|

|

|

|

|

|

|

|

onlinetaxupdate team wish to express sincere thanks to all the readers, authors, subscribers for the support extended to us.

|

|

|

|

Dear Reader,

|

Please find newsletter for your reading and reference.

|

|

Newsletter no.108 dated 16.01.2024

|

|

|

Index of the Newsletter

- Recent updates

- GST/IT/Press Release

- Lawgics by Ms. Nidhi Aggarwal

- GST Notes by CMA Anil Sharma

- GST Daily by CA Pradeep Modi

- Judgment Analysis by CA Nitin Bhuta

- Article

- PPT

|

|

|

|

|

|

|

Export consignments to West Asia will continue to receive enhanced insurance cover against payment defaults until September 30, the Directorate General of Foreign Trade (DGFT) said in a notification on Monday.

|

Earlier, the enhanced cover for exporters taking credit risk insurance from Export Credit Guarantee Corporation (ECGC) was available for shipments to West Asia sent between March 16 and June 15.

|

The enhanced risk cover announced on March 19 was part of the Resilience and Logistics Intervention for Export Facilitation (RELIEF) scheme under the Export Promotion Mission (EPM) to support exports to West Asia in view of the Iran war.

|

"The eligibility timelines under Component II of the EPM RELIEF intervention are extended up to September 30, 2026 to support Indian exporters and mitigate logistics challenges arising out of the continuing West Asia Crisis," the DGFT said.

|

Source: The Economic Times

|

|

|

|

|

|

|

|

Threshold limit for Inter-state movement of goods is Rs. 50,000/-. However, for intra-state movement of goods there is exceptional higher limit of Rs.1,00,000/- in some states.

|

Here is the list of e-way bill limit state-wise.

|

|

|

|

|

|

|

|

Directorate General of Foreign Trade (DGFT) issued Public Notice No. 17/2026-27 dated 04.06.2026 regarding Enlistment under Appendix 2E of FTP, 2023-Agency Authorised to issue Certificate of Origin (Non-Preferential)

|

|

|

|

|

|

2 Media - GST/IT/Press Release

|

|

|

|

|

CBIC -

To commemorate nine years of the Goods and Services Tax (GST), the Central Board of Indirect Taxes and Customs (CBIC) organized a special celebration at CSOI, New Delhi, on 1 July 2026. The event was held under the theme, ‘सुगम कर व्यवस्था, सशक्त भारत’, highlighting GST's

|

GST Indore -

The 9th #GSTDay was celebrated with great enthusiasm at CGST & Central Excise Commissionerate, Indore under the theme "सुगम कर व्यवस्था, सशक्त भारत".

|

GST Samvad an interaction among officers, taxpayers, trade & industry representatives, and tax professionals was organised on 30.06.2026 to commemorate nine years of GST as a transformative reform. The programme highlighted taxpayer facilitation initiatives, digital services, policy updates, and the importance of timely and voluntary compliance.

|

9 Years of GST! The CGST Indore Commissionerate celebrated the 9th anniversary of the Goods and Services Tax. The event marked nearly a decade of economic transformation and a unified national market.

|

Recognizing Excellence: The Department felicitated leading revenue contributors-Bharat Petroleum( @BPCLimited), HDFC Limited(@HDFCLTD), and MRF Limited(@MRF_Corporate)-for their exemplary tax compliance.10 dedicated departmental officers and a meritorious student were also honored

|

Taxpayer First: CGST Indore Commissioner Shri Peeyoush Bhati highlighted GST’s role in nation-building and announced that the Commissionerate will now regularly host monthly meetings with taxpayers to address grievances and ensure a transparent, efficient regime.

|

GST Aurangabad Commissionerate -

CGST AURANGABAD building lit up to kick in early 9th GST day celebrations

|

CGST Mumbai West -

As part of the #GSTPakhwada on occasion of upcoming 9th GST Day, on this year’s theme "सुगम कर व्यवस्था, सशक्त भारत” (Easy Tax System, Empowered India), CGST Mumbai West Commissionerate organised an Essay Writing Competition for officers and staff.

|

The winners and participants were felicitated by the Hon’ble Commissioner, CGST&C.Ex. Mumbai West appreciating their enthusiasm and insightful contributions.

|

WIRC of The Institute of Cost Accountants of India

Celebrating one of India’s landmark tax reforms that strengthened transparency, unity and the vision of One Nation, One Tax, One Market.

|

DGTPS MUMBAI CBIC

9वें GST दिवस के उपलक्ष्य में DGTS MZU & AZU द्वारा "Nine Years of GST: Perspective from Taxpayers" विषय पर Kendriya Vidyalayas के विद्यार्थियों हेतु एक वेबिनार आयोजित किया गया।

|

इस सत्र के माध्यम से GST के प्रति जागरूकता, वित्तीय साक्षरता को बढ़ावा दिया गया तथा विद्यार्थियों को राष्ट्र निर्माण में कराधान की भूमिका से अवगत कराया गया।

|

CGST Thane -

CGST Thane organized a 'Hindi & Marathi Essay Competition' for officers & staff

|

The Commissioner honored winners with certificates for outstanding performance

|

Celebrating language, awareness & commitment to GST

|

CGST MUMBAI EAST

As part of the 9th GST Day celebrations, CGST & Central Excise, Mumbai East Commissionerate organised Essay Writing and Drawing Competitions for students of Sandesh Vidyalaya & Junior College, Vikhroli (East), on 30.06.2026, with enthusiastic participation from young students.

|

The essay competition focused on GST and citizens’ responsibility towards tax compliance, while the drawing competition encouraged students to express ideas creatively. Prizes were awarded to winners, promoting taxation awareness and responsible citizenship among young minds.

|

As part of the 9th Anniversary celebrations of GST, CGST & Central Excise, Mumbai East Commissionerate organised GST "SAMVAD" and interactive session with members of trade and tax professionals on 29 June 2026 at Vikhroli to mark the occasion with active participation.

|

The session witnessed enthusiastic participation. Queries on filing of appeals, GST returns and other GST-related issues were addressed by officers, making it a valuable platform for knowledge sharing, constructive dialogue and promoting voluntary tax compliance across sectors.

|

CGST & Customs Thiruvananthapuram Zone

On the occasion of International Day Against Drug Abuse & Illicit Trafficking, the officers and staff of CGST & Customs Thiruvananthapuram Zone took a solemn pledge under the #NashaMuktBharatAbhiyan to build a society free from the menace of drugs.

|

DGTS AHMEDABAD CBIC

30.06.2026 को,DGTS AZU और MZU ने JG University के साथ मिलकर GST Awareness & Overview पर एक हाइब्रिड सेमिनार आयोजित किया।DGTS के Pr. ADG,श्री सुमित कुमार ने उद्घाटन भाषण दिया। CBIC के रिटायर्ड सुपरिटेंडेंट श्री जॉन क्रिश्चियन मुख्य वक्ता थे। #DGTS #GST #GSTDAY2026 #CBIC

|

Article Writing Competition 2026

To commemorate 9th Year of GST, Online Tax Update (OTU) launched 'Article Writing Competition 2026'. Registration starts today 1st July 2026 and ends on 15th July 2026. Article submission till 31st July 2026 and Winner Announcement in August, 2026. Cash Award + Certificate of Participation. Participation fees Rs. 300/- Read more

