|

|

|

|

|

|

|

|

onlinetaxupdate team wish to express sincere thanks to all the readers, authors, subscribers for the support extended to us.

|

|

|

|

Dear Reader,

|

Please find newsletter for your reading and reference.

|

|

Newsletter no.103 dated 16.11.2023

|

|

|

Index of the Newsletter

- Recent updates

- Article

- Lawgics - Judgments by Ms. Nidhi Aggarwal

- GST notes by CMA Anil Sharma

|

|

|

|

|

|

|

Complete CGST, IGST, and Compensation Cess Acts & All Rules and GSTAT Rules

|

- Tracking of Notifications, Circulars and Orders, and

- Content Links through Bookmarks

by Adv. (CA) Rakesh Garg & Sandeep Garg, CMA, FCA

|

|

|

|

|

|

|

|

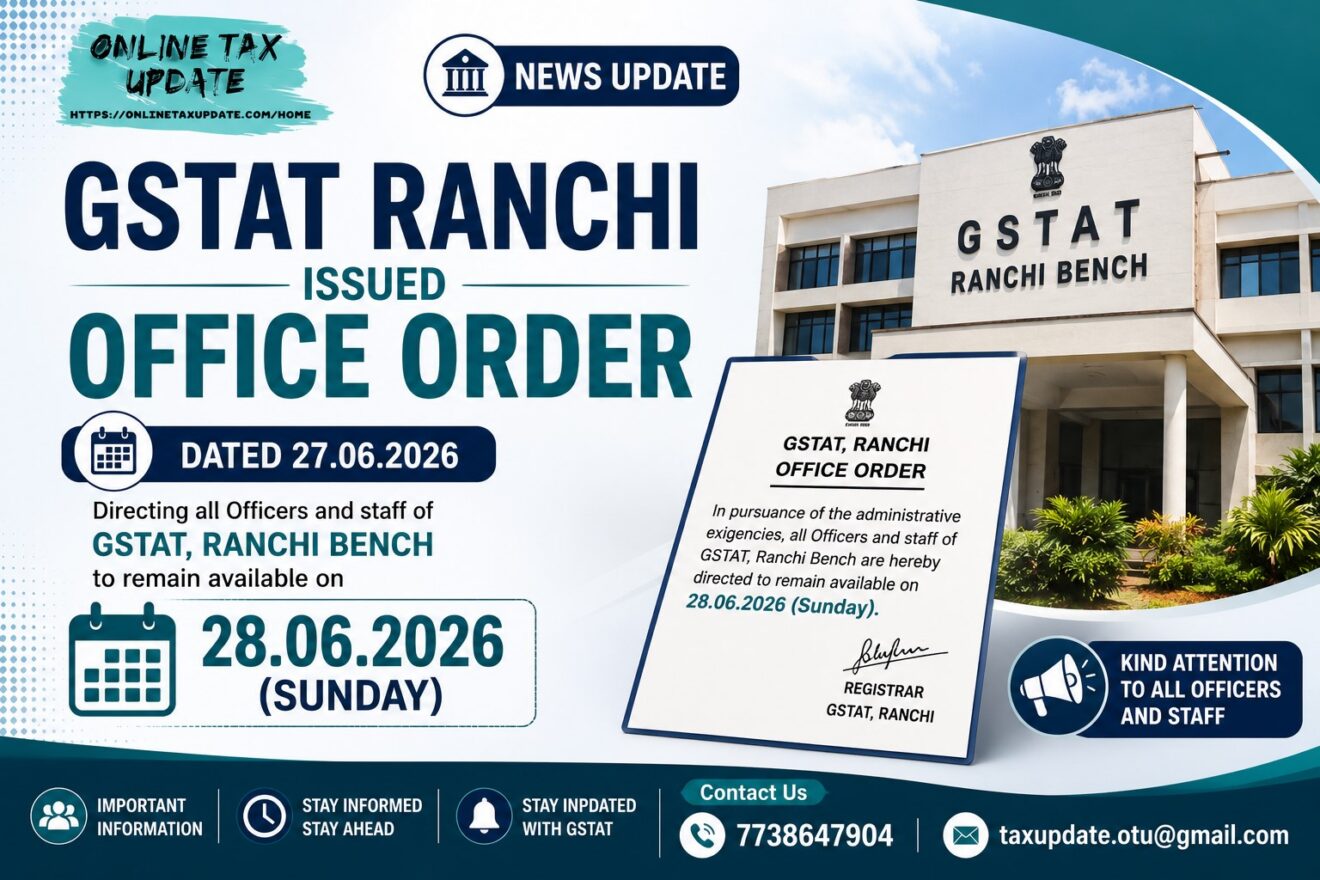

GST Appellate Tribunal (GSTAT) , Department of Revenue, Ranchi Jharkhand issued OFFICE ORDER -03/2026 on 27.06.2026 directing all Officers and staff of GSTAT, Ranchi Bench to remain available on 28.06.2026 (Sunday).

|

It has been observed that the last date for filing appeals before the Goods and Services Tax Appellate Tribunal (GSTAT), i.e. 30th June, 2026, is fast approaching. Consequently, there has been a substantial increase in the number of appeals being field before the GSTAT during the past few days.

|

In view of the above, all officers and staff of GSTAT, Ranchi Bench, are hereby directed to remain available on 28.06.2026 (Sunday) and extend all necessary assistance for resolving any last-minute difficulties, technical issues, or queries that may be faced by taxpayers, appellants, or other stakeholders in connection with the filing of appeals.

|

The deployment of officers and staff under this Office Order shall be treated as official duty for all purposes.

|

This issues with the approval of the Hon'ble Vice President, GSTAT Ranchi Bench.

|

Deputy Registrar, GSTAT Ranchi Bench, Ranchi.

|

- The Registrar, GSTAT, Principal Bench

- The Concerned Official

- Notice Board

- Guard File

|

|

|

|

|

|

|

The Institute of Chartered Accountants of India (ICAI) published Handbook on Finalisation of Accounts with GST Perspective in June, 2026.

|

|

|

|

|

|

|

|

The Institute of Chartered Accountants of India (ICAI) published 4th Edition of "Handbook on Job Work under GST" in June, 2026

|

|

|

|

|

|

|

|

The Institute of Chartered Accountants of India released 12th Edition in April, 2026 of GST Act(s) and Rules (s) Bare Law.

|

- THE CENTRAL GOODS AND SERVICES TAX ACT, 2017

- THE CENTRAL GOODS AND SERVICES TAX RULES, 2017

- THE INTEGRATED GOODS AND SERVICES TAX ACT, 2017

- THE INTEGRATED GOODS AND SERVICES TAX RULES, 2017

- THE UNION TERRITORY GOODS AND SERVICES TAX ACT, 2017

- THE GOODS AND SERVICES TAX (COMPENSATION TO STATES) ACT, 2017

- THE CONSTITUTION (ONE HUNDRED AND FIRST AMENDMENT) ACT, 2016

|

|

|

|

|

|

|

The Institute of Chartered Accountants of India issued a Handbook on Practical Guide to GST Adjudication and Appeals including GSTAT. This is the first edition released in April, 2026.

|

Content:

- Chapter 1 : Introduction

- Chapter 2 General Principles

- Chapter 3 Principles of Evidence

- Chapter 4 Scope of Assessment, Audit, Investigation and Demand

- Chapter 5 Aspects of Investigation and Summons

- Chapter 6 Litigation Strategy

- Chapter 7 Understanding SCN and Approach

- Chapter 8 Appellate Relief

- Chapter 9 Revisionary Proceedings

- Chapter 10 Drafting and Pleadings

- Chapter 11 Appearance

- Chapter 12 GSTAT Portal and Appeal Filing

|

|

|

|

|

|

|

Compilation by B. Venkateswaran I.R.S, Assistant Commissioner Central GST (Retired) Consultant GST, Coimbatore , M - 9442012335 / 8500885294 , E - beevenkateswaran@gmail.com

|

|

|

|

|

|

|

|

ICAI Published on Handbook on Key Compliances and Exemptions for Private Limited Company under the Companies Act, 2013

|

|

|

|

|

|

|

|

The Institute of Chartered Accountants of India (ICAI) published Second edition in February, 2026 on CROSS BORDER TRANSACTIONS AND INVESTMENTS

|

|

|

|

|

|

|

|

The Institute of Chartered Accountants of India (ICAI) issued First Edition of Handbook on Applicability of GST on Agricultural Sector

|

Content:

