|

|

|

Newsletter no. 75 dated 13.03.2023

|

|

|

|

|

|

This website contains information about recent changes mainly in GST laws. It also contains Articles on various topic in GST. Please visit the website and read more.

|

|

|

|

Index

|

2. State Circular/State Budget

|

|

6. Book by CMA Anil Sharma

|

|

|

|

|

|

|

|

GSTN is taking downtime to enhance its services on the GST Portal on 27.06.2026 from 12:00 AM onwards until 2:30 am of 27.06.2026.

|

|

We shall be enhancing services on the GST portal on : 27th June’26 12:00 AM onwards. GST Portal services will not be available until 27th June’26 02:30 AM. The inconvenience caused is regretted.

|

|

|

|

|

|

|

|

|

|

|

GSTN is taking downtime to enhance its services on the GST Portal on 12.06.2026 from 11:30 AM onwards until 7:30 am of 13.06.2026.

|

We shall be enhancing services on the GST portal on : 12th June’26 11:30 PM onwards. GST Portal services will not be available until 13th June’26 07:30 AM. The inconvenience caused is regretted.

|

|

|

|

|

|

|

|

CBIC issued clarification via F. No. CBIC-20016/75/2025-GST dated 25.09.2025 on requirement of separate GST registration for importers storing goods in Warehouses in other States

|

|

|

|

|

|

|

|

Department of Trade and Taxes, New Delhi issued Circular No. F.IV/42/T&T/Admn./Misc./2025/8464-67 date 23.07.2025

|

Several instances have come to the notice of the Competent Authority that GSTIs/ Field Functionaries to whom the physical verification visit of 'High Risk Score' Registration Application are marked, are not submitting the verification reports on time and in some cases the report is submitted with remarks that the address mentioned in the ARN is not in their jurisdiction.

|

The Competent Authority has taken a serious note of the aforementioned conduct of officials and directed that it is imperative upon the GSTI to whom the visit is marked, to conduct the visit and submit the report timely.

|

Any dereliction shall be viewed adversely and invite strict action as per rules.

|

|

|

|

|

|

|

|

Directorate General of Goods & Services Tax (DGGST), South Zone, Chennai, is conducting a nationwide study on demand notices and adjudication orders to strengthen the working regime and promote a more trader-friendly ecosystem. The objective is to identify procedural gaps, understand root causes, and recommend reforms to enhance fairness, consistency, and administrative efficiency in adjudication.

|

This initiative is also aligned with the broader goal of improving the Ease of Doing Business, by ensuring that tax administration practices are transparent, predictable, and minimally intrusive for taxpayers.

|

As part of this study, a virtual interactive session has been scheduled with your association and members on 23.07.2025 (Wednesday) at 3:0 PM. The objective of the session is to solicit feedback and practical suggestions from trade and industry stakeholders, based on your experience with Show Cause Notices (SCNs), personal hearings, and adjudication orders.

|

You are requested to kindly:

|

- Share the names and contact details of participants from your association who will join the meeting;

- Come prepared with inputs highlighting specific concerns or patterns observed in SCNs and adjudication orders.

- Supplement the discussion, if possible, with case examples or material that could add depth and value to the deliberations.

The link for the virtual meeting will be shared with the confirmed participants in due course. We look forward to your valuable contribution to this important initiative.

|

|

|

|

|

|

|

|

Government of National Capital Territory of Delhi, Department of Trade & Taxes New Delhi issued a Circular No. F.3(640)/GST/P&R/2025/348-55 dated 13.06.2025 prescribing Guidelines for Mandatory Conduct of Personal Hearings through Virtual Mode in All Proceedings under the Delhi GST Act, 2017 and the Rules framed thereunder.

|

A personal hearing is a vital procedural safeguard that ensures individual(s) or entities facing tax demands or penalties are granted a fair opportunity to be heard and to present their case. Provisions under sub-section (4) of section 75, sub-section (3) of section 126, and sub-section (8) of section 107 of the Delhi GST Act, 2017, explicitly mandate the granting an opportunity of a personal hearing before any adverse order is passed by the Proper Officer or the Appellate Authority. These provisions underscore the necessity of adhering to the principles of natural justice in both letter and spirit.

|

2. There Department of Trade and Taxes, Government of NCT of Delhi is committed for fostering transparency, efficiency, and ease of compliance in tax administration. In pursuit of these objectives and as a step towards establishing faceless and technology-driven mechanism under GST the Department has decided to make it mandatory to conduct all personal hearings in GST proceedings through virtual mode, thereby ensuring greater accessibility and streamlined processes for all taxpayers.

|

3. Accordingly, to ensure transparency, efficiency, and strict adherence to the principles of natural justice, the following guidelines are being issued to outline the procedures and protocols to be followed during virtual hearings. All Proper Officers, including Appellate Authorities-hereinafter referred to as "the Authority" appointed and functioning under the provisions of the Delhi GST Act, 2017 and the Rules framed there under, are hereby directed to comply with the following guidelines.

|

- a. In any proceedings, all the personal hearings shall be mandatorily be conducted in virtual mode and no person shall be required to appear in person for personal hearing.

- b. Such virtual hearings shall be conducted through available applications such as WEBEX, Google-Meet etc. The date and time of hearing along with a link for the virtual hearing shall be informed well in advance to the taxpayer or authorized representative through the registered email id and/ or mobile number.

- c. In the said e-mail, Authority shall also provide details of the staff/officer who would provide assistance to the party, for conducting the virtual hearing. This link shall not be shared with any other person without the consent of the said officer.

- d. The taxpayer or his authorized representative shall download the required application on their computer system /laptop/ mobile phone beforehand and be ready with appropriate network connectivity and bandwidth for the virtual hearing and join the same at the time and date allocated to them.

- e. The taxpayer or authorized representative shall be required to submit his vakalatnama or authorization letter along with the copy of his photo-id card and provide contact details well in advance to the said officer, devoid of which he shall not be allowed to represent the taxpayer.

- f. The virtual hearings shall be conducted from office of the concerned Authority only.

- g. All persons participating in the virtual hearing shall be appropriately dressed and shall maintain the decorum and dignity at all times.

- h. The submissions made by the taxpayer or his authorized representative during the virtual hearing shall be recorded as "Record of Personal Hearing" by the concerned Authority on online PH module and after generating it in pdf format, Authority shall put his signature and stamp thereon. A copy of above-said "Record of Personal Hearing" shall be shared on the registered email id provided by the taxpayer or his authorized representative in Para e hereinabove.

- i. In case of any adjournment, a notice of adjournment shall also be sent through BO Portal mentioning details of next date of hearing.

- j. If the taxpayer /authorized representative prefer the Authority to consider any document including additional documents during the virtual hearing, he may do so sending the scanned copy of such self-attested document via official mail to the Authority concerned before virtual hearing.

- k. In cases of requirement of submission of physical set of documents the same shall be submitted after due attestation by the taxpayers or his authorized representative, to the Authority concerned during working hours.

- l. The proceedings of virtual hearing as well as documents submitted in the above manner shall be deemed to be valid document/ record for the purpose of CGST/DGST Act and Rules made there under read with section 4 of the Information Technology Act, 2000.

- m. It is made clear that while conduct of personal hearing through virtual mode is being made mandatory, there may yet be rare and accentuating circumstances on the part of the taxpayer or his authorized representative on account of which this cannot be done. Each such request shall be approved only by the Zonal Incharge/ officer concerned after recording the reasons for the same.