|

|

|

|

|

|

|

|

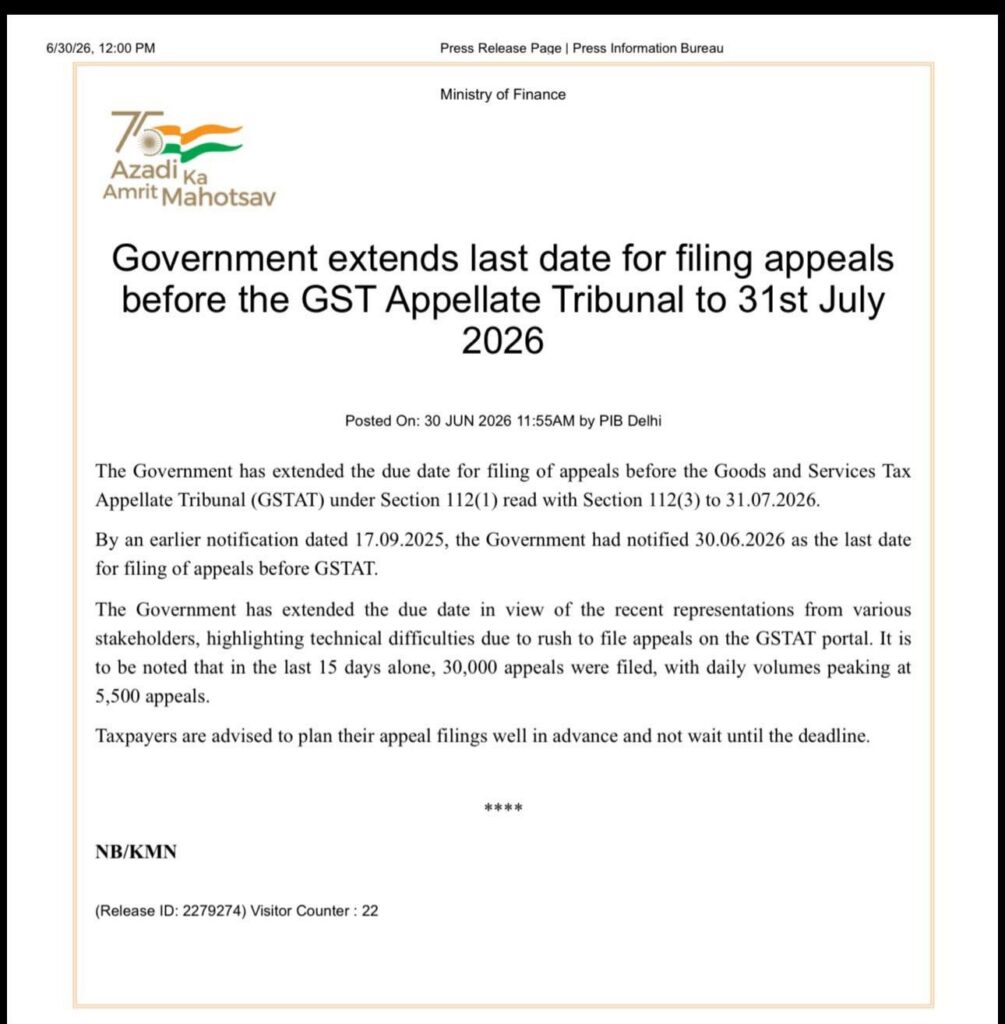

Centre has extended the last date for filing appeals before the Goods and Services Tax Appellate Tribunal (GSTAT) to July 31, 2026, giving taxpayers an additional month to submit their cases after a surge in filings led to technical difficulties on the GSTAT portal.

|

The extension applies to appeals filed under Section 112(1) read with Section 112(3) of the Goods and Services Tax (GST) law.

|

The revised deadline replaces the earlier cut-off of June 30, 2026, which had been notified by the government on September 17, 2025.

|

The decision follows recent representations from various stakeholders who flagged technical issues arising from a rush of appeals being filed on the GSTAT portal ahead of the deadline.

|

While noting that the original due date had been notified well in advance in September 2025, the government said filing activity had intensified sharply in recent weeks. It said 30,000 appeals were filed in the last 15 days alone, with daily filings touching a peak of 5,500 appeals.

|

Advising against eleventh-hour filings, the government urged taxpayers to complete their appeal submissions well in advance to ease pressure on the GSTAT portal.

|

The GST Appellate Tribunal serves as the first judicial appellate forum for taxpayers seeking to challenge orders issued by GST authorities after the disposal of their first appeals.

|

Source: The Economic Times

|

|

|

|

|

|

|

|

|

GST & IDT Committee has requested the Chairman, IDT Committee, ICAI, New Delhi to urgently represent before the respective forums for the date extension of GSTAT, i.e., 30-Jun-2026.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Tata Steel Limited said tax authorities have filed an appeal seeking restoration of penalties worth Rs. 368.72 crore that were earlier dropped in a GST adjudication order, even as proceedings on the underlying demand remain stayed by the Jharkhand High Court, according to a stock exchange filing.

|

"One June 16, 2026, the Assistant Commissioner, Division-I, CGST & Central Excise , Jamshedpur, Jharkhand filed an appeal before the Commissioner (Appeals) of CGST & Central Excise, Ranchi against the above-mentioned Adjudication Order dated December 18, 2026, to the extend that the Adjudicating Authority has dropped the penalty amounting to Rs. 3,68,72,21,158/-," Tata Steel said in its exchange filing.

|

The appeal, filed on June 16 by the Assistant Commissioner, CGST & Central Excise, Jamshedpur, challenges the December 18, 2025, adjudication order to the extent it waived the penalty.

|

The original show-cause notice, issued in June 2025, proposed disallowance of input tax credit for FY 2018-19 to FY 2022-23, with an aggregate GST demand of about Rs. 1,007.55 crore. Of this, Tata Steel said it has already paid Rs. 514.19 crore in the normal course, leaving an alleged exposure of Rs. 493.35 crore.

|

In December 2025, the adjudicating authority confirmed the tax demand of Rs. 493.35 crore, imposed a penalty of Rs. 638.83 crore and applicable interested, while dropping an earlier proposed penalty of Rs. 368.72 crore. Tata Steel subsequently moved the Jharkhand High Court, which granted a stay on all further proceedings in March 2026.

|

"This matter is, inter-alia, contingent upon the final adjudication of the issue concerning the issuance of show cause notices for multiple periods, which is presently sub judice before the High Court," Tata Steel said.

|

Tata Steel added that it has a good case on merit and hence will contest the same before the Appellate Authority within the statutory timelines, noting that the development has no impact on its financial or operational position, arising from the said appeal.

|

Source: The Economic Times

|

|

|

|

|

|

|

|

With the June 30 deadline for filing legacy appeals before the Goods and Services Tax Appellate Tribunal (GSTAT) fast approaching , tax professionals, chartered accountants and industry bodies have urged the Finance Ministry to extend the filing window, warning that persistent technical glitches on the GSTAT portal could prevent thousands of taxpayers from filing their appeals before the deadline.

|

The demand comes as taxpayers seek to file appeals arising from nearly nine years of litigation accumulated during the period when the Tribunal remained non-operational. Experts said the combination of a massive backlog, voluminous documentation and continuing portal-related issues has significantly constrained taxpayers' ability to meet the deadline.

|

According to Aditya Singhania, Founder of Trackase, the backlog is estimated at nearly four lakh to 4.5 lakh legacy appeals, while only around 36,929 appeals have been filed nationalwide so far.

|

"The ground reality is deeply concerning. Against an anticipated backlog of nearly four to four and a half lakh appeals accumulated over nine years of the Tribunal's non-operationality, only around 36,929 appeals have been filed nationally as of now," Singhania said.

|

He attributed the slow pace of filings to the teething troubles of the newly launched e-filing portal, including server time-outs, authentication challenges, payment gateway reconciliation issues and a filing structure that requires considerable time and effort to navigate.

|

Experts cite portal hurdles, record backlog

According to experts and representations submitted to the Finance Ministry, taxpayers continue to face multiple technical issues on the GSTAT portal, including session expiry, repeated login failures., Aadhaar authentication problems, Digital Signature Certificate (DSC) validation failures, payment reconciliation delays and incomplete integration between the Goods and Services Tax Network (GSTN) and the GSTAT portal.

|

Experts said taxpayers are also required to retrieve and compile extensive records accumulated over several years, including adjudication orders, invoices, reconciliations, e-way bills, ledger extracts and other supporting documents, making the filing process particularly time-consuming.

|

CA Nitin Bansal, State-President, BJP CA Cell Haryana, said the Finance Ministry has received several representations highlighting the practical challenges taxpayers are facing in filing appeals before the Tribunal.

|

"With the Tribunal becoming operational after nearly nine years, taxpayers must now prepare and file a substantial backlog of appeals within a limited window, many involving voluminous, multi-year records, even as the GSTAT e-filing portal continues to stabilise," Bansal said.

|

He added that extending the deadline would be revenue-neutral as the mandatory pre-deposit and other conditions would remain unchanged while ensuring genuine taxpayers are not denied their appellate remedy because of circumstances beyond their control.

|

Over-time extension sought

CA Sonu Goel, Chairman, Panipat Branch of the Institute of Chartered Accountants of India (ICAI), said a one-time extension would ensure disputes are decided on their merits rather than procedural constrints.

|

"One-time extension would safeguard taxpayers' right to appeal, uphold the principles of natural justice, and ensure that dispute are decided on merits rather than being defeated by procedural or technological constraints. This pragmatic relief would further reinforce the Government's commitment to ease of doing business while maintaining certainty and confidence in the GST ecosystem," Goel said.

|

Parag Mehta, Partner at N.A. Shah Associates LLP, said the portal continues to experience issues ranging from login failures and incorrect fee calculations to disappearing data.

|

"Considering the fact that the portal is not fully supporting the filing process and the number of appeals filed remains significantly lower than expected, the deadline should be extended. GSTAT is an important appellate remedy and taxpayers should not be deprived of that opportunity," Mehta said.

|

Bas association flags nationwide concerns

The Sales Tax Bar Association has also written to the Finance Ministry seeking an extension of the filing deadline, stating that taxpayers and tax professional across the country continue to face significant practical and technical difficulties while filing appeals through the GSTAT portal.

|

In its representation, the association said the present limitation period covers appellate orders accumulated over nearly nine years when the Tribunal remained non-functional, requiring taxpayers to retrieve historical records and prepare detailed documentation within a limited period.

|

The association highlighted recurring issues including server interruptions, repeated Aadhaar authentication and DSC validation failures, payment gateway reconciliation delays, manual duplication of information already available on the GSTN portal and challenges in uploading voluminous records.

|

It warned that if the deadline is not extended, thousands of taxpayers could lose the opportunity to pursue their statutory appeals because of technological and procedural constraints, potentially leading to avoidable litigation before various High Courts.

|

Prabhat Ranjan, Senior Director at Nexdigm, said extending the filing deadline has become "the need of the hour".

|

"The appellate process should be about the actual merits of the issues between both parties and not technical questions of delay. This is a taxpayer-friendly measure that will make GST dispute resolution processes more fair and credible," he said.

|

As of publication, the government has not announced any extension of the June 30 deadline for filing legacy GSTAT appeals. While the GSTAT has extended the period for relaxed scrutiny of filed appeals until December 31, 2026 , tax professionals, industry experts and representative bodies continue to seek a one-time extension of the filing deadline, arguing that additional time would enable taxpayers to exercise their statutory right of appeal without affecting revenue, as the mandatory pre-deposit requirements would continue to apply.