- Introduction

- Relevant Definitions

- Registration

- Classification

- Taxability of Goods & Services

- Reverse Charge Mechanism

- Input Tax Credit and Reversal thereof

- Refund

- Documentation

|

|

|

|

|

|

|

|

|

Centre has extended the last date for filing appeals before the Goods and Services Tax Appellate Tribunal (GSTAT) to July 31, 2026, giving taxpayers an additional month to submit their cases after a surge in filings led to technical difficulties on the GSTAT portal.

|

The extension applies to appeals filed under Section 112(1) read with Section 112(3) of the Goods and Services Tax (GST) law.

|

The revised deadline replaces the earlier cut-off of June 30, 2026, which had been notified by the government on September 17, 2025.

|

The decision follows recent representations from various stakeholders who flagged technical issues arising from a rush of appeals being filed on the GSTAT portal ahead of the deadline.

|

While noting that the original due date had been notified well in advance in September 2025, the government said filing activity had intensified sharply in recent weeks. It said 30,000 appeals were filed in the last 15 days alone, with daily filings touching a peak of 5,500 appeals.

|

Advising against eleventh-hour filings, the government urged taxpayers to complete their appeal submissions well in advance to ease pressure on the GSTAT portal.

|

The GST Appellate Tribunal serves as the first judicial appellate forum for taxpayers seeking to challenge orders issued by GST authorities after the disposal of their first appeals.

|

Source: The Economic Times

|

|

|

|

|

|

|

|

The Union government on Tuesday granted a six-month extension to the tenure of Central Board of Direct Taxes (CBDT) Chairman Ravi Agrawal till December 2026.

|

The 1988 batch IRS officer was to retire on Tuesday(June 30).

|

The Appointments Committee of the Cabinet (ACC) in an order on Tuesday said it has approved "re-appointment" of Ravi Agrawal as Chairman, CBDT on contract basis for a period of six months with effect from 01.07.2026 or until further orders, whichever is earlier, on the terms and conditions applicable to re-employed central government officers, in relaxation of the Recruitment Rules.

|

He was made chief of CBDT, the policy-making body for the Income Tax Department, for a one-year term in June 2024. His tenure was extended by a year in June 2025.

|

The CBDT is headed by a chairman and can have up to six members, who are equivalent to special secretary rank.

