|

|

|

|

|

|

|

|

This website contains information about recent changes mainly in GST laws. It also contains Articles on various topic in GST. Please visit the website and read more.

|

|

|

|

Dear Reader,

|

Please find newsletter for your reading and reference.

|

|

Newsletter no. 95 dated 01.08.2023

|

|

|

Index of the Newsletter

- Recent updates

- GST in media

- Income Tax in media

- Articles

- Lawgics by Ms.Nidhi Aggarwal

- GST notes by CMA Anil Sharma

|

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Notification no. 02/2026 – Central Tax dated 07.05.2026.

|

GOVERNMENT OF INDIA

MINISTRY OF FINANCE

DEPARTMENT OF REVENUE

|

Notification No. 02/2026 – Central Tax dated 07.05.2026

|

S.O. 2286(E).— In exercise of the powers conferred by sub-section (1A) of section 101A of the Central Goods and Services Tax Act, 2017 (12 of 2017) (hereinafter referred to as the said Act), the Central Government, on the recommendations of the Council, hereby empowers the Principal Bench of the Appellate Tribunal, New Delhi constituted under sub-section (3) of section 109 of the said Act, to hear appeals made under section 101B of the said Act.

|

This notification shall be deemed to have come into force on the 1st day of April, 2026.

|

BALASUBRAMANIAN KRISHNAMURTHY,

Joint Secretary

|

|

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Notification no. 01/2026 – Central Tax dated 21.04.2026 that Seeks to extends the due date for furnishing the return in FORM GSTR-3B for the month of March, 2026 till the twenty-first day of April, 2026.

|

GOVERNMENT OF INDIA

MINISTRY OF FINANCE

DEPARTMENT OF REVENUE

CENTRAL BOARD OF INDIRECT TAXES AND CUSTOMS

Notification No. 01 /2026 Central Tax dated 21.04.2026

|

G.S.R (E)… ( In exercise of the powers conferred by sub section (6) of section 39 of the Central Goods and Services Tax Act, 2017 (12 of 2017), the Commissioner, on the recommendations of the GST Council, hereby extends the due date for furnishing the return in FORM GSTR 3B for the month of March, 2026 till the twenty first day of April, 2026, for the registered persons who are required to furnish return under sub section (1) of section 39 read with clause (i) of sub rule (1) of rule 61 of the Central Goods and Services Tax Rules, 2017.

|

2. This notification shall come into effect from 20th day of April, 2026.

|

(Kangale Shrunkhala Motiram)

Director

|

|

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Notification no. 20/2025 – Central Tax dated 31.12.2025 which Seeks to notify Central Goods and Services Tax (Fifth Amendment) Rules, 2025

|

1. These rules may be called as the Central Goods and Services Tax (Fifth Amendment) Rules, 2025. They shall come into force from 1st day of February, 2026.

|

2. In the Central Goods and Services Tax Rules, 2017 (hereinafter referred to as the said rules), after rule 31C, the following rule shall be inserted, namely: —

|

"31D. Value of supply of goods on basis of retail sale price. -(1) Notwithstanding anything contained in the provisions of this Chapter, the value of supply of goods bearing the description specified in column (3), falling under the corresponding Chapter/ heading/ sub-heading/ tariff item specified in column (2), of the Table below, shall be deemed to be the retail sale price declared on such goods, less the amount of tax as applicable, namely: -

|

(2) The amount of applicable tax referred to in sub-rule (1) shall be determined in the following manner, namely: —

|

Tax amount = (Retail sale price X tax rate in % of applicable taxes) / (100+ sum of applicable tax rate).

|

Explanation. — For the purposes of this rule, —

|

(a) “applicable tax” means IGST or CGST or SGST or UTGST as the case may be.

|

(b) "retail sale price" means the maximum price declared on goods at which such goods in packaged

form may be sold to the ultimate consumer and includes all taxes, duties, surcharge or cess by

whatever name called;

|

(c) where on the package of any specified goods more than one retail sale price is declared, the

maximum of such retail sale price shall be deemed to be the retail sale price;

|

(d) where the retail sale price declared on packages of any specified goods is altered to increase the

retail sale price at any stage before, during, or after the supply, such altered retail sale price shall be

deemed to be the retail sale price;

|

(e) where different retail sale prices are declared on different packages for the sale of any specified

goods above in packaged form in different areas, each such retail sale price shall be the retail sale

price for the purposes of valuation of the specified goods intended to be sold in the area to which

the retail sale price relates.".

|

3. In the said rules, in rule 86B, in the first proviso, after clause (e), the following clause shall be inserted, namely: —

|

"(f) the registered person other than a manufacturer shall be exempted from the provisions of this rule only in respect of goods specified under rule 31D, on which the tax has been paid by the supplier on the basis of retail sale price:".

|

Note: The principal rules were published in the Gazette of India, Extraordinary, Part II, Section 3, Sub section (i) vide notification No. 3/2017-Central Tax, dated the 19th June, 2017, published vide number G.S.R. 610(E), dated the 19th June, 2017 and were last amended, vide notification No. 18/2025– Central Tax, dated the 31st October, 2025, vide number G.S.R. 805(E), dated the 31st October, 2025

|

|

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Notification no. 19/2025 – Central Tax dated 31.12.2025 which Seeks to notify supplies under section 15(5) of CGST Act for valuation based on Retail sale price (RSP)

|

|

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Notification no. 18/2025 – Central Tax dated 31.10.2025 that Seeks to notify the Central Goods and Services Tax (Fourth Amendment) Rules 2025

|

|

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Notification no. 17/2025 – Central Tax dated 18.10.2025 Seeking to extend date of filing GSTR-3B.

|

|

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Notification no. 16/2025 – Central Tax dated 17.09.2025 that Seeks to notify clauses (ii), (iii) of section 121, section 122 to section 124 and section 126 to 134 of Finance Act, 2025 to come into force.

