|

|

|

|

|

|

|

Happy Gokulashtami !

to all the readers, authors, subscribers etc.

onlinetaxupdate team wish to express sincere thanks to all the readers, authors, subscribers for the support extended to us. A special thanks to authors mentioned below for contributing their article for this 100th newsletter.

|

- Mr. CA Bimal Jain

- Mr. CA Nitin Bhuta

- Shri Seethapati Rao

- Mr. Rameshchandra Jena

- Mr. M.S. Vijayakumar

- Mr. Akshay Hiregange

- Ms. Aanchal Kapoor

- Mr. CA Nihal Jain

|

|

|

Dear Reader,

|

Please find newsletter for your reading and reference.

|

|

Newsletter no.100 dated 07.09.2023

|

|

|

Index of the Newsletter

- Recent updates

- GST in media

- Article

- Lawgics by Ms. Nidhi Aggarwal

- GST notes by CMA Anil Sharma

|

|

|

|

|

|

|

Press release ID 2279424 dated 30.06.26

|

The Government had earlier provided a full Customs Duty exemption on imports of critical petrochemical products till 30th June 2026, as a temporary and targeted relief in view of the conflict in West Asia and the consequent disruptions in global supply chains.

|

The exemption was provided to ensure sufficient availability of petrochemicals in the domestic market as Indian petroleum companies had been asked to concentrate on the production of LPG during this period. As the situation is gradually normalizing, to ensure a smooth and non-disruptive transition for the affected sectors, it has been decided to extend the said exemption by a further period of 15 days, that is, till 15th July 2026.The list of products covered remains the same as notified earlier.

|

The Government remains committed to supporting India's manufacturing sector. As before, the exemption is expected to benefit a wide range of sectors dependent on petrochemical feedstock and intermediates, including plastics, packaging, textiles, pharmaceuticals, chemicals, automotive components and other manufacturing segments. This will also provide relief to consumers of final products.

|

Link to previous press note issued:

|

|

|

|

|

|

|

|

Press release ID 2279409 dated 30.06.2026

|

|

In a major operation the officers of the Directorate of Revenue Intelligence (DRI) successfully dismantled a trans-border gold smuggling syndicate and seized 15 kg foreign-origin smuggled gold, valued at approximately Rs. 21.40 crore, operating from Delhi.

|

|

|

DRI officers intercepted an international courier consignment originating from Thailand at Courier Terminal, Delhi. The consignment was in the name of a firm linked to a foreign national.

|

A meticulous examination of the consignment declared as "worn gear", led to the recovery of eight disc-shaped pieces of foreign-origin gold, each weighing 1.5 kg, ingeniously concealed inside gear parts. In total, 12 kg smuggled foreign-origin gold was recovered from the courier consignment.

|

Simultaneous searches conducted at the residence of the intended recipient and the alleged mastermind resulted in the recovery of two more identical disc-shaped pieces of foreign-origin gold, each weighing 1.5 kg.

|

Four persons, including the mastermind, who is a repeat offender, and a foreign national have been arrested in relation with the case.

|

Preliminary investigations also reveal that crypto-currency was being used to transfer the money across borders to finance the smuggling.

|

|

|

|

|

|

|

|

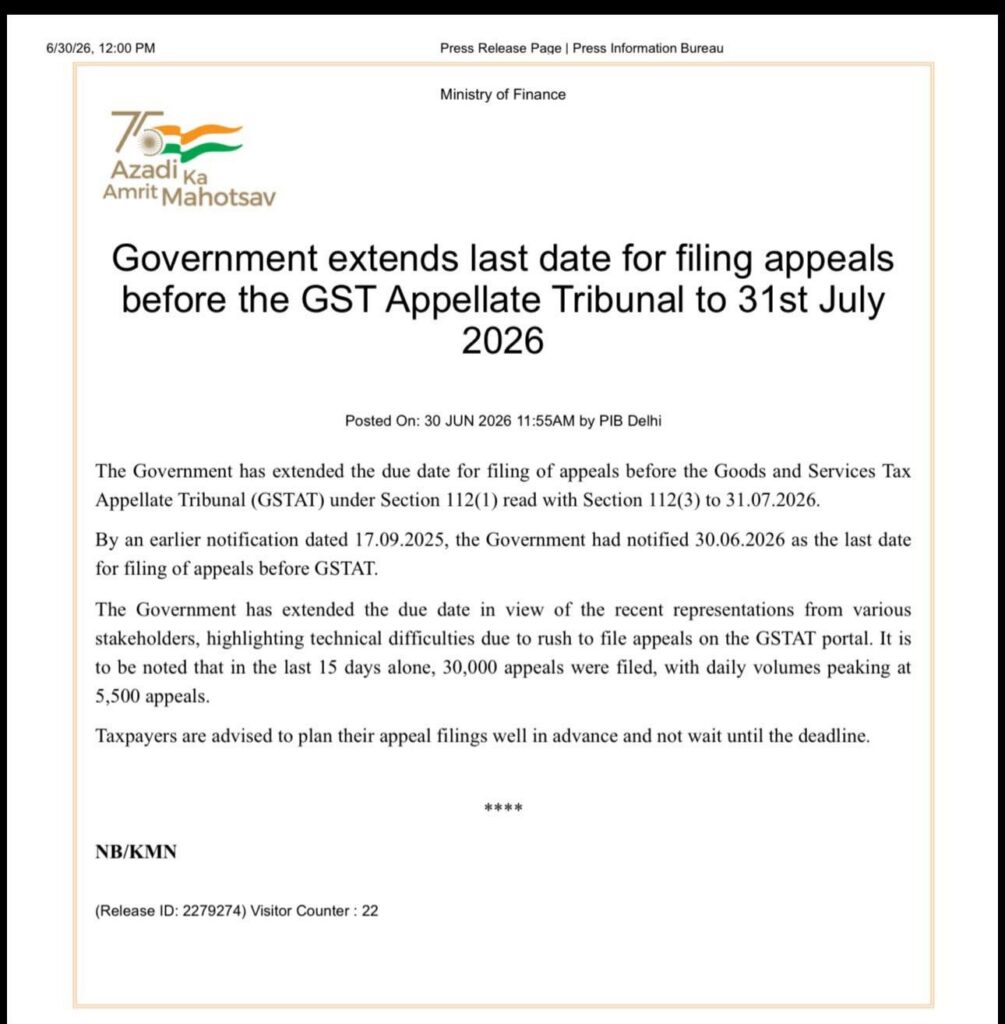

Source: Press release id 2279274 dated 30.06.26

|

The government has extended the due date for filing of appeal before the Goods and Services Tax Appellate Tribunal (GSTAT) under section 112(1) read with section 112(3) to 31.07.2026.

|

The government has extended the due date in view of the recent representation from various stakeholders , highlighting technical difficulties due to rush to file appeals on the GSTAT portal. It is to be noted that in the last 15 days alone, 30,000 appeals were filed, with daily volumes peaking at 5,500 appeals.

|

|

Taxpayers are advised to plan their appeal filings well in advance and not wait until the deadline.

|

|

|

|

|

|

|

|

|

|

|

Press release ID 2278205 dated 26.06.26

|

|

In a major crackdown against smuggling of foreign origin gold, the the Directorate of Revenue Intelligence (DRI) has successfully unearthed and dismantled a highly organised gold smuggling syndicate operating through Mumbai Airport. In this operation DRI detected and busted gold melting facility that was being used for melting of foreign origin smuggled gold.

|

|

|

Seized gold from melting facility in Mumbai

|

A total of nine persons involved across the entire smuggling chain, including the airport staff, her handler, three intermediaries, the melting facility operator, and three persons engaged in the melting process have been arrested. Further, about 6 kg foreign-origin smuggled gold recovered at the spot has been seized.

|

|

This case underscores the evolving sophistication of organised gold smuggling syndicates, which increasingly exploit insider access at airports and employ layered distribution networks to evade detection. In another operation at Bengaluru, DRI seized 1.8 kg 24 KT gold in paste form ingeniously concealed within the layers of garments of an international passenger. Subsequent follow up search at his residential premises led to seizure of around 1.5 kg gold jewellery, 45 kg silver, and Indian & foreign currencies. The person was arrested.

|

|

|

Gold in paste form concealed in undergarments; Seized at Bengaluru

|

|

earlier in this week, DRI has conducted a series of operations at other airports, railways station and land customs stations at Hyderabad, Rajkot, Calicut, Vishakhapatnam, Calicut, Guwahati and Petrapole, leading to the cumulative seizure of another 6 kg foreign-origin smuggled gold. Five persons have been arrested in these operations.

|

|

|

Overall, with busting of gold smuggling syndicate, these operations resulted in seizure of about 15 kg gold, 45 kg silver, valued at around Rs. 23 crore, and arrest of 15 persons.

|

|

|

|

|

|

|

|

GSTN is taking downtime to enhance its services on the GST Portal on 27.06.2026 from 12:00 AM onwards until 2:30 am of 27.06.2026.

|

|

We shall be enhancing services on the GST portal on : 27th June’26 12:00 AM onwards. GST Portal services will not be available until 27th June’26 02:30 AM. The inconvenience caused is regretted.

|

|

|

|

|

|

|

|

|

|

|

GSTN is taking downtime to enhance its services on the GST Portal on 12.06.2026 from 11:30 AM onwards until 7:30 am of 13.06.2026.

|

We shall be enhancing services on the GST portal on : 12th June’26 11:30 PM onwards. GST Portal services will not be available until 13th June’26 07:30 AM. The inconvenience caused is regretted.

|

|

|

|

|

|

|

|

GSTN Advisory no. 664 dated 17.06.2026

|

Reference is invited to the GSTN Advisory dated 20.05.2026 regarding enhancements in the e-Way Bill system, wherein it was informed that “Ship-to GSTIN” shall be mandatorily captured in Bill-to/Ship-to transactions. It was also clarified that where the consignee is an unregistered person, the value “URP” shall be entered in the Ship-to GSTIN field.

|

In this regard, representations have been received from trade, ERP vendors, GSPs, ASPs, private IRPs and other stakeholders seeking clarification on the applicability of the said requirement in cases where e-Way Bill is generated along with e-Invoice or by using IRN. Representations have also been received regarding the Voluntary Closure of e-Way Bill facility and its impact on portal-based and API-based operations.Accordingly, an advisory has been issued to apprise stakeholders of the corresponding changes introduced in the e-Invoice API, e-Way Bill by IRN API and EWB Closure API. It has also been informed that the aforesaid changes have been made available in the Sandbox environment for testing and system preparedness. The changes are scheduled to be implemented in the Production environment with effect from 1st August, 2026.