|

Source: The Economic Times

|

|

|

|

|

|

|

|

|

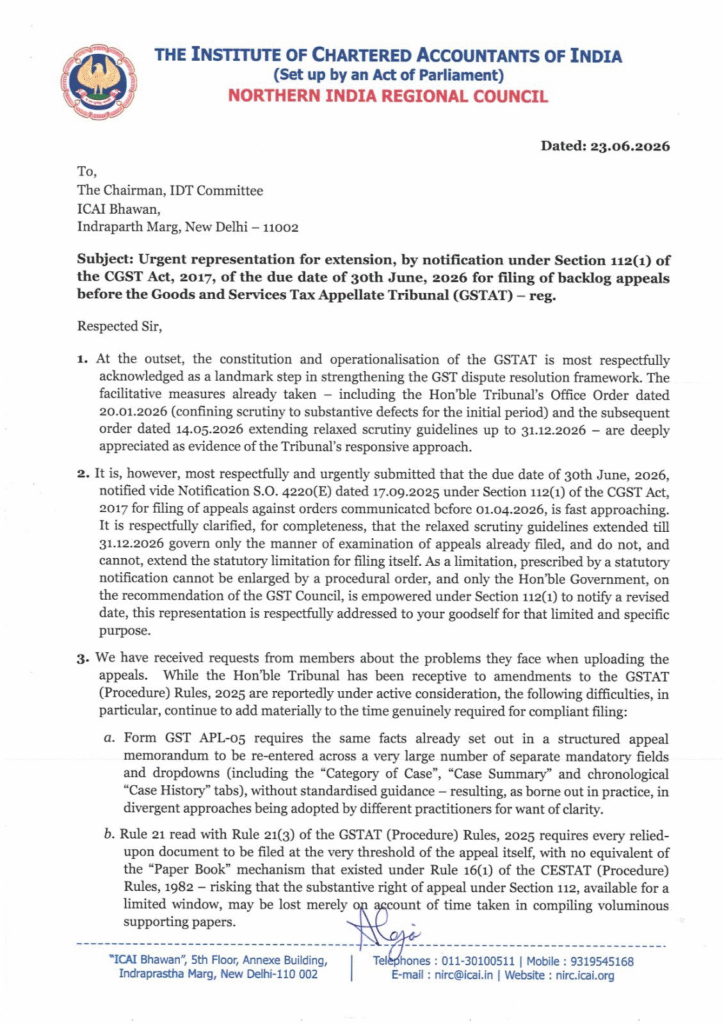

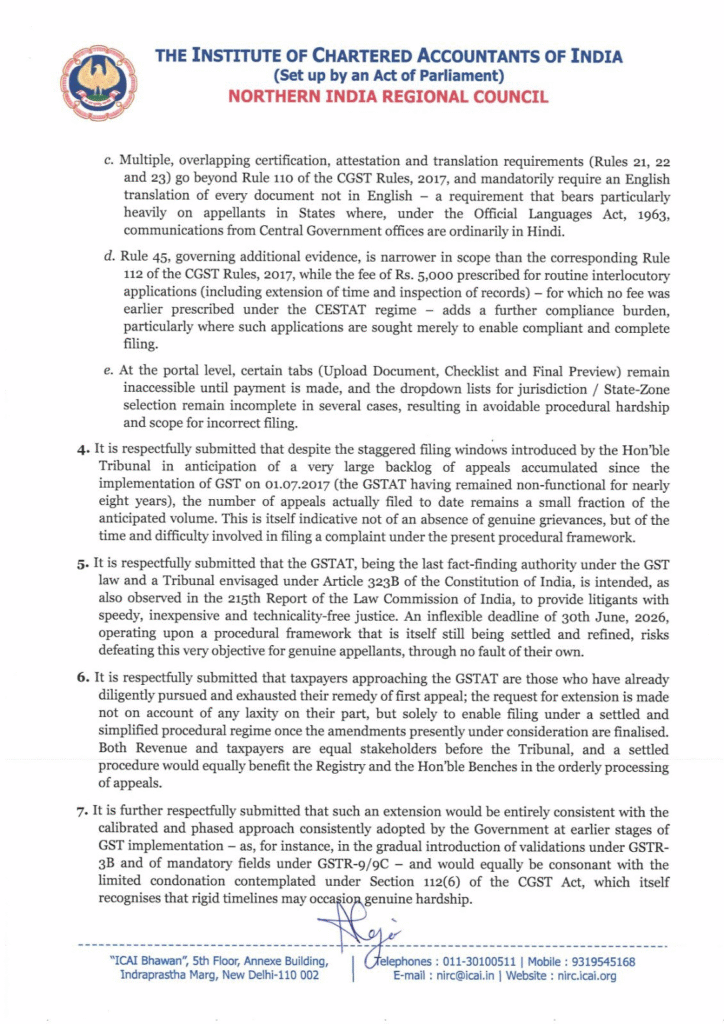

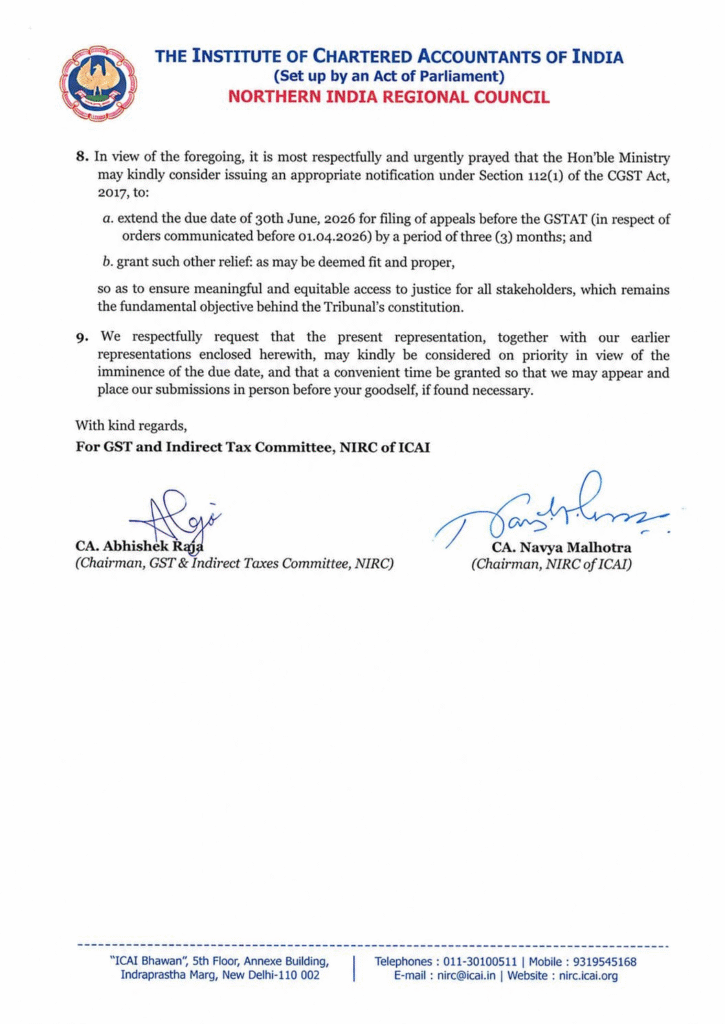

GST & IDT Committee has requested the Chairman, IDT Committee, ICAI, New Delhi to urgently represent before the respective forums for the date extension of GSTAT, i.e., 30-Jun-2026.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Tata Steel Limited said tax authorities have filed an appeal seeking restoration of penalties worth Rs. 368.72 crore that were earlier dropped in a GST adjudication order, even as proceedings on the underlying demand remain stayed by the Jharkhand High Court, according to a stock exchange filing.

|

"One June 16, 2026, the Assistant Commissioner, Division-I, CGST & Central Excise , Jamshedpur, Jharkhand filed an appeal before the Commissioner (Appeals) of CGST & Central Excise, Ranchi against the above-mentioned Adjudication Order dated December 18, 2026, to the extend that the Adjudicating Authority has dropped the penalty amounting to Rs. 3,68,72,21,158/-," Tata Steel said in its exchange filing.

|

The appeal, filed on June 16 by the Assistant Commissioner, CGST & Central Excise, Jamshedpur, challenges the December 18, 2025, adjudication order to the extent it waived the penalty.

|

The original show-cause notice, issued in June 2025, proposed disallowance of input tax credit for FY 2018-19 to FY 2022-23, with an aggregate GST demand of about Rs. 1,007.55 crore. Of this, Tata Steel said it has already paid Rs. 514.19 crore in the normal course, leaving an alleged exposure of Rs. 493.35 crore.

|

In December 2025, the adjudicating authority confirmed the tax demand of Rs. 493.35 crore, imposed a penalty of Rs. 638.83 crore and applicable interested, while dropping an earlier proposed penalty of Rs. 368.72 crore. Tata Steel subsequently moved the Jharkhand High Court, which granted a stay on all further proceedings in March 2026.

|

"This matter is, inter-alia, contingent upon the final adjudication of the issue concerning the issuance of show cause notices for multiple periods, which is presently sub judice before the High Court," Tata Steel said.

|

Tata Steel added that it has a good case on merit and hence will contest the same before the Appellate Authority within the statutory timelines, noting that the development has no impact on its financial or operational position, arising from the said appeal.

|

Source: The Economic Times

|

|

|

|

|

|

|

|

With the June 30 deadline for filing legacy appeals before the Goods and Services Tax Appellate Tribunal (GSTAT) fast approaching , tax professionals, chartered accountants and industry bodies have urged the Finance Ministry to extend the filing window, warning that persistent technical glitches on the GSTAT portal could prevent thousands of taxpayers from filing their appeals before the deadline.

|

The demand comes as taxpayers seek to file appeals arising from nearly nine years of litigation accumulated during the period when the Tribunal remained non-operational. Experts said the combination of a massive backlog, voluminous documentation and continuing portal-related issues has significantly constrained taxpayers' ability to meet the deadline.

|

According to Aditya Singhania, Founder of Trackase, the backlog is estimated at nearly four lakh to 4.5 lakh legacy appeals, while only around 36,929 appeals have been filed nationalwide so far.

|

"The ground reality is deeply concerning. Against an anticipated backlog of nearly four to four and a half lakh appeals accumulated over nine years of the Tribunal's non-operationality, only around 36,929 appeals have been filed nationally as of now," Singhania said.

|

He attributed the slow pace of filings to the teething troubles of the newly launched e-filing portal, including server time-outs, authentication challenges, payment gateway reconciliation issues and a filing structure that requires considerable time and effort to navigate.

|

Experts cite portal hurdles, record backlog

According to experts and representations submitted to the Finance Ministry, taxpayers continue to face multiple technical issues on the GSTAT portal, including session expiry, repeated login failures., Aadhaar authentication problems, Digital Signature Certificate (DSC) validation failures, payment reconciliation delays and incomplete integration between the Goods and Services Tax Network (GSTN) and the GSTAT portal.

|

Experts said taxpayers are also required to retrieve and compile extensive records accumulated over several years, including adjudication orders, invoices, reconciliations, e-way bills, ledger extracts and other supporting documents, making the filing process particularly time-consuming.

|

CA Nitin Bansal, State-President, BJP CA Cell Haryana, said the Finance Ministry has received several representations highlighting the practical challenges taxpayers are facing in filing appeals before the Tribunal.

|

"With the Tribunal becoming operational after nearly nine years, taxpayers must now prepare and file a substantial backlog of appeals within a limited window, many involving voluminous, multi-year records, even as the GSTAT e-filing portal continues to stabilise," Bansal said.

|

He added that extending the deadline would be revenue-neutral as the mandatory pre-deposit and other conditions would remain unchanged while ensuring genuine taxpayers are not denied their appellate remedy because of circumstances beyond their control.

|

Over-time extension sought

CA Sonu Goel, Chairman, Panipat Branch of the Institute of Chartered Accountants of India (ICAI), said a one-time extension would ensure disputes are decided on their merits rather than procedural constrints.

|

"One-time extension would safeguard taxpayers' right to appeal, uphold the principles of natural justice, and ensure that dispute are decided on merits rather than being defeated by procedural or technological constraints. This pragmatic relief would further reinforce the Government's commitment to ease of doing business while maintaining certainty and confidence in the GST ecosystem," Goel said.

|

Parag Mehta, Partner at N.A. Shah Associates LLP, said the portal continues to experience issues ranging from login failures and incorrect fee calculations to disappearing data.

|

"Considering the fact that the portal is not fully supporting the filing process and the number of appeals filed remains significantly lower than expected, the deadline should be extended. GSTAT is an important appellate remedy and taxpayers should not be deprived of that opportunity," Mehta said.

|

Bas association flags nationwide concerns

The Sales Tax Bar Association has also written to the Finance Ministry seeking an extension of the filing deadline, stating that taxpayers and tax professional across the country continue to face significant practical and technical difficulties while filing appeals through the GSTAT portal.

|

In its representation, the association said the present limitation period covers appellate orders accumulated over nearly nine years when the Tribunal remained non-functional, requiring taxpayers to retrieve historical records and prepare detailed documentation within a limited period.

|

The association highlighted recurring issues including server interruptions, repeated Aadhaar authentication and DSC validation failures, payment gateway reconciliation delays, manual duplication of information already available on the GSTN portal and challenges in uploading voluminous records.

|

It warned that if the deadline is not extended, thousands of taxpayers could lose the opportunity to pursue their statutory appeals because of technological and procedural constraints, potentially leading to avoidable litigation before various High Courts.

|

Prabhat Ranjan, Senior Director at Nexdigm, said extending the filing deadline has become "the need of the hour".

|

"The appellate process should be about the actual merits of the issues between both parties and not technical questions of delay. This is a taxpayer-friendly measure that will make GST dispute resolution processes more fair and credible," he said.

|

As of publication, the government has not announced any extension of the June 30 deadline for filing legacy GSTAT appeals. While the GSTAT has extended the period for relaxed scrutiny of filed appeals until December 31, 2026 , tax professionals, industry experts and representative bodies continue to seek a one-time extension of the filing deadline, arguing that additional time would enable taxpayers to exercise their statutory right of appeal without affecting revenue, as the mandatory pre-deposit requirements would continue to apply.