|

|

|

|

|

|

The Central Board of Indirect Taxes vide F. No.225/56/2026/ITA-II dated 04.06.2026 issued Guidelines for Compulsory Selection of returns for Complete Scrutiny during the financial year 2026-27 - procedure for compulsory selection in such cases.

|

The Guidelines for Compulsory Selection of returns filed during the financial year 2025-26 under the Income-tax, Act 1961 are hereby issued in pursuance of Section 536(2)(c) of the Income-tax Act, 2025. The parameters for compulsory selection of returns for complete scrutiny during Financial Year 2026-27 and procedure for compulsory selection in such cases are prescribed as under:

|

3. For Assessing Officers in International Taxation and Central charges: Cases may be selected for compulsory scrutiny by the International Taxation and Central Charges following the above prescribed parameters at Para 2 with prior administrative approval of Pr.CIT/Pr.DIT/CIT/DIT concerned and these selected cases shall continue to be handled by International Taxation and Central Circle charges respectively, as earlier. It is further clarified that communication to NaFAC for access and /or further action after selection for Compulsory Scrutiny will not apply to the International Taxation and Central charges.

|

4. Time limit: As per the proviso to section 143(2) of the Income tax Act, 1961 and in terms of section 536(2)(c) of the Income-tax Act, 2025, the time limit for service of notice u/s 143(2) of the Income-tax Act, 1961 for the ITRs filed in the Financial Year (FY) 2025-26 is 30.06.2026.

|

5. These instructions may be brought to the notice of all concerned for necessary compliance.

|

|

|

|

|

|

|

|

Form of Declaration under section 393(6) of the Income-tax Act, 2025 for receipt ofcertain incomes without deduction of tax

|

|

|

|

|

|

Directorate of Commercial Taxes, Kolkatta issued Order No. 4302CT dated 04.07.2025 regarding Extension of period for completion of Audit as per the proviso to sub-section (4) of section 65 of the WBGST Act, 2017 for the period starting on or after 1st day of April, 2021 and ending on or before 31st day of March, 2022 or part thereof.

|

WHEREAS Audit of selected registered persons under section 65 of the West Bengal Goods and Services Tax Act, 2017 (hereinafter referred to as the said Act) for the period starting on or after 1st day of April, 2021 and ending on or before 31st day of March, 2022 or part thereof has commenced;

|

AND WHEREAS sub-section (4) of section 65 of the said Act stipulates that Audit has to be completed within a period of three (03) months from the date of commencement;

|

AND WHEREAS the progress of audit in all these cases got delayed due to requests received from various auditees for further time for production of books of accounts as required for completion of audit;

|

AND WHEREAS I am satisfied that such Audit cases cannot be completed within three months from the individual date of their commencement;

|

NOW THEREFORE, in exercise of the power conferred by proviso to sub-section (4) of section 65 of the said Act, I hereby extend the period for completion of Audit cases for the period starting on or after 1st day of April, 2021 and ending on or before 31st day of March, 2022 or part thereof, for a further period till the 22nd day of August, 2025 or three months from the actual date of commencement whichever is later.

|

This order shall come into force with immediate effect.

|

|

|

|

|

|

Kolkata is likely to host the 57th meeting of the GST Council next month, sources said, although the Union Finance Ministry has not yet officially confirmed the venue or the schedule. The meeting is expected to be held in the second half of July, and could take up the next round of indirect tax policy reforms.

|

Hosting the meeting in Kolkata holds significance as it would mark one of the first major meetings of a Constitutional federal body in West Bengal after the Assembly elections. While the GST Council independently decides its agenda and meeting schedule, the choice of Kolkata would coincide with the Centre’s broader emphasis on strengthening the State’s profile as a destination for investment and financial activity following the change in government.

|

New reforms

The previous GST Council meeting, held on September 3, 2025, came after a gap of nearly nine months, despite the rules providing for at least one meeting every quarter. That meeting unveiled GST 2.0, including rate rationalisation and measures to ease compliance. Tax experts now expect the council to consider another set of policy reforms, some of which were discussed during 4th Annual Seminar on Direct and Indirect Taxes of the Bengal Chamber of Commerce & Industry (BCCI).

|

Vivek Jalan, Chairperson of the National Fiscal Affairs and Taxation Committee of BCCI, said that in the spirit of GST 2.0, which was launched to strengthen India’s manufacturing base, the council should correct the anomaly of non‑refund of Input Service ITC under the inverted duty structure. While GST 2.0’s rate rationalisation has supported consumption, the cost pressures has deepened on manufacturers. “Addressing this gap will ensure reducing cascading taxes, boosting competitiveness and advancing India’s vision of becoming the world’s third‑largest economy by 2047,” he said.

|

Also, it has been proposed before the GST Council to consider reducing the GST rate on autism care centres and allied sectors from 18 per cent to 5 per cent. Such a measure under GST would ease the financial strain on families and institutions, while reinforcing the government’s vision of inclusive growth. “By aligning tax policy with compassion, the council can ensure that essential services for differently‑abled children remain affordable, accessible and sustainable, a step that truly reflects the spirit of GST reforms,” said Jalan.

|

Source: The Hindu businesline

|

|

|

|

|

|

|

|

CGST rates on goods as on 22.09.2025 as per Notification No. 09/2025-Central Tax (Rate), dated 17th September, 2025.

|

|

|

|

|

|

|

|

NCH strengthens consumer empowerment through a dedicated GST sub-category

|

The Department of Consumer Affairs has taken steps to align the National Consumer Helpline (NCH) with the Next-Gen GST Reforms 2025 approved during the 56th meeting of the GST Council chaired by the Union Finance Minister and in line with the vision articulated by the Hon’ble Prime Minister in his Independence Day 2025 address.