4. Any officer representing the Department may also participate in the virtual hearing through video conferencing, as required.

|

5. Difficulties faced, if any, in the implementation of this circular may be informed at the earliest.

|

This issues with the prior approval of Commissioner (Trade and Taxes).

|

|

|

|

|

|

|

|

Department of Trade & Taxes, Vyapar Bhawan I.P. Estate, New Delhi (Law & Judicial Branch) issued Circular No. L&J/Misc/T&T/2024-25/285-86 dated 03.06.2025 announcing Summer break from 02.06.2025 to 30.06.2025

|

As an annual feature, the Sales Tax Bar Association will observe summer break w.e.f. 02.06.2025 to 30.06.2025. Accordingly, it has been decided that the officers of the department will not pass any ex-parte order on account of non-appearance of Counsel /Advocates during this period. However, if any Counsel/ Advocate chose to appear on his own or in response to the earlier fixation of any notice, he/she may do so. This dispensation will not apply to the remand assessment cases, registration cases and any other cases or legal requirement which will be getting time barred during this period.

|

The spare time available with the Appellate Authorities/ Objection Hearing Authority/ Ward Officers may be utilized for finalisation of important matters like weeding out files and clearance of pendency of other works.

|

This issues with prior approval of the Competent Authority.

|

|

|

|

|

|

|

|

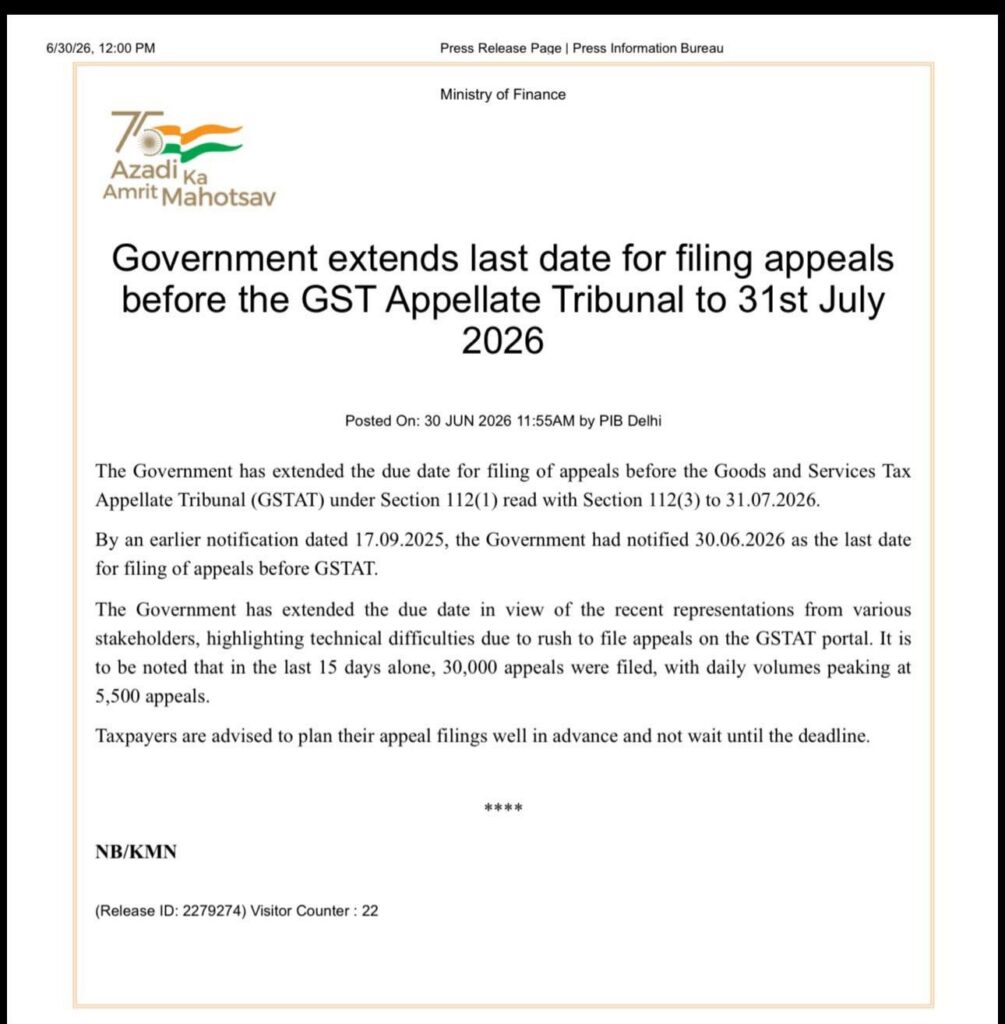

Centre has extended the last date for filing appeals before the Goods and Services Tax Appellate Tribunal (GSTAT) to July 31, 2026, giving taxpayers an additional month to submit their cases after a surge in filings led to technical difficulties on the GSTAT portal.

|

The extension applies to appeals filed under Section 112(1) read with Section 112(3) of the Goods and Services Tax (GST) law.

|

The revised deadline replaces the earlier cut-off of June 30, 2026, which had been notified by the government on September 17, 2025.

|

The decision follows recent representations from various stakeholders who flagged technical issues arising from a rush of appeals being filed on the GSTAT portal ahead of the deadline.

|

While noting that the original due date had been notified well in advance in September 2025, the government said filing activity had intensified sharply in recent weeks. It said 30,000 appeals were filed in the last 15 days alone, with daily filings touching a peak of 5,500 appeals.

|

Advising against eleventh-hour filings, the government urged taxpayers to complete their appeal submissions well in advance to ease pressure on the GSTAT portal.

|

The GST Appellate Tribunal serves as the first judicial appellate forum for taxpayers seeking to challenge orders issued by GST authorities after the disposal of their first appeals.