|

Source: The Economic Times

|

|

|

|

|

|

|

|

Businesses shifting their principal place of business to a new GST jurisdiction will not have to restart pending tax proceedings with the Central Board of Indirect Taxes and Customs (CBIC) clarifying that the new jurisdictional authority will take over and complete all ongoing cases from the stage at which they were left, reported PTI.

|

The clarification comes after the CBIC received references from field formations seeking guidance on the validity of proceedings and the authority responsible for handling cases when a registered taxpayer changes jurisdiction because of a shift in its principal place of business.

|

Under the circular, any action or proceeding - including investigation, audit, show cause notice or adjudication under the Central GST law - initiated by the tax officer having jurisdiction over the registered taxpayer at the time the action was undertaken (transferor jurisdiction authority) will remain valid even if the taxpayer subsequently shifts to another tax jurisdiction (transferee jurisdictional authority).

|

"The transferee jurisdictional authority shall act upon, give effect to, and proceed on the basis of such earlier valid action taken by the transferor jurisdictional authority, as if it had itself initiated the same," the CBIC said in the circular.

|

The indirect tax board further clarified that if any fresh issue comes to the notice of the earlier jurisdictional authority after the taxpayer has shifted, the tax officer should intimate the new jurisdictional officer for appropriate action.

|

"Where the taxable person migrates to another jurisdiction during the pendency of any action or proceeding initiated by the transferor jurisdictional authority, the transferee jurisdictional authority shall take over and conclude the same from the stage at which it stood at the time of migration/ transfer," the CBIC circular said.

|

The new jurisdictional officer will also have the authority to initiate and conclude any consequential proceedings arising from the case.

|

Rajat Mohan, Managing Partner at AMRG Global, said the clarification addresses a key procedural gap under the GST regime.

|

"By clearly defining the responsibilities of transferor and transferee authorities, CBIC has removed ambiguity that often resulted in jurisdictional objections and delays in adjudication," Mohan said.

|

Source: The Times of India

|

|

|

|

|

|

|

|

On the occasion of 9th GST Day to be celebrated on 1st July, 2026 the Central Board of Indirect Taxes and Customs vide Office Memorandum dated 29.06.2026 has decided to grant Certificate of Meritorious Service (CBIC-CMS) to the following officers:

|

|

|

|

|

|

|

|

The Malad Chamber of Tax Consultants made a representation to the Hon'ble Union Finance Minister, Smt. Nirmala Sitharaman, New Delhi on 26.06.2026 requesting an extension of the statutory deadline for filing GSTAT appeals under Section 112 of the CGST Act, 2017 from 30th June 2026 to 31st December 2026.

|

|

|

|

|

|

|

|

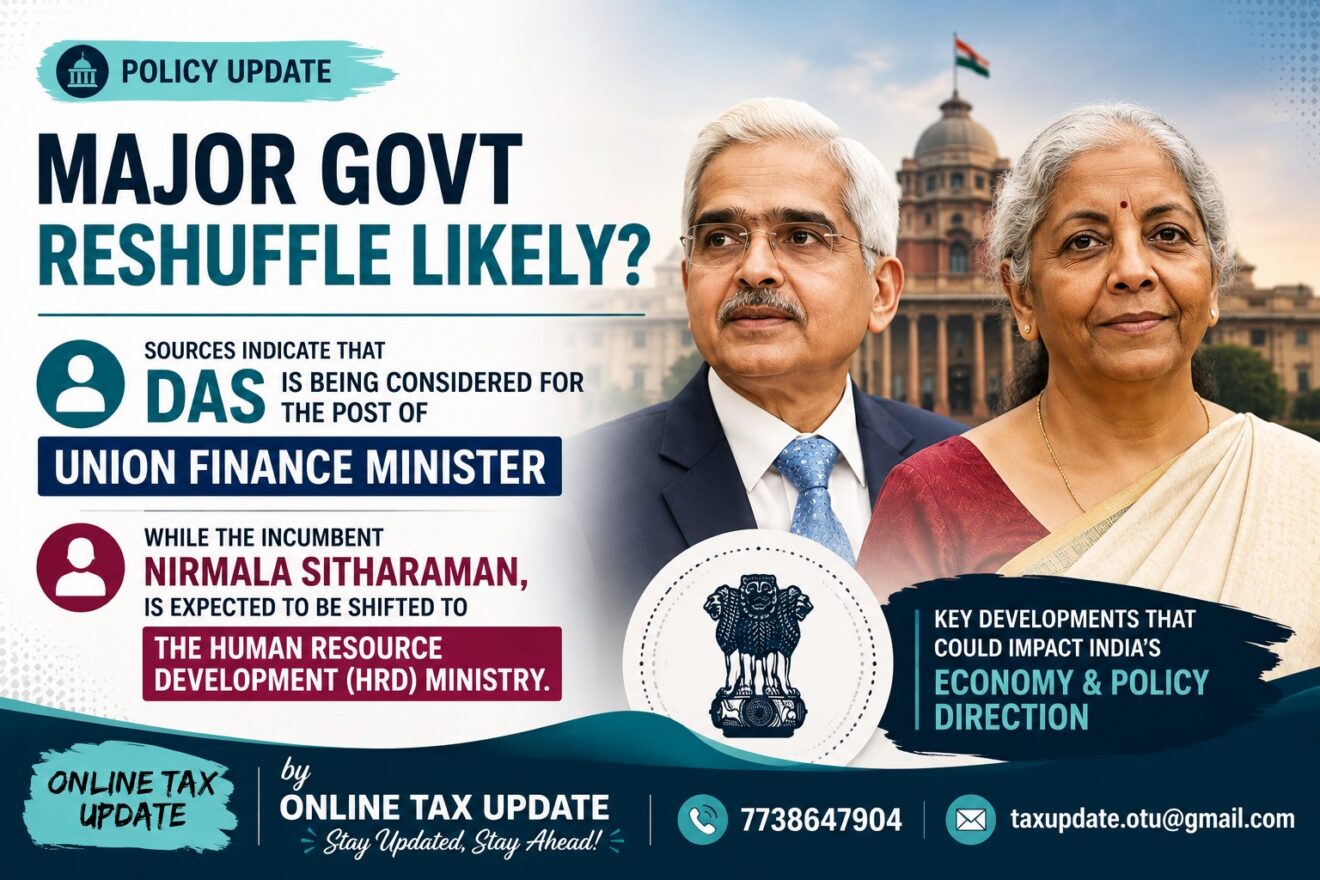

The recent meeting between Prime Minister Narendra Modi and President Droupadi Murmu, followed by a meeting between Home Minister Amit Shah and the President, have fuelled speculation over a possible Union cabinet reshuffle as well as changes in the BJP's organisational structure.

|

According to sources, the reshuffle is likely to take place before the upcoming Monsoon Session of Parliament.

|

Among the names being discussed is that of former Reserve Bank of India (RBI) governor Shaktikanta Das, who is currently serving as the Principal Secretary to the Prime Minister.

|

Sources indicated that Das is being considered for the post of Union finance minister, while the incumbent , Nirmala Sitharaman, is expected to be shifted to the human resource development (HRD) ministry. Sitharaman has been serving as the Union Minister for finance and corporate affairs since 2019.

|

There has, however, been no official confirmation from either the government or the BJP regarding any proposed changes.

|

If the move materialises, it would bring into the Cabinet a seasoned administrator with more than four decades of experience across several areas of governance.

|

Das served as the 25th Governor of the RBI from 2018 to 2024. Before assuming charge at the RBI, he was a member of the 15th Finance Commission and India's G20 Sherpa.

|

Over the course of his career, Das has held several key positions in both the Central and State governments, handling portfolios related to finance, taxation and industries and infrastructure.

|

During his tenure in the finance ministry, he was closely associated with the preparation of eight Union Budgets, giving him extensive experience in public finance and economic policymaking. Besides, Das was also the senior Department of Economic Affairs official in the finance ministry during the planning and implementation phase of demonetisation.

|

A postgraduate from St. Stephen's College, University of Delhi, Das has also served as India's Alternate Governor to the World Bank, the Asian Development Bank, the New Development Bank, and the Asian Infrastructure Investment Bank. He has represented India at major international forums, including the IMF, G20, BRICS, and SAARC.

|

|

|

|

|

|

|

|

Kolkata is likely to host the 57th meeting of the GST Council next month, sources said, although the Union Finance Ministry has not yet officially confirmed the venue or the schedule. The meeting is expected to be held in the second half of July, and could take up the next round of indirect tax policy reforms.

|

Hosting the meeting in Kolkata holds significance as it would mark one of the first major meetings of a Constitutional federal body in West Bengal after the Assembly elections. While the GST Council independently decides its agenda and meeting schedule, the choice of Kolkata would coincide with the Centre’s broader emphasis on strengthening the State’s profile as a destination for investment and financial activity following the change in government.

|

New reforms

The previous GST Council meeting, held on September 3, 2025, came after a gap of nearly nine months, despite the rules providing for at least one meeting every quarter. That meeting unveiled GST 2.0, including rate rationalisation and measures to ease compliance. Tax experts now expect the council to consider another set of policy reforms, some of which were discussed during 4th Annual Seminar on Direct and Indirect Taxes of the Bengal Chamber of Commerce & Industry (BCCI).

