|

onlinetaxupdate team wish to express sincere thanks to all the readers, authors, subscribers for the support extended to us. Please share your feedback at

|

taxupdate.otu@gmail.com or 7738647904

|

Newsletter 145 dated 25.11.2024

|

|

|

|

|

|

|

|

|

Dear Reader,

|

Please find newsletter for your reading and reference.

|

|

Index of the Newsletter

- Recent updates

- Portal updates

- Article

- Lawgics by Ms.Nidhi Aggarwal

- GST Notes by CMA Anil Sharma

- GST Daily by CA Pradeep Modi

- PPT/Handbook

- GST/IT/Customs in media

|

|

|

|

|

|

|

CBIC issued Notification No. 58/2026-Customs (N.T.) dated 22.06.2026 to hereby appoint the officer to exercise the powers and discharge the duties conferred on the officers for the purpose of adjudication of the show cause notices.

|

|

|

|

|

|

|

|

CBIC issued Notification No. 57/2026-Customs (N.T.) dated 18.06.2026 to further amend Notification No. 27/2018-Customs (N.T.) dated 28.03.2018.

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Notification no. 12/2026-Customs (ADD) dated 19.06.2026 Seeking to continue anti-dumping duty on imports of Polyethylene Terephthalate resin having an intrinsic viscosity of 0.72 decilitres per gram or higher originating in or exported from China for a period of 5 years

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Circular no. 28/2026-Customs dated 15.06.2026 regarding testing of samples of export consignments

|

|

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Circular no. 27/2026-Customs dated 15.06.2026 regarding Exemption of Merchant Overtime Charges (MOT) on International Cruise passengers and baggage clearance at cruise ports.

|

|

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Circular no. 26/2026-Customs dated 19.05.2026 regarding Standardisation of procedures relating to grant of Entry Inward and Vessel Sail-Out Clearance.

|

|

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Circular no. 25/2026-Customs dated 14.05.2026 regarding Extension of Validity of the circulars issued under Section 143AA of the Customs Act, 1962, to mitigate challenges arising from the ongoing disruptions in maritime routes due to the closure of the Strait of Hormuz.

|

|

|

|

|

|

Central Board of Indirect Taxes & Customs issued CAVR Review Order No. 2/2025-Customs dated 26.11.2025 for extension of validity of CAVR Order No. 02/2023-Customs under the Custom (Assistance in Value Declaration of Identified imported Goods) Rules. 2023 in respect of Stainless Steel of J3 grade classified under HS Codes 72191200. 72191300. 72191400, 72192390. 72193290. 72193390. 72193490. 72193590. 72199012. 72199013. 72199090. 72202029. 72202090, 72209022,72209029 & 72209090

|

ln exercise of the powers conferred by clause (iv) of the second proviso to sub-section (1) ol section 14 of the Customs Act, 1962 (52 of 1 962), read with sub rule (2) of rule 10 and rule 5 of the Customs (Assistance in Value Declaration of Identified Imported Goods) Rules,2023, the Central Board of Indirect Taxes & Customs hereby extends the validity of CAVR Order No. 02/2023-Customs dated 15th November, 2023, issued in respect of Stainless Steel of J3 grade falling under HS Codes 72191200, 72191300, 72191400, 72192390, 72193290, 72193390, 72193490, 72193590, 72199012, 72199013, 72199090, 72202029, 72202090,72209022,72209029 & 72209090, for a period of one year with effect from 29th November, 2025. This order shall remain in force till 28th November, 2026

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Notification no. 02/2026 – Central Tax dated 07.05.2026.

|

GOVERNMENT OF INDIA

MINISTRY OF FINANCE

DEPARTMENT OF REVENUE

|

Notification No. 02/2026 – Central Tax dated 07.05.2026

|

S.O. 2286(E).— In exercise of the powers conferred by sub-section (1A) of section 101A of the Central Goods and Services Tax Act, 2017 (12 of 2017) (hereinafter referred to as the said Act), the Central Government, on the recommendations of the Council, hereby empowers the Principal Bench of the Appellate Tribunal, New Delhi constituted under sub-section (3) of section 109 of the said Act, to hear appeals made under section 101B of the said Act.

|

This notification shall be deemed to have come into force on the 1st day of April, 2026.