|

All concerned stakeholders may accordingly be advised to access the advisory through the link given below and undertake necessary testing, system changes and preparedness within the prescribed timeline.

|

|

|

|

|

|

|

|

|

|

Centre has extended the last date for filing appeals before the Goods and Services Tax Appellate Tribunal (GSTAT) to July 31, 2026, giving taxpayers an additional month to submit their cases after a surge in filings led to technical difficulties on the GSTAT portal.

|

The extension applies to appeals filed under Section 112(1) read with Section 112(3) of the Goods and Services Tax (GST) law.

|

The revised deadline replaces the earlier cut-off of June 30, 2026, which had been notified by the government on September 17, 2025.

|

The decision follows recent representations from various stakeholders who flagged technical issues arising from a rush of appeals being filed on the GSTAT portal ahead of the deadline.

|

While noting that the original due date had been notified well in advance in September 2025, the government said filing activity had intensified sharply in recent weeks. It said 30,000 appeals were filed in the last 15 days alone, with daily filings touching a peak of 5,500 appeals.

|

Advising against eleventh-hour filings, the government urged taxpayers to complete their appeal submissions well in advance to ease pressure on the GSTAT portal.

|

The GST Appellate Tribunal serves as the first judicial appellate forum for taxpayers seeking to challenge orders issued by GST authorities after the disposal of their first appeals.

|

Source: The Economic Times

|

|

|

|

|

|

|

|

|

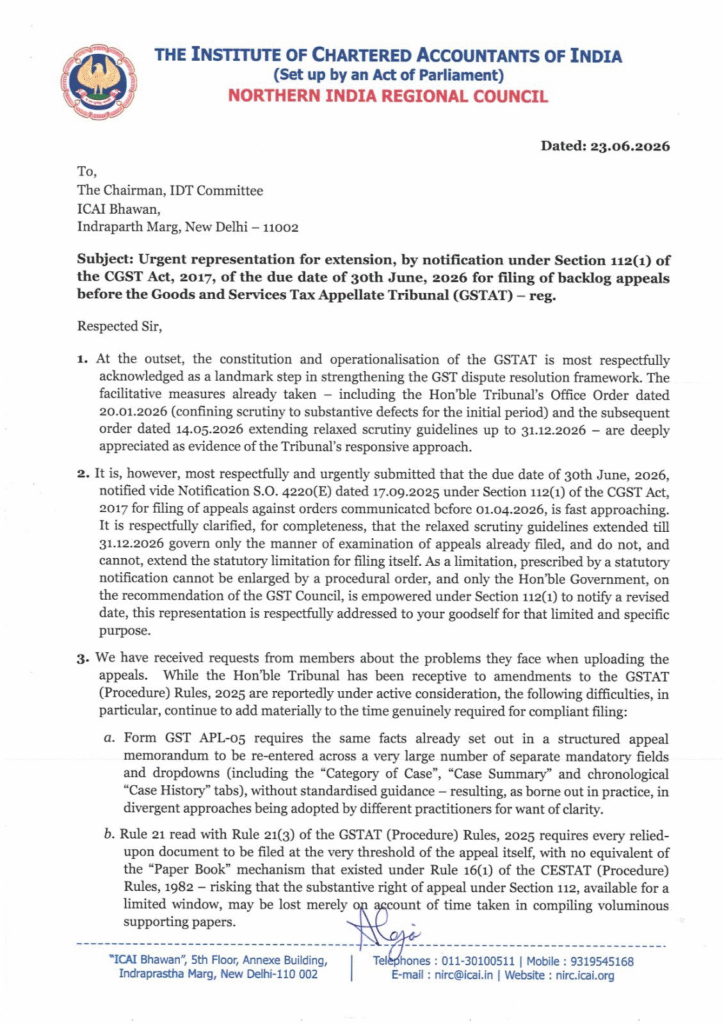

GST & IDT Committee has requested the Chairman, IDT Committee, ICAI, New Delhi to urgently represent before the respective forums for the date extension of GSTAT, i.e., 30-Jun-2026.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Tata Steel Limited said tax authorities have filed an appeal seeking restoration of penalties worth Rs. 368.72 crore that were earlier dropped in a GST adjudication order, even as proceedings on the underlying demand remain stayed by the Jharkhand High Court, according to a stock exchange filing.

|

"One June 16, 2026, the Assistant Commissioner, Division-I, CGST & Central Excise , Jamshedpur, Jharkhand filed an appeal before the Commissioner (Appeals) of CGST & Central Excise, Ranchi against the above-mentioned Adjudication Order dated December 18, 2026, to the extend that the Adjudicating Authority has dropped the penalty amounting to Rs. 3,68,72,21,158/-," Tata Steel said in its exchange filing.

|

The appeal, filed on June 16 by the Assistant Commissioner, CGST & Central Excise, Jamshedpur, challenges the December 18, 2025, adjudication order to the extent it waived the penalty.

|

The original show-cause notice, issued in June 2025, proposed disallowance of input tax credit for FY 2018-19 to FY 2022-23, with an aggregate GST demand of about Rs. 1,007.55 crore. Of this, Tata Steel said it has already paid Rs. 514.19 crore in the normal course, leaving an alleged exposure of Rs. 493.35 crore.

|

In December 2025, the adjudicating authority confirmed the tax demand of Rs. 493.35 crore, imposed a penalty of Rs. 638.83 crore and applicable interested, while dropping an earlier proposed penalty of Rs. 368.72 crore. Tata Steel subsequently moved the Jharkhand High Court, which granted a stay on all further proceedings in March 2026.

|

"This matter is, inter-alia, contingent upon the final adjudication of the issue concerning the issuance of show cause notices for multiple periods, which is presently sub judice before the High Court," Tata Steel said.

|

Tata Steel added that it has a good case on merit and hence will contest the same before the Appellate Authority within the statutory timelines, noting that the development has no impact on its financial or operational position, arising from the said appeal.

|

Source: The Economic Times

|

|

|

|

|

|

|

|

With the June 30 deadline for filing legacy appeals before the Goods and Services Tax Appellate Tribunal (GSTAT) fast approaching , tax professionals, chartered accountants and industry bodies have urged the Finance Ministry to extend the filing window, warning that persistent technical glitches on the GSTAT portal could prevent thousands of taxpayers from filing their appeals before the deadline.

|

The demand comes as taxpayers seek to file appeals arising from nearly nine years of litigation accumulated during the period when the Tribunal remained non-operational. Experts said the combination of a massive backlog, voluminous documentation and continuing portal-related issues has significantly constrained taxpayers' ability to meet the deadline.

|

According to Aditya Singhania, Founder of Trackase, the backlog is estimated at nearly four lakh to 4.5 lakh legacy appeals, while only around 36,929 appeals have been filed nationalwide so far.

|

"The ground reality is deeply concerning. Against an anticipated backlog of nearly four to four and a half lakh appeals accumulated over nine years of the Tribunal's non-operationality, only around 36,929 appeals have been filed nationally as of now," Singhania said.

|

He attributed the slow pace of filings to the teething troubles of the newly launched e-filing portal, including server time-outs, authentication challenges, payment gateway reconciliation issues and a filing structure that requires considerable time and effort to navigate.

|

Experts cite portal hurdles, record backlog

According to experts and representations submitted to the Finance Ministry, taxpayers continue to face multiple technical issues on the GSTAT portal, including session expiry, repeated login failures., Aadhaar authentication problems, Digital Signature Certificate (DSC) validation failures, payment reconciliation delays and incomplete integration between the Goods and Services Tax Network (GSTN) and the GSTAT portal.

|

Experts said taxpayers are also required to retrieve and compile extensive records accumulated over several years, including adjudication orders, invoices, reconciliations, e-way bills, ledger extracts and other supporting documents, making the filing process particularly time-consuming.

|

CA Nitin Bansal, State-President, BJP CA Cell Haryana, said the Finance Ministry has received several representations highlighting the practical challenges taxpayers are facing in filing appeals before the Tribunal.

|

"With the Tribunal becoming operational after nearly nine years, taxpayers must now prepare and file a substantial backlog of appeals within a limited window, many involving voluminous, multi-year records, even as the GSTAT e-filing portal continues to stabilise," Bansal said.

|

He added that extending the deadline would be revenue-neutral as the mandatory pre-deposit and other conditions would remain unchanged while ensuring genuine taxpayers are not denied their appellate remedy because of circumstances beyond their control.

|

Over-time extension sought

CA Sonu Goel, Chairman, Panipat Branch of the Institute of Chartered Accountants of India (ICAI), said a one-time extension would ensure disputes are decided on their merits rather than procedural constrints.

|

"One-time extension would safeguard taxpayers' right to appeal, uphold the principles of natural justice, and ensure that dispute are decided on merits rather than being defeated by procedural or technological constraints. This pragmatic relief would further reinforce the Government's commitment to ease of doing business while maintaining certainty and confidence in the GST ecosystem," Goel said.

|

Parag Mehta, Partner at N.A. Shah Associates LLP, said the portal continues to experience issues ranging from login failures and incorrect fee calculations to disappearing data.

|

"Considering the fact that the portal is not fully supporting the filing process and the number of appeals filed remains significantly lower than expected, the deadline should be extended. GSTAT is an important appellate remedy and taxpayers should not be deprived of that opportunity," Mehta said.

|

Bas association flags nationwide concerns

The Sales Tax Bar Association has also written to the Finance Ministry seeking an extension of the filing deadline, stating that taxpayers and tax professional across the country continue to face significant practical and technical difficulties while filing appeals through the GSTAT portal.

|

In its representation, the association said the present limitation period covers appellate orders accumulated over nearly nine years when the Tribunal remained non-functional, requiring taxpayers to retrieve historical records and prepare detailed documentation within a limited period.

|

The association highlighted recurring issues including server interruptions, repeated Aadhaar authentication and DSC validation failures, payment gateway reconciliation delays, manual duplication of information already available on the GSTN portal and challenges in uploading voluminous records.