|

Vivek Jalan, Chairperson of the National Fiscal Affairs and Taxation Committee of BCCI, said that in the spirit of GST 2.0, which was launched to strengthen India’s manufacturing base, the council should correct the anomaly of non‑refund of Input Service ITC under the inverted duty structure. While GST 2.0’s rate rationalisation has supported consumption, the cost pressures has deepened on manufacturers. “Addressing this gap will ensure reducing cascading taxes, boosting competitiveness and advancing India’s vision of becoming the world’s third‑largest economy by 2047,” he said.

|

Also, it has been proposed before the GST Council to consider reducing the GST rate on autism care centres and allied sectors from 18 per cent to 5 per cent. Such a measure under GST would ease the financial strain on families and institutions, while reinforcing the government’s vision of inclusive growth. “By aligning tax policy with compassion, the council can ensure that essential services for differently‑abled children remain affordable, accessible and sustainable, a step that truly reflects the spirit of GST reforms,” said Jalan.

|

Source: The Hindu businesline

|

|

|

|

|

|

|

|

The Karnataka State Chartered Accountants Association (R) (KSCAA) has submitted a representation highlighting practical and procedural issues faced by taxpayers and professionals in relation to the Goods and Services Tax Appellate Tribunal (GSTAT). The representation focuses on addressing operational challenges and suggesting measures to enhance the efficiency, accessibility, and effectiveness of the GSTAT framework.

|

Considering the initial challenges faced by stakeholders in adapting to the newly operational GSTAT framework and portal, KSCAA has also requested an extension of the timelines for filing appeals and related compliances, so that taxpayers are not prejudiced on account of procedural and technical difficulties. Addressing these concerns and providing adequate transition time will facilitate smoother implementation, reduce avoidable litigation, and ensure meaningful access to the appellate remedy envisaged under the GST law.

|

|

|

|

|

|

|

|

Nine years after the rollout of the goods and services tax (GST) regime, businesses have largely embraced India's biggest indirect tax reform, with 99% reporting a positive or neutral experience, according to a Deloitte India survey. As the tax regime matures, businesses are now shifting their focus to ‘GST 2.0’, seeking reducing disputes, speeding up of refunds, improving working capital and simplifying compliance.

|

The findings come at a time when GST collections continue to be robust. In May, the Centre and states together collected ₹1.94 trillion in gross GST revenue, before adjusting for refunds, up 3.2% from ₹1.88 trillion mopped up a year ago.

|

The survey covered 1,096 C-suite and C-1 level executives across banking and financial services, consumer, energy, resources and industrials, government and public services, life sciences and healthcare, global capability centres, private equity and venture capital, and technology, media and telecommunications. Respondents included micro small and medium enterprises (MSMEs), large companies and very large enterprises.

|

About 69% respondents identified compliance digitalization as the biggest benefit of GST, followed by supply chain optimization and gains from rate rationalization. The survey noted that confidence in GST has been driven by the digitalization of compliance, automation of tax processes and the stabilization of e-invoicing and e-way bill systems.

|

"GST has significantly improved compliance and transparency with the GST Network as India's trusted tax framework. This digital backbone enables taxpayers, businesses and the government with real-time compliance and data-driven decision-making," said Gokul Chaudhri, president, tax at Deloitte South Asia.

|

Businesses ranked interpretational clarity as their top policy priority, with 87% of the respondents seeking greater certainty in tax administration. This was followed by demands for improved working capital management (67%), uniform audits (61%) and faster refunds.

|

The survey also found strong support for centralized audits, simplified GST rates and allowing reverse-charge mechanism payments through input tax credit.

|

"The key industry expectations include the need to resolve interpretational ambiguities, improve working capital through streamlined refunds and credit utilization, address ITC disputes and implement a unified and harmonized audit process," said Mahesh Jaising, partner and leader, indirect tax at Deloitte India.

|

Addressing inverted duty structures emerged as another major area of concern. Nearly 69% of respondents favoured expanding the refund formula to include all input taxes, while 63% supported further rate rationalization to reduce inversion-related issues. More than half sought refund benefits for accumulated input tax credit balances.

|

Technology is expected to play a bigger role in the next phase of GST reforms. Nearly 89% of respondents supported the use of artificial intelligence (AI) for tax data processing and reconciliation, while many sought a unified taxpayer dashboard, automatic tax utilization and improved integration across GST systems.

|

The survey found that priorities varied across sectors. Consumer and energy firms highlighted supply-chain optimization as the biggest gain from GST, while technology companies placed greater emphasis on compliance digitalization. Life sciences and healthcare companies cited benefits from competitive pricing following rate rationalization, while BFSI and global capability centres favoured greater automation and integrated digital infrastructure.

|

For MSMEs, quarterly return filing emerged as the most appreciated reform, with positive responses rising to 67% in 2026 from 12% in 2023. Smaller businesses also strongly supported invoice-based input tax credit eligibility, quarterly payment mechanisms and faster refunds to ease liquidity pressures, the survey said.

|

Some economists underscored the need for a more efficient refund mechanism under GST.

|

“Faster and more predictable GST refunds are critical for improving business cash flows. Delays in refunds increase working capital requirements and financing costs," said Dharmveer, assistant professor, economics at the Delhi School of Economics. "A more streamlined refund mechanism would enhance liquidity, especially for MSMEs and exporters, and support investment and growth.”

|

GST was introduced on 1 July 2017 as India's biggest indirect tax reform, replacing multiple central and state taxes with a single tax system. Since then, the regime has evolved with the rollout of e-invoicing, e-way bills and other digital compliance measures aimed at making tax administration easier and more transparent.

|

|

|

|

|

|

|

|

A Kanpur man is making headlines after he received relief from the Income Tax Appellate Tribunal (ITAT) in a case involving a Rs 1.95 crore trading loss incurred through his wife’s account.

|

According to The Economic Times, the man, whose identity remains undisclosed, transferred funds to his wife's account and used it to carry out Futures and Options (F&O) trading. The transactions resulted in a loss of Rs 1.95 crore during the financial year. When filing his income tax return, he reported the loss on his own return and adjusted it against his income.

|

However, the Income Tax Department challenged the claim and raised a tax demand, stating that the loss belonged to his wife's account and therefore could not be adjusted against the husband's income.

|

The dispute eventually reached the ITAT's Lucknow Bench. After examining the facts, the tribunal found that the husband had transferred funds to his wife's account, and that he carried out the trading through his wife's account, and the loss occurred there.

|

The tribunal pointed out that, under the Income Tax Act’s clubbing rules, income generated from assets gifted or transferred to a spouse is typically included in the transferor’s income.

|

|

|

|

|

|

|

|

The Uttar Pradesh Electricity Regulatory Commission (UPERC) has ruled that the reduction in GST on renewable energy equipment from 12% to 5% will be treated as a “Change in Law” event under power purchase agreements signed under the PM-KUSUM Component-C2 scheme.

|

In a suo motu order issued on June 23, the Commission said the GST reduction, effective September 22, 2025, lowers the cost of procuring solar and other renewable energy equipment and therefore reduces the overall capital cost of projects. The resulting financial benefit must be passed on to the power procurer, Uttar Pradesh Power Corporation Ltd (UPPCL), and, ultimately, to consumers.

|

UPERC noted that the Ministry of Power had advised regulators to recognise the GST reduction as a Change in Law event and ensure that the benefits are transferred to consumers at the earliest.

|

The order applies to projects whose bids were submitted before September 22, 2025, and where invoices were raised or payments made on or after that date. The Commission directed that project-wise assessments be conducted to quantify the actual savings resulting from the GST reduction.

|

To implement the exercise, UPERC has ordered the constitution of expert committees comprising representatives of UPNEDA, UPPCL, the concerned discom and finance officials. Developers will be required to submit supporting documents, including invoices, payment records and auditor certificates, to establish the benefit accrued.

|

The Commission said revised tariffs would be determined on a project-by-project basis and directed developers and UPPCL to complete the assessment process within 90 days of the project’s commercial operation date.

|

Source: The Hindu business line

|

|

|

|

|

|

|

|

Sales Tax Bar Association (Regd.) (STBA) made representation for extension of the time limit for filing appeals before the Goods and Services Tax Appellate Tribunal (GSTAT) vide letter reference STBA/2026/25 dated 25.06.2026

|

Subject: Representation seeking extension of the time limit for filing appeals before the Goods and Services Tax Appellate Tribunal (GSTAT) beyond 30.06.2026 on account of persistent technical and practical difficulties in the GSTAT e-filing portal.

|

- Sales Tax Bar Association (Regd.), having been established on 30th March, 1957, is one of the oldest and the largest Association of Tax Professionals in the country. The Bar represents majority of members of various professions practicing in the Direct & Indirect Taxes. Sales Tax Bar Association (Regd.) plays a major role in revenue collection by the department. Present membership of our Bar Association is around 2000 comprising of Advocates, CA's and Tax Practitioners. Some of our members were elevated as Judges of the Hon'ble Delhi High Court and elevated as Judges of the Hon'ble Supreme Court. Some of our members further were also selected for appointment as Member of the Income Tax Appellate Tribunal (ITAT) and Goods & Services Tax Appellate Tribunal (GSTAT).