|

Source: The Economic Times

|

|

|

|

|

|

|

|

|

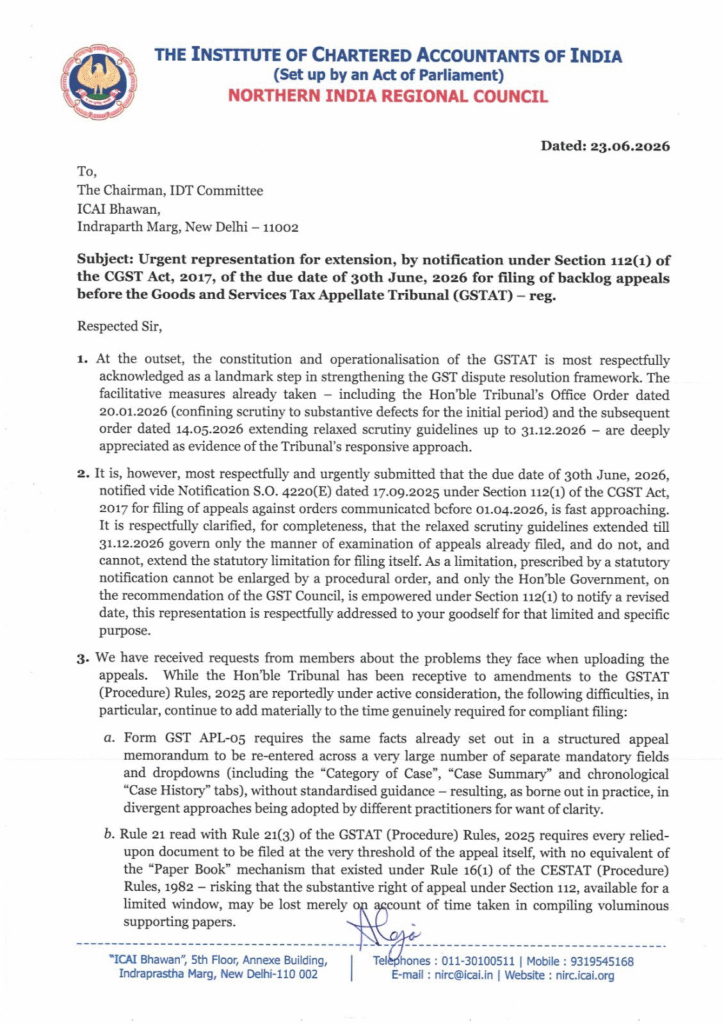

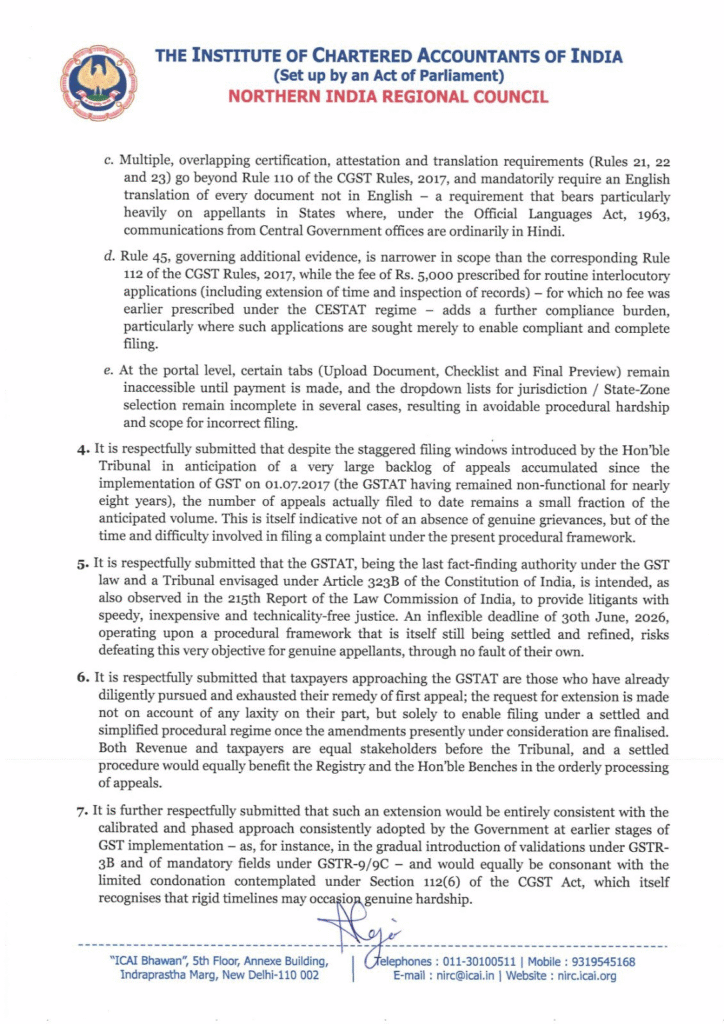

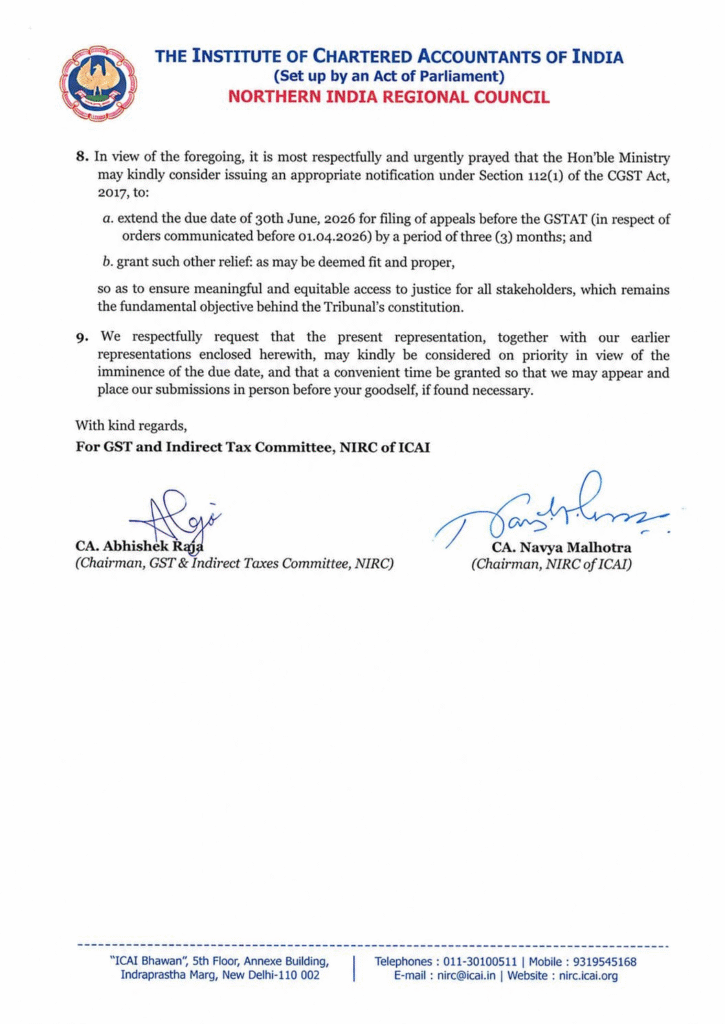

GST & IDT Committee has requested the Chairman, IDT Committee, ICAI, New Delhi to urgently represent before the respective forums for the date extension of GSTAT, i.e., 30-Jun-2026.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Tata Steel Limited said tax authorities have filed an appeal seeking restoration of penalties worth Rs. 368.72 crore that were earlier dropped in a GST adjudication order, even as proceedings on the underlying demand remain stayed by the Jharkhand High Court, according to a stock exchange filing.

|

"One June 16, 2026, the Assistant Commissioner, Division-I, CGST & Central Excise , Jamshedpur, Jharkhand filed an appeal before the Commissioner (Appeals) of CGST & Central Excise, Ranchi against the above-mentioned Adjudication Order dated December 18, 2026, to the extend that the Adjudicating Authority has dropped the penalty amounting to Rs. 3,68,72,21,158/-," Tata Steel said in its exchange filing.

|

The appeal, filed on June 16 by the Assistant Commissioner, CGST & Central Excise, Jamshedpur, challenges the December 18, 2025, adjudication order to the extent it waived the penalty.

|

The original show-cause notice, issued in June 2025, proposed disallowance of input tax credit for FY 2018-19 to FY 2022-23, with an aggregate GST demand of about Rs. 1,007.55 crore. Of this, Tata Steel said it has already paid Rs. 514.19 crore in the normal course, leaving an alleged exposure of Rs. 493.35 crore.

|

In December 2025, the adjudicating authority confirmed the tax demand of Rs. 493.35 crore, imposed a penalty of Rs. 638.83 crore and applicable interested, while dropping an earlier proposed penalty of Rs. 368.72 crore. Tata Steel subsequently moved the Jharkhand High Court, which granted a stay on all further proceedings in March 2026.

|

"This matter is, inter-alia, contingent upon the final adjudication of the issue concerning the issuance of show cause notices for multiple periods, which is presently sub judice before the High Court," Tata Steel said.

|

Tata Steel added that it has a good case on merit and hence will contest the same before the Appellate Authority within the statutory timelines, noting that the development has no impact on its financial or operational position, arising from the said appeal.

|

Source: The Economic Times

|

|

|

|

|

|

|

|

With the June 30 deadline for filing legacy appeals before the Goods and Services Tax Appellate Tribunal (GSTAT) fast approaching , tax professionals, chartered accountants and industry bodies have urged the Finance Ministry to extend the filing window, warning that persistent technical glitches on the GSTAT portal could prevent thousands of taxpayers from filing their appeals before the deadline.

|

The demand comes as taxpayers seek to file appeals arising from nearly nine years of litigation accumulated during the period when the Tribunal remained non-operational. Experts said the combination of a massive backlog, voluminous documentation and continuing portal-related issues has significantly constrained taxpayers' ability to meet the deadline.

|

According to Aditya Singhania, Founder of Trackase, the backlog is estimated at nearly four lakh to 4.5 lakh legacy appeals, while only around 36,929 appeals have been filed nationalwide so far.

|

"The ground reality is deeply concerning. Against an anticipated backlog of nearly four to four and a half lakh appeals accumulated over nine years of the Tribunal's non-operationality, only around 36,929 appeals have been filed nationally as of now," Singhania said.

|

He attributed the slow pace of filings to the teething troubles of the newly launched e-filing portal, including server time-outs, authentication challenges, payment gateway reconciliation issues and a filing structure that requires considerable time and effort to navigate.

|

Experts cite portal hurdles, record backlog

According to experts and representations submitted to the Finance Ministry, taxpayers continue to face multiple technical issues on the GSTAT portal, including session expiry, repeated login failures., Aadhaar authentication problems, Digital Signature Certificate (DSC) validation failures, payment reconciliation delays and incomplete integration between the Goods and Services Tax Network (GSTN) and the GSTAT portal.

|

Experts said taxpayers are also required to retrieve and compile extensive records accumulated over several years, including adjudication orders, invoices, reconciliations, e-way bills, ledger extracts and other supporting documents, making the filing process particularly time-consuming.

|

CA Nitin Bansal, State-President, BJP CA Cell Haryana, said the Finance Ministry has received several representations highlighting the practical challenges taxpayers are facing in filing appeals before the Tribunal.

|

"With the Tribunal becoming operational after nearly nine years, taxpayers must now prepare and file a substantial backlog of appeals within a limited window, many involving voluminous, multi-year records, even as the GSTAT e-filing portal continues to stabilise," Bansal said.

|

He added that extending the deadline would be revenue-neutral as the mandatory pre-deposit and other conditions would remain unchanged while ensuring genuine taxpayers are not denied their appellate remedy because of circumstances beyond their control.

|

Over-time extension sought

CA Sonu Goel, Chairman, Panipat Branch of the Institute of Chartered Accountants of India (ICAI), said a one-time extension would ensure disputes are decided on their merits rather than procedural constrints.

|

"One-time extension would safeguard taxpayers' right to appeal, uphold the principles of natural justice, and ensure that dispute are decided on merits rather than being defeated by procedural or technological constraints. This pragmatic relief would further reinforce the Government's commitment to ease of doing business while maintaining certainty and confidence in the GST ecosystem," Goel said.

|

Parag Mehta, Partner at N.A. Shah Associates LLP, said the portal continues to experience issues ranging from login failures and incorrect fee calculations to disappearing data.

