|

onlinetaxupdate team wish to express sincere thanks to all the readers, authors, subscribers for the support extended to us. Please share your feedback at

|

taxupdate.otu@gmail.com or 7738647904

|

Newsletter 135 dated 16.09.2024

|

|

|

|

|

|

|

|

|

Dear Reader,

|

Please find newsletter for your reading and reference.

|

|

Index of the Newsletter

- Recent updates

- GST Council - 54th meet proposed

- Article

- Lawgics by Ms.Nidhi Aggarwal

- GST Notes by CMA Anil Sharma

- GST Daily by CA Pradeep Modi

- PPT/Handbook

- GST/IT/Customs in media

- Latest Update - Recap

|

|

|

|

|

|

|

OFFICE OF THE COMMISSIONER OF STATE TAXMAHARASHTRA STATE, MUMBAI issued NOTIFICATION NO: - SGST/e-way bill/02/2025-26 dated 20.02.2026 Waiving off requirement of e-way bill for motor vehicles for road testing where goods are transported for reasons other than by way of supply under sub-rule (5) of rule 138A of MGST Rules, 2017.

|

M/s. Tata Motors Limited, having principal place of business at TATA MOTORS LIMITED, Nigadi Bhosari Road, Pimpri Chinchwad, Pune, Maharashtra, 411 018. (GSTIN: 27AALCT0864B1ZE) (hereinafter called as ‘taxpayer’), have made a representation vide their letter GST/MH/056 dated 13th November 2025. for waiving off requirement of e-way bill for motor vehicles for road testing where goods are transported for reasons other than by way of supply under sub-rule (5) of rule 138A of MGST Rules, 2017(hereinafter referred as MGST Rules, 2017).

|

Whereas I, Asheesh Sharma, Commissioner of State Tax. Maharashtra State, am of the opinion that the difficulties being faced by the ‘taxpayer’ are genuine and require due consideration. Now, therefore I, Asheesh Sharma, Commissioner of State Tax, Maharashtra State, in exercise of the powers conferred upon me under sub-rule (5) of rule 138A of the MGST Rules, 2017, am pleased to issue this notification for grant of permission to M/s. Tata Motors Limited. having principal place of business at TATA MOTORS LIMITED, Nigadi Bhosari Road, Pimpri Chinchwad, Pune, Maharashtra, 411 018 (GSTIN: 27AALCT0864B1ZE) to waive the requirement of e-way bill for motor vehicles to perform various road tests across India, subject to the following procedure and conditions as mentioned below.

|

(i) The ‘ taxpayer ’ shall execute a bond sufficient to cover the value of the motor vehicle being cleared for the purpose of road testing in a calendar month, with the Jurisdictional State Tax Officer, PIMPRI_702, Division - PUNE_SOUTH_EAST, Zone - PUNE_SOUTH_WEST, PUNE undertaking to follow all the conditions mentioned hereunder;

|

(ii) Motor vehicles shall be removed by the ‘taxpayer’ for the purpose of road test under a delivery challan, duly signed by the authorized signatory of the “taxpayer”;

|

(iii) The exemption to carry delivery challan instead of e-way bill is limited only to transportation of motor vehicles for reasons other than by way of supply and limited to road test of such motor vehicles;

|

(iv) The delivery challan shall be induplicate, pre-authenticated and having running serial number for every calendar year and printed format and shall contain the following information.

|

(a) The name and address of the “taxpayer”, it’s ‘GSTIN’

|

(b) Name of the jurisdictional officer, Division and Zone with whom the taxpayer is registered for the purpose of GST and notification number under which permission under sub-rule (5) of rule 138(A) of MGST Rules, 2017 for such removal has been given;

|

(c) The description, vehicle serial number/ engine number/ chassis number, as the case may be, to identify the vehicle which has been cleared for the purpose carrying out road test along with the value of such motor vehicle;

|

(d) The date of dispatch of such motor vehicle for road test and probable time line for return of the motor vehicles to its place of clearance;

|

(v) The Motor vehicle/ transport equipment will also carry trade plate as prescribed under Central Motor Vehicles Rules, 1989 or under any other law in force for the purpose of undertaking testing of such motor vehicle as the case may be;

|

(vi) The ‘taxpayer’ shall maintain proper records to correlate the dispatch and return of the motor vehicles sent for road testing. If at any point of time the value of the motor vehicles cleared for road test exceeds the amount for which the bond has been executed, the ‘taxpayer’ shall execute a separate bond of differential value with the concerned, before removal of the motor vehicle for testing purpose;

|

(vii) The taxpayer’ shall submit to the Jurisdictional State Tax Officer, PIMPRI_702, Division - PUNE_SOUTH_EAST, Zone - PUNE_SOUTH_ WEST, PUNE a monthly account containing the details of all motor vehicles sent and received back after road testing;

|

(viii) The ‘taxpayer’ shall furnish any additional relevant information pertaining to the instant subject matter which may be required by the Jurisdictional State Tax Officer, PIMPRI_702, Division-PUNE_SOUTH_EAST, Zone - PUNE_SOUTH_WEST, PUNE.

|

2. The ‘ taxpayer ’ shall be fully responsible and accountable for the taxable goods so removed without generation of e-way bill under sub-rule (5) of rule 138(A) of MGST Rules, 2017 as permitted under this notification.

|

3. If the above said conditions are not adhered to or are violated, the impugned permission shall be revoked/withdrawn without any prior intimation.

|

4. This notification is valid for financial year 2025-26, i.e. up to 31st March 2026

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Circular no. 255/01/2026-GST dated 25.06.2026 to provide Clarification regarding jurisdiction in cases involving migration/ transfer of taxable persons from one jurisdiction to another jurisdiction.

|

|

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Circular no. 254/11/2025-GST dated 27.10.2025 regarding Assigning proper officer under section 74A, section 75(2) and section 122 of the Central Goods and Services Tax Act, 2017

|

|

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Circular no. 253/10/2025-GST dated 01.10.2025 for withdrawal of circular No. 212/6/2024-GST.

|

F. No. CBIC-20001/3/2025-GST

Government of India

Ministry of Finance

Department of Revenue

Central Board of Indirect Taxes and Customs

GST Policy Wing

|

Circular No. 253/10/2025 – GST dated 01.10.2025

|

The Principal Chief Commissioners / Chief Commissioners (All)

|

The Principal Director Generals / Director Generals (All)

|

Subject: Withdrawal of circular No. 212/6/2024-GST dated 26th June, 2024 – reg.