|

It warned that if the deadline is not extended, thousands of taxpayers could lose the opportunity to pursue their statutory appeals because of technological and procedural constraints, potentially leading to avoidable litigation before various High Courts.

|

Prabhat Ranjan, Senior Director at Nexdigm, said extending the filing deadline has become "the need of the hour".

|

"The appellate process should be about the actual merits of the issues between both parties and not technical questions of delay. This is a taxpayer-friendly measure that will make GST dispute resolution processes more fair and credible," he said.

|

As of publication, the government has not announced any extension of the June 30 deadline for filing legacy GSTAT appeals. While the GSTAT has extended the period for relaxed scrutiny of filed appeals until December 31, 2026 , tax professionals, industry experts and representative bodies continue to seek a one-time extension of the filing deadline, arguing that additional time would enable taxpayers to exercise their statutory right of appeal without affecting revenue, as the mandatory pre-deposit requirements would continue to apply.

|

Source: The Economic Times

|

|

|

|

|

|

|

|

Businesses shifting their principal place of business to a new GST jurisdiction will not have to restart pending tax proceedings with the Central Board of Indirect Taxes and Customs (CBIC) clarifying that the new jurisdictional authority will take over and complete all ongoing cases from the stage at which they were left, reported PTI.

|

The clarification comes after the CBIC received references from field formations seeking guidance on the validity of proceedings and the authority responsible for handling cases when a registered taxpayer changes jurisdiction because of a shift in its principal place of business.

|

Under the circular, any action or proceeding - including investigation, audit, show cause notice or adjudication under the Central GST law - initiated by the tax officer having jurisdiction over the registered taxpayer at the time the action was undertaken (transferor jurisdiction authority) will remain valid even if the taxpayer subsequently shifts to another tax jurisdiction (transferee jurisdictional authority).

|

"The transferee jurisdictional authority shall act upon, give effect to, and proceed on the basis of such earlier valid action taken by the transferor jurisdictional authority, as if it had itself initiated the same," the CBIC said in the circular.

|

The indirect tax board further clarified that if any fresh issue comes to the notice of the earlier jurisdictional authority after the taxpayer has shifted, the tax officer should intimate the new jurisdictional officer for appropriate action.

|

"Where the taxable person migrates to another jurisdiction during the pendency of any action or proceeding initiated by the transferor jurisdictional authority, the transferee jurisdictional authority shall take over and conclude the same from the stage at which it stood at the time of migration/ transfer," the CBIC circular said.

|

The new jurisdictional officer will also have the authority to initiate and conclude any consequential proceedings arising from the case.

|

Rajat Mohan, Managing Partner at AMRG Global, said the clarification addresses a key procedural gap under the GST regime.

|

"By clearly defining the responsibilities of transferor and transferee authorities, CBIC has removed ambiguity that often resulted in jurisdictional objections and delays in adjudication," Mohan said.

|

Source: The Times of India

|

|

|

|

|

|

|

|

On the occasion of 9th GST Day to be celebrated on 1st July, 2026 the Central Board of Indirect Taxes and Customs vide Office Memorandum dated 29.06.2026 has decided to grant Certificate of Meritorious Service (CBIC-CMS) to the following officers:

|

|

|

|

|

|

|

|

The Malad Chamber of Tax Consultants made a representation to the Hon'ble Union Finance Minister, Smt. Nirmala Sitharaman, New Delhi on 26.06.2026 requesting an extension of the statutory deadline for filing GSTAT appeals under Section 112 of the CGST Act, 2017 from 30th June 2026 to 31st December 2026.

|

|

|

|

|

|

|

|

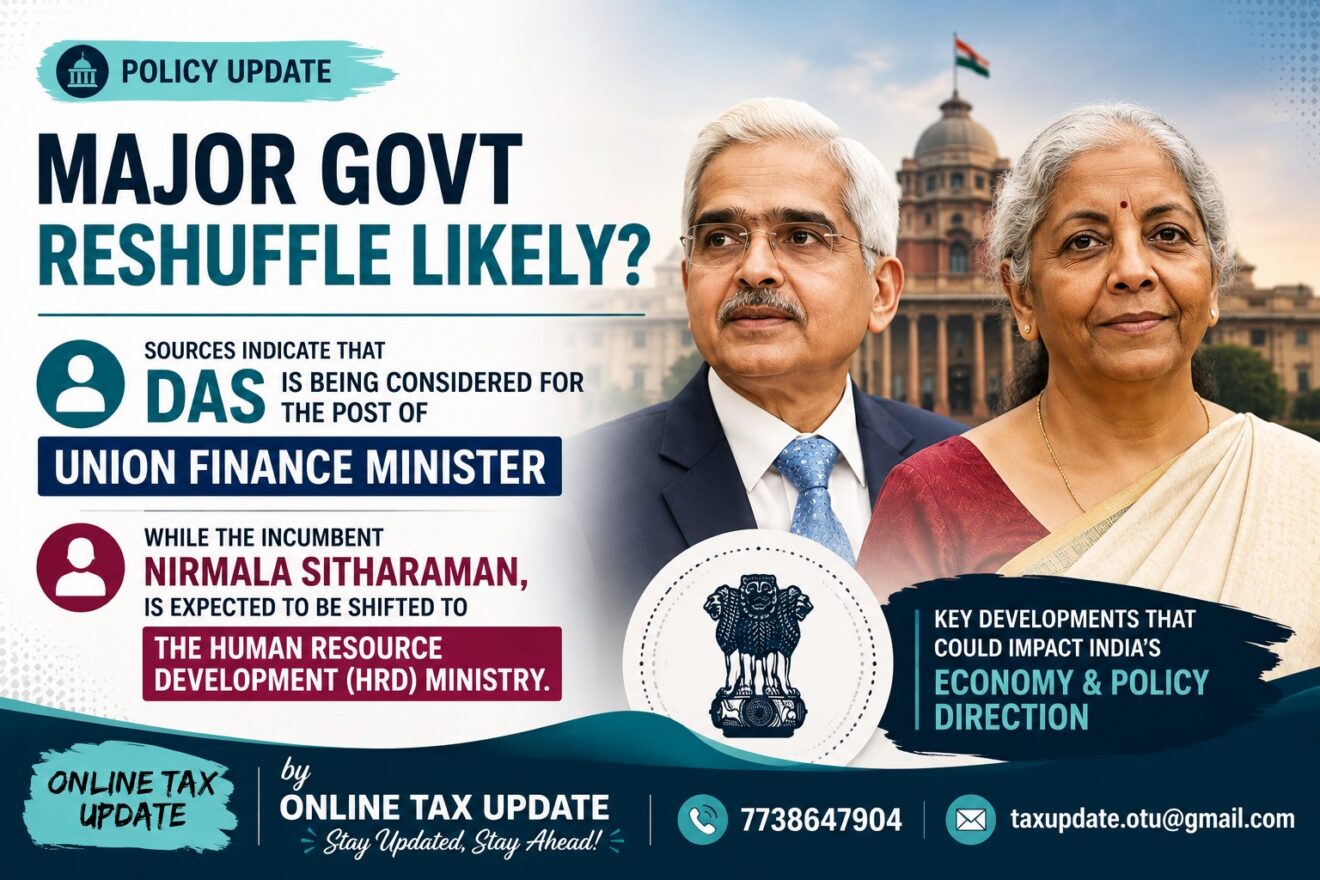

The recent meeting between Prime Minister Narendra Modi and President Droupadi Murmu, followed by a meeting between Home Minister Amit Shah and the President, have fuelled speculation over a possible Union cabinet reshuffle as well as changes in the BJP's organisational structure.

|

According to sources, the reshuffle is likely to take place before the upcoming Monsoon Session of Parliament.

|

Among the names being discussed is that of former Reserve Bank of India (RBI) governor Shaktikanta Das, who is currently serving as the Principal Secretary to the Prime Minister.

|

Sources indicated that Das is being considered for the post of Union finance minister, while the incumbent , Nirmala Sitharaman, is expected to be shifted to the human resource development (HRD) ministry. Sitharaman has been serving as the Union Minister for finance and corporate affairs since 2019.

|

There has, however, been no official confirmation from either the government or the BJP regarding any proposed changes.

|

If the move materialises, it would bring into the Cabinet a seasoned administrator with more than four decades of experience across several areas of governance.

|

Das served as the 25th Governor of the RBI from 2018 to 2024. Before assuming charge at the RBI, he was a member of the 15th Finance Commission and India's G20 Sherpa.

|

Over the course of his career, Das has held several key positions in both the Central and State governments, handling portfolios related to finance, taxation and industries and infrastructure.

|

During his tenure in the finance ministry, he was closely associated with the preparation of eight Union Budgets, giving him extensive experience in public finance and economic policymaking. Besides, Das was also the senior Department of Economic Affairs official in the finance ministry during the planning and implementation phase of demonetisation.

|

A postgraduate from St. Stephen's College, University of Delhi, Das has also served as India's Alternate Governor to the World Bank, the Asian Development Bank, the New Development Bank, and the Asian Infrastructure Investment Bank. He has represented India at major international forums, including the IMF, G20, BRICS, and SAARC.

|

|

|

|

|

|

|

|

Kolkata is likely to host the 57th meeting of the GST Council next month, sources said, although the Union Finance Ministry has not yet officially confirmed the venue or the schedule. The meeting is expected to be held in the second half of July, and could take up the next round of indirect tax policy reforms.

|

Hosting the meeting in Kolkata holds significance as it would mark one of the first major meetings of a Constitutional federal body in West Bengal after the Assembly elections. While the GST Council independently decides its agenda and meeting schedule, the choice of Kolkata would coincide with the Centre’s broader emphasis on strengthening the State’s profile as a destination for investment and financial activity following the change in government.

|

New reforms

The previous GST Council meeting, held on September 3, 2025, came after a gap of nearly nine months, despite the rules providing for at least one meeting every quarter. That meeting unveiled GST 2.0, including rate rationalisation and measures to ease compliance. Tax experts now expect the council to consider another set of policy reforms, some of which were discussed during 4th Annual Seminar on Direct and Indirect Taxes of the Bengal Chamber of Commerce & Industry (BCCI).