|

To address the expected consumer queries and complaints on NCH following the implementation of revised GST charges, rates and exemptions effective from 22.09.2025, a dedicated category has been enabled on the INGRAM portal. This category features major sub-categories including Automobiles, Banking, Consumer Durables, E-commerce, FMCG and others wherein GST related complaints will be registered.

|

In preparation for this initiative, an inaugural training session by Central Board of Indirect Taxes & Customs (CBIC) officials was conducted on 11.09.2025 to equip NCH counsellors to handle GST related queries and grievances effectively. Recently, a stakeholder consultation meeting was convened under the chairpersonship of Secretary (Consumer Affairs) on 17.09.2025 with participation from leading e-commerce platforms, representatives of industry associations and consumer durables companies. During the meeting, participants were urged to pass on the benefits of GST rate reductions on specified goods and services to consumers.

|

The helpline will also share data and insights generated from consumer complaints under this sector with concerned companies, CBIC and other concerned authorities to enable timely action under relevant laws. This initiative is expected to strengthen GST compliance and promote a participatory governance model by empowering consumers to become active stakeholders in fair market practices.

|

The National Consumer Helpline (www.consumerhelpline.gov.in) has emerged as a single point of access for consumers across the country to register grievances at the pre-litigation stage. Consumers can now lodge their complaints in 17 languages (including Hindi, English, Kashmiri, Punjabi, Nepali, Gujarati, Marathi, Kannada, Telugu, Tamil, Malayalam, Maithili, Santhali, Bengali, Odia, Assamese, and Manipuri) via toll-free number 1915 or through the Integrated Grievance Redressal Mechanism (INGRAM). This omni-channel IT-enabled platform supports multiple registration modes including WhatsApp, SMS, email, NCH app, web portal and Umang app providing convenience and flexibility to consumers.

|

Over the years, NCH has grown into a robust ecosystem collaborating with 1,142 convergence partners till date comprising private companies, regulators, ombudsman and government agencies, thereby enabling centralized and faster grievance resolution. Each complaint is assigned a unique docket number for transparent tracking and resolution. The platform currently receives over one lakh complaints per month reflecting the growing consumer trust.

|

The technological transformation of the NCH has significantly boosted its call-handling capacity. The number of calls received by NCH has grown more than tenfold from 12,553 in December 2015 to 1,55,138 in December 2024. This exponential growth reflects the rising confidence of consumers in the helpline. Similarly, the average number of complaints registered per month has surged from 37,062 in 2017 to 1,70,585 in 2025. With the introduction of digital modes, nearly 65% of consumer grievances on the helpline are registered through online and digital channels.

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Corrigendum on 12.06.2026 to Notification no. 45/2025 -Customs dated 24.10.2025 -

|

G.S.R…(E).- In the notification of the Government of India, Ministry of Finance (Department of Revenue) No. 45/2025-Customs, dated the 24th October, 2025, published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i), vide number G.S.R. 781(E), dated the 24th October, 2025, at page 291, in lines 12 and 14, for ‘1993’ read ‘1983’.

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Notification no. 01/2026-Central Tax (Rate) dated 30.04.2026 that Seeks to amend Notification No 9/2025 - Central tax (Rate) to align them with changes made vide Finance Act, 2026

|

|

|

|

|

|

Central Board of Direct Taxes issued Circular no. 4 of 2026 dated 31.03.2026 regarding Document Identification Number (DIN).

|

|

|

|

|

|

Press release ID 2279424 dated 30.06.26

|

The Government had earlier provided a full Customs Duty exemption on imports of critical petrochemical products till 30th June 2026, as a temporary and targeted relief in view of the conflict in West Asia and the consequent disruptions in global supply chains.

|

The exemption was provided to ensure sufficient availability of petrochemicals in the domestic market as Indian petroleum companies had been asked to concentrate on the production of LPG during this period. As the situation is gradually normalizing, to ensure a smooth and non-disruptive transition for the affected sectors, it has been decided to extend the said exemption by a further period of 15 days, that is, till 15th July 2026.The list of products covered remains the same as notified earlier.

|

The Government remains committed to supporting India's manufacturing sector. As before, the exemption is expected to benefit a wide range of sectors dependent on petrochemical feedstock and intermediates, including plastics, packaging, textiles, pharmaceuticals, chemicals, automotive components and other manufacturing segments. This will also provide relief to consumers of final products.

|

Link to previous press note issued:

|

|

|

|

|

|

Threshold limit for Inter-state movement of goods is Rs. 50,000/-. However, for intra-state movement of goods there is exceptional higher limit of Rs.1,00,000/- in some states.

|

Here is the list of e-way bill limit state-wise.

|

|

|

|

|

|

GSTN Advisory no. 666 dated 01.07.2026

|

It is informed that the Aggregate Annual Turnover (AATO) functionality is currently being upgraded to enable automatic updation of AATO as subsequent returns are filed post amendment window. As this enhanced functionality is being deployed from 1st July 2026, the window for amendment of AATO by taxpayers for FY 2025-26 has been revised on the GST Portal.

|

GSTN had earlier issued an advisory dated 02 May 2022 regarding the functionality for amendment of Aggregate Annual Turnover (AATO) on the GST Portal, which was applicable for AATO till FY 2024-25. Under the said advisory, taxpayers were provided the facility to amend their turnover during the month of May.

|

In continuation thereof, it is informed that the timelines for submission of amendment applications and verification of amended AATO details by Tax Officers, in respect of FY 2025-26, have been revised.

|

To ensure greater consistency, accuracy, and uniformity in the reporting of AATO across various modules of the GST Portal, certain system-level enhancements are being implemented. Consequently, the revised timelines for amendment of AATO for FY 2025-26 by the taxpayers and subsequent action by the tax officers are as under:

|

AATO Amendment Application window for FY 2025-26

01 July to 31 July 2026

|

Review by jurisdictional Tax officer

01 Aug to 15 Aug 2026

|

Accordingly, the facility for amendment of AATO, which was earlier available during May as per the previous advisory, shall now be made available from 01 July to 31 July 2026 for FY 2025-26. The amended AATO details will be available for review of Tax Officers from 01 Aug to 15 Aug.