|

Kind attention is invited to circular No. 212/6/2024-GST dated 26th June, 2024 wherein clarifications were given in relation to mechanism for providing evidence of compliance of conditions of Section 15(3)(b)(ii) of the CGST Act, 2017 by the suppliers.

|

2. In order to ensure uniformity in the implementation of the provisions of the law across field formations, the Board, in exercise of its powers conferred by section 168(1) of the Central Goods and Services Tax Act, 2017, hereby withdraws, circular No. 212/6/2024-GST dated 26th June, 2024. Therefore, the procedure prescribed vide the aforesaid circular for providing evidence of compliance of conditions of Section 15(3)(b)(ii) shall not be required.

|

3. It is requested that suitable trade notices may be issued to publicize the contents of this Circular.

|

4. Difficulty, if any, in implementation of this circular may please be brought to the notice of the Board.

|

(Gaurav Singh)

Commissioner (GST)

|

|

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Circular no. 252/09/2025-GST dated 23.09.2025 regarding Communication to taxpayers through eOffice - requirement of Document Identification Number (DIN)

|

F. No. GST/INV/DIN-Utility/2022-23

Government of India

Ministry of Finance

Department of Revenue

(Central Board of Indirect Taxes and Customs)

|

Circular No. 252/09/2025 -GST dated 23.09.2025

|

Subject: Communication to taxpayers through eOffice - requirement of Document Identification Number (DIN) - reg.

|

Attention is invited to Board's Circular No. 122/41/2019- GST dated 05th November 2019 and 128/47/2019-GST dated 23rd December 2019 regarding Generation and Quoting of Document Identification Number (DIN), initially on specified documents and subsequently expanded to all communications (including e-mails) sent to taxpayers and concerned persons.

|

2. Attention is also invited to subsequent Board's Circular No. 249/06/2025-GST dt. 09th June 2025 clarifying that for communications via GST common portal (in compliance with Section 169 of the CGST Act, 2017) having verifiable Reference Number (RFN), quoting of Document Identification Number (DIN) is not required and such communication bearing RFN is to be treated as a valid communication.

|

3. On similar lines, it has been brought to the notice of the Board that communications issued through eOffice of CBIC bear an automatically generated unique ‘Issue number’. However, no online utility was available to verify the authenticity of such communications through Issue number, hence DIN was required to be generated and quoted on such communications. Now an online utility has been developed and made functional (URL https://verifydocument.cbic.gov.in ) , where the taxpayers and other concerned persons can verify online the electronically generated unique “Issue number” borne on communications dispatched using public option in eOffice application by CBIC officers. Upon verification, this utility confirms the Issue number, and other details and provides information to authenticate the document, like, -

|

i. File number,

ii. Date of issuing the document,

iii. Type of communication,

iv. Name of Office issuing the document,

v. Recipient name (masked),

vi. Recipient address (masked),

vii. Recipient email (masked).

|

4. The name of the office issuing the document is captured from the data available within eOffice, while the document type, recipient name, recipient address, recipient email are entered in the metadata by the officers creating the document. Officers responsible for issuing communications via CBIC's eOffice must mandatorily fill and ensure correctness of this information in the metadata while creating the draft before its approval.

|

5. In light of the above, quoting separate DIN on such communications dispatched using public option in eOffice application, which already bear issue number, will result into two different electronically generated verifiable unique numbers namely Issue No. & DIN on the same communication, which renders quoting of separate DIN on such communication unnecessary. It is therefore decided that for communications dispatched using public option in CBIC’s eOffice application, the verifiable eOffice ‘Issue number’ shall be deemed to be the Document Identification Number and such communication shall be treated as a valid communication.

|

6. The Document Identification Number generated through DIN utility shall continue to be mandatorily quoted on all other communications which have either not been dispatched using public option in CBIC’s eOffice application or which do not bear the verifiable Reference Number (RFN) generated on GST common portal.

|

7. To the above extent, Circular No. 122/41/2019- GST dated 05th November 2019, Circular No. 128/47/2019-GST dated 23rd December 2019 and Circular No. 249/06/2025-GST dated 09th June 2025 issued by the Board, stands modified.

|

भवदी य,

(डॉ . अभि )

आयु क्त, (आरआई & आई)

सी

.बी .आई.सी ., राजस्व विविवभाग

ई मे ल आई डी : gstinv-cbic@gov.in

|

To,

1. All Pr. Chief Commissioners/Chief Commissioners, CGST Zones/ CGST & Customs Zones.

2. All Principal Directors General/Directors General under CBIC.

3. DG-Systems for incorporating appropriate information/link for taxpayers for verification of documents containing eOffice ‘Issue No.’ along with verification links for communications bearing DIN or RFN generated through GST Common portal.

4. The webmaster, CBIC for uploading on official website.

|

|

|

|

|

|

GSTN Advisory no. 666 dated 01.07.2026

|

It is informed that the Aggregate Annual Turnover (AATO) functionality is currently being upgraded to enable automatic updation of AATO as subsequent returns are filed post amendment window. As this enhanced functionality is being deployed from 1st July 2026, the window for amendment of AATO by taxpayers for FY 2025-26 has been revised on the GST Portal.

|

GSTN had earlier issued an advisory dated 02 May 2022 regarding the functionality for amendment of Aggregate Annual Turnover (AATO) on the GST Portal, which was applicable for AATO till FY 2024-25. Under the said advisory, taxpayers were provided the facility to amend their turnover during the month of May.

|

In continuation thereof, it is informed that the timelines for submission of amendment applications and verification of amended AATO details by Tax Officers, in respect of FY 2025-26, have been revised.

|

To ensure greater consistency, accuracy, and uniformity in the reporting of AATO across various modules of the GST Portal, certain system-level enhancements are being implemented. Consequently, the revised timelines for amendment of AATO for FY 2025-26 by the taxpayers and subsequent action by the tax officers are as under:

|

AATO Amendment Application window for FY 2025-26

01 July to 31 July 2026

|

Review by jurisdictional Tax officer

01 Aug to 15 Aug 2026

|

Accordingly, the facility for amendment of AATO, which was earlier available during May as per the previous advisory, shall now be made available from 01 July to 31 July 2026 for FY 2025-26. The amended AATO details will be available for review of Tax Officers from 01 Aug to 15 Aug.

|

All taxpayers are requested to take note of the revised timelines and carefully review the AATO details while submitting the amendment application and ensuring that the amended details are accurate before submission.

|

In case of any difficulty or concern, taxpayers are advised to raise a grievance through the Self-Service Portal available on the GST Portal, along with all relevant details, to facilitate prompt and effective resolution.