|

"Considering the fact that the portal is not fully supporting the filing process and the number of appeals filed remains significantly lower than expected, the deadline should be extended. GSTAT is an important appellate remedy and taxpayers should not be deprived of that opportunity," Mehta said.

|

Bas association flags nationwide concerns

The Sales Tax Bar Association has also written to the Finance Ministry seeking an extension of the filing deadline, stating that taxpayers and tax professional across the country continue to face significant practical and technical difficulties while filing appeals through the GSTAT portal.

|

In its representation, the association said the present limitation period covers appellate orders accumulated over nearly nine years when the Tribunal remained non-functional, requiring taxpayers to retrieve historical records and prepare detailed documentation within a limited period.

|

The association highlighted recurring issues including server interruptions, repeated Aadhaar authentication and DSC validation failures, payment gateway reconciliation delays, manual duplication of information already available on the GSTN portal and challenges in uploading voluminous records.

|

It warned that if the deadline is not extended, thousands of taxpayers could lose the opportunity to pursue their statutory appeals because of technological and procedural constraints, potentially leading to avoidable litigation before various High Courts.

|

Prabhat Ranjan, Senior Director at Nexdigm, said extending the filing deadline has become "the need of the hour".

|

"The appellate process should be about the actual merits of the issues between both parties and not technical questions of delay. This is a taxpayer-friendly measure that will make GST dispute resolution processes more fair and credible," he said.

|

As of publication, the government has not announced any extension of the June 30 deadline for filing legacy GSTAT appeals. While the GSTAT has extended the period for relaxed scrutiny of filed appeals until December 31, 2026 , tax professionals, industry experts and representative bodies continue to seek a one-time extension of the filing deadline, arguing that additional time would enable taxpayers to exercise their statutory right of appeal without affecting revenue, as the mandatory pre-deposit requirements would continue to apply.

|

Source: The Economic Times

|

|

|

|

|

|

|

|

Businesses shifting their principal place of business to a new GST jurisdiction will not have to restart pending tax proceedings with the Central Board of Indirect Taxes and Customs (CBIC) clarifying that the new jurisdictional authority will take over and complete all ongoing cases from the stage at which they were left, reported PTI.

|

The clarification comes after the CBIC received references from field formations seeking guidance on the validity of proceedings and the authority responsible for handling cases when a registered taxpayer changes jurisdiction because of a shift in its principal place of business.

|

Under the circular, any action or proceeding - including investigation, audit, show cause notice or adjudication under the Central GST law - initiated by the tax officer having jurisdiction over the registered taxpayer at the time the action was undertaken (transferor jurisdiction authority) will remain valid even if the taxpayer subsequently shifts to another tax jurisdiction (transferee jurisdictional authority).

|

"The transferee jurisdictional authority shall act upon, give effect to, and proceed on the basis of such earlier valid action taken by the transferor jurisdictional authority, as if it had itself initiated the same," the CBIC said in the circular.

|

The indirect tax board further clarified that if any fresh issue comes to the notice of the earlier jurisdictional authority after the taxpayer has shifted, the tax officer should intimate the new jurisdictional officer for appropriate action.

|

"Where the taxable person migrates to another jurisdiction during the pendency of any action or proceeding initiated by the transferor jurisdictional authority, the transferee jurisdictional authority shall take over and conclude the same from the stage at which it stood at the time of migration/ transfer," the CBIC circular said.

|

The new jurisdictional officer will also have the authority to initiate and conclude any consequential proceedings arising from the case.

|

Rajat Mohan, Managing Partner at AMRG Global, said the clarification addresses a key procedural gap under the GST regime.

|

"By clearly defining the responsibilities of transferor and transferee authorities, CBIC has removed ambiguity that often resulted in jurisdictional objections and delays in adjudication," Mohan said.

|

Source: The Times of India

|

|

|

|

|

|

|

|

The Hon’ble Allahabad High Court in Ashish Tyagi v. Director General of GST Intelligence & Ors. allowed the habeas corpus petition and declared the arrest and consequent detention of the assessee under Section 132 of the Central Goods and Services Tax Act, 2017 (“the CGST Act”) as illegal, on the ground that the arrest memo neither contained the specific grounds of arrest nor disclosed the place of arrest, and the grounds of arrest did not bear the mandatory CBIC-Document Identification Number (“DIN”), thereby violating the mandate of law and the safeguards laid down by the Hon’ble Supreme Court in D.K. Basu v. State of West Bengal . Accordingly, the Court directed the immediate release of the assessee, while granting liberty to the Revenue to proceed afresh strictly in accordance with law.

|

- Mr. Ashish Tyagi (“the Petitioner”) was arrested by the officers of the Directorate General of GST Intelligence, Ghaziabad (“the Respondent”) for alleged offences under Section 132(1)(a), Section 132(1)(f) and Section 132(1)(i) of the CGST Act. The grounds of arrest were dated December 10, 2025.

- The Petitioner was thereafter remanded to judicial custody by the Special Chief Judicial Magistrate, Meerut vide order dated February 18, 2026 passed in Case No. 2122 of 2025 (Union of India v. Ashish Tyagi).

- The Petitioner contended that neither were the grounds of arrest mentioned in the arrest memo nor were they supplied as an annexure thereto, in clear violation of Circular No. 02/2022-23 issued by the CGST Department, which mandates communication of the grounds of arrest.

- It was further contended that the arrest memo merely recorded that the grounds of arrest were “explained” to the arrestee, without any recital indicating that the grounds were actually supplied to the Petitioner. Moreover, columns (i) to (iv) of the jamatalashi (personal search memo) were left blank and the Petitioner’s signatures were obtained thereon mechanically.

- The Petitioner also urged that the arrest memo did not disclose the place of arrest and that the Remand Magistrate failed to consider these discrepancies while granting remand, rendering the arrest, detention and remand illegal.

- The Respondent filed a counter affidavit; however, it could not rebut the submissions of the Petitioner by placing any material or document on record.

- Aggrieved by the illegal arrest and detention, the Petitioner filed a habeas corpus writ petition before the Hon’ble Allahabad High Court seeking a declaration that the arrest, detention and subsequent remand were unconstitutional, illegal and arbitrary, and praying for release forthwith.

Whether the arrest and consequent detention of the Petitioner under Section 132 of the CGST Act can be sustained when the arrest memo neither contains the specific grounds of arrest nor discloses the place of arrest, and the grounds of arrest do not bear the mandatory CBIC-DIN?

|

The Hon’ble Allahabad High Court in Writ Petition No. 509 of 2026 held as under:

|

- Observed that, the arrest memo did not disclose the place of arrest of the Petitioner, which is in violation of the law laid down by the Hon’ble Supreme Court in D.K. Basu v. State of West Bengal .

- Noted that, the grounds of arrest dated December 10, 2025 did not bear any CBIC-DIN, and the Petitioner was merely made to endorse on the arrest memo that he had received the arrest memo along with the grounds of arrest and that he had informed his friend about his arrest through a mobile phone call.

- Noted that, the submission of the Petitioner that, in terms of Circular No. 02/2022-23 issued by the CGST Department, every document is required to bear a CBIC-DIN, remained uncontroverted by the Respondent, who failed to place any material on record to rebut the allegations.

- Held that, the Petitioner has been illegally detained in violation of the mandate of law, and accordingly, the arrest and detention of the Petitioner are declared illegal and the Petitioner is directed to be released forthwith.

- Directed that, it shall, however, remain open to the Respondent to proceed against the Petitioner afresh, strictly in accordance with law.