|

Source: The Economic Times

|

|

|

|

|

|

|

|

Businesses shifting their principal place of business to a new GST jurisdiction will not have to restart pending tax proceedings with the Central Board of Indirect Taxes and Customs (CBIC) clarifying that the new jurisdictional authority will take over and complete all ongoing cases from the stage at which they were left, reported PTI.

|

The clarification comes after the CBIC received references from field formations seeking guidance on the validity of proceedings and the authority responsible for handling cases when a registered taxpayer changes jurisdiction because of a shift in its principal place of business.

|

Under the circular, any action or proceeding - including investigation, audit, show cause notice or adjudication under the Central GST law - initiated by the tax officer having jurisdiction over the registered taxpayer at the time the action was undertaken (transferor jurisdiction authority) will remain valid even if the taxpayer subsequently shifts to another tax jurisdiction (transferee jurisdictional authority).

|

"The transferee jurisdictional authority shall act upon, give effect to, and proceed on the basis of such earlier valid action taken by the transferor jurisdictional authority, as if it had itself initiated the same," the CBIC said in the circular.

|

The indirect tax board further clarified that if any fresh issue comes to the notice of the earlier jurisdictional authority after the taxpayer has shifted, the tax officer should intimate the new jurisdictional officer for appropriate action.

|

"Where the taxable person migrates to another jurisdiction during the pendency of any action or proceeding initiated by the transferor jurisdictional authority, the transferee jurisdictional authority shall take over and conclude the same from the stage at which it stood at the time of migration/ transfer," the CBIC circular said.

|

The new jurisdictional officer will also have the authority to initiate and conclude any consequential proceedings arising from the case.

|

Rajat Mohan, Managing Partner at AMRG Global, said the clarification addresses a key procedural gap under the GST regime.

|

"By clearly defining the responsibilities of transferor and transferee authorities, CBIC has removed ambiguity that often resulted in jurisdictional objections and delays in adjudication," Mohan said.

|

Source: The Times of India

|

|

|

|

|

|

|

|

On the occasion of 9th GST Day to be celebrated on 1st July, 2026 the Central Board of Indirect Taxes and Customs vide Office Memorandum dated 29.06.2026 has decided to grant Certificate of Meritorious Service (CBIC-CMS) to the following officers:

|

|

|

|

|

|

|

|

The Malad Chamber of Tax Consultants made a representation to the Hon'ble Union Finance Minister, Smt. Nirmala Sitharaman, New Delhi on 26.06.2026 requesting an extension of the statutory deadline for filing GSTAT appeals under Section 112 of the CGST Act, 2017 from 30th June 2026 to 31st December 2026.

|

|

|

|

|

|

|

|

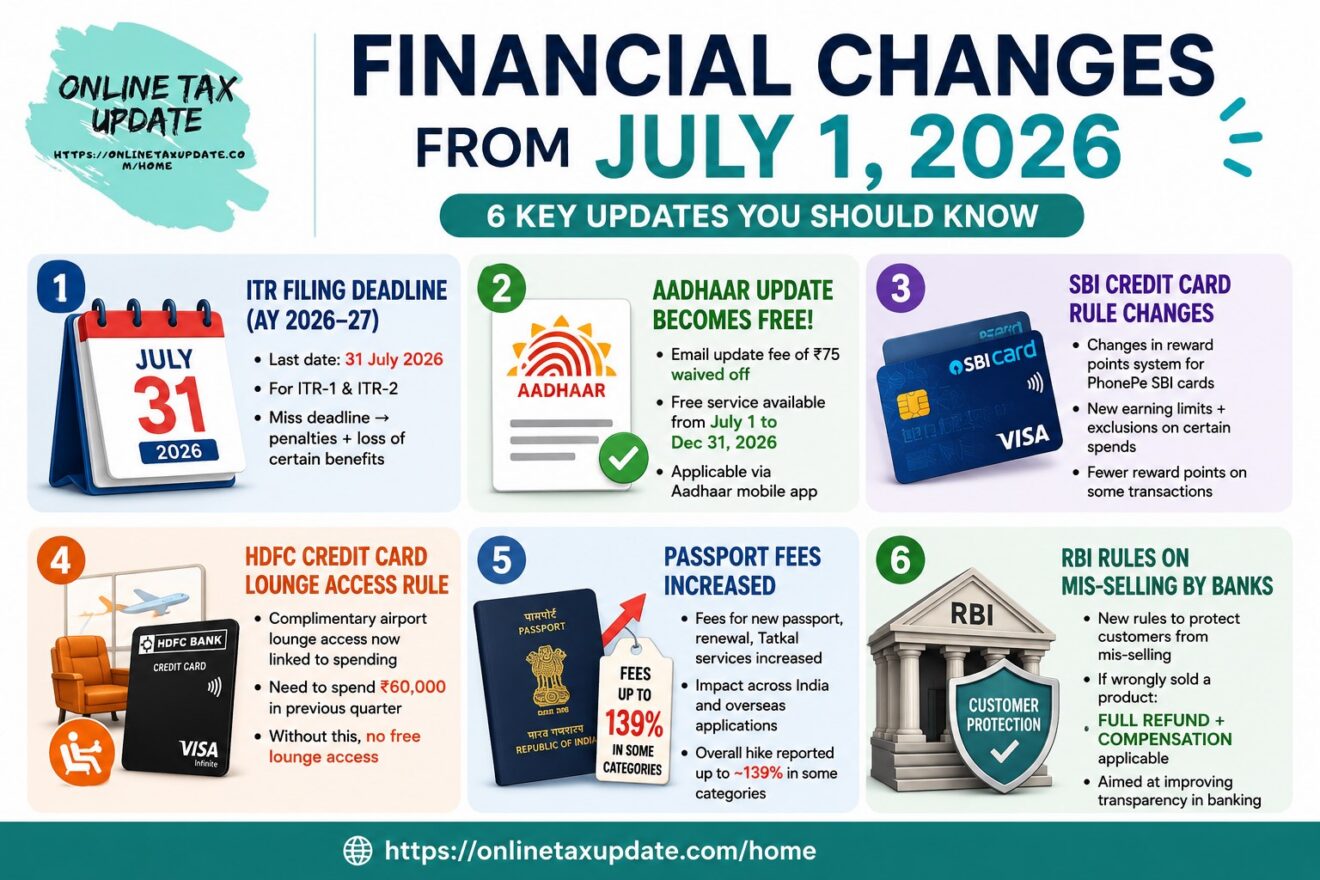

Several important financial changes are set to take effect on July 1, 2026. These changes could impact taxpayers, bank customers, credit card users, passport applicants and Aadhaar card holders. Here's a look at the key financial changes coming into effect in July 2026.

|

1. ITR-1, ITR-2 deadlines

For taxpayers filing ITR-1 and ITR-2 forms, due dates for filing returns for the Financial Year 2025-26 (Assessment Year 2026-27), is July 31, 2026. Missing the prescribed deadlines could result in penalties, restrictions on choosing certain tax regimes and limitations on carrying forward eligible losses to future assessment years.

|

2. Free update in Aadhaar card

Starting July 1, the Unique Identification Authority of India (UIDAI) has temporarily waived off the Rs 75 fee for updating your registered email address on your Aadhaar card. This service will be completely free of cost for six months (until December 31, 2026).

|

According to an official notification, "It has been decided to waive off the charges (i.e., Rs 75) for availing the service of email address update through the Aadhaar mobile application and make it free of cost for a period of six months with effect from July 1, 2026, to December 31, 2026."

|

3. SBI credit card changes

SBI Card has announced changes to the reward point programme for select PhonePe SBI Credit Cards, which will come into effect from July 1, 2026. The revision affects both PhonePe SBI Credit Card PURPLE and PhonePe SBI Credit Card SELECT BLACK card holders, as new limits on earning reward points and a broader list of transactions that won't earn reward points have been introduced.

|

4. HDFC Credit card changes

From July 1, 2026, HDFC credit card holders will be eligible for three complimentary domestic airport lounge visits per calendar quarter, provided they have spent at least Rs 60,000 in the preceding calendar quarter.

|

For instance, to avail lounge access during the July–September 2026 quarter, a card holder must have spent Rs 60,000 or more between April and June 2026. This spend-based eligibility will apply to every subsequent calendar quarter.

|

5. Higher passport fees

Obtaining a passport will soon become more expensive for both normal and Tatkaal applicants. The Ministry of External Affairs has increased services fee for normal and tatkal passports (India and overseas) from July 1, 2026.