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Corrigendum on 12.06.2026 to Notification no. 45/2025 -Customs dated 24.10.2025 -

|

G.S.R…(E).- In the notification of the Government of India, Ministry of Finance (Department of Revenue) No. 45/2025-Customs, dated the 24th October, 2025, published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i), vide number G.S.R. 781(E), dated the 24th October, 2025, at page 291, in lines 12 and 14, for ‘1993’ read ‘1983’.

|

|

|

|

|

|

CBIC issued Notification No. 58/2026-Customs (N.T.) dated 22.06.2026 to hereby appoint the officer to exercise the powers and discharge the duties conferred on the officers for the purpose of adjudication of the show cause notices.

|

|

|

|

|

|

|

|

CBIC issued Notification No. 57/2026-Customs (N.T.) dated 18.06.2026 to further amend Notification No. 27/2018-Customs (N.T.) dated 28.03.2018.

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Circular no. 28/2026-Customs dated 15.06.2026 regarding testing of samples of export consignments

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Notification no. 03/2026 – Customs (CVD) dated 10.06.2026 to amend Notification no. 4/2021-Customs (CVD) dated 24.09.2021

|

Government of India

Ministry of Finance

(Department of Revenue)

|

Notification No. 3/2026-Customs (CVD) dated 10.06.2026

|

G.S.R…-(E).- In exercise of the powers conferred by sub-sections (1) and (6) of section 9 of the Customs

Tariff Act,1975 (51 of 1975), read with rules 20 and 24 of the Customs Tariff (Identification, Assessment and Collection of Countervailing Duty on Subsidized Articles and for Determination of Injury) Rules, 1995, the Central Government hereby makes the following amendment in the notification of the Government of India, in the Ministry of Finance (Department of Revenue) No. 4/2021-Customs (CVD), dated the 24th September, 2021, published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i), vide number G.S.R. 662(E), dated the 24th September, 2021, namely:-

|

In the said notification, after paragraph 2, the following paragraph shall be inserted, namely:-

|

“3. Notwithstanding anything contained in paragraph 2, the countervailing duty imposed under this

notification shall remain in force up to and inclusive of the 23rd March, 2027, unless revoked, superseded or amended earlier.”.

|

(Dheeraj Sharma)

Under Secretary

|

Note: The principal notification No. 4/2021-Customs (CVD) dated the 24th September, 2021, was published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i), vide number G.S.R. 662(E), dated the 24th September, 2021.

|

|

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Notification no. 02/2026 – Customs (CVD) dated 02.06.2026

|

|

|

|

|

|

Export consignments to West Asia will continue to receive enhanced insurance cover against payment defaults until September 30, the Directorate General of Foreign Trade (DGFT) said in a notification on Monday.

|

Earlier, the enhanced cover for exporters taking credit risk insurance from Export Credit Guarantee Corporation (ECGC) was available for shipments to West Asia sent between March 16 and June 15.

|

The enhanced risk cover announced on March 19 was part of the Resilience and Logistics Intervention for Export Facilitation (RELIEF) scheme under the Export Promotion Mission (EPM) to support exports to West Asia in view of the Iran war.

|

"The eligibility timelines under Component II of the EPM RELIEF intervention are extended up to September 30, 2026 to support Indian exporters and mitigate logistics challenges arising out of the continuing West Asia Crisis," the DGFT said.

|

Source: The Economic Times

|

|

|

|

|

|

|

|

Directorate General of Foreign Trade (DGFT) issued Public Notice No. 17/2026-27 dated 04.06.2026 regarding Enlistment under Appendix 2E of FTP, 2023-Agency Authorised to issue Certificate of Origin (Non-Preferential)

|

|

|

|

|

|

|

|

Directorate General of Foreign Trade (DGFT) issued Trade Notice 07/2026-27 dated 03.06.2026 regarding request for comments on alignment of Schedule-II (Export Policy) of ITC (HS), 2022 consequent to amendments introduced under the Finance Act, 2026

|

|

|

|

|

|

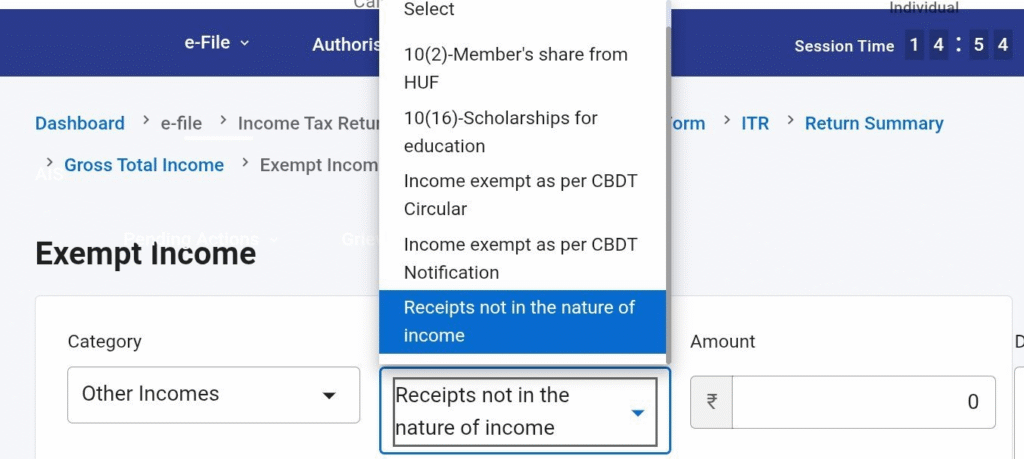

From AY 2026-27, the option to report 'Other Exempt Income' was removed.

|

Earlier, this was useful in situations such as:

|

- Sale of rural agricultural land/ Reporting of Gifts from Relatives - although disclosure was not required as same is not income .

|

The column of 'Other Income' under Exempt incomes has now been added.