The power of arrest under GST flows from Section 69 of the CGST Act, which empowers the Commissioner to authorise the arrest of a person where he has “reasons to believe” that such person has committed specified offences under Section 132 of the CGST Act. Section 69(2) of the CGST Act, read with Article 22(1) of the Constitution of India, casts a mandatory obligation on the arresting officer to inform the arrested person of the grounds of arrest and to produce him before a Magistrate within twenty-four hours. These safeguards are not empty formalities but constitutional imperatives, as repeatedly emphasised by the Hon’ble Supreme Court since D.K. Basu v. State of West Bengal , which prescribed, inter alia, the preparation of a proper arrest memo recording the time and place of arrest, duly attested and countersigned.

|

Insofar as the DIN requirement is concerned, the CBIC, vide Circular No. 122/41/2019-GST dated November 05, 2019, read with Circular No. 128/47/2019-GST dated December 23, 2019, mandated electronic generation and quoting of a DIN on all communications, including those issued during investigation such as search authorisations, summons, arrest memos and inspection notices. Significantly, the said Circular categorically provides that any specified communication which does not bear a DIN shall be treated as invalid and shall be deemed to have never been issued. The Hon’ble Supreme Court in Pradeep Goyal v. Union of India also underscored the importance of the DIN mechanism as a measure to ensure transparency and accountability in tax administration. The present ruling applies this discipline to arrest documentation as well, holding that grounds of arrest not bearing a CBIC-DIN cannot satisfy the mandate of law.

|

Further, the CBIC, vide Instruction No. 02/2022-23 dated August 17, 2022, laid down detailed guidelines for arrest and bail in relation to offences under the CGST Act, requiring that the grounds of arrest be explained to the arrested person and recorded in the arrest memo. Subsequently, pursuant to the judgment of the Hon’ble Supreme Court in Radhika Agarwal v. Union of India , the CBIC issued Instruction No. 01/2025-GST (Inv.) dated January 13, 2025, mandating that the grounds of arrest must be furnished to the arrested person in writing, as an annexure to the arrest memo, and an acknowledgement thereof obtained. In Radhika Agarwal (supra), the Hon’ble Supreme Court held that the ratio of Pankaj Bansal v. Union of India and Prabir Purkayastha v. State (NCT of Delhi) , requiring written communication of the grounds of arrest, applies with equal force to arrests under the Customs and GST laws, failing which the arrest itself stands vitiated.

|

On a pari materia footing, the Hon’ble Delhi High Court in Kshitij Ghildiyal v. Director General of GST Intelligence, Delhi declared an arrest by DGGI officers illegal where the grounds of arrest were not communicated to the arrestee in writing, and directed his release. The present decision of the Hon’ble Allahabad High Court adds a significant dimension to this line of authority by holding that even where an endorsement of receipt of the grounds of arrest is obtained, the absence of a CBIC-DIN on such grounds, coupled with blank columns in the search memo and non-disclosure of the place of arrest, vitiates the arrest in its entirety.

|

The takeaway for the Department is that procedural safeguards surrounding arrest under GST, viz. furnishing of written grounds of arrest bearing a valid DIN, complete and contemporaneous arrest documentation, and adherence to the D.K. Basu guidelines, are mandatory and non-negotiable, and any breach thereof would render the arrest and consequent remand illegal, notwithstanding the gravity of the alleged offence. For taxpayers and arrestees, the ruling reaffirms that habeas corpus remains an efficacious remedy where curable procedural lapses cross the threshold into violations of constitutional safeguards, although the Revenue retains liberty to proceed afresh in accordance with law.

|

|

|

|

|

|

|

|

The Hon’ble Gauhati High Court in M/s Metal Syndicate and Another v. The Union of India & Ors. set aside the Order-in-Original and the Order-in-Appeal confirming GST demand of Rs. 78,70,952/- along with interest and equivalent penalty, and held that a bona fide purchasing dealer cannot be denied Input Tax Credit (“ITC”) merely on account of the supplier’s failure to deposit the tax collected with the Government. The Court reiterated that the Department’s remedy in such circumstances lies against the defaulting supplier and not against the genuine recipient, who has discharged all statutory obligations.

|

M/s Metal Syndicate (“the Petitioner”), a proprietorship firm based in Silchar, Assam, engaged in trading of scrap/waste batteries, purchased goods from suppliers based in Kolkata during the Financial Years 2017-18 and 2018-19. The Petitioner received the goods along with proper tax invoices and made payments, including applicable GST, through banking channels. ITC was availed and utilized strictly in accordance with Section 16(2) of the Central Goods and Services Tax Act, 2017 (“the CGST Act”), and GSTR-1 and GSTR-3B returns were duly filed within the prescribed time.

|

The Directorate General of GST Intelligence (“DGGI”), Guwahati Zonal Unit, issued summons alleging that the Petitioner had availed ineligible ITC on the strength of invoices issued without actual receipt of goods. The Petitioner appeared before the authorities on April 05, 2019, and submitted all relevant documents including GSTR-1, GSTR-3B and purchase invoices. A search was subsequently conducted at the Petitioner’s business premises on July 09, 2019, during which no incriminating material was recovered or seized.

|

Thereafter, a Show Cause Notice (“SCN”) dated July 28, 2022 was issued alleging wrong availment and utilization of ITC of Rs. 78,70,952/- in violation of Section 16(2)(a) and (b) of the CGST Act. Vide Order-in-Original No. 22/GST/AC/SIL/2023-24 dated February 19, 2024, the Assistant Commissioner confirmed the demand comprising IGST of Rs. 47,12,010/-, CGST of Rs. 15,52,967/- and SGST of Rs. 16,05,975/- for the period July 2017 to March 2019, along with interest under Section 50 of the CGST Act and an equivalent penalty of Rs. 78,70,952/- under Section 74(1) read with Section 122 of the CGST Act and Section 20 of the Integrated Goods and Services Tax Act, 2017. The appeal preferred by the Petitioner was rejected vide Order-in-Appeal dated February 14, 2025.

|

Aggrieved, the Petitioner approached the Hon’ble Gauhati High Court by way of a writ petition challenging both the impugned orders.

|

Petitioner’s Contentions:

|

- The Petitioner had purchased goods from registered suppliers, received valid tax invoices and discharged the full consideration (including GST) through banking channels, thereby complying with all conditions of Section 16(2) of the CGST Act.

- The sole basis for denial of ITC was the alleged failure of the suppliers to discharge their tax liability — a circumstance entirely beyond the Petitioner’s control.

- No effective opportunity of hearing was afforded, and the SCN was not uploaded on the GST portal; notices were served manually beyond the date of hearing.

- The controversy stood squarely covered by the Division Bench ruling of the Hon’ble Gauhati High Court in National Plasto Moulding v. State of Assam , which in turn relied on the Hon’ble Delhi High Court decision in On Quest Merchandising India Pvt. Ltd. v. Government of NCT of Delhi .

WhetherITC can be denied to a bona fide purchasing dealer solely on account of the supplier’s failure to deposit the tax collected with the Government, where the recipient has otherwise complied with all the statutory conditions prescribed under Section 16(2) of the CGST Act?

|

The Hon’ble Gauhati High Court in W.P.(C) No. 2960/2026 held as under:

|

- Observed that the Petitioner had purchased goods from registered suppliers, received tax invoices, made payments including GST through proper banking channels and claimed ITC after complying with the statutory requirements prescribed under Section 16(2) of the CGST Act.

- Noted that both the counsel for the Petitioner as well as the Department were in consensus that the issue involved stood squarely covered by the Division Bench ruling in National Plasto Moulding (supra), wherein the Court, relying on the Delhi High Court decision in On Quest Merchandising India Pvt. Ltd. (supra), held that a purchasing dealer cannot be punished for the act of the selling dealer where the latter has failed to deposit the tax collected.

- Held that where a purchasing dealer has entered into bona fide transactions with a registered supplier and has complied with the statutory requirements, denial of ITC solely on account of the supplier’s failure to deposit tax with the Government would not be justified. The remedy of the Department, in such circumstances, lies against the defaulting supplier and not against the bona fide recipient.

- Quashed the impugned Order-in-Original dated February 19, 2024 and the Order-in-Appeal dated February 14, 2025.

- Directed that the Department shall be at liberty to proceed against the Petitioner in accordance with law in the event materials surface indicating that the transactions in question were not bona fide or were entered into in collusion with the suppliers.

Section 16 of the CGST Act lays down the eligibility and conditions for availing ITC. Specifically, Section 16(2)(c) prescribes that no registered person shall be entitled to ITC unless the tax charged in respect of the supply has been actually paid to the Government, either in cash or by utilization of ITC. This provision has consistently been a flashpoint of litigation, as it effectively transfers the consequences of the supplier’s non-compliance onto the genuine recipient, who has no statutory mechanism or practical means to monitor or compel the supplier to deposit the tax collected with the exchequer.

|

The present ruling reaffirms the well-settled jurisprudential principle that the law cannot impose an impossible burden of compliance on a bona fide recipient. The Hon’ble Delhi High Court in On Quest Merchandising India Pvt. Ltd. (supra) had, while dealing with the pari materia provision under Section 9(2)(g) of the Delhi Value Added Tax Act, 2004, read down the said provision and held that denial of ITC to a bona fide purchaser would be violative of Article 14 of the Constitution. The Hon’ble Supreme Court dismissed the Revenue’s Special Leave Petition against the said ruling on January 10, 2018, thereby giving finality to the principle.

|

The same view has been consistently followed across various jurisdictions:

|

- The Hon’ble Calcutta High Court in Suncraft Energy Pvt. Ltd. v. Assistant Commissioner of State Tax (Bagnan Charge)held that the recovery action must first be initiated against the defaulting supplier and only in exceptional circumstances (such as where the supplier is missing, has been deregistered, or where collusion is established) can recovery be effected from the recipient. The Hon’ble Supreme Court dismissed the Special Leave Petition filed by the Revenue against the said order.