|

BALASUBRAMANIAN KRISHNAMURTHY,

Joint Secretary

|

|

|

|

|

|

Central Board of Direct Taxes issued Circular no. 4 of 2026 dated 31.03.2026 regarding Document Identification Number (DIN).

|

|

|

|

|

|

|

|

Central Board of Direct Taxes (TPL Division) issued Circular No. 03 of 2026 dated 30.03.2026 regarding Notification of Sovereign Wealth Fund under Schedule V of the Income-tax Act, 2025

|

|

|

|

|

|

Central Board of Direct Taxes (CBDT) issued notification no. 72/2026 dated 25.06.2026 to hereby approves deductions under section 45(3)(a)(i) of the Income-tax Act, 2025 and rules 32 and 34 of the Income-tax Rules, 2026 to the Public Health Foundation of India, Delhi (PAN: AABAP4445L) for Scientific Research under the category of University, college or other institution.

|

|

|

|

|

|

CBIC issued clarification via F. No. CBIC-20016/75/2025-GST dated 25.09.2025 on requirement of separate GST registration for importers storing goods in Warehouses in other States

|

|

|

|

|

|

Press release ID 2279424 dated 30.06.26

|

The Government had earlier provided a full Customs Duty exemption on imports of critical petrochemical products till 30th June 2026, as a temporary and targeted relief in view of the conflict in West Asia and the consequent disruptions in global supply chains.

|

The exemption was provided to ensure sufficient availability of petrochemicals in the domestic market as Indian petroleum companies had been asked to concentrate on the production of LPG during this period. As the situation is gradually normalizing, to ensure a smooth and non-disruptive transition for the affected sectors, it has been decided to extend the said exemption by a further period of 15 days, that is, till 15th July 2026.The list of products covered remains the same as notified earlier.

|

The Government remains committed to supporting India's manufacturing sector. As before, the exemption is expected to benefit a wide range of sectors dependent on petrochemical feedstock and intermediates, including plastics, packaging, textiles, pharmaceuticals, chemicals, automotive components and other manufacturing segments. This will also provide relief to consumers of final products.

|

Link to previous press note issued:

|

|

|

|

|

|

|

|

|

GSTN is taking downtime to enhance its services on the GST Portal on 27.06.2026 from 12:00 AM onwards until 2:30 am of 27.06.2026.

|

|

We shall be enhancing services on the GST portal on : 27th June’26 12:00 AM onwards. GST Portal services will not be available until 27th June’26 02:30 AM. The inconvenience caused is regretted.

|

|

|

|

|

|

|

|

|

|

|

4. Lawgics by Ms.Nidhi Aggarwal

|

Ms. Nidhi Aggarwal is delighted to present judgment with a great vision to spread complex GST law in a simple manner amongst the taxpayers, tax professionals, students and knowledge seeker.

|

|

Recently added notes are listed below:

|

|

|

|

|

|

Synopsis: The Delhi High Court dismissed the writ petition involving fraudulent ITC claims, directing the petitioner to pursue appellate remedy u/s 107 of the CGST Act.

|

Caste name: Banson Enterprises & Anr. vs Assistant Commissioner CGST & Ors.

|

Citation: W.P. (C) 6503/2025 dated 15.05.2025

|

Authority: Delhi High Court

|

The petition challenges the Order-in-Original dated 02.02.2025 based on a Show Cause Notice (SCN) dated 03.08.2024 A search was conducted, and statements were recorded including that of one Director admitting to the issuance of fake invoices during the Central Excise period. It was alleged that the Petitioner issued goods-less invoices to enable fraudulent Input Tax Credit (ITC) claims amounting to Rs. 1.85 crore.

|

Contentions of the Petitioner:

|

SCN was issued by unauthorized officer, thus, violates Rule 142(1)(a) of CGST Rules. No pre-consultation as required under Rule 142(1A) of CGST Rules was issued. Consolidated SCN for multiple financial years was issued and challenge to such consolidated action is pending in a separate matter (Quest Infotech case).

|

Contentions of the Department:

The impugned order is appealable, hence writ is not maintainable. The Petitioner’s Director admitted to allegations. Natural justice was followed as the Petitioner received the SCN, filed a reply, and availed of personal hearing. Reliance must be made on SC judgments and Allahabad HC rulings emphasizing alternate remedy u/s 107 CGST Act.

|

Findings and Decision of the Court:

The Court refused to interfere under writ jurisdiction, citing:

|

- No breach of fundamental rights or principles of natural justice.