|

|

|

|

|

|

|

|

|

Press release ID 2279424 dated 30.06.26

|

The Government had earlier provided a full Customs Duty exemption on imports of critical petrochemical products till 30th June 2026, as a temporary and targeted relief in view of the conflict in West Asia and the consequent disruptions in global supply chains.

|

The exemption was provided to ensure sufficient availability of petrochemicals in the domestic market as Indian petroleum companies had been asked to concentrate on the production of LPG during this period. As the situation is gradually normalizing, to ensure a smooth and non-disruptive transition for the affected sectors, it has been decided to extend the said exemption by a further period of 15 days, that is, till 15th July 2026.The list of products covered remains the same as notified earlier.

|

The Government remains committed to supporting India's manufacturing sector. As before, the exemption is expected to benefit a wide range of sectors dependent on petrochemical feedstock and intermediates, including plastics, packaging, textiles, pharmaceuticals, chemicals, automotive components and other manufacturing segments. This will also provide relief to consumers of final products.

|

Link to previous press note issued:

|

|

|

|

|

|

|

|

Press release ID 2279409 dated 30.06.2026

|

|

In a major operation the officers of the Directorate of Revenue Intelligence (DRI) successfully dismantled a trans-border gold smuggling syndicate and seized 15 kg foreign-origin smuggled gold, valued at approximately Rs. 21.40 crore, operating from Delhi.

|

|

|

DRI officers intercepted an international courier consignment originating from Thailand at Courier Terminal, Delhi. The consignment was in the name of a firm linked to a foreign national.

|

A meticulous examination of the consignment declared as "worn gear", led to the recovery of eight disc-shaped pieces of foreign-origin gold, each weighing 1.5 kg, ingeniously concealed inside gear parts. In total, 12 kg smuggled foreign-origin gold was recovered from the courier consignment.

|

Simultaneous searches conducted at the residence of the intended recipient and the alleged mastermind resulted in the recovery of two more identical disc-shaped pieces of foreign-origin gold, each weighing 1.5 kg.

|

Four persons, including the mastermind, who is a repeat offender, and a foreign national have been arrested in relation with the case.

|

Preliminary investigations also reveal that crypto-currency was being used to transfer the money across borders to finance the smuggling.

|

|

|

|

|

|

|

|

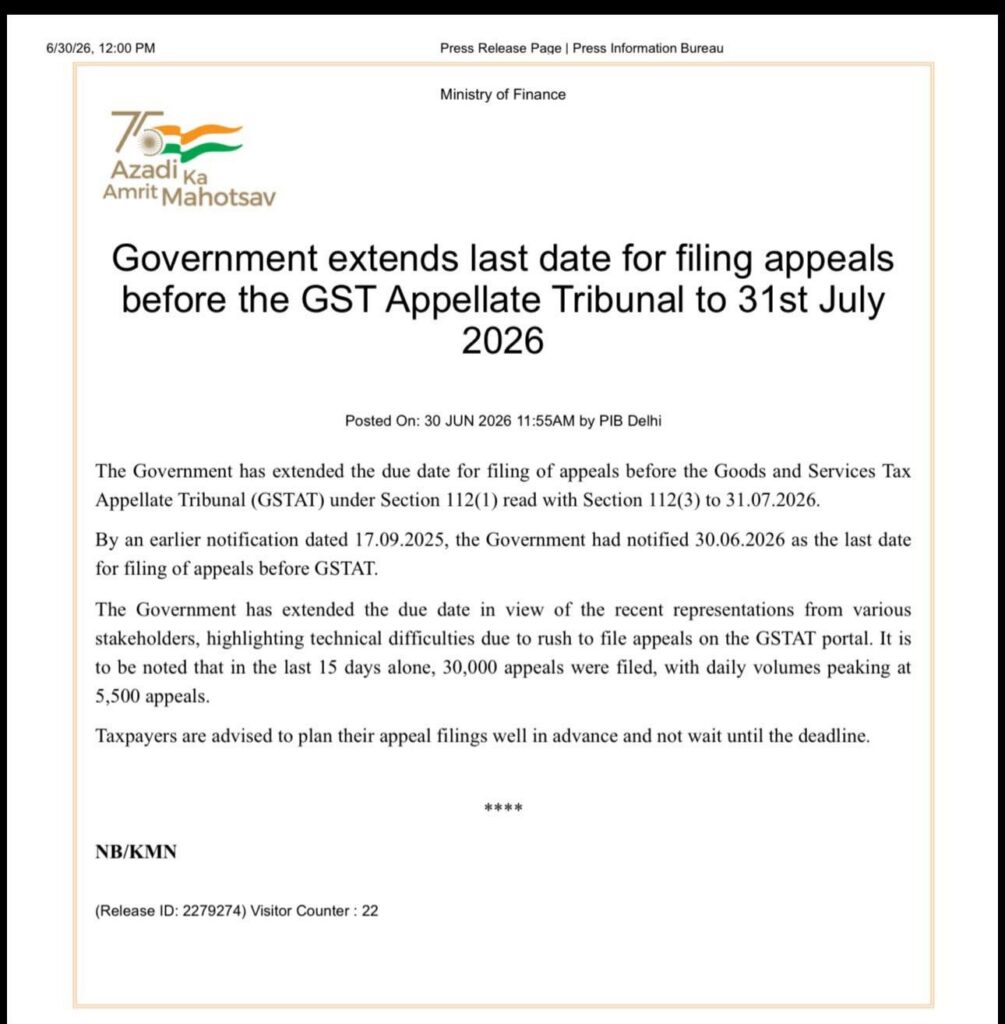

Source: Press release id 2279274 dated 30.06.26

|

The government has extended the due date for filing of appeal before the Goods and Services Tax Appellate Tribunal (GSTAT) under section 112(1) read with section 112(3) to 31.07.2026.

|

The government has extended the due date in view of the recent representation from various stakeholders , highlighting technical difficulties due to rush to file appeals on the GSTAT portal. It is to be noted that in the last 15 days alone, 30,000 appeals were filed, with daily volumes peaking at 5,500 appeals.

|

|

Taxpayers are advised to plan their appeal filings well in advance and not wait until the deadline.

|

|

|

|

|

|

|

|

|

|

|

Press release ID 2278205 dated 26.06.26

|

|

In a major crackdown against smuggling of foreign origin gold, the the Directorate of Revenue Intelligence (DRI) has successfully unearthed and dismantled a highly organised gold smuggling syndicate operating through Mumbai Airport. In this operation DRI detected and busted gold melting facility that was being used for melting of foreign origin smuggled gold.