- The Hon’ble Madras High Court in D.Y. Beathel Enterprises v. State Tax Officerset aside the assessment order denying ITC to the recipient on the ground that no enquiry was conducted against the defaulting supplier despite the recipient having discharged the consideration including GST.

- The Hon’ble Allahabad High Court in Malik Traders v. State of U.P.and the Hon’ble Kerala High Court in Diya Agencies v. State Tax Officer, while broadly affirming the conditions of Section 16(2)(c), have also held that the recipient’s claim cannot be rejected on the basis of GSTR-2A mismatches alone, without verifying the supplier’s compliance.

It is, however, pertinent to mention that the Hon’ble Kerala High Court in Nahasshukoor v. Assistant Commissioner, while recognising the practical challenges during the initial phase of GST rollout, upheld the constitutional validity of Sections 16(2)(c) and 16(4) of the CGST Act.

|

Until such pronouncement, the ruling in Metal Syndicate (supra), being a consistent reaffirmation of the bona fide recipient’s right to ITC, serves as a valuable precedent for genuine taxpayers facing identical demands. Recipients facing such proceedings should, as a matter of practice, maintain robust documentation — including tax invoices, e-way bills, transportation records, weighment slips, banking trail and acknowledgments of receipt of goods — to demonstrate the genuineness of their transactions. The Department’s right to proceed in cases involving collusion or fraudulent transactions remains preserved, and accordingly, the bona fide character of the transaction will continue to be the touchstone of every adjudication.

|

Accordingly, the question of the constitutional validity of Section 16(2)(c) — and by extension, the foundational right of a bona fide purchaser to avail ITC — remains open and pending adjudication at the highest judicial level.

|

|

|

|

|

|

|

|

The Hon’ble Madras High Court (Madurai Bench) in Tvl. Manickavasagam S. v. The Proper Officer/Commercial Tax Officer set aside the assessment order passed under Section 74 of the Tamil Nadu Goods and Services Tax Act, 2017 (“the TNGST Act”) pertaining to levy of GST on seigniorage fees and held that since the very incidence of tax itself is at large is pending before the Hon’ble Supreme Court of India, the matter is remanded for fresh consideration without imposing the customary condition of pre-deposit, with the further direction that the final orders shall be kept in abeyance and enforcement and further demand of any liability so determined shall await the outcome of the Supreme Court’s judgment.

|

Tvl. Manickavasagam S. (“the Petitioner”) was issued an assessment order in GST ASMT 15 Temporary ID: 332500004524 TMP/2020-2021, dated February 24, 2026 (“the Impugned Order”) by the Proper Officer/Commercial Tax Officer, Sivagangai (“the Respondent”) under Section 74 of the TNGST Act, 2017.

|

The subject matter of dispute pertained to the levy of GST on seigniorage fees, an issue which is presently pending adjudication before the Hon’ble Supreme Court of India.

|

The Petitioner had filed a reply to the show cause notice; however, the said reply was not considered by the Respondent while passing the Impugned Order.

|

Aggrieved, the Petitioner preferred a writ petition before the Hon’ble Madras High Court under Article 226 of the Constitution of India seeking quashing of the Impugned Order as illegal, arbitrary and against the principles of natural justice.

|

The Petitioner contended that the subject matter in dispute is pending before the Hon’ble Supreme Court of India and that the Hon’ble High Court has already held in earlier matters that the authorities shall await the orders of the Apex Court.

|

Per contra, the Revenue contended that the Hon’ble High Court has been directing the assessing authorities to complete the proceedings; however, the orders of the Appellate Authority were directed to be kept in abeyance until the orders are passed by the Hon’ble Supreme Court of India. The Revenue placed reliance on the orders of the Madras High Court in M/s. Marginal M Sand v. State Tax Officer andTvl. Rajapalayam Cement and Chemicals Limited v. Assistant Commissioner .

|

Whether the assessment order passed under Section 74 of the TNGST Act, 2017 levying GST on seigniorage fees, where the very incidence of tax itself is at large before the Hon’ble Supreme Court of India and where the Petitioner’s reply was not considered, can be sustained?

|

The Hon’ble Madras High Court (Madurai Bench) in W.P(MD) No. 14948 of 2026held as under:

|

- Observed that, while in earlier matters such as M/s. Marginal M Sand and Tvl. Rajapalayam Cement and Chemicals Limited, the Court had granted permission to the assessing authorities to complete the proceedings, it had simultaneously directed that final orders shall not be passed and that the authorities have to await the orders of the Hon’ble Supreme Court of India.

- Noted that, in the present case, although the order of assessment had been passed, the reply filed by the Petitioner was not considered by the Respondent, thereby violating the principles of natural justice.

- Held that, considering the fact that the very incidence of tax itself is at large, the Petitioner can be granted an opportunity to be heard afresh. Further, although the Court normally imposes a condition of deposit of 25% while granting such opportunity on equitable considerations, since in this case the very incidence of tax itself is at large, no such additional condition is imposed on the Petitioner.

- Directed that, the Impugned Order dated February 24, 2026 shall stand set aside and the matter shall stand remanded back to the file of the Respondent for fresh consideration. The Petitioner shall, within two weeks from receipt of a web copy of the order, file additional reply along with supporting documents and the Respondent shall consider the matter afresh; however, the final orders shall be kept in abeyance until the orders are passed by the Hon’ble Supreme Court of India.

- Further directed that, if the order on remand is in favour of the Petitioner, then there is no difficulty; however, if it results in the assessment of tax or imposition of penalty, the same shall be communicated to the Petitioner, but the enforcement and further demand of the liability so determined shall be kept in abeyance until the judgment of the Hon’ble Supreme Court of India. As and when the Hon’ble Supreme Court pronounces its judgment, the Petitioner shall be entitled to take further steps subject to the outcome of the said judgment.

Hence, the writ petition was allowed and the matter remanded back to the Assessing Officer for fresh consideration.

|

Section 74 of the CGST Act, 2017 (pari materia with Section 74 of the TNGST Act, 2017) empowers the Proper Officer to determine tax not paid, short paid, erroneously refunded or input tax credit wrongly availed or utilised by reason of fraud, wilful misstatement or suppression of facts to evade tax. It mandates the issuance of a show cause notice, consideration of the assessee’s reply, and a reasoned order — a quasi-judicial exercise where non-consideration of the assessee’s reply vitiates the order on the ground of violation of natural justice, as squarely demonstrated in the present case.

|

The issue of GST leviability on seigniorage fee/royalty paid to the State Government for extraction of minerals from mining/quarry leases is intrinsically linked to the larger question of whether royalty is in the nature of “tax”, which is presently pending before the Nine-Judge Constitution Bench of the Hon’ble Supreme Court in Mineral Area Development Authority v. Steel Authority of India. Pending the verdict, several High Courts have consistently directed that GST adjudication on royalty/seigniorage be held in abeyance to avoid prejudicing taxpayers.

|

The Hon’ble Madras High Court in A. Venkatachalam v. Assistant Commissioner (ST) had similarly kept orders of adjudication with respect to levy of GST on mining lease/royalty in abeyance and stayed recovery, until the Nine-Judge Constitution Bench in Mineral Area Development Authority decides the issue as to the nature of royalty.

|

In a pari materiaruling, the Hon’ble Telangana High Court in PLR-NCC-NECL (JV) v. Union of India granted interim stay on the order-in-original dated May 5, 2025, which had confirmed GST demand on amounts deducted towards royalty/seigniorage, District Mineral Foundation (DMF), and State Mineral Exploration Trust (SMET), reinforcing the consistent judicial trend of staying coercive recovery on this issue.

|

Further, the Andhra Pradesh Authority for Advance Ruling in Sudhakara Infratech ruled that an Excess Royalty Collection Contractor (ERCC) is not liable to discharge GST under forward charge on collection of royalty/seigniorage fee, District Mineral Foundation (DMF), Mineral Exploration and Research & Innovation Trust (MERIT) and similar statutory levies from mining/quarry leaseholders, lending support to the view that such statutory levies may not constitute a taxable “supply” within the meaning of the GST law.