|

Vivek Jalan, Chairperson of the National Fiscal Affairs and Taxation Committee of BCCI, said that in the spirit of GST 2.0, which was launched to strengthen India’s manufacturing base, the council should correct the anomaly of non‑refund of Input Service ITC under the inverted duty structure. While GST 2.0’s rate rationalisation has supported consumption, the cost pressures has deepened on manufacturers. “Addressing this gap will ensure reducing cascading taxes, boosting competitiveness and advancing India’s vision of becoming the world’s third‑largest economy by 2047,” he said.

|

Also, it has been proposed before the GST Council to consider reducing the GST rate on autism care centres and allied sectors from 18 per cent to 5 per cent. Such a measure under GST would ease the financial strain on families and institutions, while reinforcing the government’s vision of inclusive growth. “By aligning tax policy with compassion, the council can ensure that essential services for differently‑abled children remain affordable, accessible and sustainable, a step that truly reflects the spirit of GST reforms,” said Jalan.

|

Source: The Hindu businesline

|

|

|

|

|

|

|

|

The Karnataka State Chartered Accountants Association (R) (KSCAA) has submitted a representation highlighting practical and procedural issues faced by taxpayers and professionals in relation to the Goods and Services Tax Appellate Tribunal (GSTAT). The representation focuses on addressing operational challenges and suggesting measures to enhance the efficiency, accessibility, and effectiveness of the GSTAT framework.

|

Considering the initial challenges faced by stakeholders in adapting to the newly operational GSTAT framework and portal, KSCAA has also requested an extension of the timelines for filing appeals and related compliances, so that taxpayers are not prejudiced on account of procedural and technical difficulties. Addressing these concerns and providing adequate transition time will facilitate smoother implementation, reduce avoidable litigation, and ensure meaningful access to the appellate remedy envisaged under the GST law.

|

|

|

|

|

|

|

|

Nine years after the rollout of the goods and services tax (GST) regime, businesses have largely embraced India's biggest indirect tax reform, with 99% reporting a positive or neutral experience, according to a Deloitte India survey. As the tax regime matures, businesses are now shifting their focus to ‘GST 2.0’, seeking reducing disputes, speeding up of refunds, improving working capital and simplifying compliance.

|

The findings come at a time when GST collections continue to be robust. In May, the Centre and states together collected ₹1.94 trillion in gross GST revenue, before adjusting for refunds, up 3.2% from ₹1.88 trillion mopped up a year ago.

|

The survey covered 1,096 C-suite and C-1 level executives across banking and financial services, consumer, energy, resources and industrials, government and public services, life sciences and healthcare, global capability centres, private equity and venture capital, and technology, media and telecommunications. Respondents included micro small and medium enterprises (MSMEs), large companies and very large enterprises.

|

About 69% respondents identified compliance digitalization as the biggest benefit of GST, followed by supply chain optimization and gains from rate rationalization. The survey noted that confidence in GST has been driven by the digitalization of compliance, automation of tax processes and the stabilization of e-invoicing and e-way bill systems.

|

"GST has significantly improved compliance and transparency with the GST Network as India's trusted tax framework. This digital backbone enables taxpayers, businesses and the government with real-time compliance and data-driven decision-making," said Gokul Chaudhri, president, tax at Deloitte South Asia.

|

Businesses ranked interpretational clarity as their top policy priority, with 87% of the respondents seeking greater certainty in tax administration. This was followed by demands for improved working capital management (67%), uniform audits (61%) and faster refunds.

|

The survey also found strong support for centralized audits, simplified GST rates and allowing reverse-charge mechanism payments through input tax credit.

|

"The key industry expectations include the need to resolve interpretational ambiguities, improve working capital through streamlined refunds and credit utilization, address ITC disputes and implement a unified and harmonized audit process," said Mahesh Jaising, partner and leader, indirect tax at Deloitte India.

|

Addressing inverted duty structures emerged as another major area of concern. Nearly 69% of respondents favoured expanding the refund formula to include all input taxes, while 63% supported further rate rationalization to reduce inversion-related issues. More than half sought refund benefits for accumulated input tax credit balances.

|

Technology is expected to play a bigger role in the next phase of GST reforms. Nearly 89% of respondents supported the use of artificial intelligence (AI) for tax data processing and reconciliation, while many sought a unified taxpayer dashboard, automatic tax utilization and improved integration across GST systems.

|

The survey found that priorities varied across sectors. Consumer and energy firms highlighted supply-chain optimization as the biggest gain from GST, while technology companies placed greater emphasis on compliance digitalization. Life sciences and healthcare companies cited benefits from competitive pricing following rate rationalization, while BFSI and global capability centres favoured greater automation and integrated digital infrastructure.

|

For MSMEs, quarterly return filing emerged as the most appreciated reform, with positive responses rising to 67% in 2026 from 12% in 2023. Smaller businesses also strongly supported invoice-based input tax credit eligibility, quarterly payment mechanisms and faster refunds to ease liquidity pressures, the survey said.

|

Some economists underscored the need for a more efficient refund mechanism under GST.

|

“Faster and more predictable GST refunds are critical for improving business cash flows. Delays in refunds increase working capital requirements and financing costs," said Dharmveer, assistant professor, economics at the Delhi School of Economics. "A more streamlined refund mechanism would enhance liquidity, especially for MSMEs and exporters, and support investment and growth.”

|

GST was introduced on 1 July 2017 as India's biggest indirect tax reform, replacing multiple central and state taxes with a single tax system. Since then, the regime has evolved with the rollout of e-invoicing, e-way bills and other digital compliance measures aimed at making tax administration easier and more transparent.

|

|

|

|

|

|

|

|

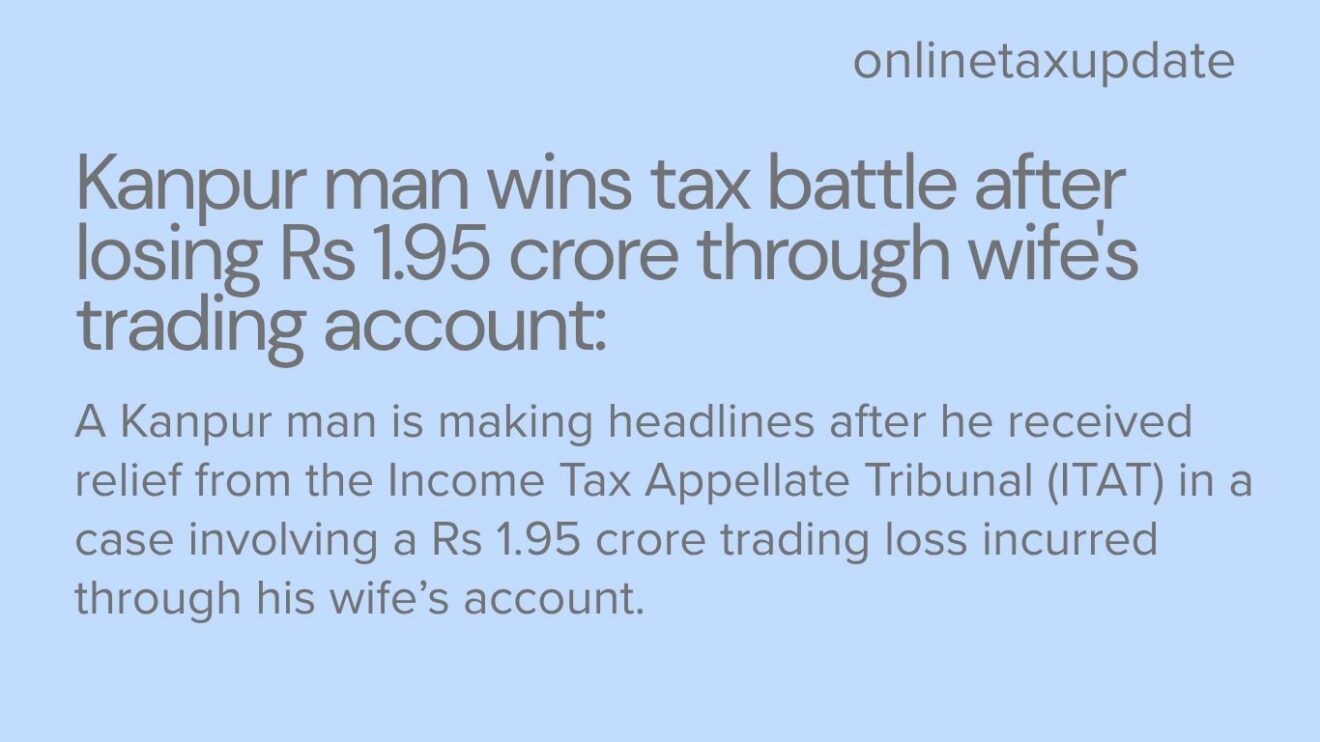

A Kanpur man is making headlines after he received relief from the Income Tax Appellate Tribunal (ITAT) in a case involving a Rs 1.95 crore trading loss incurred through his wife’s account.

|

According to The Economic Times, the man, whose identity remains undisclosed, transferred funds to his wife's account and used it to carry out Futures and Options (F&O) trading. The transactions resulted in a loss of Rs 1.95 crore during the financial year. When filing his income tax return, he reported the loss on his own return and adjusted it against his income.

|

However, the Income Tax Department challenged the claim and raised a tax demand, stating that the loss belonged to his wife's account and therefore could not be adjusted against the husband's income.

|

The dispute eventually reached the ITAT's Lucknow Bench. After examining the facts, the tribunal found that the husband had transferred funds to his wife's account, and that he carried out the trading through his wife's account, and the loss occurred there.

|

The tribunal pointed out that, under the Income Tax Act’s clubbing rules, income generated from assets gifted or transferred to a spouse is typically included in the transferor’s income.