|

6. New rules for banks on mis-selling of bank products

The RBI has announced new rules to curb the mis-selling of financial products by banks. Under the new framework, customers who are mis-sold products will be entitled to a full refund and compensation for losses. The rules are set to come into effect on July 1, 2026.

|

Source: The Economic Times

|

|

|

|

|

|

|

|

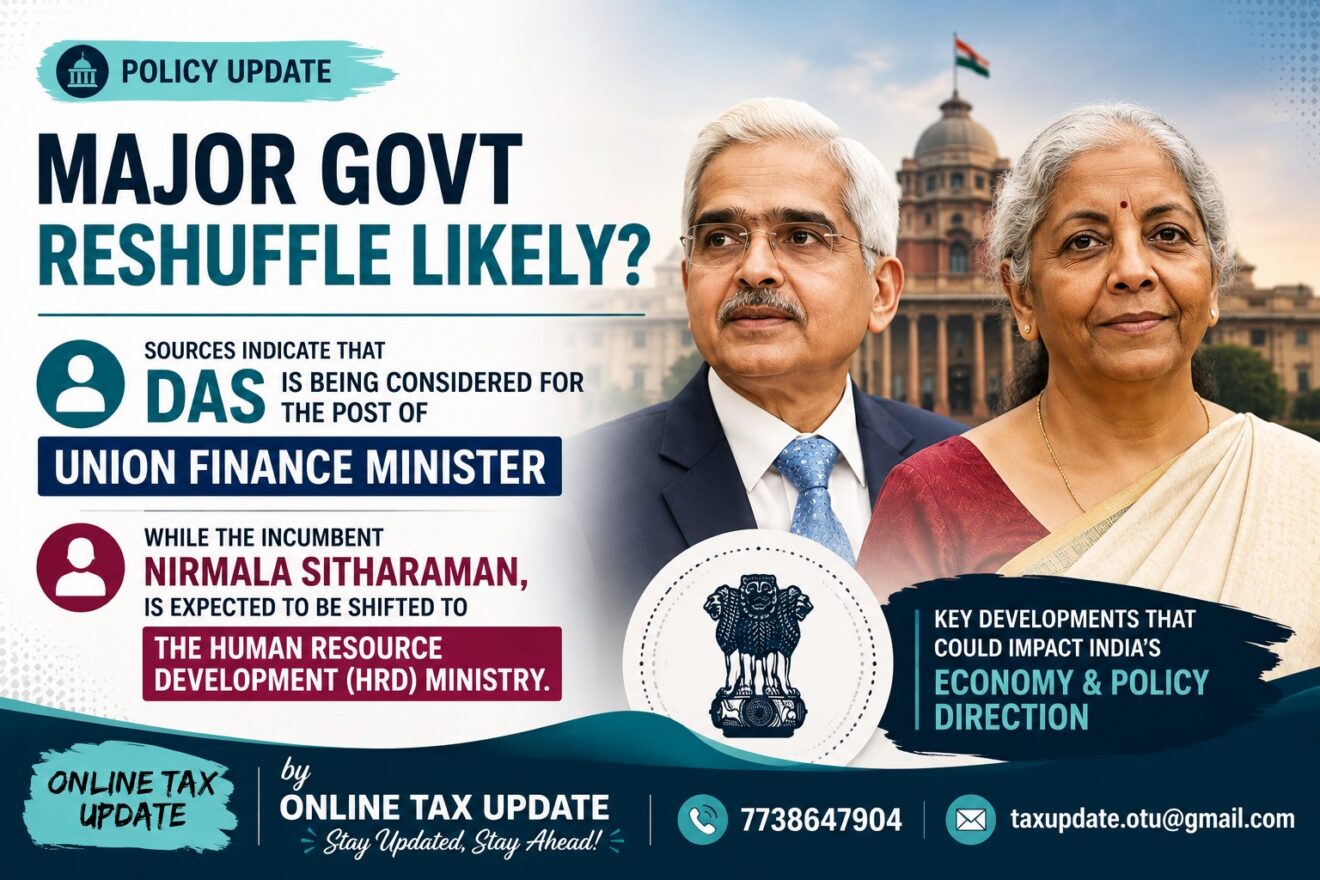

The recent meeting between Prime Minister Narendra Modi and President Droupadi Murmu, followed by a meeting between Home Minister Amit Shah and the President, have fuelled speculation over a possible Union cabinet reshuffle as well as changes in the BJP's organisational structure.

|

According to sources, the reshuffle is likely to take place before the upcoming Monsoon Session of Parliament.

|

Among the names being discussed is that of former Reserve Bank of India (RBI) governor Shaktikanta Das, who is currently serving as the Principal Secretary to the Prime Minister.

|

Sources indicated that Das is being considered for the post of Union finance minister, while the incumbent , Nirmala Sitharaman, is expected to be shifted to the human resource development (HRD) ministry. Sitharaman has been serving as the Union Minister for finance and corporate affairs since 2019.

|

There has, however, been no official confirmation from either the government or the BJP regarding any proposed changes.

|

If the move materialises, it would bring into the Cabinet a seasoned administrator with more than four decades of experience across several areas of governance.

|

Das served as the 25th Governor of the RBI from 2018 to 2024. Before assuming charge at the RBI, he was a member of the 15th Finance Commission and India's G20 Sherpa.

|

Over the course of his career, Das has held several key positions in both the Central and State governments, handling portfolios related to finance, taxation and industries and infrastructure.

|

During his tenure in the finance ministry, he was closely associated with the preparation of eight Union Budgets, giving him extensive experience in public finance and economic policymaking. Besides, Das was also the senior Department of Economic Affairs official in the finance ministry during the planning and implementation phase of demonetisation.

|

A postgraduate from St. Stephen's College, University of Delhi, Das has also served as India's Alternate Governor to the World Bank, the Asian Development Bank, the New Development Bank, and the Asian Infrastructure Investment Bank. He has represented India at major international forums, including the IMF, G20, BRICS, and SAARC.

|

|

|

|

|

|

When Mr. Yadav from Kanpur filed his income tax return (ITR) for FY 2018-19, he combined his wife's stock market and F&O trading losses with his own income under clubbing provisions (Section 64(1)(iv)) and claimed a set-off, thereby reducing his total tax liability.

|

However, the tax department objected to the claim on two grounds.

|

First, her total stock market trading loss was about Rs 1.95 crore, of which only Rs 1.15 crore was attributable to funds gifted by Yadav to his wife; the remaining Rs 80 lakh came from her own resources.

|

Second, the Assessing Officer treated her as an independent taxpayer and held that the gains and losses arose from trading activities undertaken in her name and account, making the losses her own and not eligible for set-off in her husband's hands. Accordingly, the tax officer rejected the clubbing claim and denied the set-off of losses.

|

Unhappy with this decision, Mr Yadav filed an appeal before the commissioner of appeals (CIT (A) arguing that he maintains a joint bank account with ICICI Bank and routinely transfers money to this account citing reasons like 'investment', 'gift', 'budget'. He explained that just like these routine transfers, he transferred Rs 1.15 crore of his own money to their joint bank account and used it to trade in the stock market from her demat account.

|

To support his claims, he submitted the gift deed showing he had transferred Rs 1.15 crore to his wife without any consideration and fully out of his earnings and past savings. He also filed an affidavit declaring that the amount has been transferred without any consideration and without agreement to live part.

|

However, CIT (A) rejected his appeal, and so he took his case to ITAT Lucknow. The primary reason why both the CIT (A) and tax officer didn't believe him was because they thought that the income / loss generated in his wife's case was not merely the result of asset transfer (money) but rather the result of risk-taking by her.

|

The idea that she herself possessed enough skill to trade in the stock market was solidified by the fact that she had earned an independent income of Rs 30,239 shown as speculative business profit, as evident from the statement of income submitted.

|

CIT (A) and the tax officer concluded that on the one hand, Yadav was treating speculative business profit as an independent income of his wife, while on the other hand, a large portion of the Rs 1.14 crore-loss of his wife was being set off against his own income. Therefore, the reply of the assessee was not found to be acceptable on merits.

|

Thus both CIT (A) and the tax officer ruled that Section 64(1) (iv) is not applicable if the wife possesses technical or professional qualifications and the income or loss was solely attributable to the application of his or her technical or professional knowledge and experience.