|

All taxpayers are requested to take note of the revised timelines and carefully review the AATO details while submitting the amendment application and ensuring that the amended details are accurate before submission.

|

In case of any difficulty or concern, taxpayers are advised to raise a grievance through the Self-Service Portal available on the GST Portal, along with all relevant details, to facilitate prompt and effective resolution.

|

|

|

|

|

|

|

|

GSTN Advisory no. 665 dated 01.07.2026

|

Gross and Net GST revenue collections for the month of June, 2026

|

|

|

|

|

|

2. GST in Media - Council meeting

|

|

|

|

|

GSTN is taking downtime to enhance its services on the GST Portal on 27.06.2026 from 12:00 AM onwards until 2:30 am of 27.06.2026.

|

|

We shall be enhancing services on the GST portal on : 27th June’26 12:00 AM onwards. GST Portal services will not be available until 27th June’26 02:30 AM. The inconvenience caused is regretted.

|

|

|

|

|

|

|

|

|

|

|

GSTN is taking downtime to enhance its services on the GST Portal on 12.06.2026 from 11:30 AM onwards until 7:30 am of 13.06.2026.

|

We shall be enhancing services on the GST portal on : 12th June’26 11:30 PM onwards. GST Portal services will not be available until 13th June’26 07:30 AM. The inconvenience caused is regretted.

|

|

|

|

|

|

|

|

GSTN Advisory no. 664 dated 17.06.2026

|

Reference is invited to the GSTN Advisory dated 20.05.2026 regarding enhancements in the e-Way Bill system, wherein it was informed that “Ship-to GSTIN” shall be mandatorily captured in Bill-to/Ship-to transactions. It was also clarified that where the consignee is an unregistered person, the value “URP” shall be entered in the Ship-to GSTIN field.

|

In this regard, representations have been received from trade, ERP vendors, GSPs, ASPs, private IRPs and other stakeholders seeking clarification on the applicability of the said requirement in cases where e-Way Bill is generated along with e-Invoice or by using IRN. Representations have also been received regarding the Voluntary Closure of e-Way Bill facility and its impact on portal-based and API-based operations.Accordingly, an advisory has been issued to apprise stakeholders of the corresponding changes introduced in the e-Invoice API, e-Way Bill by IRN API and EWB Closure API. It has also been informed that the aforesaid changes have been made available in the Sandbox environment for testing and system preparedness. The changes are scheduled to be implemented in the Production environment with effect from 1st August, 2026.

|

All concerned stakeholders may accordingly be advised to access the advisory through the link given below and undertake necessary testing, system changes and preparedness within the prescribed timeline.

|

|

|

|

|

|

|

|

GSTN Advisory no. 663 dated 09.06.2026

|

Reference is invited to the GSTN Advisory dated 20.05.2026, wherein it was informed that the following functionalities would be implemented in the E-Way Bill system with effect from 15th June, 2026:

|

- Mandatory capture of "Ship To GSTIN" in Bill-To/Ship-To transactions; and

- Voluntary Closure of E-Way Bill functionality.

Representations have been received from trade and industry seeking extension of the implementation timeline, citing the requirement of system changes, testing, API/ERP readiness and master data updation across the taxpayer ecosystem.

|

In view of the above, and to facilitate smooth transition and adequate preparedness by taxpayers, GSPs, ERP providers and other stakeholders, it has been decided to extend the implementation timeline for both the above functionalities.

|

Accordingly, the mandatory capture of "Ship To GSTIN" in Bill-To/Ship-To transactions and the Voluntary Closure of E-Way Bill functionality shall be implemented with effect from 1st August, 2026, instead of 15th June, 2026.

|

Taxpayers, GSPs, ERP providers and other stakeholders are advised to complete the necessary system changes, testing and operational preparedness before the revised implementation date.Thank you,

Team GSTN

|

|

|

|

|

|

|

|

GSTN is taking downtime to enhance its services on the GST Portal on 06.06.2026 from 01:30 AM onwards until 3:30 am of 06.06.2026.

|

|

We shall be enhancing services on the GST portal on : 6th June’26 01:30 AM onwards. GST Portal services will not be available until 6th June’26 03:30 AM.The inconvenience caused is regretted.

|

|

|

|

|

|

|

|

|

|

|

GSTN is taking downtime to enhance its services on the GST Portal on 05.06.2026 from 12:00 AM onwards until 4:00 am of 05.06.2026.

|

|

We shall be enhancing services on the GST portal on : 5th June’26 12:00 AM onwards. GST Portal services will not be available until 5th June’26 04:00 AM. The inconvenience caused is regretted.

|

|

|

|

|

|

|

|

|

|

|

GSTN is taking downtime to enhance its services on the GST Portal on 04.06.2026 from 12:00 AM onwards until 1:30 am of 04.06.2026.

|

|

We shall be enhancing services on the GST portal on : 4th June’26 12:00 AM onwards. GST Portal services will not be available until 4th June’26 01:30 AM. The inconvenience caused is regretted.

|

|

|

|

|

|

|

|

|

|

|

GSTN Advisory no. 662 dated 01.06.2026

|

Please click on the link below to view the gross and net GST revenue collections for the month of May, 2026.

|

|

|

|

|

|

|

|

GSTN is taking downtime to enhance its services on the GST Portal on 02.06.2026 from 12:00 AM onwards until 6:30 am of 02.06.2026.

|

|

We shall be enhancing services on the GST portal on : 2nd June’26 12:00 AM onwards. GST Portal services will not be available until 2nd June’26 06:30 AM. The inconvenience caused is regretted.