- However, despite the commencement of the Tribunal and the introduction of the online filing mechanism, taxpayers and tax professionals across the country continue to face substantial practical and technical challenges in filing appeals through the GSTAT portal. These difficulties are neither isolated nor individual in nature. Our Association has received numerous grievances from Professionals practicing across different State highlighting recurring issues that have significantly affected the ability of taxpayers to file appeals within the prescribed period.

- It is respectfully submitted that the Government has already been very sensitive to the problems faced by the taxpayers in filing of the appeals in the GSTAT and accordingly the Government vide Notification No. S.O. 4220 (E) dated 17.09.2025 had issued a notification by exercising its power under Section 112 (1) of the CGST Act, 2017. That vide the said Notification the Government had notified the due date for filing of appeal before the Appellate Tribunal as 30th June, 2026 in respect of all cases, where the order sought to be appealed against was passed on or before 01st April, 2026.

- It is respectfully submitted that thus the present limitation period pertains to appellate orders accumulated over almost nine years, during which the Tribunal remained non-functional. Preparation of these appeals itself requires considerable effort, including retrieval of old records, compilation of tax demands and preparation of detailed paper books. The recent operationalisation of the GSTAT portal has, therefore, resulted in an unprecedented volume of appeals being required to be prepared and filed within a comparatively shot period.

- While taxpayers and professionals have made every endeavour to comply with the prescribed timelines, the practical functioning of the portal has substantially reduced the effective period available for filing appeals. Some of the major difficulties experienced across the country are summarised below:

- Firstly, taxpayers continue to experience frequent portal-related issues including slow response time, session expiry, server interruptions and repeated login failures. In several instances, professionals spend considerable time completing an appeal, uploading documents and entering detailed information, only to find that the session has expired or the portal has hanged and become unresponsive, compelling them to recommence the entire process.

- Secondly, repeated failures in Aadhaar authentication and Digital Signature Certificate (DSC) validation have caused significant disruption in completing the filing process. Even where taxpayers possess valid Aadhaar credentials and duly registered Digital Signature Certificates, authentication, frequently fails or requires multiple attempts before the appeal can proceed further to the next stage.

- Thirdly, payment of the mandatory pre-deposit and court fee through the integrated payment gateway has also presented considerable practical difficulties. There have been instances where payments are debited from the taxpayer's account but the payment status is not immediately reflected on the portal, creating uncertainty regarding successful filing and necessitating further follow-up and reconciliation.

- Fourthly, the portal presently requires extensive manual entry of information which is already available on the GST common portal. Instead of seamless integration between the GSTN and the GSTAT portal, taxpayers are required to repeatedly enter registration particulars, order details and other information , making the filing process unnecessarily time-consuming and increasing the possibility of inadvertent errors.

- Fifthly, appeals under the GST regime frequently involve voluminous records comprising show cause notices, replies, adjudication orders, appellate orders, invoices, reconciliations, e-way bills, ledger extracts bank details and other supporting documents accumulated over several years. Preparation of such records in accordance with the portal's prescribed technical specifications regarding document size, format and uploading requirement has itself become a substantial exercise, particularly for appeals involving complex factual issues.

- Further, practical issues continue to be experienced in filing appeals relating to certain categories of persons, including matters involving penalties imposed upon directors, partners and other persons who do not have a valid GST registration. In several such cases, the portal does not presently facilities smooth filing of appeals, thereby creating uncertainty regarding the availability of the appellate remedy.

- It may also be appreciated that the GSTAT is a newly operationlised appellate forum with a completely new electronic filing framework. Taxpayers, advocates, chartered accountants and tax practitioners across the country are simultaneously familiarising themselves with the portal architecture, procedural requirements and filing methodology. A reasonable transition period is, therefore, both necessary and desirable to ensure effective implementation of this important final facts finding appellate forum.

- The above circumstances demonstrate that the request for extension does not arise on account of any lack of diligence on the part of taxpayers or professionals. On the contrary, taxpayers are making genuine efforts to exercise the statutory remedy available to them but are encountering practical difficulties beyond their control while navigating a newly introduced electronic problem.

- If the present timeline is not extended, thousands and thousand of genuine taxpayers may lose the opportunity to avail the appellate remedy solely because of technical and procedural difficulties associated with the portal. Such a situation would inevitably lead to avoidable litigation before various High Courts seeing appropriate reliefs in respect of limitation and portal-related issues , thereby increasing the burden upon the judiciary, the Department and the Tribunal itself. This would also run contrary to the Government's consistent objective of promoting ease of doing business, reducing litigation and facilitating voluntary tax compliance through efficient digital governance.

- It is respectfully submitted that granting a reasonable extension would not prejudice the interest of the Revenue in any manner. The statutory conditions governing appeals, including the mandatory pre-deposit prescribed under the Act, would continue to remain fully applicable. The extension would merely ensure that genuine taxpayers are afforded a fair and effective opportunity to avail the appellate remedy intended by the Legislature, while simultaneously allowing adequate time for further stabilisation of the GSTAT portal.

- In these circumstances, we most respectfully request your kind intervention to :

- Extend the last date for filing appeals before the GST Appellate Tribunal from 30.06.2026 to 30.09.2026 or for such further period as the Government may consider appropriate.

- Ensure that taxpayers facing genuine portal-related technical difficulties are not deprived of their opportunity to file appeals on account of circumstances beyond their control; and

- Continue strengthening and stabilising the GSTAT e-filing system during the extended period so that the objective of establishing an efficient, accessible and technology-driven appellate mechanism may be fully realised.

We are confident that your good office, which has consistently demonstrated its commitment towards taxpayer-friendly reforms and fair tax administration, will kindly consider this genuine request sympathetically in the larger interest of justice, efficient tax administration and ease of doing business.

|

We shall remain grateful for your kind consideration.

|

,

President (m) : 9810071545

|

,

Secretary (m) : 9811949733

|

- Hon'ble Minister of State for Finance, Room no. 16042, 6th Floor, A Wing, Kartavya Bhawan -I, New Delhi - 110001.

- The Revenue Secretary, Ministry of Finance, Govt. of India, Room No. 14102, Kartavya Bhawan - I, New Delhi -110001.

- The Joint Secretary, GST Council, 5th Floor, Tower II, Jeevan Bharti Building, Connaught Place, New Delhi-110001.

- The Chairman, CBIC, North Block, Central Secretariat, Room No. 14042, Kartavya Bhawan - I, New Delhi -110001.

- The President, GSTAT Pr. Bench, 6th Floor, Tower II, Jeevan Bharti Building, Connaught Place, New Delhi-110001.

|

|

|

|

|

|

|

GST Appellate Tribunal Bar Association, Delhi made a representation before The Chairman, Central Board of Indirect Taxes and Customs, Department of Revenue, Ministry of Finance, Government of India, North Block, New Delhi - 110001 vide Letter Ref. No. GSTATBAR/2026/005 dated 20.06.2026 seeking extension of the last date for filing appeals before GSTAT.

|

- Locus standi of the Association : The GSTAT Bar Association, Delhi ("the Association") is a duly constituted representative body of Advocates, Chartered Accountants and other tax professionals enrolled to practise before the Goods and Services Tax Appellate Tribunal ("GSTAT"/"the Tribunal"), with its registered office at the address mentioned above. The Association is a recognised stakeholder body under the GST Appellate Tribunal (Procedure) Rules, 2025, and its locus standi to espouse the collective grievances of its members, and through them of the larger body of assessees they represent, is fortified by the law laid down by the Hon'ble Supreme Court in S.P. Gupta v. Union of India, (1981) Supp SCC 87, wherein it was authoritatively held that any person or body possessing sufficient interest is entitled to maintain an action for redressal of a public injury, more so where the grievance concerns denial of affective access to a statutory forum of adjudication. It is in this representative capacity, in furtherance of the collective professional and public interest, that the present representation is respectfully submitted, and not in any individual cause.

- Statutory backdrop: Vide Notification bearing F. No. A-50/7/2025-GSTAT-DoR dated 17.09.2025 (S.O. 4220(E)), issued in exercise of the power conferred by sub-section (1) of Section 112 of the Central Goods and Services Tax Act, 2017 (‘the CGST Act’), and on the recommendation of the GST Council made at its 56th meeting held on 03.09.2025, the Central Government notified 30.06.2026 as the outer date up to which appeals in respect of orders communicated to the appellant before 01.04.2026 may be filed before the GSTAT. It is respectfully submitted that the said Notification was itself a product of the Government’s own recognition articulated through the Council’s recommendations – that the Tribunal, having remained non-functional for over nine years from the enactment of the CGST Act despite its constitution under Section 109 thereof, required a calibrated and staggered window to absorb the entire backlog of second appeals, estimated at over 4.8 lakh matters nationally against which only 20,111 appeals were filed by today. The Association submits, with the utmost respect, that the very rationale which persuaded the Government to grant this one-time window continues to subsist – and has, if anything, been aggravated – by reason of the persistent and substantial technical infirmities of the GSTAT e-filing portal (efiling.gstat.gov.in), none of which lie within the control of the taxpayer or his authorised representative, as elaborated in the grounds set out hereinbelow.

- It is further submitted that under Section 1 12(8) of the CGST Act, a pre-deposit of ten per cent (10%) of the disputed tax amount, over and above the deposit made under Section 107(6) at the first appellate stage, is a mandatory jurisdictional condition precedent for maintainability of the second appeal. The Board itself, recognising the difficulty faced by taxpayers in complying with this requirement during the period when the Tribunal was yet to become operational, had issued an interim mechanism vide Circular No. 224/18/2024 GST dated 11.07.2024. The grievances articulated below demonstrate that infirmities of a closely analogous nature persist even at the present, post operationalisation stage.