|

|

|

|

|

|

|

|

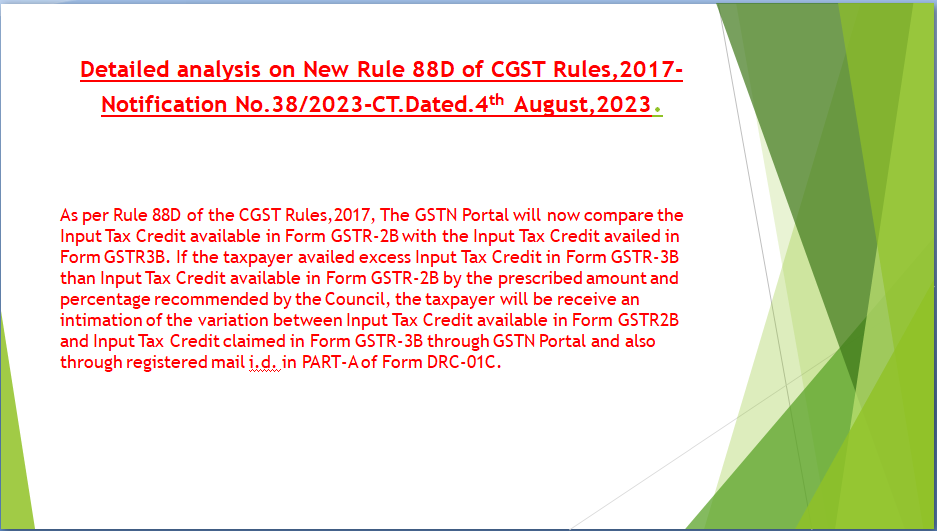

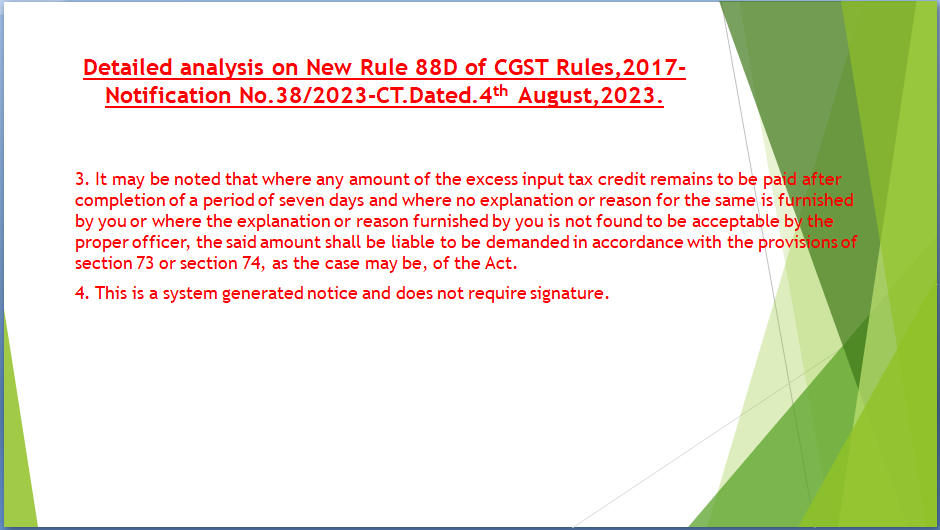

Recent changes in GST Rules has been captured in the slides format by the author.

|

|

Author: CA Nihalchand J Jain

|

|

|

|

|

|

|

|

|

|

Clause 44 in Form 3CD under Section 44AB of the Income Tax Act 1961.– Updated FAQs

|

(Note: Views expressed are my personal views and they are based on my understanding of the subject as dealt by this article and views shared may be acceptable or may not be acceptable to the readers of this article. All readers are requested to take their considered views based on their own study to reach any suitable conclusions. There can be many other situations under the law but through this article I have tried to sow the seed of thought in the minds of readers. Suggestions to improve the article are always welcome with folded hands).

|

|

Table 1- Clause 44 – GST Reporting Information

|

|

|

|

Table 2- Clause 44 – GST Reporting Information – Detailed

|

|

|

|

|

|

|

|

|

|

|

|

|

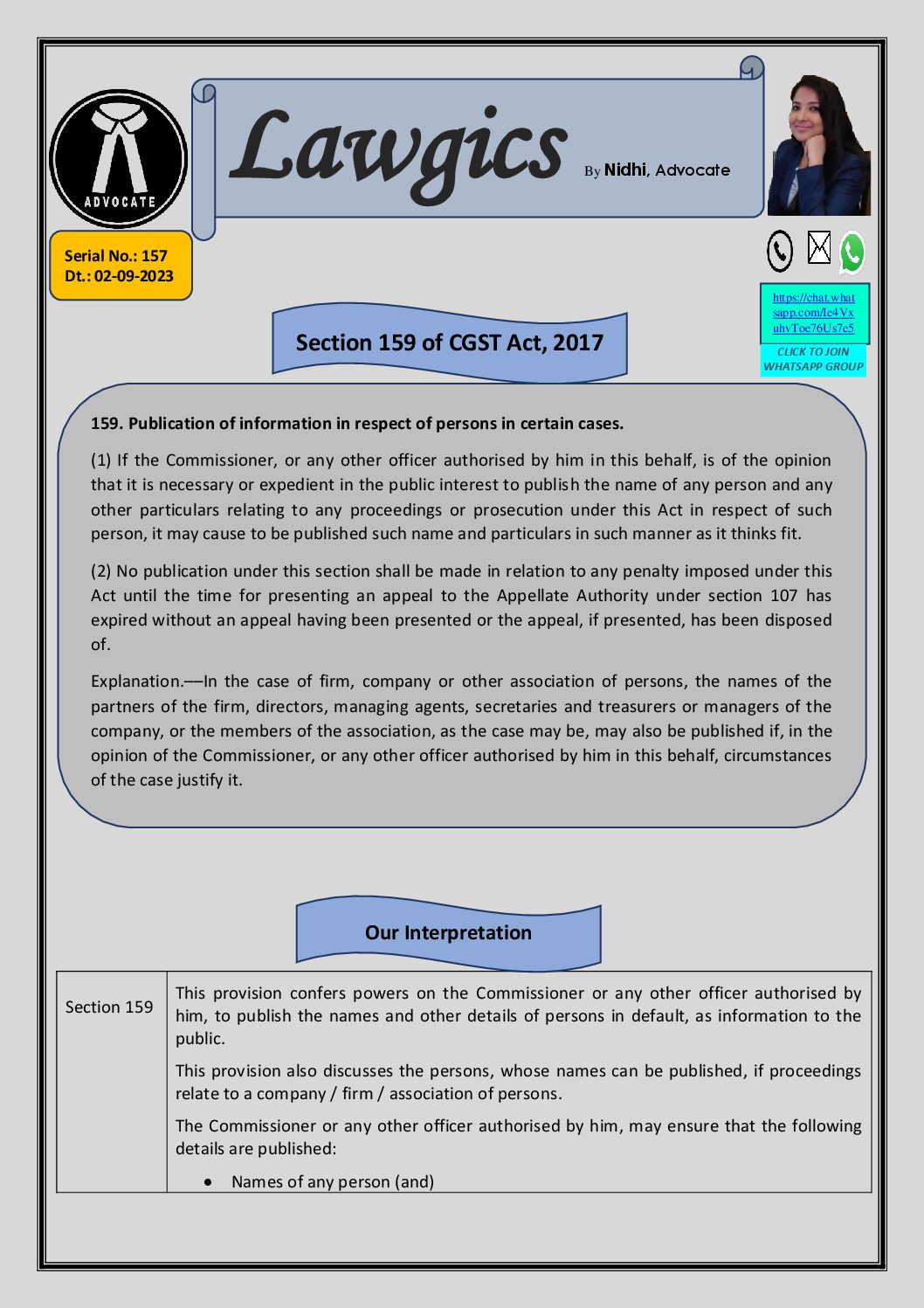

Provisional attachment of property including Bank account of a taxable person to protect Government revenue in certain cases has been prescribed under Section 83 of the CGST Act, 2017 read with Rule 159 of the CGST Rules, 2017. The adjudicating authority initiate the recovery of tax during pendency of any proceedings under Section 59 to 64 of the CGST Act, 2017, Section 67 to 72 of the CGST Act, 2017 & Section 73 / Section 74 of the CGST Act, 2017 by way of provisional attachment of property including bank account.

|

Statutory provisions for attachment of Bank Account:

|

Section 83 of the CGST Act empowers the Commissioner to provisionally attach the any property including bank account belonging to a taxable person or any person specified in sub-section (1A) of section 122 of the CGST Act. The attachment can be made where, after initiation of any proceedings, the Commissioner is of the opinion that for the purpose of protecting the interest of the Government revenue.

|

No attachment of property can be initiated by the proper officer unless an order in FORM GST DRC-22 pass by the Commissioner under Rule 159 of the CGST Rules, 2017 read with Section 83 of the CGST Act, 2017. Rule 159(6) of the CGST Act, the Commissioner may, upon being satisfied that the property was or is no longer liable for attachment, release such property by issuing an order in FORM GST DRC-23.

|

Provisional attachment lapses after one year:

|

Section 83 (2) of the CGST Act, provides that every provisional attachment shall cease to have effect after the expiry of a period of one year from the date of order made under sub-section (1) of section 83 of the CGST Act,2017.

|

The Hon’ble Supreme Court in the case of Radha Krishan Industries vs. State of Himachal Pradesh, reported in 2021 (48) G.S.T.L113 (S.C), held that the Provisional attachment is draconian power exercised before finalization of assessment or raising of demand It has to be exercised with due caution. It is provisional as in aid of something else and its purpose is to protect revenue. Its validity depends on strict observance of statutory pre-conditions. Formation of Commissioner’s opinion must have proximate and live nexus to protection of revenue interest and it is not left to unguided subjective discretion. The Commissioner’s opinion must be based on tangible material regarding statutory requirements.

|

Therefore, the Hon’ble Supreme Court has issued the following mandatory guidelines to be followed while ordering for provisional attachment of property including bank account of the taxable person.

|

- The power to order a provisional attachment of the property of the taxable person including a bank account is draconian in nature and the conditions which are prescribed by the statute for a valid exercise of the power must be strictly fulfilled;

- The exercise of the power for ordering a provisional attachment must be preceded by the formation of an opinion by the Commissioner that it is necessary so to do for the purpose of protecting the interest of the government revenue. Before ordering a provisional attachment the Commissioner must form an opinion on the basis of tangible material that the assessee is likely to defeat the demand, if any, and that therefore, it is necessary so to do for the purpose of protecting the interest of the government revenue.