|

|

|

|

|

|

|

|

|

|

|

GSTN planned Disaster Recovery Drill at GST Portal on 29.05.2026 from 11:00 PM onwards until 5:00 am of 30.05.2026.

|

|

A Disaster Recovery switchover is scheduled on 29/5/2026 at 11:00 PM. GST system services will remain unavailable until 05:00 AM on 30/5/2026. Kindly plan your activities accordingly. Inconvenience caused is regretted.

|

|

|

|

|

|

|

|

|

|

|

GSTN is taking downtime to enhance its services on the GST Portal on 22.05.2026 from 02:00 AM onwards until 3:30 am of 22.05.2026.

|

|

We shall be enhancing services on the GST portal on : 22nd May’26 2:00 AM onwards. GST Portal services will not be available until 22nd May’26 03:30 AM. The inconvenience caused is regretted.

|

|

|

|

|

|

|

|

|

The Union government on Tuesday granted a six-month extension to the tenure of Central Board of Direct Taxes (CBDT) Chairman Ravi Agrawal till December 2026.

|

The 1988 batch IRS officer was to retire on Tuesday(June 30).

|

The Appointments Committee of the Cabinet (ACC) in an order on Tuesday said it has approved "re-appointment" of Ravi Agrawal as Chairman, CBDT on contract basis for a period of six months with effect from 01.07.2026 or until further orders, whichever is earlier, on the terms and conditions applicable to re-employed central government officers, in relaxation of the Recruitment Rules.

|

He was made chief of CBDT, the policy-making body for the Income Tax Department, for a one-year term in June 2024. His tenure was extended by a year in June 2025.

|

The CBDT is headed by a chairman and can have up to six members, who are equivalent to special secretary rank.

|

Source: The Economic Times

|

|

|

|

|

|

|

|

Manner of issuance of invoice

|

Rule 48 of the Central Goods and Services Tax Rules, 2017 (CGST Rules) provides for the ‘manner of issuing invoice’.

|

Sub-rule (1) of rule 48 states that the invoice should be raised in triplicate on supply of goods and as per sub-rule (2) the invoice should be raised in duplicate on supply of services.

|

On 13th of December, 2019 sub-rule (4), (5) and (6) was inserted to rule 48 providing the additional condition for the manner of issuance of invoice. The newly inserted sub-rules are re-produced below:

|

“(4) The invoice shall be prepared by such class of registered persons as may be notified by the Government, on the recommendations of the Council, by including such particulars contained in FORM GST INV-01 after obtaining an Invoice Reference Number by uploading information contained therein on the Common Goods and Services Tax Electronic Portal in such manner and subject to such conditions and restrictions as may be specified in the notification.

|

(5) Every invoice issued by a person to whom sub-rule (4) applies in any manner other than the manner specified in the said sub-rule shall not be treated as an invoice.

|

(6) The provisions of sub-rules (1) and (2) shall not apply to an invoice prepared in the manner specified in sub-rule (4).”.

|

Sub-rules (1) and (2) is re-produced below:

|

Sub-rule (1) The invoice shall be prepared in triplicate, in the case of supply of goods, in the following manner, namely,-

|

(a) the original copy being marked as ORIGINAL FOR RECIPIENT;

|

(b) the duplicate copy being marked as DUPLICATE FOR TRANSPORTER; and

|

(c) the triplicate copy being marked as TRIPLICATE FOR SUPPLIER.

|

Sub-rule (2) The invoice shall be prepared in duplicate, in the case of the supply of services, in the following manner, namely,-

|

(a) the original copy being marked as ORIGINAL FOR RECIPIENT; and

|

(b) the duplicate copy being marked as DUPLICATE FOR SUPPLIER.

|

As per above stated rules, the Government will select certain class of registered persons on the recommendations of the GST Council who shall be uploading the information of the invoice in Form GST INV-01 in the common electronic portal subject to certain conditions and restrictions and get invoice reference number and shall incorporate it in the invoice.

|

In the event the selected class of registered person fails to upload the information in the common electronic portal then the invoice raised shall not be treated as an invoice. In other words, the invoice raised by certain class of registered person, not having invoice reference number incorporated on it shall not be considered as a valid invoice. If this be the case then one of the condition prescribed u/s 16(2)(a) to claim input tax credit by the recipient person will not get fulfilled and as a reason his claim of input tax credit would be rejected. .

|

The selected class of registered person who meets the compliance of sub-rule (4) are not required to fulfill the requirement of sub-rule (1) and (2) i.e. invoice need not be prepared in triplicate or duplicate on the supply of goods or services as the case may be.

|

Selected class of registered persons

|

CBIC has notified the class of registered person vides Notification no. 70/2019 – Central Tax dated 13.12.2019 that shall be generating invoice reference number. As prescribed in the notification, the registered persons whose aggregate turnover in a financial year exceeds one hundred crore rupees shall do the compliance of rule 48(4) effective from 01.04.2020.

|

In the month of March, 2020 a Notification no. 13/2020 – Central Tax dated 21.03.2020 was published superseding notification no. 70/2019 supra, and extending the date of implementation of rule 48(4) to 01.10.2020.

|

E-invoicing: 500 crore turnover- 01.10.2020

|

On 30.07.2020 the said threshold limit was increased to 500 crores vide notification no. 61/2020 – Central Tax.

|

On 30th September, 2020 Notification no. 70/2020 – Central Tax was published to amend the Notification no. 13/2020 – Central dated 21.03.2020 so as to substitute, - a) ‘financial year’ with ‘any preceding financial year from 2017-18 onwards and b) ‘goods or services or both to a registered person’, the words ‘’or exports’ shall be inserted.

|

E-invoicing was implemented on 01.10.2020. As a first time relief a special procedure was prescribed for period from 01.10.2020 to 31.10.2020 whereby it was allowed to generate e-invoice within thirty days from the date of such invoice.