- Availability of a statutory remedy (appeal) under Section 107 CGST Act.

The Court noted that the Allegations involve serious misuse of ITC, requiring fact-based adjudication, not suited for writ jurisdiction. Thus, the Petitioner was granted liberty to file appeal, and if filed with pre deposit, the appeal shall not be dismissed on limitation.

|

|

|

|

|

|

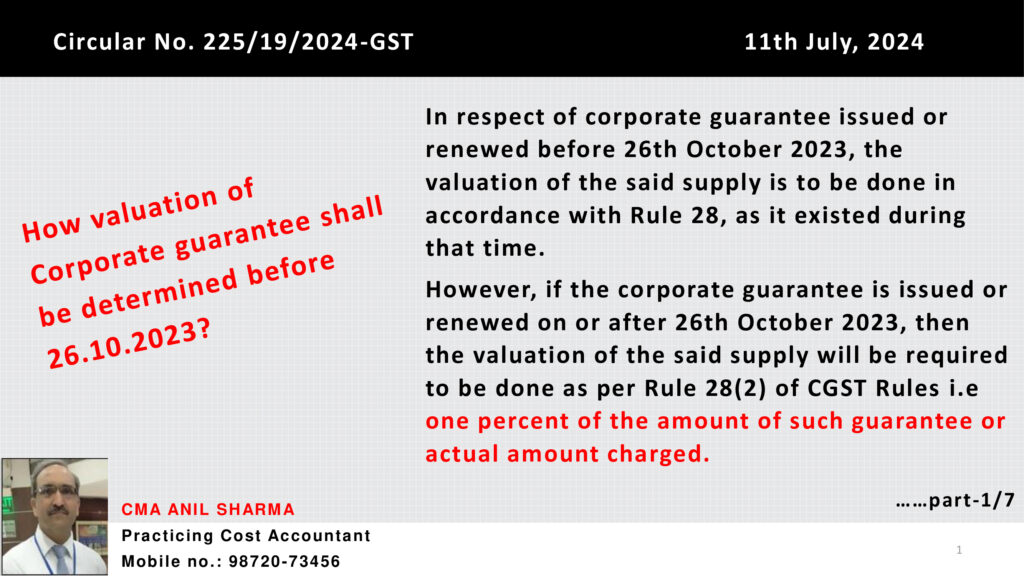

5. GST Notes by CMA Anil Sharma

1) New series title "Capsule" is added in the Notes section.

|

- Total 62 slides in capsule-01 & capsule 02 Part 1 & 2 and capsule 03 part 1 is added

|

|

|

|

|

|

|

|

6. GST Daily by CA Pradeep Modi

CA Pradeep Modi is presenting judgment analysis under title 'GST Daily - Stay yourself updated'

|

|

|

|

|

|

THE HON'BLE ALLAHABAD HIGH COURT IN THE CASE OF Vibhuti Tyres V/s State of U.P., decided on 7-5-2025

|

✔️ Is it justified that GST order with higher demand than show-cause notice?

|

👉 The Hon'ble High Court Judgement:-

|

✔️ Where in show-cause notice amount representing tax, interest and penalty was indicated as Rs. 8,81,080, but in order, much higher demand was raised at Rs. 32,97,336, same was in violation of section 75(7); matter was to be remanded back.

|

Section 75 of Central Goods and Services Tax Act, 2017

|

|

|

|

|

|

7. PPT/Handbook on GST

|

|

|

|

8. GST/Income Tax in Media

|

|

|

|

|

|

|

|

|

|

|

|

|

Webinar - GST Litigation Course

|

|

|

🗓 Date: 26, 27 & 28.11.2024 (Tuesday, Wednesday & Thursday)

⏰ Time: 6:00 pm to 8:00 pm.

🎤 Speaker: Adv. (CA) Arup Dasgupta

▶ Medium: English

🤝 Fees: Rs. 1,999/-

🎥 Recording - Yes

📚 Study material - Yes

🎖 Certificate - Yes

|

|

|

|

|

|

|

|

|

|

|

Hope the above updates is of use to you. Please share your input and feedback at taxupdate.otu@gmail.com

|

|

|

|

|

|

|

|

|

Visit our website

|

OTU provides you

|

- Articles on various topics

|

|

- Media - GST, Income Tax & Press R.

|

|

|

|