|

|

|

Seized gold from melting facility in Mumbai

|

A total of nine persons involved across the entire smuggling chain, including the airport staff, her handler, three intermediaries, the melting facility operator, and three persons engaged in the melting process have been arrested. Further, about 6 kg foreign-origin smuggled gold recovered at the spot has been seized.

|

|

This case underscores the evolving sophistication of organised gold smuggling syndicates, which increasingly exploit insider access at airports and employ layered distribution networks to evade detection. In another operation at Bengaluru, DRI seized 1.8 kg 24 KT gold in paste form ingeniously concealed within the layers of garments of an international passenger. Subsequent follow up search at his residential premises led to seizure of around 1.5 kg gold jewellery, 45 kg silver, and Indian & foreign currencies. The person was arrested.

|

|

|

Gold in paste form concealed in undergarments; Seized at Bengaluru

|

|

earlier in this week, DRI has conducted a series of operations at other airports, railways station and land customs stations at Hyderabad, Rajkot, Calicut, Vishakhapatnam, Calicut, Guwahati and Petrapole, leading to the cumulative seizure of another 6 kg foreign-origin smuggled gold. Five persons have been arrested in these operations.

|

|

|

Overall, with busting of gold smuggling syndicate, these operations resulted in seizure of about 15 kg gold, 45 kg silver, valued at around Rs. 23 crore, and arrest of 15 persons.

|

|

|

|

|

|

|

|

Recommendations of the Group of Ministers (GoM) looking into issues pertaining to GST on life and health insurance will be placed before the GST Council when received, Parliament was informed on Monday. The issue of exempting/reducing GST on life and health insurance was placed before the GST Council in its 54th meeting on September 9, 2024.

|

After detailed deliberations, the Council recommended constituting a GoM to holistically look into issues pertaining to GST on life and health insurance. Accordingly, a GoM was constituted under the Chairmanship of Samrat Chaudhary, Deputy Chief Minister of Bihar.

|

First meeting of the GoM was held on October 19, 2024 at New Delhi where issues of GST rate on health and life insurance policies were discussed, Minister of State for Finance Pankaj Chaudhary said in a written reply to the Lok Sabha.

|

"Recommendations of the GoM when received will be placed before the GST Council," he said.

|

GST on health insurance services and pure term life insurance services is levied at standard rate of 18 per cent.

|

GST rates and exemptions on all services (including health and life insurance) are prescribed on recommendations of the GST Council, a constitutional body comprising members from both the Union and State/UT governments.

|

Replying to another question, the minister informed the House that revenue generated from GST on healthcare and life insurance services was Rs 8,263 crore and Rs 8,135 crore, respectively during fiscal 2023-24, as against Rs 7,638 crore and Rs 9,132 crore in the preceding financial year.

|

|

|

|

|

|

GST Council recommends Group of Ministers (GoM) on life and health insurance related GST with existing GoM on Rate Rationalisation; to submit report by end of October 2024

|

GST Council also recommends formation of a GoM to study the future of compensation cess

|

GST Council recommends to exempt supply of research and development services by a Government Entity; or a research association, university, college or other institution notified u/s 35 of Income Tax Act using government or private grants

|

GST Council recommends reduction in GST rates on cancer drugs - Trastuzumab Deruxtecan, Osimertinib and Durvalumab from 12% to 5%.

|

GST Council recommends roll out of a pilot for B2C e-Invoicing

|

The 54th GST Council met under the Chairpersonship of Union Minister for Finance & Corporate Affairs Smt. Nirmala Sitharaman in New Delhi today i.e. 09.09.2024.

|

The meeting was also attended by Union Minister of State for Finance Shri Pankaj Chaudhary, Chief Ministers of Goa and Meghalaya; Deputy Chief Ministers of Arunachal Pradesh, Bihar, Madhya Pradesh, and Telangana; besides Finance Ministers of States & UTs (with legislature) and senior officers of the Ministry of Finance & States/ UTs.

|

The GST Council inter-alia made the following recommendations relating to changes in GST tax rates, provide relief to individuals, measures for facilitation of trade and measures for streamlining compliances in GST.

|

A. Changes/Clarifications in GST Tax Rates:

|

1. Namkeens and Extruded/Expanded Savoury food products

|

- The GST rate of extruded or expanded products, savoury or salted (other than un-fried or un-cooked snack pellets, by whatever name called, manufactured through process of extrusion), falling under HS 1905 90 30 to be reduced from 18% to 12% at par with namkeens, bhujia, mixture, chabena (pre-packaged and labelled) and similar edible preparations in ready for consumption form which are classifiable under HS 2106 90. The GST rate of 5% will continue on un-fried or un-cooked snack pellets, by whatever name called, manufactured through process of extrusion.

- To also clarify that the reduced GST rate of 12% on extruded or expanded products, savoury or salted (other than un-fried or un-cooked snack pellets, by whatever name called, manufactured through process of extrusion), falling under HS 1905 90 30 is applicable prospectively.

- The GST rate on cancer drugs namely, Trastuzumab Deruxtecan, Osimertinib and Durvalumab to be reduced from 12% to 5%.

- Reverse Charge Mechanism (RCM) to be introduced on supply of metal scrap by unregistered person to registered person provided that the supplier shall take registration as and when it crosses threshold limit and the recipient who is liable to pay under RCM shall pay tax even if supplier is under threshold.

- A TDS of 2% will be applicable on supply of metal scrap by registered person in B to B supply.

4. Roof Mounted Package Unit (RMPU) Air Conditioning Machines for Railways

|

- To clarify that Roof Mounted Package Unit (RMPU) Air Conditioning Machines for Railways would be classified under HSN 8415 attracting a GST rate of 28%.

5. Car and Motor cycle seats

|

- To clarify that car seats are classifiable under 9401 and attract a GST rate of 18%.

- GST rate on car seats classifiable under 9401 to be increased from 18% to 28%. This uniform rate of 28% will be applicable prospectively for car seats of motor cars in order to bring parity with seats of motorcycles which already attract a GST rate of 28%.