|

E-invoicing: 100 crore turnover- 01.01.2021

|

On 10th November, 2020, notification no. 88/2020 – Central Tax was published to lower the threshold to 100 crore effective from 01.01.2021.

|

E-invoicing: 50 crore turnover- 01.04.2021

|

On 8th March, 2021, notification no. 05/2021 – Central Tax was published to lower the threshold to 50 crore effective from 01.04.2021.

|

A notification no. 23/2021 – Central Tax dated 01.06.2021 was published to amend first para of the notification no. 13/2020 – Central Tax dated 21.03.2020. After the words “notified registered person, other than” the words “a government department, a local authority,’

|

E-invoicing: 20 crore turnover- 01.04.2022

|

On 24th February, 2022 a notification no. 01/2022 – Central Tax was published to lower the threshold limit to 20 crore effective from 01.04.2022.

|

E-invoicing: 10 crore turnover- 01.10.2022

|

On 01st August, 2022 a notification no. 17/2022 – Central Tax was published to lower the threshold limit to 10 crore effective from 01.10.2022.

|

E-invoicing: 5 crore turnover- 01.08.2023

|

On 10th May, 2023 a notification no. 10/2023 – Central Tax was published to lower the threshold limit to 5 crore effective from 01.08.2023

|

Summary of the date-wise change in the e-invoice compliance

|

Few important points given below :

|

Threshold / Aggregate turnover for the purpose of checking if you fall under the compliance of rule 48(4)

|

- Aggregate value of all taxable suppliers,

- exempt suppliers

- exports of goods or services or both

- interstate supplies of persons having same PAN

To be computed on all India basis.

|

- value of inward supplies on which reverse charge applies

- all taxes viz IGST, CGST, SGST, UTGST

It is 64 character hash algorithm containing GSTIN of supplier, invoice number, document type and financial year.

|

Quick Reference code consist of

|

- GSTIN of supplier

- GSTIN of buyer

- Invoice number,

- Invoice date

- Invoice value

- Number of line items

- HSN of major commodity as per value

- Unique IRN (Hash)

Applicability of e-invoicing

|

- B2B invoices

- Export invoices

- Credit notes

- Debit notes

Non- applicability of e-invoice

|

- B2C supplies

- Bill of entry /imports

- SES Units

- Insurer or a banking company or a financial institution, including a non-banking financial company.

- Goods transporter agency supplying services in relation to transportation of goods by road in a goods carriage.

- Suppliers of passenger tra nsportation service

- Suppliers of services by way of submission to exhibition of cinematograph films in multiplex screens

Modes of generation of e-invoice

|

- Through GST System – Invoice Registration Portal (IRP) – Machine to Machine

- Small Taxpayers – NIC –GePP – On System, & GePP-off System

- API Based, SMS Based, Mobile App based, offline tool (JSON file).

- GSP Based & Web Based

Cancellation of E-invoice

|

- IRN generated on the portal can be cancelled within 24 houres

- IRN cannot be cancelled, if valid E-Way Bills exists for that IRN

- Once e-invoice (IRN) is cancelled, then one more IRN cannot be generated on same invoice number

|

|

|

|

|

|

|

Issuing demand notice on the account of mismatch between GST Returns (GSTR) are daily routine practice for the Revenue Officers, which can be settled/argued by reverting it with proper reconciliation along with its proper documentary evidences. Especially, after the 50th meeting of GST Council and issuance of eight new circulars; present matter is in the spotlight nowadays. Elaborating on this issue, present write-up shall attempt to analyze the legal sustainability of such situation affecting the substantial right of ITC of the any taxpayer/assessee. Before that, it also provides, brief glimpses of department’s intention, practical aspects and judicial perspective.

|

Background with Legal Interpretation

|

Going beyond the diminishing limits of Input Tax Credit (ITC) claims; Central Board of Indirect Taxes and Customs (CBIC) has nought down the bottleneck by restricting the same as per the figures showing in static GSTR-2B i.e., auto-drafted ITC statements. Accordingly, w.e.f. 01 January 2022, ITC can be availed up to the extent it is reflected in GSTR-2B only. Therefore, while filing GSTR-3B i.e., details of outward & inward supplies with its payment of taxes; a taxpayer/assessee is eligible to claim ITC in terms of values communicated in GSTR-2B only and rest of the ITC showing in dynamic GSTR-2A could not be considered during discharging the exigible GST at the time of filing of GSTR-3B. With the objective to further tightening the impugned restriction, in the 50th meeting the GST Council has recommended to introduce system-based intimation through a new form i.e., DRC-01C by incorporating Rule 88D in CGST Rules, 2017which will help in reducing ITC mismatches/ misuses.

|

Accordingly, it can be emerged that in future, every taxpayer shall be served with a demand notice on the account of mismatch happened in GSTR-2B & 3B, on mandatory basis.

|

As we all know, values reflected in the static GSTR-2A/2B are the inward supplies which is an auto-drafted supplies/ITC statement communicated by the vendors or suppliers of a taxpayer/assessee and from the year 2022, ITC can be claimed as per the same restrictively, immaterial of the fact that valid reconciliation is available. Previously, the taxpayer has the limited liberty to submit, for claiming credit which were not shown in GSTR-2A by submitting proper backing of the ITC claims like, CA certificate or vendor declaration etc. Before moving forward, it is pertinent to highlight the common reason behind the mismatch of GSTR-2A/2B & 3B, which is non-compliance happened on the part of the vendor who has not properly furnished details in their GSTR-1 . Due to such mistake the same could not reflected in the GSTR-2A (up to 31st Dec. 2021) or 2B (after 01st Jan. 2022) and consequently, it can’t be used by the taxpayer while filing the GSTR-3B.