- The expression “necessary so to do for protecting the government revenue” implicates that the interests of the government revenue cannot be protected without ordering a provisional attachment;

- The formation of an opinion by the Commissioner under Section 83(1) must be based on tangible material bearing on the necessity of ordering a provisional attachment for the purpose of protecting the interest of the government revenue;

- In the facts of the present case, there was a clear non-application of mind by the Joint Commissioner to the provisions of Section 83, rendering the provisional attachment illegal;

- Under the provisions of Rule 159(5), the person whose property is attached is entitled to dual procedural safeguards :

(a) An entitlement to submit objections on the ground that the property was or is not liable to attachment; and

|

(b) An opportunity of being heard;

|

- The Commissioner is duty bound to deal with the objections to the attachment by passing a reasoned order which must be communicated to the taxable person whose property is attached;

- A final order having been passed under Section 74(9), the proceedings under Section 74 are no longer pending as a result of which the provisional attachment must come to an end.

The Hon’ble High Court of Madras in the case of Senior Intelligence officer, DGGI, vs. KPN Travels India Ltd, reported in 2021(49) G.S.T.L.338( Mad.), held that “In the considered view of this Court, an order of attachment of the first respondent’s bank account, which are stated to be 14 in number, should be for the purpose of protecting the interest of the Government Revenue and the Commissioner should be of the opinion, it is for such purposes and he is required to pass an order in writing attaching provisionally any property including bank account. The procedure is in terms of Rule 159 of the CGST Rules. Thus, if the first respondent is able to explain to the satisfaction of the officer that the provisional attachment is not warranted, it goes without saying that the Commissioner can exercise powers and lift the order of provisional attachment or otherwise confirm the provisional attachment. Admittedly, the investigation is yet to be completed and therefore, time is yet to come for issuance of show cause notice for recovery of alleged tax due or for that matter to crystallize the alleged liability, the first appellant shall consider and pass appropriate interim orders, if found tenable, considering the lifting of the provisional attachment in respect of a few bank accounts to enable the first respondent to carry on its business activities.”

|

The Hon’ble High Court of Bombay in the case of Chotu Lal vs. Union of India, reported in 2023 (72) G.S.T.L. 167(Bom), held that the petitioner to approach the concerned authority under Rule 159(5) of the GST Rules for revocation of the attachment, the authority will make endeavour to take a decision thereupon as per law, within three weeks of filing of such application for revocation of bank attachment.

|

The High Court of Madras in the case of Federal Bank Ltd, vs. Sub Registrar , reported in 2023(72) G.S.T.L.40 (Mad.), held that “Section 83(2) of GST Rule make it clear that every such provisional attachment shall cease to have effect after expiry of a period of one year from the date of the order made under sub-section(1),. Therefore, provisional attachment made by the second respondent vide order dated 18.12.2021 has ceased to have effect, after expiry of a period of one year. There is no material to show any final order of attachment, or any subsequent order passed by the second respondent pursuant to the aforesaid order. Therefore, this court is of view that the impugned order dated 17-10-2022 is liable to be quashed.

|

The Hon’ble High Court of Madras in the case of Sree Minakshi Industries vs. Commissioner of commercial tax, reported in 2022 (65) G.S.T.L. 457 (Mad.), held that” It is made clear that, this order, setting aside the provisional attachment order and the consequential bank communication in respect of these two cases, shall not stand in the way for the respondent/Revenue to invoke Section 83 once again, if they have reasons with tangible materials and records to form an opinion that in the interest of Revenue, such an invocation of Section 83 become inevitable and after recording such reasons that kind of invocation could be possible at the hands of the Revenue. Insofar as the assessment is concerned, it is open to the Revenue to complete the assessment at the earliest with utmost co-operation of the petitioners”

|

The Hon’ble High Court of Delhi in the case of Karmatji Jaiswal vs. Commissioner of Central Tax, reported in 2022(66) G.S.T.L. 333 ( Del.), held that Admittedly, every provisional order ceases to have effect after the expiry of a period of one year from the date of the order made under Section 83(1) of the CGST Act. After the issuance of the impugned orders, no fresh attachment order has been issued. Consequently, this Court directs the Respondent to defreeze the bank account and release the immovable properties of the Petitioner not later than three days from the date of uploading the order.

|

The Hon’ble High Court of Telangana in the case of Rahul Aggarwal vs. Commissioner of Central Tax, reported in 2022(64) G.S.T.L. 290 (Telangana), held that in the instant case, provisional attachment was ordered on 9-2-2021. Thus, the period of one year has expired. Though a statement has been made in the counter affidavit that the provisional attachment was reviewed by the Commissioner on 11-3-2022 where after such attachment for further period was approved, no such order has been placed on record. In any case, sub-section (2) of Section 83 of the CGST Act is very clear. Every provisional attachment made under sub-section (1) of Section 83 of the CGST Act shall cease to have effect after expiry of a period of one year from the date of the order made under sub-section (1) of Section 83 of the CGST Act. That being the position, we are of the considered opinion that continuance of the impugned order of provisional attachment dated 9-2-2021 cannot be sustained. The same is accordingly set aside and quashed. Respondents are directed to forthwith de-attach the aforesaid bank account of the petitioners. The Hon’ble High Court of Gujarat in the case of Mahavir Enterprise vs. State of Gujarat, reported in 2022(62) G.S.T.L.166 (Guj.) held that “The plain reading of the above referred provision would indicate that if any amount of tax, interest or penalty like the one in our case is payable by a person to the Government under

|

any of the provision of this Act or the Rule then such amount can be recovered by a proper Officer of State Tax or the Union Territory as the case may be, as if it were an arrear of State Tax or the Union Territory Tax. In other words, this provision can be interpreted or can be understood as recovery of any debts, interest or penalty by way of revenue measures. Its like recovery under the Bombay Land Revenue Code. This is possible or rather permissible only after proper attachment of any property of the assessee. This attachment which we are talking about has nothing to do with the provisional attachment under Section 83 of the Act. For the purpose of sub-clause (3), the attachment is permissible even under the provisions of the Bombay Land Revenue Code. In such circumstances referred to above, the impugned order of provisional attachment purported to have been passed under Section 83 of the Act could be said to be without jurisdiction. The same is hereby quashed and set aside. We leave it open to the respondents to initiate appropriate proceedings in accordance with law, if they intend to do so.”

|

The Hon’ble High Court of Orissa in the case of Shri Radha Raman Alloys Pvt.Ltd, vs. Union of India, reported in 2021(52) G.S.T.L.5 (Ori.), held that Rule 159 of the OGST Rules, 2017 sets out the procedure to be adopted for issuing a provisional attachment order. Under Rule 159(5) a person whose property is attached may, within seven days of such attachment, file an objection to the effect that the property attached was or is not liable to attachment. After such objection is filed, the Commissioner is required to offer the person objecting an opportunity of being heard and thereafter pass an appropriate order in FORM GST DRC-23, if he is of the view that the property is required to be released from attachment.

|

Conclusion: The provision of attachment property including bank account is the weapon in the hands of the adjudicating authority for recovery of revenue under Section 83 of the CGST Act, 2017, but it should be supported by judicious opinion of the Commissioner by issuance of Order in FORM GST DRC-22. Section 83 of the CGST Act, 2017 empowers the Commissioner to initiate proceeding of attachment property including bank account under Section 83 of the Act, if he satisfied that it is genuine reason and fit case of attachment of bank account of any registered person to protect the revenue of the Government. The Commissioner may authorize his subordinate officer to initiate proceedings of bank attachment giving an opportunity of heraing to the taxable person as per the direction of the Hon’ble Supreme Court decision in the case of Radha Krishan Industries (supra). The taxable person also an opportunity is available under Rule 159(5) of the CGST Rules, 2017 to approach the GST authority filing an objection application for the de-attachment of bank account in case he is not liable to pay any tax or his property is not liable for attachment.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Author: Subrahmanya Seethapathi Rao Bharatam

|

|

|

|

|

|

|

|

|

|

The Indirect tax regime in India provides for a complex tax environment due to multiplicity of taxes, complicated compliance obligations and tax cascading. Under the GST regime, all the key Indirect tax legislations would be subsumed except for few taxes such as duty on Electricity, Royalty on the extraction of minerals from mines, etc. In Goods and Service Tax Act the tax is levied on the supply of goods and supply of services which is different from the taxable events of the current regime that is manufactured, sale or provisions of service. The mineral sector in India is the most taxed among all countries with effective tax rate between 60%-64%, surpassing all other mining territories.

|

The minerals and mining sector in India is governed by the Mines Act, 1952 along with the Mines and Minerals Development and Regulation Act (MMDR), 1957. The mines and minerals development and regulation are undertaken as per the MMDR Act under the control of the union. As per Section 9 of the MMDR Act, 1957 the holder of a mining lease granted before or after the commencement of this act shall pay royalty in respect of any minerals removed or consumed. The Mines Act,1952 lays down the rules and regulation in relation to the safety of the labour, regulation for carrying out mining activities and the management of mines.

|

India currently produces around 89 minerals under different groups, with fuel minerals, metallic minerals, non-metallic minerals, atomic minerals and minor minerals. The country has immense potential for mining resources and reserves and is currently among the top 10 global producers of many minerals.

|

India's global position in mineral production

|

Taxation system on Mining

|

Under the GST regime, all the key Indirect tax legislations would be subsumed (except for few taxes such as duty on Electricity, Royalty on the extraction of minerals from mines, etc.).

|

|

As per Section 9 of the MMDR Act, 1957 the holder of a mining lease granted before or after the commencement of this act shall pay royalty in respect of any minerals removed or consumed.

|

|

|

whether royalty itself is in the nature of tax. This question fundamentally exerts influence on tax implications, which has been at stretch for a long time,as there cannot be levy of tax on tax which cannot be attached to the value of the goods/services. Although various judicial decisions are there and explored the matter's clear position in law, yet its tax implication still remains unclear with the taxpayers and the tax levying authority. The Supreme Court in India Cement Ltd. vs. State of Tamil Nadu case has held that royalty is not a tax and its payment is for the user of the land. Royalty on mineral rights is not a tax on land but a payment for the user of land. Although the intent and the missive were clear as set out in the judgement determining that royalty is a "tax" though not a "tax on land" as this was the question before them that whether Royalty is tax on land.

|

The mining sector incurs service tax and royalty as the procurement costs:

|

1. The mining companies may attract service tax for the services relevant to the mining industry such as exploration, mineral production, handling, transportation etc. A manufacturer and/or service provider paying service tax on procurement of services are allowed to take credit of same and it is set off against their Service tax or Excise liability. However, no credits are available to primary producers or miners, who are neither service providers nor manufacturers but simply a trader.