1. Life and Health insurance

|

- GST Council recommended to constitute a Group of Ministers (GoM) to holistically look into the issues pertaining to GST on the life insurance and health insurance. The GoM members are Bihar, UP, West Bengal, Karnataka, Kerala, Rajasthan, Andhra Pradesh, Meghalaya, Goa, Telangana, Tamil Nadu, Punjab, and Gujarat. The GoM is to submit the report by end of October 2024.

2. Transport of passengers by helicopters

|

- To notify GST @ 5% on the transport of passengers by helicopters on seat share basis and to regularise the GST for past period on ‘as is where is’ basis. To also clarify that charter of helicopter will continue to attract 18% GST.

3. Flying training courses

|

- To clarify by way of a circular that the approved flying training courses conducted by DGCA approved Flying Training Organizations (FTOs) are exempt from the levy of GST.

4. Supply of research and development services

|

- The GST Council recommended to exempt supply of research and development services by a Government Entity; or a research association, university, college or other institution, notified under clauses (ii) or (iii) of sub-section (1) of section 35 of the Income Tax Act, 1961 using Government or private grants.

- Past demands to be regularised on ‘as is where is’ basis.

5. Preferential Location Charges (PLC)

|

- To clarify that location charges or Preferential Location Charges (PLC) paid along with the consideration for the construction services of residential/commercial/industrial complex before issuance of completion certificate forms part of composite supply where supply of construction services is the main service and PLC is naturally bundled with it and are eligible for same tax treatment as the main supply that is, construction service.

i. To clarify that affiliation services provided by educational boards like CBSE are taxable. However, to exempt affiliation services provided by State/Central educational boards, educational councils and other similarly placed bodies to Government Schools prospectively. The issue for the past period between 01.07.2017 to 17.06.2021 to be regularized on ‘as is where is’ basis.

|

ii. To clarify by way of circular that the affiliation services provided by universities to their constituent colleges are not covered within the ambit of exemptions provided to educational institutions in the notification No. 12/2017-CT(R) dated 28.06.2017 and GST at the rate of 18% is applicable on the affiliation services provided by the universities.

|

7. Import of service by branch Office

|

- To exempt import of services by an establishment of a foreign airlines company from a related person or any of its establishment outside India, when made without consideration. The council also recommended to regularise the past period on ‘as is where is’ basis.

8. Renting of commercial property

|

- To bring renting of commercial property by unregistered person to a registered person under Reverse Charge Mechanism (RCM) to prevent revenue leakage.

9. Ancillary/intermediate services are provided by GTA

|

- To clarify that when ancillary/intermediate services are provided by GTA in the course of transportation of goods by road and GTA also issues consignment note, the service will constitute a composite supply and all such ancillary/intermediate services like loading/unloading, packing/unpacking, transshipment, temporary warehousing etc. will be treated as part of the composite supply. If such services are not provided in the course of transportation of goods and invoiced separately, then these services will not be treated as composite supply of transport of goods.

10. To regularise the GST liability for the past period prior to 01.10.2021 on ‘as is where is’ basis, where the film distributor or sub-distributor acts on a principal basis to acquire and distribute films.

|

11. To exempt supply of services such as application fees for providing electricity connection, rental charges against electricity meter, testing fees for meters/ transformers/capacitors, labour charges from customers for shifting of meters/service lines, charges for duplicate bills etc. which are incidental, ancillary or integral to the supply of transmission and distribution of electricity by transmission and distribution utilities to their consumers, when provided as a composite supply. GST for the past period to be regularised on ‘as is where is’ basis.

|

B. Measures for facilitation of trade:

|

- Procedure and conditions for waiver of interest or penalty or both, in respect of tax demands under section 73 of CGST Act, 2017 for FYs 2017-18, 2018-19 and 2019-20 as per section 128A of CGST Act, 2017:

- The GST Council recommended insertion of rule 164 in CGST Rules, 2017, along with certain Forms, providing for the procedure and conditions for availment of benefit of waiver of interest or penalty or both, relating to tax demands under section 73 of CGST Act, pertaining to FYs 2017-18, 2018-19 and 2019-20, as per section 128A of CGST Act. The Council also recommended to notify under sub-section (1) of section 128A of CGST Act, 31.03.2025 as the date on or before which the payment of tax may be made by the registered persons, to avail the said benefit as per section 128A of the CGST Act. The Council also recommended the issuance of a circular to clarify various issues related to availment of waiver of interest or penalty or both as per section 128A of CGST Act. The Council also recommended that section 146 of Finance (No. 2) Act, 2024, which provides for insertion of section 128A in CGST Act, 2017, may be notified with effect from 01.11.2024.

- Providing a mechanism for implementation of newly inserted sub-section (5) and sub-section (6) in section 16 of CGST Act, 2017:

- The GST Council recommended that section 118 and 150 of the Finance (No. 2) Act, 2024, which provides for insertion of sub-section (5) and sub-section (6) in section 16 of CGST Act, 2017 retrospectively with effect from 01.07.2017, may be notified at the earliest.

- The Council also recommended that a special procedure for rectification of orders may be notified under section 148 of the CGST Act, to be followed by the class of taxable persons, against whom any order under section 73 or section 74 or section 107 or section 108 of the CGST Act has been issued confirming demand for wrong availment of input tax credit on account of contravention of provisions of sub-section (4) of section 16 of the CGST Act, but where such input tax credit is now available as per the provisions of sub-section (5) or sub-section (6) of section 16 of the CGST Act, and where appeal against the said order has not been filed. The Council also recommended issuance of a circular to clarify the procedure and various issues related to implementation of the said provisions of sub-section (5) and sub-section (6) of section 16 of CGST Act, 2017.

- Amendments in rule 89 and rule 96 of CGST Rules, 2017 and to provide clarification in respect of IGST refunds on exports where benefit of concessional/ exemption notifications specified under rule 96(10) of CGST Rules, 2017 has been availed on the inputs:

- The GST Council recommended to clarify that where the inputs were initially imported without payment of integrated tax and compensation cess by availing benefits under Notification No. 78/2017-Customs dated 13.10.2017 or Notification No. 79/2017-Customs dated 13.10.2017, but IGST and compensation cess on such imported inputs are subsequently paid, along with applicable interest, and the Bill of Entry in respect of the import of the said inputs is got reassessed through the jurisdictional Customs authorities to this effect, then the IGST paid on exports, refunded to the said exporter shall not be considered to be in contravention of provisions of sub-rule (10) of rule 96 of CGST Rules.

