The contents of this article are solely for informational purpose and for the reader’s personal non-commercial use. It does not constitute professional advice or recommendation of firm. Neither the author nor firm and its affiliates accepts any liabilities for any loss or damage of any kind arising out of any information in this article nor for any actions taken in reliance thereon. Further, no portion of our article or newsletter should be used for any purpose(s) unless authorized in writing and we reserve a legal right for any infringement on usage of our article or newsletter without prior permission.

|

|

|

|

|

|

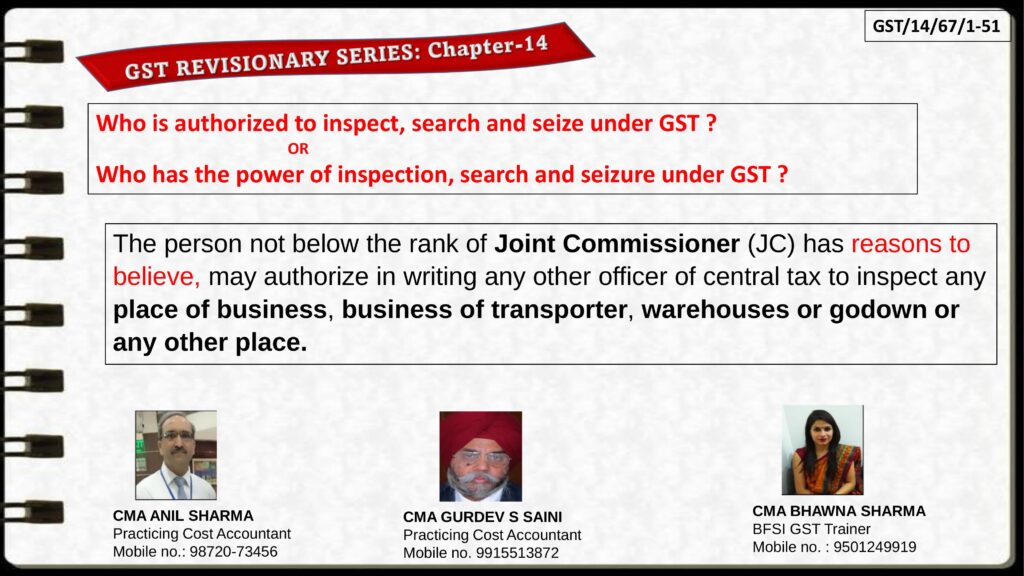

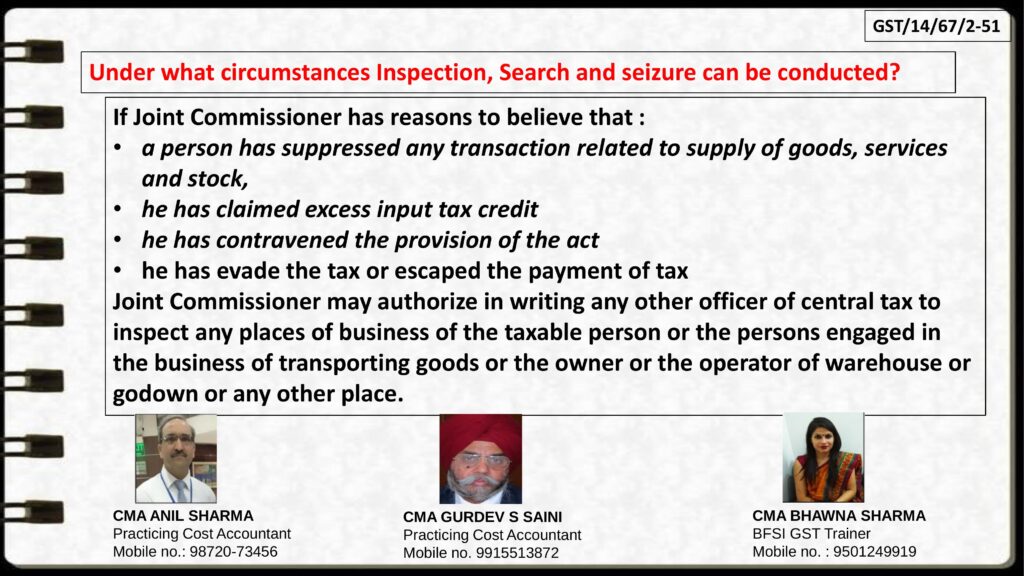

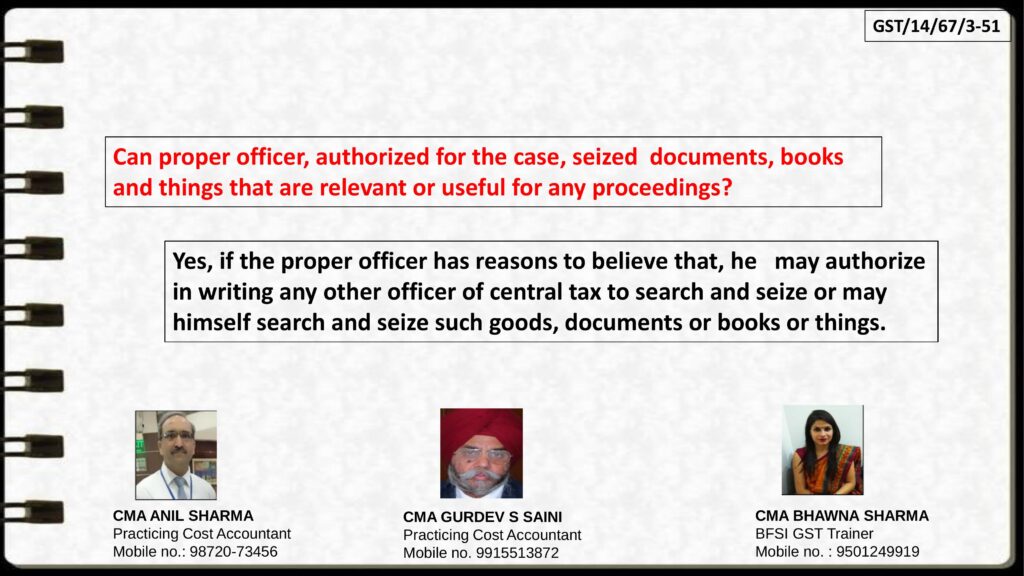

5. GST Notes by CMA Anil Sharma

1) Shri CMA Anil Sharma, Shri CMA Gurdev Singh Saini and Smt. CMA Bhawna Sharma posted Chapter-14 containing CGST Act in simple language in PPT format. This is to make dealers, professionals, academicians, students etc. understand the basics of GST laws. Each Chapter in CGST Act, 2017 is explained in the form of Slides as given below for easy understanding of the Act:

|

Chapter-14 slides given below:-

|

|

|

|

|

|

|

|

|

|

6) Book by CMA Anil Sharma, B.Com (Honrs), M.Com, FCMA co-author of the book

|

|

Handbook on GST Audit by Tax Authorities has authored yet another book

|

|

title Goods & Service Tax – Some Perceptions and Reflections. Buy now at Price Rs.300/-.

|

|

|

|

|

|

You wish to publish your Article?

|

If you wish to share your article with maximum readers then please send them at taxupdate.otu@gmail.com. We shall publish it with all due credit to you.

|

|

|

|

|

|

|

Hope the above updates is of use to you. Please share your input and feedback at taxupdate.otu@gmail.com

|

|

|

|

|

|

|

Visit our website

|

OTU provides you

|

- Articles on various topics

|

|

- Media - GST, Income Tax & Press R.

|

|

- Notes / Newsletter etc.

|

|

|

|

|