GROUND I – The Department’s own Advisory on online payment of court fees is, in substance, an admission of the payment-gateway infirmity, and offers no enforceable safeguard

|

It is submitted that the Department has itself issued an Advisory regarding online payment of court fees on the GSTAT portal (enclosed as Annexure B), which records, in terms, that where online payment has been made but the status is not reflected as ‘Success’: (i) the taxpayer is to wait upto 72 hours for the status to update; (ii) if the status does not update even thereafter, the system will not restrict or prevent filing; (iii) the taxpayer may proceed with filing without interruption; and (iv) the payment status shall be reconciled at the back end without adverse effect on the filing.

|

The Association submits, with respect, that this Advisory is, by itself, a candid and authoritative admission by the Department of the very Bharatkosh payment-gateway infirmity. More fundamentally, the Advisory is a mere administrative instruction having no statutory force under the CGST Act, the GSTAT Procedure Rules, 2025, or any notification issued thereunder; it is well settled that administrative circulars and instructions, howsoever salutary, cannot rewrite or substitute for the statute or the rules, and confer no independently enforceable right upon the taxpayer in the event the promised back-end reconciliation does not, in fact, materialise. A taxpayer whose appeal is, notwithstanding the Advisory, subsequently treated as deficient or time barred for want of a reconciled payment is left without remedy, since the Advisory creates an expectation without a corresponding statutory guarantee and therefore, it itself underscores the necessity of the extension and safeguards prayed for herein.

|

GROUND II – The mandatory checklist on the GSTAT portal travels beyond the requirements of the CGST Act and the Rules framed thereunder

|

It is submitted that several of the declarations and fields comprised in the mandatory checklist at the GSTAT Portal find no corresponding requirement either in Section 1 12 of the CGST Act or in the GSTAT Procedure Rules, 2025, and are, in substance, extra-statutory conditions superimposed by the portal’s own design.

|

It is a settled principle of administrative law that subordinate legislation and, a fortiori, a portal-level procedural prescription having even less statutory sanctity than a rule must conform to, and cannot travel beyond, the scope of the parent enactment. A checklist item unmoored from any statutory requirement, yet mandatorily insisted upon as a pre-condition to filing, is to that extent ultra vires and cannot be permitted to obstruct the substantive right of appeal conferred by Section 112.

|

GROUND III – Technical specifications such as 300 DPI scanning resolution and a 250-page document limit, nowhere prescribed under the Act, impose an unreasonable burden on tax professionals who are not, and cannot be expected to be, Information Technology professionals

|

It is submitted that’ the portal mandates document uploads to conform to a specific scanning resolution of 300 DPI and a per-document page 1imit of 250 pages, neither of which finds any mention whatsoever in the CGST Act, the GSTAT Procedure Rules, 2025, or any notification or circular issued thereunder. Such granular technical specifications, devised entirely at the portal’s back end, cannot reasonably be expected to be known> let alone complied with, by a tax professional whose domain expertise lies in tax law and litigation, and not in information technology or document engineering. A procedure that is just, fair and reasonable. A tax professional ought not to be held, nor in fact be capable of being held, to the standard of an Information Technology professional, and the imposition of such an undisclosed and disproportionate technical threshold renders the filing process oppressive and arbitrary qua an entire class of otherwise diligent and compliant appellants.

|

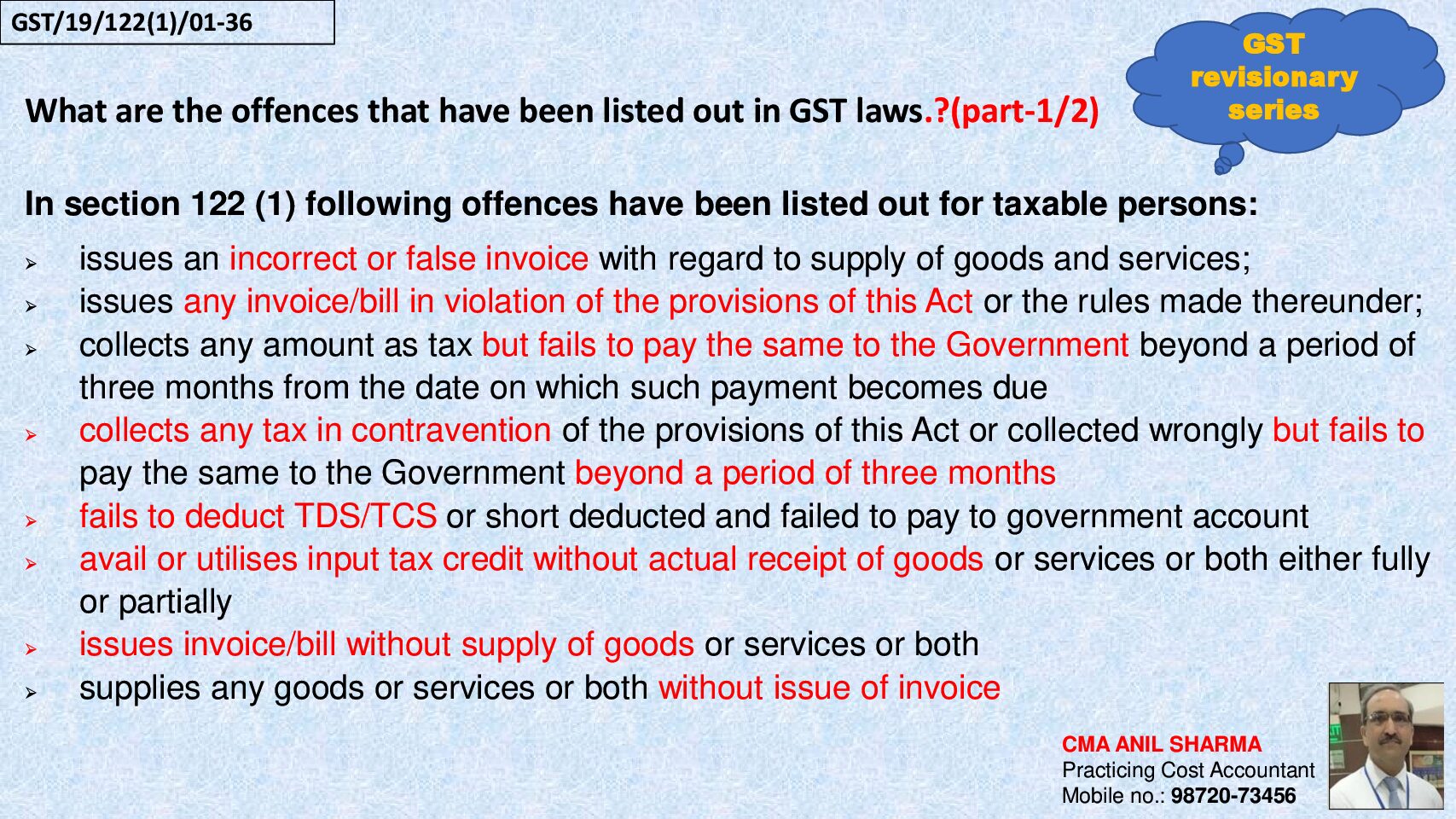

GROUND IV – Non-generation of Temporary ID in penalty matters under Section 122 read with Section 125

|

In matters involving penalty levied under Section 122 read with Section 125 of the CGST Act, the portal does not generate a Temporary Identification Number for the affected category of taxpayers, thereby foreclosing the very gateway for initiating the appeal process. The inability to even register on the forum, let alone file an appeal, amounts to a complete denial of the statutory right of appeal under Section 112, and calls for the justice-oriented approach.

|

GROUND V – Demand tab rendered uneditable upon submission

|

Once particulars in the ‘Demand’ tab of Form GST APL-05 are submitted on the portal, the same become permanently non-editable, even where a bona fide, inadvertent error requires correction before final submission. This rigidity, devoid of any provision for rectification, offends the rule of audi alteram partem and the broader principle that the maxim actus curiae neminem gravabit , “an act of the forum administering justice shall prejudice no one”, applies with equal force to a defect engineered by the portal’s own design and not by any fault of the appellant.

|

GROUND VI – The Act nowhere excludes filing of physical/hard copies of the appeal; an electronic-only filing regime devised by the Tribunal itself, without statutory warrant, amounts to a denial of the right of appeal and, in consequence, of justice itself

|

It is submitted, with the utmost respect but in the strongest terms, that neither Section 112 of the CGST Act nor any other provision thereof anywhere stipulates that an appeal before the GSTAT shall be maintainable only if filed electronically, to the exclusion of physical or hard-copy filing. The insistence on an electronic-only mode of filing is a creature of the Tribunal’s own procedural prescription, and not of the parent statute, and falls within the same vice of excess delegation.

|

Where the electronic mode is itself beset with substantial and unremedied infirmities, the foreclosure of any physical or manual fallback mechanism converts a procedural choice into a complete denial of the substantive right of appeal for the class of appellants who fall victim to those infirmities. Access to a forum of adjudication is not a matter of mere procedural convenience but is itself part of the guarantee of Article 14, and, in appropriate cases, Article 21 of the Constitution, as authoritatively held by the Hon’ble Supreme Court in various cases, where access to justice was recognised as a fundamental right in itself. The maxim ubi jus ibi remedium, “where there is a right, there is a remedy”, stands inverted on its head where the only prescribed remedy is rendered, by the remedy-giver’s own infrastructural failure, practically inaccessible: in such a state of affairs, no appeal is possible, and no appeal, in the plainest and most literal sense, means no justice; and justice withheld in this manner is justice denied as surely and as completely as if it had been refused outright.