- Further, considering the difficulty being faced by the exporters due to restriction in respect of refund on exports, imposed vide rule 96(10), rule 89(4A) & rule 89(4B) of CGST Rules, 2017, in cases where benefit of the specified concessional/ exemption notifications is availed on the inputs, the Council recommended to prospectively omit rule 96(10), rule 89(4A) & rule 89(4B) from CGST Rules, 2017. This will simplify and expedite the procedure for refunds in respect of such exports.

- Issuance of clarifications through the circulars to remove ambiguity and legal disputes in certain issues:

- The GST Council recommended issuance of circulars to provide clarity and to remove doubts and ambiguities arising in the following issues due to varied interpretations by the field formations:

- i. Clarification on the Place of Supply of advertising services provided by Indian advertising companies to foreign entities.

- ii. Clarification regarding availability of Input Tax Credit on demo vehicles by the dealers of the vehicle manufacturers.

- iii. Clarification on Place of Supply of data hosting services provided by service providers located in India to cloud computing service providers located outside India.

- The Council also recommended amendments in some other provisions of CGST Rules, 2017.

- B2C E-invoicing:

The GST Council recommended roll out of a pilot for B2C e-Invoicing, following the successful implementation of e-invoicing in the B2B sector. The Council recognized potential benefits of e-invoicing in retail, such as improved business efficiency, environmentally friendly, cost efficiency to the business, etc.

|

It would also provide an opportunity to the retail customers to verify the reporting of the invoice in the GST return. The pilot will be rolled out on voluntary basis in selected Sectors and States.

|

2. Invoice Management System and new ledgers:

|

The Council also took note of the agenda on the enhancements being made to the existing GST return architecture. These enhancements include the introduction of a Reverse Charge Mechanism (RCM) ledger, an Input Tax Credit Reclaim ledger and an Invoice Management System (IMS). Taxpayers would be given the opportunity to declare their opening balance for these ledgers by 31st October 2024.

|

IMS will allow the taxpayers to accept, reject, or to keep the invoices pending for the purpose of availment of Input Tax Credit. This will be an optional facility for taxpayers to reduce errors in claiming input tax credit and improve reconciliation. This is expected to reduce notices issued on account of ITC mismatch in the returns.

|

Note: The recommendations of the GST Council have been presented in this release containing major item of decisions in simple language for information of the stakeholders. The same would be given effect through the relevant circulars/ notifications/ law amendments which alone shall have the force of law.

|

Press Release ID: 2053233

|

|

|

|

|

|

|

|

In tax law, the plain reading of provisions is the standard approach. However, the attached recent circular marks a unique shift by clarifying the availability of input tax credit (ITC) for demo vehicles based on the intent of the law.

|

Traditionally, tax laws are interpreted literally to ensure clarity and predictability. The purposive approach, which considers the law's intent, is less common in regulatory circulars. This circular highlights that demo vehicles, used to promote the sale of similar vehicles, qualify for ITC, aligning with the broader objective of supporting business operations.

|

So, can taxpayers also use purposive interpretation to argue their cases? While regulatory bodies can issue clarifications based on intent, taxpayers' adoption of such articulations may need to be blessed by the courts.

|

However, the adoption of purposive interpretation in this circular sets a precedent for a more balanced approach to tax law interpretation. It underscores the importance of considering the broader objectives of the law behind a particular restriction or provision.

|

|

|

|

|

|

Author: Adv Minakshi Jain

|

The 54th GST Council met under the Chairpersonship of Union Minister for Finance & Corporate Affairs Smt. Nirmala Sitharaman in New Delhi ondated 09.09.2024. The GST Council inter-alia made the following recommendations relating to changes in GST tax rates, provide relief to individuals, measures for facilitation of trade and measures for streamlining compliances in GST.

|

A. Changes/Clarifications in GST Tax Rates:

|

- Namkeens and Savory Products: GST rate for extruded/expanded savory products (except un-fried/un-cooked snack pellets) reduced from 18% to 12%, aligning with namkeens and similar products. Un-fried/un-cooked snack pellets remain taxed at 5%.

- Cancer Drugs: GST on Trastuzumab Deruxtecan, Osimertinib, and Durvalumab reduced from 12% to 5%.

- Metal Scrap: Reverse Charge Mechanism (RCM) introduced for supply by unregistered persons to registered persons. 2% TDS on B2B supply by registered persons.

- RMPU Air Conditioning for Railways: GST rate clarified as 28% for roof-mounted air conditioning units (HSN 8415).

- Car and Motorcycle Seats: GST rate for car seats increased from 18% to 28%, matching motorcycle seats.

- Life and Health Insurance:Group of Ministers (GoM) to review GST on life and health insurance, report by October 2024.

- Passenger Transport by Helicopter:GST of 5% on seat-share basis for helicopters, regularizing past transactions. Helicopter charters remain taxed at 18%.

- Flying Training Courses:DGCA-approved flying training courses exempt from GST.

- R&D Services:Exemption for research and development services by government or educational institutions funded by government/private grants.

- Preferential Location Charges (PLC):PLC part of composite supply for construction services, taxed the same as construction services.

- Affiliation Services:Affiliation services by boards like CBSE taxable, while services to government schools are exempt prospectively.

- Import of Services by Branch Office:Exempt import of services by foreign airline branches from related parties, regularizing past periods.

- Commercial Property Renting:Renting by unregistered to registered persons under RCM.

GST Liability Regularization: Regularizing GST liability for past transactions in sectors like film distribution, electricity services, etc.

|

B. Measures for facilitation of trade:

|

- Waiver of Interest or Penalty (Section 128A of CGST Act, 2017):

- A procedure has been recommended for waiving interest/penalty related to tax demands for FY 2017-18, 2018-19, and 2019-20 under section 73 of the CGST Act.

- Rule 164 and relevant forms will be inserted for this purpose.

- Payment of tax must be made by 31.03.2025 to avail the waiver.

- Clarifications will be issued through a circular to address related issues.

- Section 128A of the CGST Act will come into effect from 01.11.2024.

- Implementation of Section 16(5) & 16(6) of CGST Act:

- Sections 118 and 150 of Finance (No. 2) Act, 2024, inserting sub-sections (5) and (6) into section 16 of the CGST Act, will be notified retrospectively from 01.07.2017.