|

Chartered Accountant Dharmendra Kumar appearing on Yadav's behalf in ITAT Lucknow told the tribunal that Yadav had opened that demat account in her name as well as the joint bank account in ICICI Bank. Kumar told the tribunal that she had no technical or professional expertise to trade in the stock market and so Yadav used to contribute funds to their joint bank account for trading in F&O, derivates and equities using her demat account.

|

Kumar also told the tribunal that during the year, Yadav had transferred Rs 1.15 crore to her in their joint bank account where she also had Rs 80 lakh of her own funds. As a result of this, his wife had a total capital of Rs 1.95 crore. From this capital, Yadav had undertaken trading in derivatives and equities on her behalf, as a result of which she incurred a loss of Rs 1.95 crore.

|

Bifurcating this loss from the derivative trading in her demat account, Kumar said while derivative trading losses of Rs 80 lakh (coming from her own funds) were attributable to her, the loss of Rs 1.15 crore were attributable to derivative transactions from the gift received from Yadav.

|

Thus, Kumar argued that as per the provisions of Sections 64(1)(iv), any loss derived from such transactions was allowed to be set off against the profits made by Yadav. On May 19, 2026, Yadav won the case in ITAT Lucknow (ITA No.585/LKW/2024).

|

Chartered Accountant Ashish Karundia said to ET Wealth Online: "The Tribunal has rightly reaffirmed that the clubbing provision under Section 64(1)(iv) is not a one-way street."

|

According to Karundia, if income arising from assets transferred to a spouse is liable to be clubbed in the hands of the transferor, the same principle must equally apply to losses attributable to such transferred assets.

|

Karundia says: "The Tribunal correctly held that derivative trading losses arising from transactions funded through the taxpayer's gift to his spouse are eligible for set-off in the taxpayer's hands. The ruling reinforces the principle that tax law should operate symmetrically, preventing a selective application of clubbing provisions."

|

Chartered Accontant Naveen Wadhwa, Vice President, Research and Advisory Division, Taxmann, said to ET Wealth Online: "A common misconception is that the clubbing provisions of the Income-tax Act operate only when there is an income. Where a spouse's income is liable to be clubbed in an individual's hands, a loss from that very source is equally liable to be clubbed."

|

According to Wadhwa, this conclusion is based on the principle that the expression 'income' has always been read to include a loss. So if the conditions for clubbing are otherwise met, the spouse's loss is set off against the individual's income, and any unabsorbed portion is carried forward in his own hands. The principle remains the same under the new Income-tax Act, 2025.

|

ITAT Lucknow judgement and discussion

ITAT Lucknow cited several Supreme Court rulings and decisions from other ITAT benches, concluding that losses incurred by a spouse in derivative transactions from money gifted to them, must be allowed and deducted from the income of the gifting spouse. This is in accordance with Section 64(1)(iv) read with Explanation 3(i).

|

ITAT Lucknow said: "Thus, the decision of the Assessing Officer and the ld. CIT(A) to deny the assessee the benefit of this set off, is not in accordance with the law and the judgments cited aforesaid."

|

Therefore, ITAT Lucknow held that Yadav is entitled to set off that portion of the loss arising from trading in derivatives by his wife that resulted from transactions made with the money he had gifted her.

|

However, since Yadav did not submit any evidence or working or statement showing the bifurcation of this Rs 1.95 crore loss or how these losses arose, ITAT Lucknow restored the matter to the Assessing Officer for the limited purpose of verifying the extent of losses incurred by her from transactions undertaken with the money gifted by Yadav and to allow it in accordance with the provisions of Explanation 3(i) to Section 64(1)(iv).

|

In view of the fact that the debate over the assessment order and the order of the ld. CIT(A) is mainly focused on the principle of allowability, the matter of the actual amount of losses that need to be adjusted against the income of Yadav, has not been enquired into by ITAT Lucknow.

|

Order: In the result, the appeal of the assessee (Yadav) is partly allowed. Orders pronounced on 19.05.2026.

|

Source: The Economic Times

|

|

|

|

|

|

|

|

Taxpayers who have accidentally deposited tax deducted at source (TDS) challans under the wrong financial year during transition to the new Income-tax Act, 2025 will have to rely on the old TRACES portal to correct the mistake.

|

The new TRACES platform currently does not support this correction facility.

|

The error can create problems later because the TDS credit may not reflect correctly against the taxpayer’s records for tax year 2026-27.

|

This could increase the tax payable at the time of filing the income tax return (ITR) and may also trigger mismatches between TDS statements and tax records.

|

The Income Tax department has been rolling out changes linked to the implementation of the new Income-tax Act, 2025. During this transition, taxpayers and deductors need to be careful while selecting the relevant financial year and tax details while making TDS payments.

|

Why the TDS challan correction matters

TDS deducted by an employer, bank, company or any other deductor is linked to challan details submitted to the Income Tax department. If the financial year mentioned in the challan is incorrect, the tax payment may not get mapped properly.

|

For example, if a TDS challan that should have been filed for FY27 is mistakenly deposited under FY26, the system may not recognise it for the correct tax year. This can affect the availability of tax credit while filing returns.

|

According to guidance available on the Income Tax department and TRACES platforms, corrections for eligible challan details can be made through the OLTAS Challan Correction facility.

|

New TRACES portal does not support this correction yet

|

During the transition from the Income-tax Act, 1961 to the Income-tax Act, 2025, certain legacy correction facilities continue to remain available only on the older TRACES portal.

|

Taxpayers and deductors who need to change the financial year of a TDS challan must currently use the old TRACES platform instead of the new portal.

|

The correction facility is mainly relevant for deductors managing TDS payments through TAN-based compliance.

|

How to correct wrong financial year in TDS challan

The correction process needs to be completed through the old TRACES portal:

|

- Visit the TRACES website and log in using TAN credentials.

- Go to the section for challan correction or OLTAS challan correction.

- Select the relevant statement/payment details and raise a correction request.

- Choose the correction category and submit the request.

- Once the request becomes available, update the incorrect details, such as the financial year, wherever permitted.

- Submit the corrected request and track the status.

After processing, deductors should verify whether the updated challan details are correctly reflected in the tax records.

|

What happens if the mistake is not corrected?

A wrong financial year entry can lead to several compliance issues. The taxpayer may not receive the expected TDS credit, which can increase the tax demand during ITR processing.

|

- mismatch between TDS returns and challan details;

- incorrect reflection of tax payments;

- possible tax department communication;

- delays in resolving refund or credit-related issues.

Tax experts advise deductors to check challan details carefully, especially during the shift to the new tax law framework.

|

Taxpayers should verify before filing returns

With changes being introduced under the Income-tax Act, 2025, taxpayers should ensure that payments, TDS statements and tax credits are aligned with the correct tax year.

|

The Income Tax department has advised taxpayers to use official portals for compliance-related actions and check the latest instructions as digital systems continue to be updated.

|

For now, those facing a wrong-year TDS challan entry for FY26 and tax year 2026-27 need to complete the correction through the legacy TRACES portal to avoid future tax credit issues.

|

Source: Business Standard

|

|

|

|

|

|

|

|

The Hon’ble Allahabad High Court in Ashish Tyagi allowed the habeas corpus petition and declared the arrest and consequent detention of the assessee under Section 132 of the CGST Act as illegal

|

|

|

|

|

|

|

|

The Hon’ble Gauhati High Court in M/s Metal Syndicate and Another set aside the OIO and the OIA confirming GST demand of Rs. 78,70,952/- along with interest and equivalent penalty, and held that a bona fide purchasing dealer cannot be denied ITC merely on account of the supplier’s failure to deposit the tax collected with the Government.

|

|

|

|

|

|

|

|

The Hon’ble Madras High Court (Madurai Bench) in Tvl. Manickavasagam S. set aside the assessment order passed under Section 74 of the TNGST Act pertaining to levy of GST on seigniorage fees

|

|

|

|

|

|

|

|

The Hon’ble Madras High Court in P. Baskaran set aside the order imposing interest and penalty u/s 74 of CGST Act and remanded the matter for fresh consideration on the applicability of Section 74

|

|

|

|

|

|

|

|

Deepak Bapat, an advocate in the Mumbai High Court, pointed out that even after four months of the tribunal being operational, several glitches remain.

|

|

|

|

|

|

|

|

The Hon’ble Bombay High Court in the case of Rika Global Impex Limited held that benefit under the RoDTEP Scheme cannot be denied to exporters of sugar merely because the export was categorized as ‘restricted’, ..