|

Therefore, it can be understood that after Jan. 2022, even though the assessee has all the valid documents for claiming the credit (not ineligible or blocked ITC) for substantiating the eligibility of the ITC, it cannot be available to the taxpayer as its inward suppliers has not complied with the provided procedure. It is doubtless that it is impossible to track each and every vendor/supplier that it’s filing its returns properly or not. However, no other option is left behind to the taxpayers to check such compliances, currently few software like, Bill Mantra etc. are available in the market which can assist such tracking.

|

Litigation on Eligibility of ITC

|

The question of ITC claim as a vested right were always in litigation, one of the best defence used by the petitioners is ‘substantive right of credit cannot be denied on procedural lapse grounds.' Likewise, after the introduction of GST regime; fight of eligible/ineligible credit is again remains one of the most litigative issue, but now tip of the weight scale is going towards revenue department. As the government always attempts to restrict the credit to its utmost level which affects the taxpayer drastically.

|

Before going into the legal credibility of aforesaid concern, it is imperative to clarify that, even if the department’s approach is to minimize the ITC claim by raising the eligibility standards; but in few cases, courts has allowed benefit accepting the ground of technical glitches or procedural lapse. One of the best live examples, is reopening of GST portal for filing TRAN-1 and its extension allowed by Hon’ble Supreme Court (SC) in the case of UOI v. Filco Trade Centre Pvt. Ltd. which was referred by several taxpayers seeking similar benefit highlight the vested right of ITC claims and got consequential benefit granted by the Hon’ble Apex Court.

|

ITC is Vested Right or a Concession granted by the Government

|

Irrespective of the pre & post GST era, right of ITC is urged as a substantial vested right which should not be denied on mere ground of non-compliance/mistake committed by other person or other aspects like procedural/technical lapse. Such averment has been addressed in few cases pertains to erstwhile regime; for example, ALD Automotive Pvt. Ltd. v. CTO (now upgraded as Asst. Commissioner) wherein, fiscal legislation of Tamil Nadu VAT Act, 2006 was challenged. Hearing both the side, the Division Bench of Hon’ble Supreme Court has dismissed the petition by concluding that ITC is not a vested right and concluded it to be a concessional benefit which can be strictly constructed in terms of the conditions enumerated in the statutory provisions. Similar stand was also taken in case of Jayam & Co. v. Asst. Commissioner & Anr.

|

In line of the above judicial precedents, it can be traced that though it’s a trite law that ITC claim could be considered as substantive right, but not as vested right as it’s a concession granted by the legislature which has full authority to restrict the same with pre-conditions required to be fulfilled.

|

Legal Sustainability: Denial of ITC of Eligible Credit

|

It is relevant to clarify that though it’s a trite law that ‘no innocent should be punished’. However, in present scenario; the taxpayer is losing its eligible ITC due to the default of its vendor, which may also affect the principle of natural justice.

|

Here it is necessary to note that such plea can be accepted in terms of the stipulated eligibility criteria in the applicable provisions only, as discussed in preceding paras. The said significance is also explained in one of the latest CBIC Circular No. 197/09/2023- GST dated 17 July 2023 wherein, it specifically clarified that GST refund claims pending for adjudication shall be examined in terms of GSTR-2B (w.e.f. 01 Jan. 2022).

|

Closing Statement and Suggestive Measures

|

Likewise, the burning issue of fake invoices, demand on the account of mismatch in GSTRs are trigger points for the revenue department which will be used grape each defaulter with the stick of compliance. From the side of the department superlative efforts are being made to reduce scope for the taxpayer for claiming credit and the judiciary is also operating in hand in hand. Hence, it is better to set a goal have Zero Non-Compliance and maintain records of the inward as well as outward supplies. For achieving such target, it is suggested to cautiously check credibility of the inward supplies after a particular interval of time through paid software or to the least by GSTIN portal search taxpayers. Additionally, a mechanism can be designed wherein, certificate/declaration can be taken by them showing the tax payment on which ITC can be claimed by a taxpayer.

|

In terms of Rule 36(4) of CGST Rules and clarified in Circular No. 193/05/2023-GST dated 17 July 2023; additional credit was allowed to the extent not exceeding 20% (09 Oct. 2019 to 31 Dec. 2019), 10% (01 Jan. 2020 to 31 Dec. 2020) & 5% (01 Jan. 2021 to 31 Dec. 2021) respectively, with proper declaration. Further, it may be noted that before 08 Oct. 2019, there were no such restriction.

|

GST Council has proposed some changes/improvements for the smooth and restrictive enforcement of GST laws. The same would be given effect through the relevant circulars/ notifications/ law amendments which alone shall have the force of law.

|

https://billmantra.com/ui/login/#/

|

Misc. Application Nos.1545-1546/2022 in SLP(C) No. 32709-32710/2018

|

Civil Appeal Nos. 10412-10413/2018

|

Civil Appeal Nos. 8077-8146/2016

|

|

|

|

|

|

5 Lawgics by Ms.Nidhi Aggarwal

|

|

Ms. Nidhi Aggarwal is delighted to present GST Notes/Law in a simplified manner under the title “ Lawgics ”. The note is prepared in a series of PDFs encompassing GST Law and the interpretations thereof in simple manner. The author with a great vision to spread complex GST law in a simple manner amongst the taxpayers, tax professionals, students and knowledge seeker is presenting the Lawgics in piecemeal at regular interval.