- A special procedure under section 148 will be notified for rectification of orders regarding wrong availment of input tax credit.

- Clarification on the procedure will also be issued.

- Amendments to Rule 89 and Rule 96 (IGST Refunds on Exports):

- Clarifications will be provided for IGST refunds where inputs were imported without payment of tax but were subsequently taxed.

- Rule 96(10), Rule 89(4A), and Rule 89(4B) will be omitted to simplify export refund processes.

- Issuance of Clarifications to Resolve Legal Disputes:

- Clarifications will be provided on:

- Place of supply for advertising services to foreign entities.

- Availability of input tax credit on demo vehicles

- Place of supply for data hosting services provided to foreign cloud service providers.

- New procedures for waiver of interest/penalties under the CGST Act.

- Mechanism for rectification and refunds related to input tax credit and exports clarified.

- E-Invoicing for B2C: Pilot launch for B2C e-invoicing in selected sectors and states, following B2B success.

- New Ledgers and Invoice Management System: Introduction of new ledgers and an optional Invoice Management System to improve input tax credit reconciliation.

Note: The recommendations of the GST Council have been presented in this release containing major item of decisions in simple language for information of the stakeholders. The same would be given effect through the relevant circulars/ notifications/ law amendments which alone shall have the force of law.

|

|

|

|

|

|

No, the Honorable High Court of Madhya Pradesh in the case of RCC Infraventures Limited Vs. UOI or Ors. dismissed the writ petition as withdrawn, granting the petitioner the liberty to approach the Appellate Authority for redressal. The Honorable Court observed that the petitioner's registered office is located in Agra, and the Impugned order was passed by the Additional Commissioner, CGST & Central Excise, Agra Commissionerate, Agra. Considering this, the appropriate appellate authority to address the grievance is the Additional Commissioner (Appeals), GST, located in Gomti Nagar, Lukcnow, as indicated in the impugned order. Despite this, the petitioner has opted to file a writ petition under Article 226 of the Constitution of India instead of pursing the alternative remedy of appeal. Consequently the Honorable Court dismissed the writ petition.

|

To approach the High Courts, it must be shown to the Honorable Court that the proceedings:

|

a) Deserves intervention to stop the march of injustice;

|

b) Remedy necessary, cannot be allowed in adjudication of in Appeal.

|

In the instant case, nothing of this sort was placed before the consideration of the Honorable Court; therefore, rightly the Writ petition is disposed off.

|

A Similar decision was rendered by the Honorable Rajasthan High Court in the case of M/s Thekedar Nandlal Sharma V. State of Rajasthan and Ors. where the writ petition against the Assessment Order was dismissed since the remedy of appeal was not availed.

|

|

|

|

|

|

4. Lawgics by Ms.Nidhi Aggarwal

|

Ms. Nidhi Aggarwal is delighted to present judgment with a great vision to spread complex GST law in a simple manner amongst the taxpayers, tax professionals, students and knowledge seeker.

|

|

Recently added notes are listed below:

|

|

|

|

|

|

Synopsis: The Delhi High Court dismissed the writ petition involving fraudulent ITC claims, directing the petitioner to pursue appellate remedy u/s 107 of the CGST Act.

|

Caste name: Banson Enterprises & Anr. vs Assistant Commissioner CGST & Ors.

|

Citation: W.P. (C) 6503/2025 dated 15.05.2025

|

Authority: Delhi High Court

|

The petition challenges the Order-in-Original dated 02.02.2025 based on a Show Cause Notice (SCN) dated 03.08.2024 A search was conducted, and statements were recorded including that of one Director admitting to the issuance of fake invoices during the Central Excise period. It was alleged that the Petitioner issued goods-less invoices to enable fraudulent Input Tax Credit (ITC) claims amounting to Rs. 1.85 crore.

|

Contentions of the Petitioner:

|

SCN was issued by unauthorized officer, thus, violates Rule 142(1)(a) of CGST Rules. No pre-consultation as required under Rule 142(1A) of CGST Rules was issued. Consolidated SCN for multiple financial years was issued and challenge to such consolidated action is pending in a separate matter (Quest Infotech case).

|

Contentions of the Department:

The impugned order is appealable, hence writ is not maintainable. The Petitioner’s Director admitted to allegations. Natural justice was followed as the Petitioner received the SCN, filed a reply, and availed of personal hearing. Reliance must be made on SC judgments and Allahabad HC rulings emphasizing alternate remedy u/s 107 CGST Act.

|

Findings and Decision of the Court:

The Court refused to interfere under writ jurisdiction, citing:

|

- No breach of fundamental rights or principles of natural justice.

- Availability of a statutory remedy (appeal) under Section 107 CGST Act.

The Court noted that the Allegations involve serious misuse of ITC, requiring fact-based adjudication, not suited for writ jurisdiction. Thus, the Petitioner was granted liberty to file appeal, and if filed with pre deposit, the appeal shall not be dismissed on limitation.

|

|

|

|

|

|

5. GST Notes by CMA Anil Sharma

1) New slides on GST Circulars is added in the Notes section titled as "Capsules".

|

- Total 25 slides in capsule-01 is added

|

|

|

|

|

|

|

|

6. GST Daily by CA Pradeep Modi

CA Pradeep Modi is presenting judgment analysis under title 'GST Daily - Stay yourself updated'

|

|

|

|

|

|

THE HON'BLE ALLAHABAD HIGH COURT IN THE CASE OF Vibhuti Tyres V/s State of U.P., decided on 7-5-2025

|

✔️ Is it justified that GST order with higher demand than show-cause notice?

|

👉 The Hon'ble High Court Judgement:-

|

✔️ Where in show-cause notice amount representing tax, interest and penalty was indicated as Rs. 8,81,080, but in order, much higher demand was raised at Rs. 32,97,336, same was in violation of section 75(7); matter was to be remanded back.

|

Section 75 of Central Goods and Services Tax Act, 2017

|

|

|

|

|

|

7. PPT/Handbook on GST

|

|

|

|

8. GST/Income Tax in Media

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Hope the above updates is of use to you. Please share your input and feedback at taxupdate.otu@gmail.com

|

|

|

|

|

|

|

|

|

Visit our website

|

OTU provides you

|

- Articles on various topics

|

|

- Media - GST, Income Tax & Press R.

|

|

|

|

|