|

|

|

|

|

|

|

|

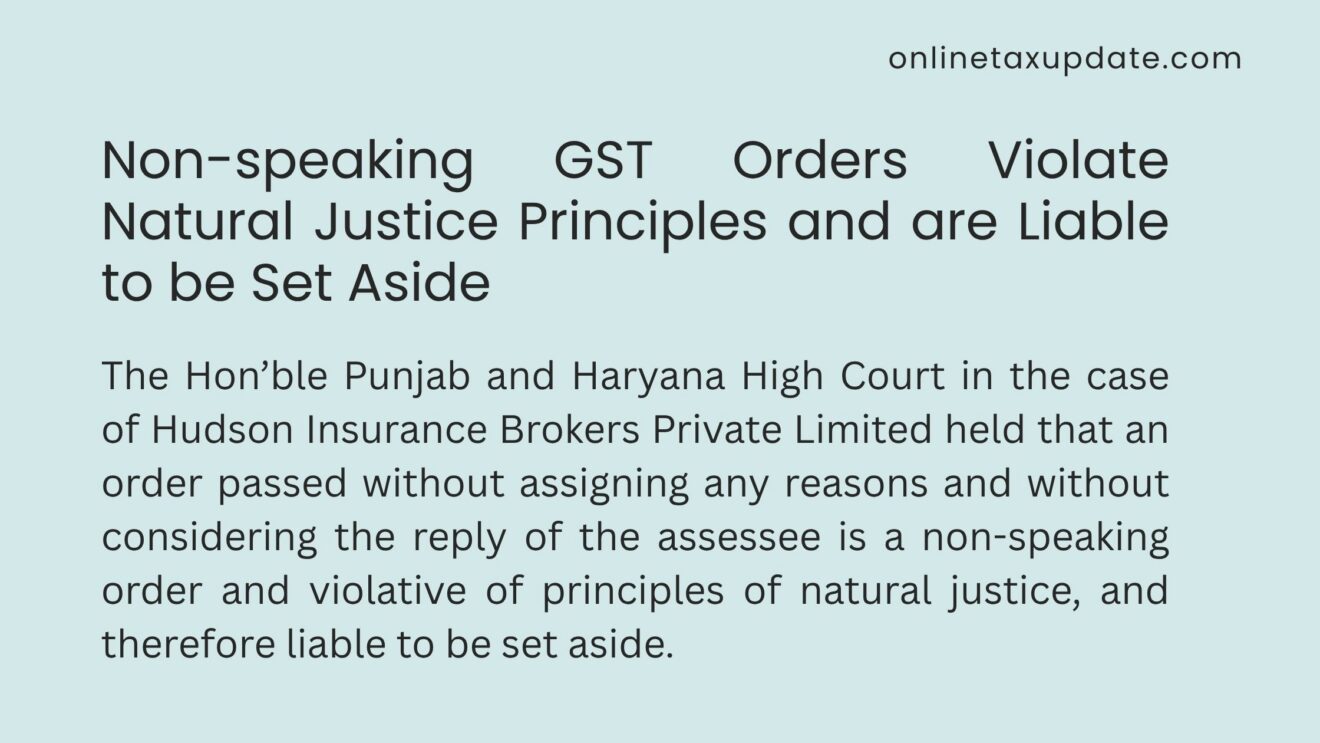

The Hon’ble Punjab and Haryana High Court in the case of Hudson Insurance Brokers Private Limited held that an order passed without assigning any reasons and without considering the reply of the assessee is a non-speaking order and violative of principles of natural justice, and therefore liable to be set aside.

|

|

|

|

|

|

|

|

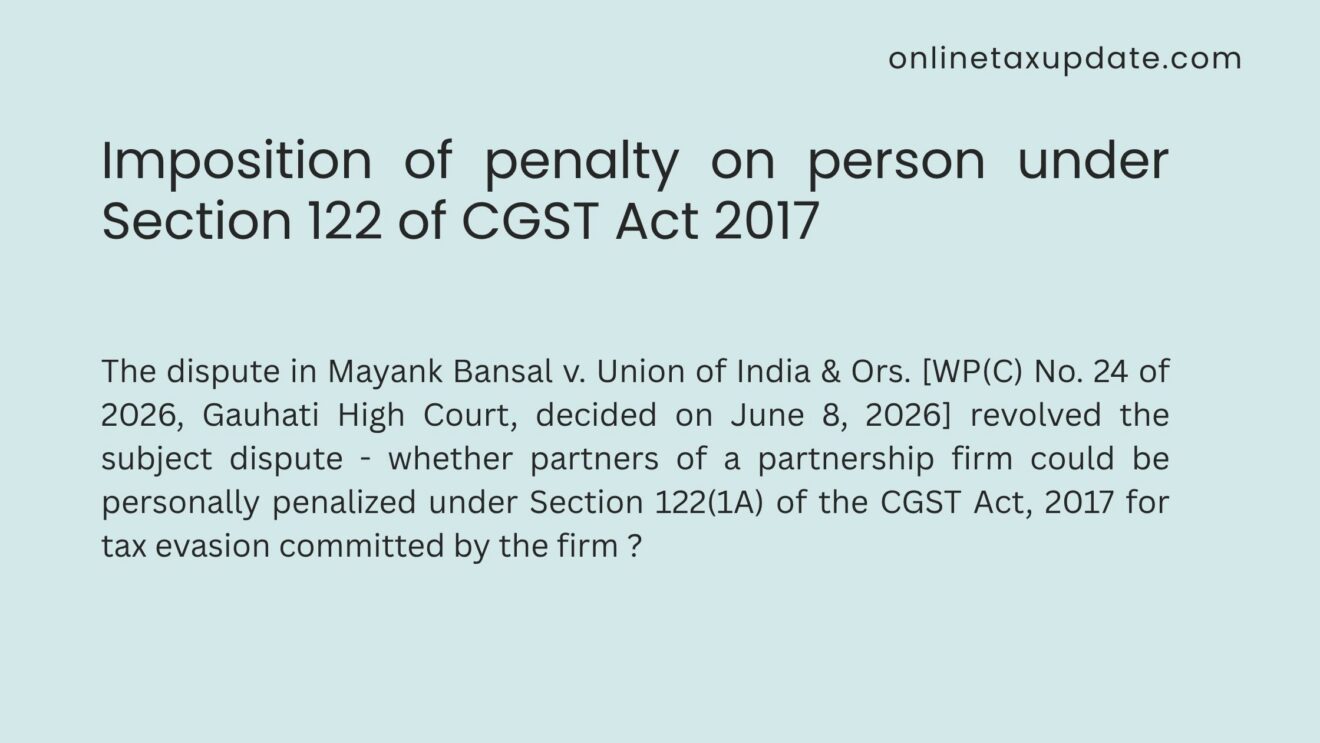

whether partners of a partnership firm could be personally penalized under Section 122(1A) of the CGST Act, 2017 for tax evasion committed by the firm ?

|

|

|

|

|

|

|

|

The Hon’ble Karnataka High Court in the case of Sri Laxmi Borewell Agencies held that the time-limit prescribed for filing an application under Section 128A of the CGST Act for waiver of interest/penalty is directory and not mandatory

|

|

|

|

|

|

|

|

The Hon’ble Punjab and Haryana High Court in the case of M/s Bagga Vet Pharma held that an order passed without assigning