|

GROUND VII – Repeated failure of Aadhaar authentication

|

Aadhaar-based authentication, intended to be a one-time, auto-populated exercise at the threshold of registration (the portal having itself fetched the taxpayer’s data from GSTN at the time of registration), is, on account of server side malfunction, required to be repeated eight to ten times within a single filing session, with complete Aadhaar particulars having to be manually re-entered on each occasion despite the data already being available with the system. Such repetitive, server-induced failure falls squarely within the mischief addressed by the Hon’ble Supreme Court in Union of India v. Filco Trade Centre Pvt. Ltd. , (2022) SCC OnLine SC 1006, wherein, taking judicial notice of technical glitches on the GST Network preventing taxpayers from availing ofa statutory right (transitional credit, in that case), the Apex Court directed reopening of the common portal for a further period of two months, holding in effect that a genuine technical inability to comply cannot be visited upon the taxpayer or permitted to defeat a substantive statutory right.

|

GROUND VIII – Bharatkosh payment gateway failures

|

The integration between the GSTAT portal and the Bharatkosh (Non-Tax Receipt Portal) gateway, through which both court fees and the Section 112(8) pre-deposit are required to be remitted, suffers from chronic latency, with sessions repeatedly timing out before the transaction can be completed despite multiple attempts. Where the appellant’s account is debited but no corresponding receipt is generated – a scenario expressly acknowledged in the portal’s own help documentation under the description ‘ Account Debited, but Payment Failed’ – the appellant is left remediless pending manual reconciliation, a delay wholly attributable to the Respondent’s own payment infrastructure and to no laches whatsoever on the part of the appellant.

|

GROUND IX – Non-availability of pre-deposit functionality for directors/partners

|

The mandatory pre-deposit under Section 1 12(8) cannot, as of date, be remitted by directors of companies or partners of firms who are very often the persons legally competent to operate the entity’s payment instruments. The relevant functionality being unavailable or non-responsive for such category of users. This persistence of difficulty, even after the Tribunal has purportedly become operational, defeats the very object of Circular No. 224/18/2024-GST dated 11.07.2024 (referred to in para 3 above), and renders the mandatory pre-deposit condition impossible of compliance for an entire category of bona fide appellants.

|

GROUND X – Non-synchronisation of GSTN and GSTAT databases

|

The data architecture of the GSTAT portal does not synchronise with that of the GST common portal administered by GSTN, with the result that particulars already available with the Department/GSTN like registration details, order particulars, ARN/CRN data which must be manually re-fed at the GSTAT portal, leading to duplication of effort, recurrent validation failures, and avoidable consumption of time within an already truncated limitation window. This sits uneasily with the object of an integrated and seamless Common Goods and Services Tax Electronic Portal contemplated under Section 146 of the CGST Act, and is contrary to the spirit of ‘ease of compliance’ repeatedly emphasised by the GST Council, including in its 56th meeting recommendations referred to in para 2 above.

|

GROUND XI – Difficulty in uploading voluminous paper-books

|

The portal’s upload functionality is configured with restrictive file-size upto 20/50mb and format limitations, rendering it practically unworkable to upload voluminous paper-books in complex matters involving multiple years, multiple show-cause notices, detailed reconciliations and judicial precedents and documents which the GSTAT Procedure Rules, 2025 themselves contemplate being filed along with the memorandum of appeal. The resultant repeated upload failures consume disproportionate time, more acutely for practitioners situated outside metropolitan centres with constrained internet infrastructure.

|

GROUND XII – DSC registration errors despite valid, subsisting registration

|

Practitioners and taxpayers attempting to digitally sign appeals through a validly registered Class III Digital Signature Certificate are confronted with a system error stating that the DSC stands ‘not registered’, notwithstanding that the very same DSC is duly registered and has been successfully used on the portal on prior occasions. This is a verifiable, recurring technical malfunction, attributable to no default of compliance on the part of the user, and forecloses the final and mandatory step of submission of an otherwise complete appeal.

|

GROUND XIII – Multiplication of the Authorised Representative’s particulars at the ‘ Add Representative’ stage, rendering self-induction impossible

|

At the stage of ‘ Add Representative’ on the portal, the name and enrolment number of the Authorised Representative (AR) is found to be reflected thrice in the very same drop-down/selection field, as a consequence whereof the AR is rendered unable to add herself as the authorised representative for the purpose of filing. This is a significant and self-evident lapse in the design of the portal, and directly impairs the right of a taxpayer to be represented by a person of his choice before a quasi-judicial forum and such right is statutorily embedded in Section 1 16 of the CGST Act, 2017. A portal-level defect that forecloses, rather than facilitates, the exercise of this right strikes at the very root of the filing process.

|

GROUND XIV- Complaints raised at GSTAT Portal are pending for more than 3 weeks

|

It is submitted that a formal complaint in respect of the aforesaid defect was duly lodged on the GSTAT portal’s grievance mechanism as far back as 26.05.2026, and that, despite the lapse of over three weeks as on the date of this representation, no resolution or even an interim workaround has been communicated by the Tribunal’s technical team. In the absence ofredressal, the taxpayer concerned stands completely foreclosed from filing the appeal and faces the real and imminent prospect of being rendered time-barred for no fault attributable to him. It bears emphasis that the law assists those who are vigilant of their rights, not those who sleep over them, inures squarely to the taxpayer’s benefit here: the grievance was raised promptly and within the limitation window itself, and the resultant prejudice flows entirely from the Respondent’s own failure to act upon a complaint of which it stands duly seized.

|

GROUND XV – Truncated window between launch of the portal and the statutory cut-off

|

As is duly borne out from the official flyer and the minutes of the inaugural proceedings of the launch programme, the GSTAT portal with detailed procedures was formally inaugurated only on 15.06.2026, a mere fifteen days prior to the statutory cut-off of 30.06.2026. This, notwithstanding that the Tribunal stood constituted as far back as 2017 under Section 109 of the CGST Act, and that its operationalisation has been an avowed legislative object of the GST regime for over nine years. A window of fifteen days for an entirely untested digital platform to be understood and operated by lakhs of taxpayers and professionals across the country, in respect of a backlog exceeding 4.8 lakh appeals, is manifestly unreasonable. The arbitrariness inherent in such a truncated window offends Article 14 of the Constitution where arbitrariness was held to be the very antithesis of equality, and disappoints the legitimate expectation of the trade and professional fraternity to a reasonable transition period.

|

GROUND XVI – The relief already granted is confined to scrutiny and does not address the anterior difficulty of filing

|

It is a matter of record, and one squarely within the Board’s own knowledge, that the difficulties faced by taxpayers and professionals on the GSTAT portal stand already partially acknowledged, inasmuch as the lenient scrutiny dispensation, under which defects of mere form not going to the merits are not insisted upon at the threshold, has itself been extended from 30.06.2026 to 31.12.2026

|

The Association submits, with respect, that this extension, salutary as far as it goes, addresses only the scrutiny of appeals that have already been filed, and does nothing whatsoever to redress the anterior and more fundamental difficulty, namely, the inability of taxpayers to file the appeal at all within the truncated window on account of the infirmities set out in above Grounds. The grant of relief at the scrutiny stage, without corresponding relief at the filing stage, is, with respect, incongruous and self-defeating, since a taxpayer who cannot complete the act of filing derives no comfort from a relaxed scrutiny of a filing that was never made. Far from militating against the present prayer, this circumstance constitutes the strongest internal corroboration of its merit, the Board having, in substance, already conceded the existence of system-level hardship warranting administrative relaxation.

|

CUMULATIVE SUBMISSION AND THE POWER OF THE BOARD TO GRANT RELIEF

|

- Each of the grounds set out hereinabove, viewed individually or, a fort tori, cumulatively, establishes that the inability of the taxpaying and professional community to file appeals within the window ending 30.06.2026 stems not from any want of diligence on their part but from systemic and unrectified infirmities of the Respondent’s own digital infrastructure. The settled position in law is that where failure to exercise a statutory right within time is attributable to the inadequacy of the very mechanism through which that right is required to be exercised, equity leans firmly in favour of an extension of the prescribed window.

- The Association is conscious that, under Section 112(6) of the CGST Act, the Tribunal possesses a limited power to condone delay in filing for a further period not exceeding three months, and that the Hon’ble Supreme Court in Singh Enterprises v. Commissioner of Central Excise, Jamshedpur, (2008) 3 SCC 70, and Commissioner of Customs & Central Excise v. Hongo India (P) Ltd., (2009) 5 SCC 791, has held that neither a Tribunal nor a Court can enlarge a period of limitation beyond what the statute itself permits. It is precisely for this reason that the Tribunal’s condonation power is both limited in degree and, more fundamentally, premised on an appeal having first been filed that the present representation is addressed to the Board. The remedy sought is not condonation of delay in a filed appeal, but an upstream extension, by the Government on the recommendation of the Council, of the cut-off date already notified under Section 1 12( 1), exactly as was done vide the Notification dated 17.09.2025 that fixed the present 30.06.2026 date. The power once exercised to grant a staggered window remains equally available, mutatis mutandis , to extend it further where, as here, the underlying rationale continues to subsist and has, if anything, been compounded by intervening and continuing technical failure.