|

2. Exporters are allowed to claim a refund of tax paid on procurement in various forms.

|

3. Royalty on mining is collected by the State Government from the business entities in relation to the lease of the mines granted to them.

|

The Supreme Court, in India, Cement Ltd. v. State of Tamil Nadu and others (AIR 1990 SC 85) had held that royalty is a tax and its payment is for the use of land. The judgment had relied on the concept that royalty was attributed to the extracted mineral created due to interaction among land, capital and labour, each of which possesses some definite intrinsic economic value. In this sense, royalty was viewed as a kind of tax linked either directly or indirectly to the intrinsic economic value of a mineral realised through sale by the lessee. Though the Hon'ble Supreme Court subsequently doubted the correctness of the above referred judgements and referred the case as to “whether royalty is tax or not” to a larger bench of nine judges and the same is yet to be pronounced and therefore the judgement of India Cement Limited can be considered as the law as on date. If the Supreme Court decides that royalty is in nature of tax then both excise duty and service tax cannot be levied, since there cannot be taxed on tax.

|

a. The grant for the mining lease rights is one of the methods of assignment of rights to use any natural resources and the consideration that is paid by the leaseholder is royalty as fixed by the State Government at the time of grant of lease. This royalty which is in the nature of the annual amount payable to the state government are seemingly subject to service tax.

|

b. The mining industry incurs an excise duty; value added tax and central sales tax as the output tax liability:

|

c. In case of merchant miners as the extraction does not amount to manufacture there is no excise duty liability as output tax. In case of mining cum manufacturing sector if any further processing of the minerals so extracted from the mines is undertaken in order to remove the impurities from the minerals or any other value addition process are being undertaken then the same would attract excise duty.

|

d. The Value Added Tax (VAT) is levied on the sale of goods within the state. The mines output is subject to VAT, miners are allowed to take the credit of the vat paid on their inputs if any. The VAT cost flows from the mining company to the manufacturer and then to the distributor and reseller.

|

Analysis under the Goods and Service Tax:

|

|

The Constitutional Amendment Bill has deleted only the VAT, Entry Tax and Entertainment Tax from the state lists and Excise duty and Service Tax from the union list. As per Section 3, of the GST Model Law, 2016 the Goods and Service Tax is levied on the supply of goods and services. Various supplies of services such as exploration, mineral production, handling, transportation and the supply of the minerals to consumers would attract GST. Under GST there would be output taxes at the time of supply of output of the mines, but at the same time the input tax cost incurred by the miners would be allowed as credit.

|

|

|

As per schedule IV of the Goods and Service Tax Act, the consideration paid by the lease holder to the State Government for the grant of the lease of the mines in form of royalty would be chargeable to GST. However, as explained earlier, the matter is to be decided by nine-member bench of Hon'ble Supreme Court as to whether royalty is a tax or not. Thus, if it concluded that is it in the nature of tax, GST on same cannot be levied. Thus, as far as GST laws are concerned, there would be GST on the amount of Royalty paid but since Royalty itself is not within the frame work of GST, credit of royalty paid to the State Government becomes a cost of miner, whether merchant or manufacturer.

|

Royalty on Minerals excavated from Mines Whether liable to GST Constitutional Validity of entry No. 5 of notification 13/2017-CT(R) dated 28.6.2017 (HSN code 9973). Recently, Rajasthan HC, dismissed on 27.9.2022, a Number of writ petitions, seeking relief in payment of GST, on reverse charge basis, on ‘Royalty” in respect of Minerals excavated from Mines: Sudarshan Lal Gupta Contractor & Ors. v. Union of India & Ors.(2022) 38 J.K. Jain’s GST & VR 288 (issue dated 9.10.2022). It resulted into initiation of proceedings for levy of GST on Royalty.

|

A five-member bench in the case of State of West Bengal vs. Kesoram Industries Limited and Others were of the view that in the decision of India Cement, it was a typographical error in drafting the judgement either attributable to the stenographer's devil or to sheer inadvertence. It held that what the actual meaning and intent of the statement was that royalty was not a tax on land as it was not directly related to the land as required by Entry 49 but a different kind of tax that is to say, a tax on mineral extracted by individual which would be indirectly related to land. The five-member bench in Kesoram Industries Ltd. subsequently, to examine whether royalty is a tax or otherwise, referred the matter of Mineral Area Development Authority etc. vs. Union of India and Ors. to a nine-member bench of the Supreme Court. Further, the Supreme Court in the matter of Mineral Area Development Authority etc. vs. UOI and Ors. held that royalty paid may not be tax under common parlance but going by the definition of 'taxation' under Article 366(28) of the Constitution, royalty payable on extraction of minerals being in the nature of statutory impost comes under the purview of taxation.

|

The mining sector in India has been opposed for levying of tax on royalty paid on mining operations. In the Service Tax Regime after introduction of negative list regime, all services provided by the government were brought under the tax net and were subjected to reverse charge. This issue continued into the GST regime as well since the statutory liability for payment of tax on such government services fell on the recipient of such services under reverse charge mechanism (RCM) in terms of Entry 5 of Notification 13/2017-CT(R) dated 28.06.2017. The applicable rate on services by way of grant of mineral exploration and mining rights is 18% in terms of entry 17 (viii) (Leasing or rental services, without operator) of Notification No. 11/20171 w.e.f. January 1, 2019.

|

However, dispute arose whether royalty can be classified under entry 17 (viia) of Notification No. 11/2017 wherein any transfer of right in goods or of undivided share in goods without the transfer of title thereof attracts same GST rate as the supply of like goods prior to January 01, 2019, due to divergent rulings passed by various advance rulings authorities.

|

The Central Board of Indirect Taxes and Customs vide Circular dated 06.10.20212 has clarified that the intention of the government has always been to levy tax services by way of grant of mineral exploration and mining rights @18% and therefore, cannot be considered as leasing or renting of goods in terms of entry 17(viia) of Notification No. 11/2017 as mining rights is entirely different activity. Hence, the department's stand was clarified that there was no separate rate of tax specified under GST for service provided by way of grant of mineral exploration and mining rights, and that such service remained taxable @18% during period July 1, 2017, to December 31, 2018.

|

The clarification issued vide the Circular was challenged by the industry and consequently the Supreme Court has given a stay on GST on royalty paid to the States for mining rights in the matter of Lakhwinder Singh Vs UOI.

|

VALIDITY OF TAX LEVY, ULTIMATUM AND WAY FORWARD

|

Relying upon the judicial decisions under the erstwhile regime, royalty cannot be termed as a consideration received by the government to grant rights over for mineral extraction. Further, it cannot also be said that State Government has provided any service of granting rights for mineral extraction to bring it under the ambit of supply and thus no GST can be levied on royalty, dead rent and DMF charges paid towards mineral rights. It is a settled position of law that Royalty paid under a mining lease is in the nature of tax and thus, the contention that GST could not be imposed on royalty since royalty itself is a tax becomes very strong.

|

1. Notification No. 11/2017-CT(R) dated June 28, 2017

|

2. Circular No. 164/20/2021-GST dated 6.10.2021

|

Question: As per standard practice, the service tax/GST department called for information from mining department of state (Gujarat) which in turned provided list of firms (quarries) in whose name royalty is paid. Accordingly, the service tax/GST department issued SCN and passed order levying SERVICE TAX ON RCM on royalty paid as per list provided by mining department.

|

In given case, department had issued SCN and passed order in the name of “A” quarry who had taken land on lease for quarry business from mining department of the state.

|

But in actual “A” quarry had sub-leased the whole land to “B” quarry who had paid royalty directly to mining department and also claimed royalty expenditure. “A” quarry had neither paid any royalty nor claimed such royalty expense in books.

|

Only because “A” quarry had originally leased land from mining department, there name was forwarded to service tax/GST department.

|

What stand should be taken by “A” quarry to avoid service tax demand. As per information that whether royalty is tax or not question is pending before 9 judge benches of SC. What other stand can be taken in given facts?

|

Royalty is a fee or payment made against the license to use minerals including its exploration and evaluation. In other words, royalty is a fee or consideration paid to the property owner for the right to use the property or patentee for the use of a patent or property against money obtained on sold of each patent or value of extract resources during the licensed period.

|

Royalties are agreed upon as a percentage of gross or net revenues obtained from the use of an asset so authorised by the party assets owns.

|

In terms of Section 9 of the Mines and Minerals (Development and Regulation) Act, 1957 the holder of mining lease shall pay royalty in respect of any mineral removed / consumed.

|

The Hon’ble Supreme Court in the case of State of Orissa and others v. M/s Steel Authority of India Ltd. (AIR 1998 SC 3052), the Apex Court opined that Section 9(1) of the MMDR Act, 1957 also contemplates the levy of royalty on the mineral consumed by the holder of a mining lease in the leased area, hence processing of mineral amounts to consumption and, therefore, the entire mineral is eligible to levy of royalty.

|

Thus, levy and applicability of tax on royalty was disputed in the erstwhile Service tax regime. But in GST regime the applicability is not the matter of dispute rather applicable rate of GST on royalty is the matter of litigation, which has been clarified by the CBIC vide Notification No. 27/2018-C.T. (Rate), dated 31-12.2018 as amended and rate of GST on royalty shall be chargeable to 18% on amount of royalty so collected from the license holders of mines under RCM.

|

Further, it is clarified vide Sectoral FAQ’s by CBEC, is that “ The Government provides license to various companies including public sector undertakings for exploration of natural resources like oil, hydrocarbons, iron ore, manganese, etc. For having assigned the right to use the natural resources, the licensee companies are required to pay consideration in the form of annual license fee, lease charge, royalty, etc to the Government. The activity of assignment of rights to use natural resources is treated as supply of service and the licensee is required to pay GST on the amount of consideration paid in the form of royalty or any other form under reverse charge mechanism”.

|

In the given case since lease is in the name of “A” ,it is his duty for payment of royalty on lease and not of “B”. In may be considered that the royalty may be paid by “B” in the name of “A”. The liability of payment of GST on royalty will fall on “A” through RCM.

|

Let’s consider that “B” has also not paid the royalty and GST on RCM, then it is liability of “A” to pay GST on RCM. On other hand if “B” has paid the same then there is not liability of “A” for payment of GST or Service Tax, since double taxation on the same matter cannot be paid.