|

|

|

|

|

|

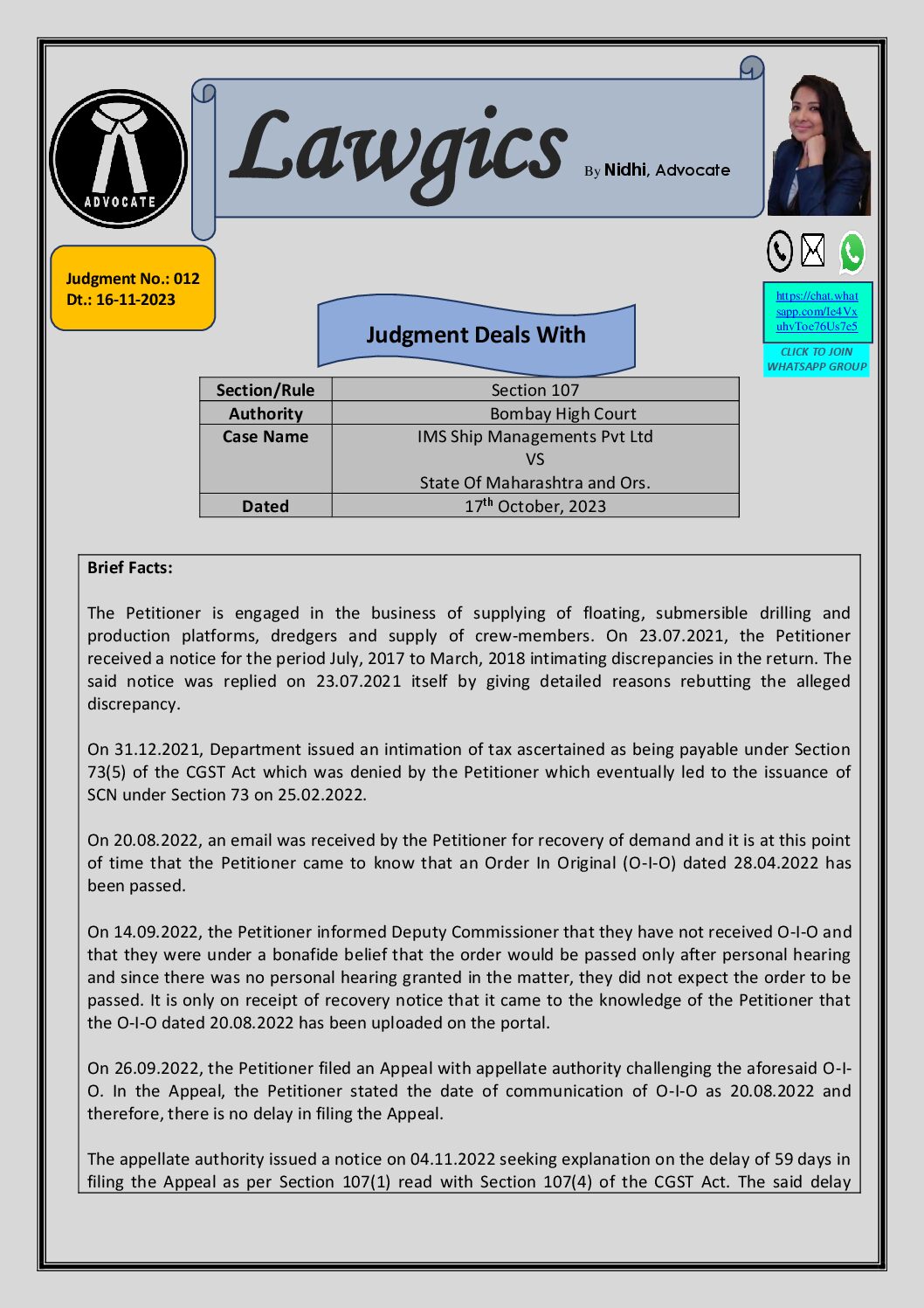

4 Judgment by Ms.Nidhi Aggarwal

|

Ms. Nidhi Aggarwal is delighted to present judgment with a great vision to spread complex GST law in a simple manner amongst the taxpayers, tax professionals, students and knowledge seeker.

|

|

Lawgics- 12 Judgment is added for your reading

|

|

|

|

|

|

|

5. GST Notes by CMA Anil Sharma

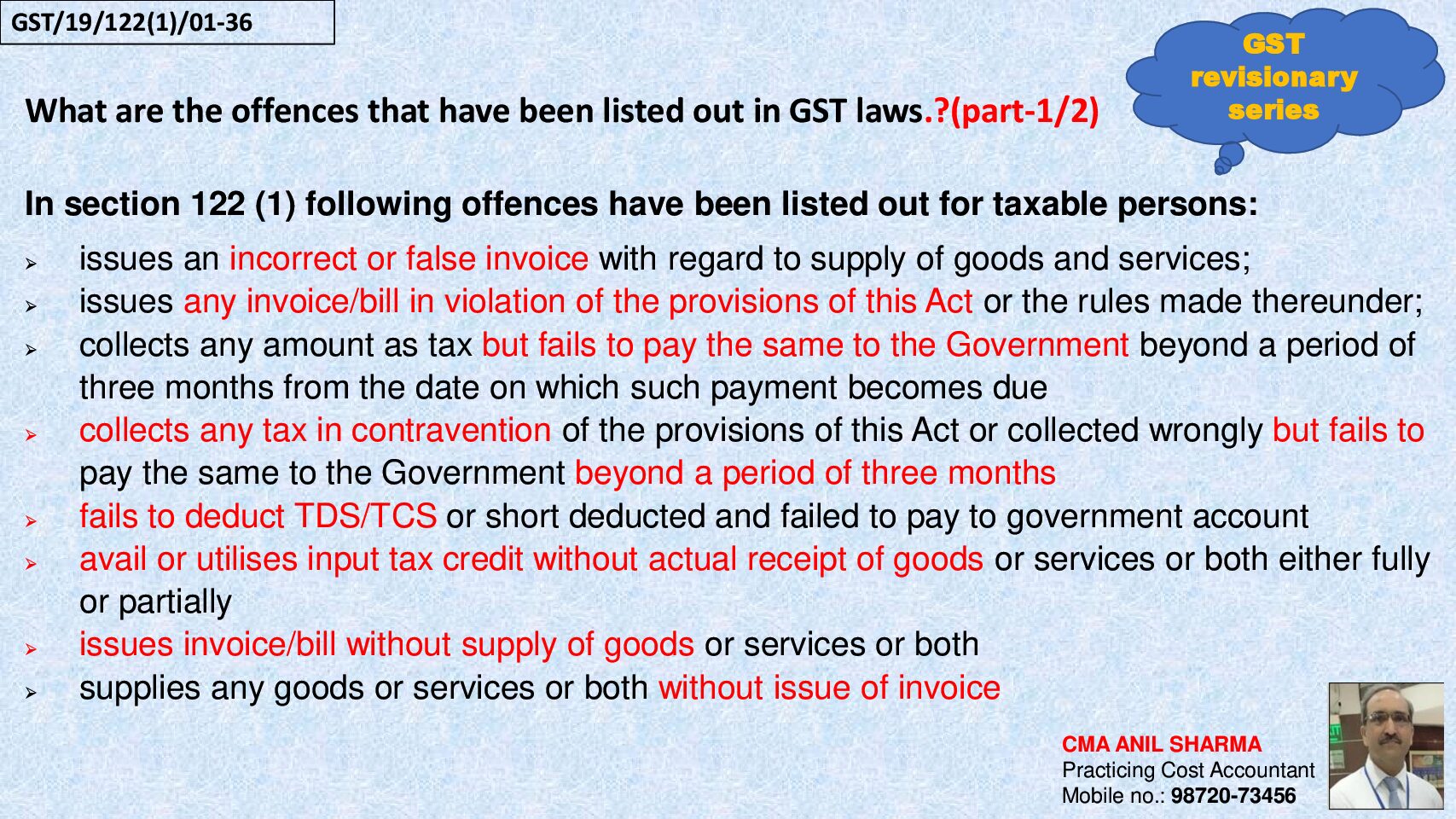

1) Shri CMA Anil Sharma, Shri CMA Gurdev Singh Saini and Smt. CMA Bhawna Sharma posted Chapter-19 recently containing CGST Act in simple language in PPT format. This is to make dealers, professionals, academicians, students etc. understand the basics of GST laws.

|

Chapter-19th slide is given below.

|

|

|

|

|

|

|

|

|

Do you wish to publish your Article?

If you wish to share your article with maximum readers then please send it at taxupdate.otu@gmail.com. We shall publish it with all due credit to you.

|

|

The topic can be on GST, Income Tax, Pre-GST laws, PPT, Notes etc. The article may contain 500 words to 1500 words or it may be more than that if the article demands.

|

|

|

|

|

|

|

If you wish to subscribe to weekly Newsletter at Rs. 149/- for one year, please subscribe. We shall send you the updates weekly.

|

|

|

|

|

|

|

Hope the above updates is of use to you. Please share your input and feedback at taxupdate.otu@gmail.com

|

|

|

|

|

|

|

Visit our website

|

OTU provides you

|

- Articles on various topics

|

|

- Media - GST, Income Tax & Press R.

|

|

- Notes / Newsletter at 149/ p.a.

|

|

|

|

|