|

|

|

|

|

|

|

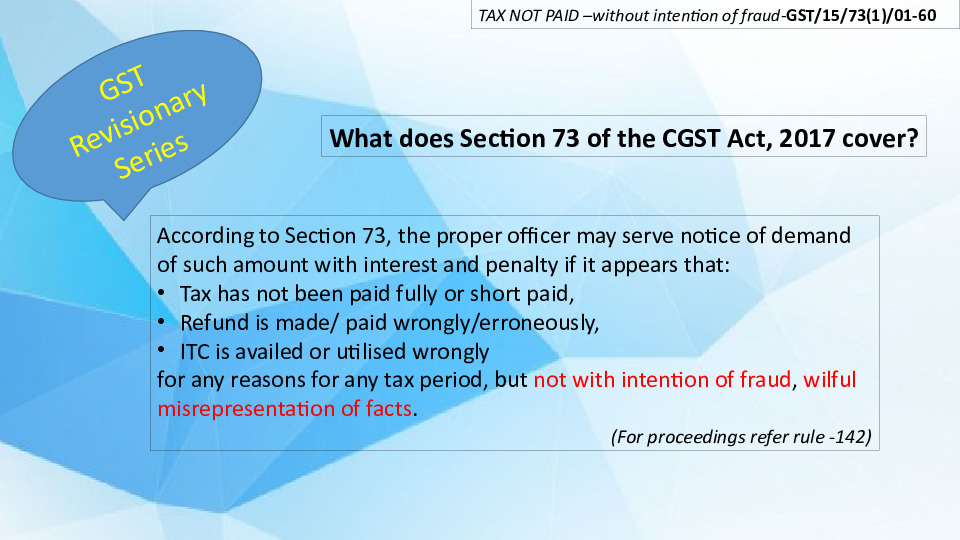

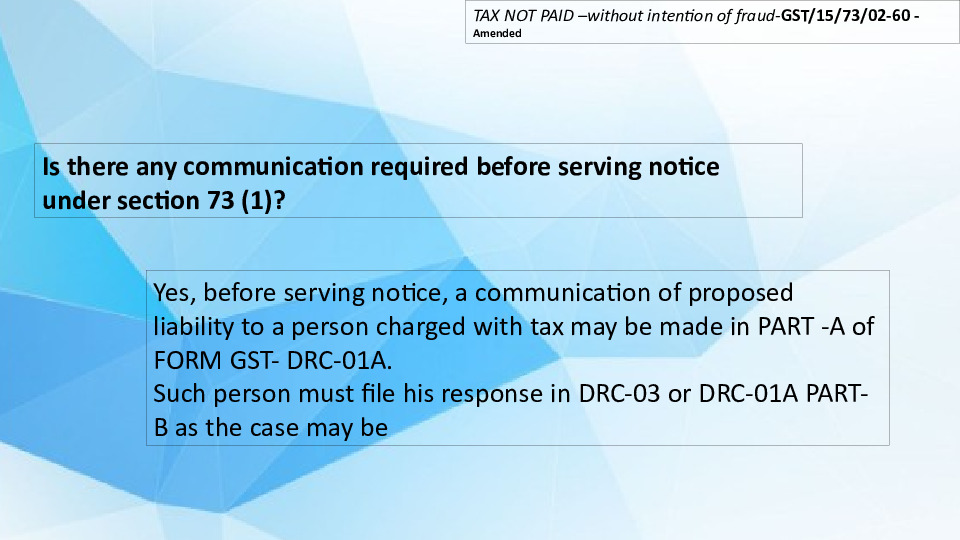

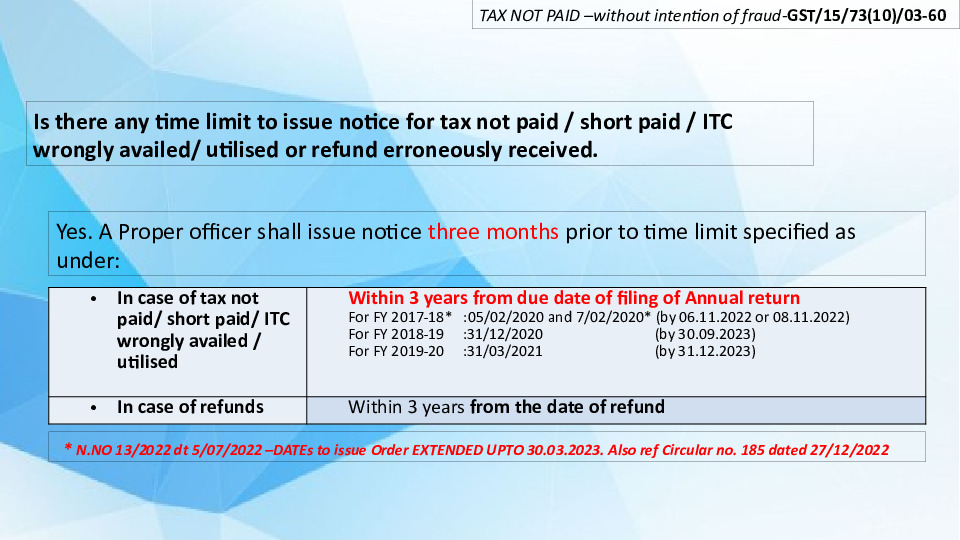

6. GST Notes by CMA Anil Sharma

1) Shri CMA Anil Sharma, Shri CMA Gurdev Singh Saini and Smt. CMA Bhawna Sharma posted Chapter-15 containing CGST Act in simple language in PPT format. This is to make dealers, professionals, academicians, students etc. understand the basics of GST laws. Each Chapter in CGST Act, 2017 is explained in the form of Slides as given below for easy understanding of the Act:

|

Chapter-15 slides given below:-

|

|

|

|

|

|

|

|

|

|

|

You wish to publish your Article?

|

If you wish to share your article with maximum readers then please send the article at taxupdate.otu@gmail.com. We shall publish it with all due credit to you.

|

|

|

|

|

|

|

Hope the above updates is of use to you. Please share your input and feedback at taxupdate.otu@gmail.com

|

|

|

|

|

|

|

Visit our website

|

OTU provides you

|

- Articles on various topics

|

|

- Media - GST, Income Tax & Press R.

|

|

- Notes / Newsletter at 149/ p.a.

|

|

|

|

|