In view of the foregoing facts, circumstances and submissions, the Association most respectfully prays that this Hon’ble Board may be pleased to:

|

(a) recommend to the GST Council, and thereafter notify under sub-section (1) of Section 1 12 of the CGST Act, 2017, an extension of the statutory cut-off date for filing of appeals before the GST Appellate Tribunal in respect of orders communicated before 01.04.2026, from 30.06.2026 to 3 1 . 12.2026;

|

(b) pending such extension, issue appropriate administrative instructions that no coercive or recovery action under Sections 78 and 79 of the CGST Act be initiated against taxpayers who are unable to file their appeals on or before 30.06.2026 on account of the technical infirmities of the GSTAT e-filing portal set out hereinabove;

|

(c) direct a time-bound technical audit and remediation of the pre-deposit, DSC-validation, Aadhaar-authentication, document-upload and payment-gateway modules of the GSTAT portal, in consultation with GSTN and the authority administering Bharatkosh; and

|

(d) pass such other order(s)/direction(s) as this Hon’ble Board may deem fit and proper in the facts and circumstances of the case.

|

The Association shall remain grateful for the consideration extended to this representation, made bona fide in the larger interest of the trade, industry and professional fraternity, and in furtherance of the object of access to justice that animates the Goods and Services Tax Appellate Tribunal itself.

|

Yours faithfully,

For GSTAT Bar Association Delhi

|

|

|

|

|

|

|

|

Taxation Bar Association, Agra represented by General Secretary Adv. Akhilesh Bhatnagar made representation to Hon'ble Smt. Nirmala Sitharaman vide Letter dated 22.06.2026.

|

Hon'ble Smt. Nirmala Sitharaman, Union Minister of Finance, Government of India, North Block, New Delhi - 110001

|

Subject: Request for Extension of the Last Date for filing of appeals before the Goods and Services Tax Appellate Tribunal (GSTAT) beyond 30.06.2026

|

On behalf of the members of the Taxation Bar Association, I most respectfully submit this representation seeking extension of the last date for filing appeals before the Goods and Services Tax Appellate Tribunal (GSTAT), which is presently fixed as 30.06.2026.

|

At the outset, we sincerely appreciate the Government of India for establishing the GST Appellate Tribunal, which fulfills a long-awaited need under the GST regime and provides an effective statutory forum for resolution of tax disputes. However, despite the operationalization of the GSTAT, taxpayers and professionals across the country have been facing several genuine technical and practical difficulties, due to which a large number of appeals could not be filed within the prescribed time.

|

The GSTAT e-filing portal has become reasonably stable only during the last one month. Prior to that, taxpayers and professionals continuously encountered several technical glitches, making the filing of appeals extremely difficult. The statutory limitation period has thus substantially elapsed without taxpayers being able to effectively utilize the online filing facility.

|

The major practical difficulties experienced by taxpayers and professionals are as follows:

|

- Frequent failure of Aadhaar OTP authentication, resulting in repeated interruption of the filing process.

- Digital Signature Certificate (DSC) related issues, including failure in DSC registration, validation, signing and successful submission of appeals.

- Frequent portal login failures, session expiry, server errors and unexpected technical interruptions, compelling taxpayers to restart the entire filing process repeartedly.

- Difficulties in uploading appeal documents, annexures and supporting records due to file validation errors and portal restrictions.

- Since the GSTAT portal remained unstable for a considerable period after its launch, taxpayers and tax professionals could not effectively utilize the statutory period available for filing appeals.

- A substantial number of appeals pertain to old adjudication and appellate orders passed over the last several years. Preparation of such appeals requires collection of assessment records, certified copies, show cause notices, replies, evidence and other supporting documents, which is a time-consuming exercise.

- Since GSTAT is a newly constituted appellate forum, taxpayers as well as professionals also required sufficient time to understand the new filing procedure, portal requirements and technical compliances.

- Limited availability of GSTAT Benches has also created serious practical difficulties. At present, there is one Principal Bench at New Delhi and only 31 State Benches for the entire country. In the State of Uttar Pradesh, only three State Benches have been notified at Lucknow, Ghaziabad and Varanasi, while Agra and Prayagraj have been notified as Circuit Benches. Consequently, taxpayers residing in cities where no regular Bench is available are compelled to identify and engage advocates practicing at the concerned Bench location. Considerable time is consumed in identifying competent counsel, coordinating documents, executing authorizations, finalizing pleadings and completing the filing process. These practical difficulties have significantly affected the timely filing of appeals.

- Many taxpayers belong to small towns and rural areas, where obtaining old records, coordinating with professionals and completing procedural formalities requires additional time and effort.

It is respectfully submitted that the right of appeal is a valuable statutory right and an essential component of the principles of natural justice. Genuine taxpayers should not be deprived of this valuable right merely because of technical and procedural difficulties beyond their control.

|

It is further submitted that extension of the limitation period would not cause any loss of revenue to the Government, whereas refusal to grant such extension may compel thousands of taxpayers to approach the Hon'ble High Courts seeking condonation of delay or appropriate relief, thereby resulting in avoidable litigation and unnecessary burden upon the judiciary as well as the Government.

|

In view of the above facts and circumstances, we most humble request your kind intervention to extend the last date of filing appeals before the Goods and Services Tax Appellate Tribunal from 30.06.2026 to at least 30.12.2026, or for such further period as the Central Government may deed fit in the interest of justice.

|

Such an extension would uphold the principles of fairness, natural justice and ease of doing business, while ensuring that no genuine taxpayer loses the valuable statutory right of appeal due to reasons beyond his control.

|

We are confident that your goodself, who has always been committed to promoting a taxpayer-friendly and transparent tax administration, will kindly consider this genuine request sympathetically in the larger interest of justice.

|

We shall remain ever grateful for your kind consideration.

|

(Adv. Akhilesh Bhatnagar)

|

Taxation Bar Association, Agra

|

- The Hon'ble Minister of State for Finance : Ministry of Finance, Government of India, New Delhi

- The Revenue Secretary: Ministry of Finance, Government of India, North Block, New Delhi.

- The Chairman: Central Board of Indirect Taxes & Customs (CBIC), North Block, New Delhi.

- The President: Goods and Services Tax Appellate Tribunal (GSTAT), New Delhi.

- The Secretary: GST Council Secretariat, New Delhi

- The Pre Commissioner, CGST & Central Excise, Agra Zone

|

|

|

|

|

|

|

Advocates' Tax Bar Association address representation to Hon’ble Smt. Nirmala Sitharaman seeking extension of the last date for filing appeals before GSTAT.

|

I have the honour to submit this representation on behalf of the Advocates Tax Bar Association, New Delhi, a national association of Advocates engaged in the practice of Direct and Indirect Taxation Laws before the Hon’ble Supreme Court of India, various High Courts, Appellate Tribunals and tax adjudicatory forums throughout the country.

|

The Association represents the collective concerns of tax practitioners and, through them, lakhs of taxpayers who depend upon the fair and efficient functioning of the tax administration and appellate system established under the Goods and Services Tax laws.

|

At the outset, we place on record our sincere appreciation for the Government’s efforts in operationalising the Goods and Services Tax Appellate Tribunal, thereby restoring the long-awaited statutory appellate remedy envisaged under Section 112 of the Central Goods and Services Tax Act, 2017.

|

However, despite the commencement of the Tribunal and the launch of the electronic filing platform, significant practical and technical difficulties continue to impede the effective filing of appeals before GSTAT, resulting in serious hardship to taxpayers across the country.

|

GSTAT: A Long Awaited Forum for Justice

|

The GST Appellate Tribunal occupies a central position in the architecture of GST dispute resolution. Since the introduction of GST in July 2017, taxpayers have waited nearly nine years for the availability of an effective second appellate forum.

|

During this prolonged period, disputes involving substantial revenue and significant legal issues remained pending without access to the statutory remedy specifically contemplated by Parliament.

|

Consequently, an enormous backlog of matters has accumulated across the country. The opening of the Tribunal therefore marks not merely the commencement of another forumbut the revival of an important statutory safeguard intended to ensure fairness anduniformity in GST administration Continuing Technical Difficulties on the GSTAT Portal

|

While the launch of the GSTAT portal is a welcome development, the practical experience of taxpayers and Advocates indicates that the system is still undergoing stabilisation.

|

Members of our Association from various States have reported recurring issues including:

|

- Repeated failures in Aadhaar authentication and registration processes;

- Difficulties in payment of court fees and mandatory pre-deposits;

- Delays in payment confirmation despite successful bank debits;

- Errors relating to Digital Signature Certificates;

- Restrictions in uploading voluminous records and paper books;

- Validation failures and system-generated errors;

- Non-synchronisation of GSTN data with GSTAT records;

- Difficulties in registration and authorisation of representatives;

- Delayed resolution of grievances raised through the portal support mechanism.

These difficulties are not attributable to taxpayers or their legal representatives. They arise from the technological infrastructure supporting the filing process and are therefore beyond the control of litigants seeking to avail their statutory remedy.

|

Statutory Right of Appeal Cannot Be Lost Due to Technological Limitations

|

The right of appeal conferred under Section 112 of the CGST Act constitutes an essential component of the GST dispute resolution framework.

|