|

If such facts exist then reliance can also be made on the judgment of Hon. Bombay High Court in case of United Spirits Ltd. vs. State of Maharashtra (Writ Petition (L) no.10092 of 2020 dt.29.4.2022) wherein High Court has held that when buyer has paid tax, vendor is not liable to pay tax. The factual position be seen accordingly.

|

The other fact appearing from query is that there is sub-lease. Therefore, on consideration received by A from B, there may be GST liability on A. This aspect should also be examined.

|

FAQ on GST for Mining sector of India

|

Question: Can small mining leaseholders with a turnover less than Rs.75 lacs operate under composition scheme

|

Answer: As per Sec. 10(1) of the CGST Act, 2017, a registered person whose aggregate turnover in the preceding FY did not exceed Rs.75 lakhs, would be eligible for paying GST under the composition scheme.

|

Question: What is the GST rate for minerals and ores in Composition Scheme

|

Answer: In a case where the process amounts to manufacture, the rate of tax will be 1% (CGST) and 1%(SGST/UTGST). In any other case, the rate will be %(CGST) and % (SGST/UTGST).

|

Question: Will they have to deposit GST under SGST/CGST heads separately

|

Answer: Yes. GST has to be paid separately under CGST and SGST/UTGST by generating a single challan through the common portal under a single return.

|

Question: Can a small Mine Lease holder undertakeinter-State supply if it avails composition scheme

|

Answer: No. If a supplier chooses to avail of composition scheme, he shall not undertake inter-State supply.

|

Question: What is the IGST rate for minerals and ores in case of inter State supply

|

Answer: At present, the IGST rate is the sum of CGST and SGST/ UTGST rate. These rates have been notified and are available in public domain.

|

Question: Can the buyer get input credit on the supply of minerals from a mine owner in composition scheme

|

Answer: No, the buyer cannot avail of the credit of tax paid by the supplier who is under the composition scheme as the person paying tax under composition scheme cannot issue a tax invoice and collect taxes on his supplies.

|

Question: Will the recipient have to pay tax under reverse charge.

|

Answer: GST on reverse charge mechanism is payable under section 9(4) of the CGST Act, 2017 only in case of purchases from unregistered suppliers. As the mine owner who is paying tax under composition scheme is registered, the recipients need not pay GST on reverse charge mechanism.

|

Question: What is the threshold limit and conditions when a small mine owner/lease holder under Composition Scheme has to migrate into full GST System

|

Answer: As per section 10(3) of the CGST Act, 2017, the option availed of by the small mine owner/ leaseholder shall lapse with effect from the day on which his aggregate turnover during a financial year exceeds Rs. 75lakhs. For details regarding other conditions, section 10 of the CGST Act, 2017 and the rules framed there under maybe referred to.

|

Question: Is the Return filing and compliance simpler under composition scheme

|

Answer: Yes, return filing and compliance is simpler under the composition scheme. The registered person has to file only one return on a quarterly basis in FormGSTR-4.

|

Question: Will the basic exemption limit from GST be applicable to the tiny & micro segment in mining

|

Answer: Yes, the basic exemption limit of Rs. 20 lakhs (Rs.10 lakhs in the case of special category States) is applicable to the tiny and micro segment even in mining. However, a person engaged in making taxable supply and having aggregate annual turnover (more than Rs.20 lakhs in any State other than the special category States) would be liable to obtain registration under GST. The return has to be filed on monthly basis by regular taxable persons and on quarterly basis by the taxable persons registered under the composition scheme.

|

Question: What is aggregate turnover

|

Answer: As per section 2(6) of the CGST Act, 2017, aggregate turnover means the aggregate value of all taxable supplies (excluding the value of inward supplies on which tax is payable by a person on reverse charge basis), exempt supplies, exports of goods or services or both and inter-State supplies of persons having the same Permanent Account Number, to be computed on all India basis but excludes Central tax, State tax, Union territory tax, integrated tax and compensation cess.

|

Question: Will the buyer of goods from unregistered person pay reverse tax

|

Answer: A registered person receiving taxable goods or services from a supplier who is not registered, would be liable to pay GST under reverse charge mechanism. However, in terms of notification no. 8/2017-Central Tax (rate) dated 28th June, 2017, aggregate value of supplies of goods and/or service received by a registered person from any or all the suppliers, who is or are not registered, up to five thousand rupees in a day is exempt from tax under reverse charge mechanism. This exemption will not apply if the value exceeds Rs.5000/-.

|

Question: Can a buyer of goods and services pay the value of services / goods to the supplier and deposit theGST component of the invoice in the suppliers account so that when the buyer claims input credit, he may get the same cross entry tallied from the suppliers account

|

Answer: No. This option is not available under GST Law.

|

Question: In case there are disputes regarding quality, weight, etc. between the buyer and the supplier and the goods are returned fully or partially, as found unfit for use, can the excess paid tax component be adjusted from future tax liability

|

Answer: In such cases, the supplier may issue a credit note to the recipient in accordance with the provisions of section 34(1) of the CGST Act, 2017.

|

Question: Whether deduction of Liquidity Damage (LD)/Penalty deduction from contractor’s bills and charging Penalty for non-lifting of coal till targeted minimum level to Annual Contractual Quantity (ACQ) will attract GST

|

Answer: Yes, it is a service being tolerating an act as per Schedule II of the CGST Act,2017 thus GST shall apply.

|

Question: Will GST be payable at the time of raising an invoice for supply of goods from a mining lease holder or it will be applicable on the amount of advance received by the mining company for booking the order

|

Answer: No. As per the provisions of section 12(2) of the CGST Act, 2017 the time of supply of goods shall be the date of issue of invoice or the date of receipt of payment, whichever is earlier. Accordingly, GST would be payable on advance payment received prior to issuance of the invoice.

|

Question: Will the supplier have to issue receipt voucher against each advance received

|

Answer: Yes, as per section 31(3)(d) of the CGST Act, 2017the supplier has to issue a receipt voucher for every advance received.

|

Question: How do I show the advance received in GSTR 1

|

Answer: Where against an advance the invoice is issued in the same tax period, the advance need not be shown separately in Form GSTR-1 but the specified details of invoice itself can be directly uploaded on the system. Details of all advances against which the invoices have not been issued till the end of the tax period shall have to be reported on a consolidated basis in Table 11 of FormGSTR-1. As and when the invoices against these advances are issued, they have to be declared in Form GSTR-1 and the adjustment of the tax paid on advances against the tax payable on the invoices uploaded in Form GSTR-1 shall have to be done in Table 11 of Form GSTR-1.

|

Question: In case no supplies are made against an advance, will the dealer have to issue a refund voucher only for the advance or for advance including GST

|

Answer: Refund voucher has to be made for the fullvalue of advance, including the amount of GST.

|

Question: It will be difficult to link between Advance Receipt Voucher and invoices in case of sales billing on Cash Sale (Rail/Road)/e-Auction etc., especially in case of Rail Cash sale, where purchasers deposit money in advance to the tune of many crores for which lifting of coal has to be made from various loading point and time. In such situation how will the billing person at one point realize how much balance advance is available for adjustment while raising invoice at his end at a specific point of time

|

Answer: Under GST gross amount of advance is to be reported and tax has to be paid. Advance can be adjusted in totality. While raising the invoice subsequent to receipt of advance, the tax payable will get reduced by the amount of tax paid on the advance and balance amount of advance may be adjusted against future supplies.

|

Question: Will GST charged on purchase of all earthmoving machinery including JCB, tippers, dumpers by a mining company be allowed as input credit

|

Answer: The provision of Sec. 17(5) (a) of the CGST Act, 2017 restricts credit on motor vehicle for specified purposes listed therein. Further, in terms of the provision of Section2(76) of the CGST Act, 2017 the expression motor vehicle shall have the same meaning as assigned to it in Clause (28) of Section 2 of the Motor Vehicle Act, 1988, which does not include the mining equipment, viz., tippers, dumpers. Thus, as per present provisions, the GST charged on purchase of earth moving machinery including tippers, dumpers used for transportation of goods by a mining company will be allowed as input credit.

|

Question: Whether GST is payable on royalty (to be paid to Government) for Mining Lease granted by State Government.

|

Answer: Yes, on royalty GST will apply under reverse charge mechanism. Further, such payment of GST under reverse charge mechanism would be eligible as ITC in the hands of the recipient of supply for payment of GST.

|

Question: Is ITC available on hiring of immovable properties (land, office, warehouse, processing unit, stock yards) for facilitation of mining operations

|

Answer: Yes. GST paid on hiring of land, office, warehouse, processing unit, stock yards when these are used in the course or furtherance of business, would be allowed as ITC.

|

Question: What is the time limit for availing input credit under GST

|

Answer: As per provisions of Section 16(4) of the CGST Act, 2017 the ITC is not available after the due date of furnishing the return for the month of September of the next year or furnishing of the annual return, whichever is earlier.

|

Question: Would the net outstanding amount of unutilized input credit be refunded by the Government

|

Answer: In terms of the provision of Section 54(3) of the CGST Act, 2017 subject to conditions, refund of unutilized input tax credit would be available in respect of zero-rated supply or where ITC has accumulated on account of rate of tax on inputs being higher than the rate of tax on the output supply. However, such refund of ITC would not be available if export duty is payable on the goods so exported out of India.

|

Question: Will GST charged by tax consultants, advocates, Chartered Accountants, environmental consultants, canteen service providers and other service providers to mining companies be allowed as input credit

|

Answer: ITC on any input service/ inputs used in the course of furtherance of business would be available subject to restrictions and other conditions as per the provisions of Chapter-V of the CGST Act, 2017. However, tax paid in respect of canteen service providers shall not be available as credit.

|

Question: Whether free issue of coal to employees paid in course of employment and on the basis of wage agreement with value below Rs.50, 000/- per employee will attract GST

|

Answer: Gifts not exceeding fifty thousand rupees in value in a financial year by an employer to an employee shall not be treated as supply of goods or services or both (as per Schedule 1 of the CGST Act, 2017). Free issue of coal based on the wage agreement is not a gift. Therefore, free issue of coal in this case will attract GST.

|

Question: Can GST charged as per transport billon movement of mineral from mine to the buyer be allowed as ITC to the buyer irrespective of the ownership of the transporting vehicle

|