|

The instant ruling is a welcome relief for taxpayers in the mining, quarrying, and allied sectors who continue to face assessment proceedings and coercive recovery actions on the disputed levy of GST on royalty/seigniorage fees. The Hon’ble Court’s nuanced approach — setting aside the order for non-consideration of the reply, dispensing with the otherwise mandatory 25% pre-deposit condition since the very incidence of tax is at large, and directing that enforcement of any future demand shall remain in abeyance until the Supreme Court’s verdict — strikes a fair balance between revenue interests and taxpayer protection. Taxpayers similarly placed may consider invoking writ jurisdiction to seek analogous protection, particularly where their replies have not been considered or where coercive recovery is being initiated pending the Supreme Court’s verdict.

|

|

|

|

|

|

|

|

The Hon’ble Madras High Court in P. Baskaran v. Deputy State Tax Officer set aside the order imposing interest and penalty under Section 74 of the Central Goods and Services Tax Act, 2017 (“the CGST Act”) and remanded the matter for fresh consideration on the applicability of Section 74, holding that the possibility of the Assessee establishing genuine supply of goods and that Section 74 was incorrectly invoked cannot be ruled out without affording the Assessee a reasonable opportunity to place material documents on record.

|

M/s. P. Baskaran (“the Petitioner”), a proprietary concern based in Salem, Tamil Nadu, was issued an order dated August 30, 2024 in FORM GST DRC-07 (Order Reference No. ZD330824291608Z) by the Deputy State Tax Officer (“the Respondent”) for the Financial Year 2018-19, imposing interest and penalty under Section 74 of the applicable GST enactments.

|

The Petitioner had availed Input Tax Credit (“ITC”) on inward supplies which was subsequently reversed; however, the Petitioner asserted that there was a genuine supply of goods and that the essential ingredients of Section 74 – namely fraud, wilful misstatement or suppression of facts – were not made out on the facts of the case.

|

Aggrieved by the impugned order on the ground of breach of principles of natural justice and erroneous invocation of Section 74, the Petitioner filed a writ petition under Article 226 of the Constitution of India before the Hon’ble Madras High Court praying for a writ of certiorari to quash the impugned order.

|

Whether the order imposing interest and penalty under Section 74 of the CGST Act, 2017 can be sustained when the Assessee has not been afforded a reasonable opportunity to place on record material documents to establish genuine supply of goods and to demonstrate that the ingredients of Section 74 are not made out?

|

The Hon’ble Madras High Court in W.P No. 18015 of 2026 and WMP. Nos. 19364 & 19367 of 2026 held as under:

|

- Observed that, the Input Tax Credit availed by the Petitioner has already stood reversed, and to that extent the interest of the Revenue is protected.

- Noted that, the Petitioner had contended that there was a genuine supply of goods and that the ingredients of Section 74 were not made out, whereas the Revenue submitted that since a reply to the show cause notice had been filed, no interference was warranted.

- Held that, the possibility of the Petitioner establishing that there was a genuine supply of goods and that Section 74 was incorrectly invoked cannot be ruled out without providing the Petitioner an opportunity to place material documents on record.

- Directed that, the impugned order is set aside to the limited extent of reconsideration of the invocation of Section 74, and a fresh order shall be passed within three months from the date of receipt of a copy of the order after granting a reasonable opportunity to the Petitioner.

Hence, the matter was remanded back to the assessing officer for fresh consideration.

|

Section 74 of the CGST Act, 2017 governs the determination of tax not paid, short paid, erroneously refunded, or input tax credit wrongly availed or utilised by reason of fraud, or any wilful misstatement, or suppression of facts to evade tax. The provision is jurisdictional in character and can be invoked by the Proper Officer only where any one or more of these aggravating ingredients is positively established. Where these ingredients are absent, the appropriate machinery is Section 73 of the CGST Act, which deals with cases not involving fraud, wilful misstatement, or suppression. The distinction is significant because Section 74 carries a longer limitation period of five years and attracts a higher quantum of penalty (equal to the tax) as compared to Section 73.

|

The present ruling reinforces a well-settled position that the adjudication process under the GST law is required to comply with the principles of natural justice. Where the Assessee contests not merely the quantum of demand but the very jurisdiction to invoke Section 74, it is incumbent upon the Proper Officer to permit the Assessee to lead documentary evidence – such as tax invoices, e-way bills, lorry receipts, weighment slips, bank statements, ledger extracts, and proof of receipt of goods – in support of the contention of genuine supply, before fastening enhanced liability and penalty.

|

The ruling is also significant in that the Hon’ble Court was conscious of safeguarding the Revenue’s interest. Since the disputed ITC already stood reversed, the Court restricted its interference only to the limited aspect of reconsidering the invocation of Section 74, thereby balancing the rights of the Assessee with the protection of public revenue.

|

Pari materia rulings on the requirement of opportunity and on the ingredients of Section 74:

|

- The Hon’ble Calcutta High Court in Suncraft Energy Private Limited v. Assistant Commissioner of State Tax , held that ITC cannot be denied to the bona fide recipient on the sole ground of mismatch with GSTR-2A or default by the supplier, without first conducting due enquiry against the supplier; the order was upheld by the Hon’ble Supreme Court in SLP (Civil) Diary No. 39332 of 2023.

- The Hon’ble Supreme Court in Commissioner of Central Excise v. HMM Limited , in the context of the pari materia provision of Section 11A of the Central Excise Act, held that the extended period of limitation and the attendant penalty cannot be invoked unless a positive finding of fraud, collusion, or wilful misstatement is recorded – a principle that has been consistently followed under GST jurisprudence.

- The Hon’ble Madras High Court in Tvl. Diamond Shipping Agencies Pvt. Ltd. v. Assistant Commissioner (ST) and a series of similar writ petitions has repeatedly set aside ex parte and non-speaking orders under Section 74 and remanded the matters for fresh adjudication, holding that where the Assessee credibly asserts genuine supply, an opportunity to place documentary evidence cannot be denied.

- The Hon’ble Karnataka High Court in LC Infra Projects Pvt. Ltd. v. Union of India and other similar rulings have emphasised that recourse to Section 74 must be supported by specific allegations and material disclosing fraud, wilful misstatement or suppression – a mechanical invocation without such material is liable to be quashed.

On the contrary, in cases where the Assessee has been afforded multiple opportunities and has failed to substantiate its claim, Courts have declined to interfere. For instance, the Hon’ble Madras High Court in numerous decisions has held that where the show cause notice clearly sets out the allegations, the Assessee has filed a reply, and a personal hearing has been afforded, the writ jurisdiction will not be exercised merely to grant another round of adjudication – the Assessee would have to pursue the statutory appellate remedy under Section 107 of the CGST Act.

|

The takeaway for the trade and industry is twofold. First, where invocation of Section 74 is contested, the Assessee must promptly file a comprehensive reply to the show cause notice supported by documentary evidence demonstrating the genuineness of inward supplies, receipt of goods, and payment of consideration through banking channels. Second, a writ remedy may be sustainable where the adjudicating authority has not permitted the Assessee to lead such evidence and has mechanically invoked Section 74 by treating mere reversal of ITC as conclusive proof of fraud or suppression – the two are conceptually distinct, and the latter requires an independent finding supported by material on record.

|

|

|

|

|

|

|

|

Press release ID 2279424 dated 30.06.26

|

The Government had earlier provided a full Customs Duty exemption on imports of critical petrochemical products till 30th June 2026, as a temporary and targeted relief in view of the conflict in West Asia and the consequent disruptions in global supply chains.

|

The exemption was provided to ensure sufficient availability of petrochemicals in the domestic market as Indian petroleum companies had been asked to concentrate on the production of LPG during this period. As the situation is gradually normalizing, to ensure a smooth and non-disruptive transition for the affected sectors, it has been decided to extend the said exemption by a further period of 15 days, that is, till 15th July 2026.The list of products covered remains the same as notified earlier.

|

The Government remains committed to supporting India's manufacturing sector. As before, the exemption is expected to benefit a wide range of sectors dependent on petrochemical feedstock and intermediates, including plastics, packaging, textiles, pharmaceuticals, chemicals, automotive components and other manufacturing segments. This will also provide relief to consumers of final products.

|

Link to previous press note issued:

|

|

|

|

|

|

|

|

Press release ID 2279409 dated 30.06.2026

|

|

In a major operation the officers of the Directorate of Revenue Intelligence (DRI) successfully dismantled a trans-border gold smuggling syndicate and seized 15 kg foreign-origin smuggled gold, valued at approximately Rs. 21.40 crore, operating from Delhi.

|

|

|

DRI officers intercepted an international courier consignment originating from Thailand at Courier Terminal, Delhi. The consignment was in the name of a firm linked to a foreign national.

|

A meticulous examination of the consignment declared as "worn gear", led to the recovery of eight disc-shaped pieces of foreign-origin gold, each weighing 1.5 kg, ingeniously concealed inside gear parts. In total, 12 kg smuggled foreign-origin gold was recovered from the courier consignment.

|

Simultaneous searches conducted at the residence of the intended recipient and the alleged mastermind resulted in the recovery of two more identical disc-shaped pieces of foreign-origin gold, each weighing 1.5 kg.

|

Four persons, including the mastermind, who is a repeat offender, and a foreign national have been arrested in relation with the case.

|

Preliminary investigations also reveal that crypto-currency was being used to transfer the money across borders to finance the smuggling.

|

|

|

|

|

|

|

|

Source: Press release id 2279274 dated 30.06.26

|

The government has extended the due date for filing of appeal before the Goods and Services Tax Appellate Tribunal (GSTAT) under section 112(1) read with section 112(3) to 31.07.2026.

|

The government has extended the due date in view of the recent representation from various stakeholders , highlighting technical difficulties due to rush to file appeals on the GSTAT portal. It is to be noted that in the last 15 days alone, 30,000 appeals were filed, with daily volumes peaking at 5,500 appeals.

|

|

Taxpayers are advised to plan their appeal filings well in advance and not wait until the deadline.

|

|

|

|

|

|

|

|

|

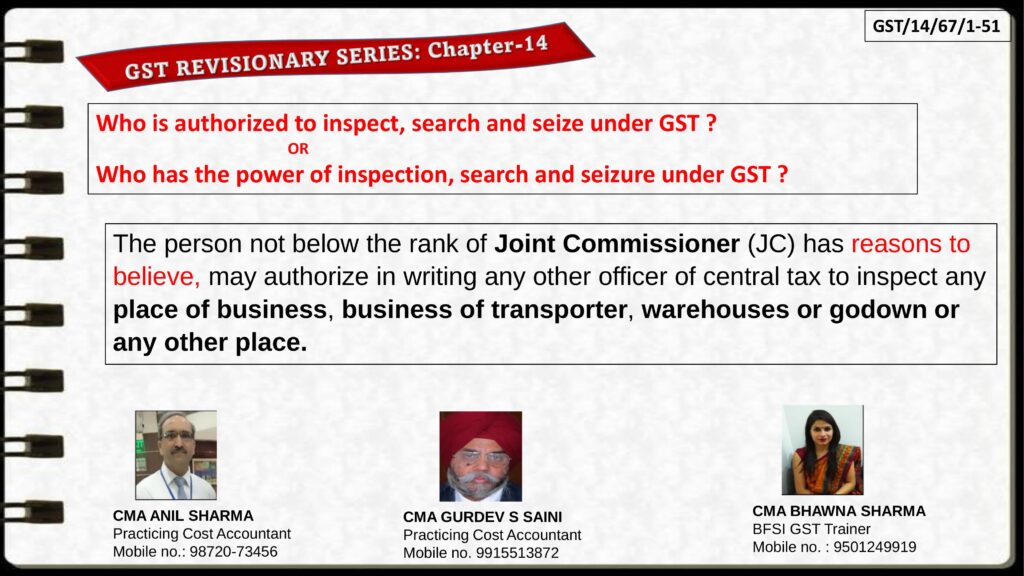

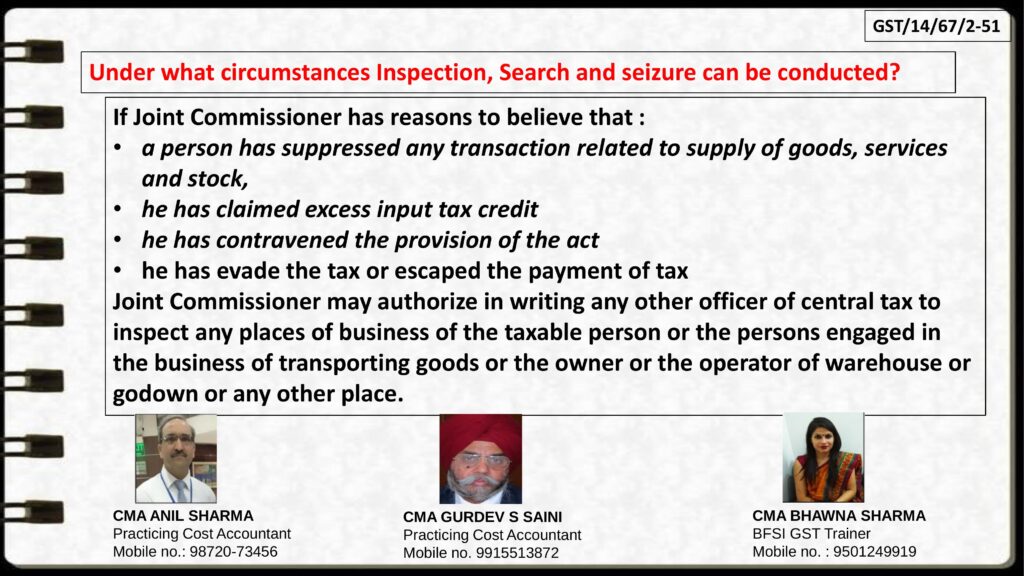

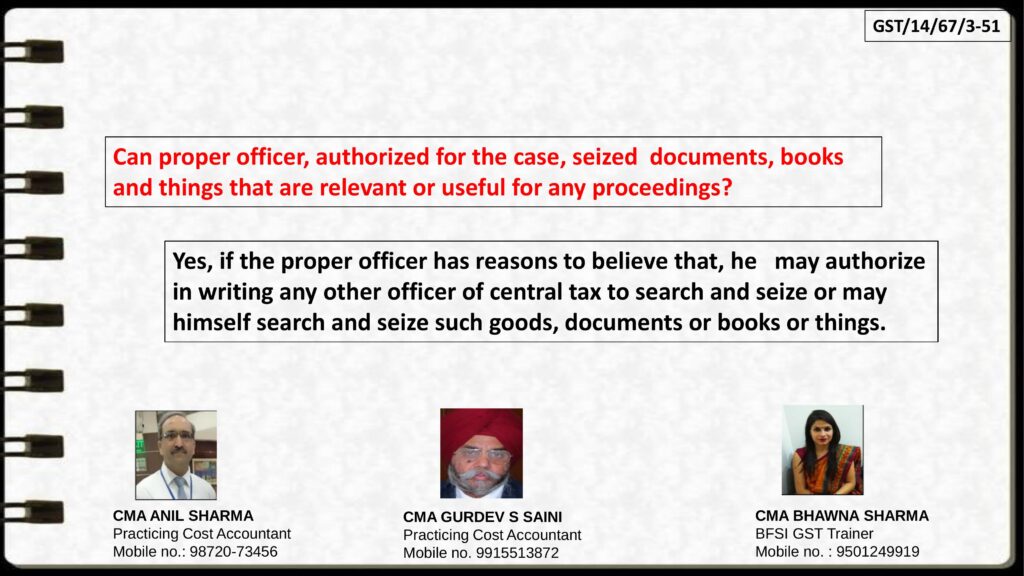

6. GST Notes by CMA Anil Sharma

1) Shri CMA Anil Sharma, Shri CMA Gurdev Singh Saini and Smt. CMA Bhawna Sharma posted Chapter-14 containing CGST Act in simple language in PPT format. This is to make dealers, professionals, academicians, students etc. understand the basics of GST laws. Each Chapter in CGST Act, 2017 is explained in the form of Slides as given below for easy understanding of the Act:

|

Chapter-14 slides given below:-

|

|

|

|

|

|

|

|

|

|

|

|

7) Book by CMA Anil Sharma, B.Com (Honrs), M.Com, FCMA co-author of the book

|

|

Handbook on GST Audit by Tax Authorities has authored yet another book

|

|

title Goods & Service Tax – Some Perceptions and Reflections. Buy now at Price Rs.300/-.

|

|

|

|

|

|

You wish to publish your Article?

|

If you wish to share your article with maximum readers then please send them at taxupdate.otu@gmail.com. We shall publish it with all due credit to you.

|

|

|

|

|

|

|

Hope the above updates is of use to you. Please share your input and feedback at taxupdate.otu@gmail.com

|

|

|

|

|

|

|

Visit our website

|

OTU provides you

|

- Articles on various topics

|

|

- Media - GST, Income Tax & Press R.

|

|

- Notes / Newsletter etc.

|

|

|

|

|