onlinetaxupdate team wish to express sincere thanks to all the readers, authors, subscribers for the support extended to us.

|

Newsletter 112 dated 23.02.2024

|

|

|

|

|

|

|

|

|

Dear Reader,

|

Please find newsletter for your reading and reference.

|

|

Index of the Newsletter

- Recent updates

- GST Portal

- Lawgics by Ms.Nidhi Aggarwal

- GST Notes by CMA Anil Sharma

- GST/IT in media

- Press Release

|

|

|

|

|

|

|

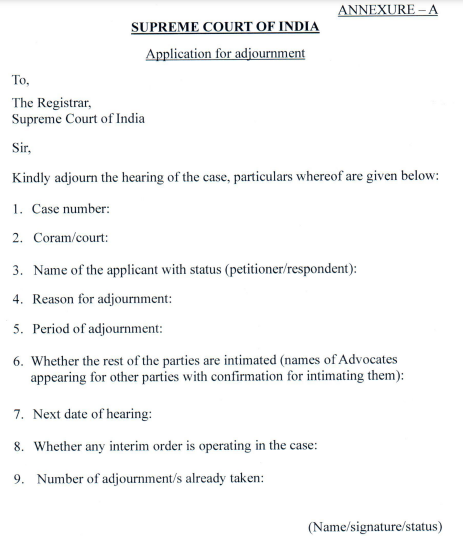

The Hon'ble Supreme Court issued Circular F. No. 4 /Judl./2024 dated 14th February, 2024 laying down the procedure/modalities relating to circulation of Letters for adjournment of cases.

|

F. No. 4 /Judl./2024

14th February, 2024

|

The following will be the procedure/modalities relating to circulation of Letters for adjournment of cases:

|

1) Procedure in after-notice miscellaneous matters:

|

a) No letters for adjournment shall be entertained in cases:

|

i) relating to bail/anticipatory bail;

|

ii) where exemption from surrendering has been granted;

|

iii) where interim order is operating in favour of the party who seeks adjournment; and

|

iv) where suspension of sentence has been sought for.

|

b) In other matters, letters for adjournment can be circulated till one day prior to publication of main list.

|

3) Specific reason for seeking adjournment and number of adjournments already sought shall be mentioned.

|

4) It is mandatory to obtain consent/no objection of advocates/parties appearing on the other side / Caveator before circulating the letter for adjournment.

|

5) Letters can be circulated by one party/counsel to the case only once.

|

6) Two consecutive adjournments, irrespective of which party is seeking an adjournment, shall not be permitted without the matter being listed before the Court.

|

7) Matters so adjourned will be listed before the Court within an outer limit of four weeks with a specific date of listing and no mentioning for seeking preponement of the date in such matters is permitted.

|

8) Letter(s) seeking adjournment shall be placed before the competent authority. If such request(s) is/are considered favourably, the list of matters not listed as per schedule will be notified on the website of this Court.

|

9) Circulating letters for adjournment in fresh and regular hearing matters is not permitted.

|

|

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Notification no. 02/2026 – Central Tax dated 07.05.2026.

|

GOVERNMENT OF INDIA

MINISTRY OF FINANCE

DEPARTMENT OF REVENUE

|

Notification No. 02/2026 – Central Tax dated 07.05.2026

|

S.O. 2286(E).— In exercise of the powers conferred by sub-section (1A) of section 101A of the Central Goods and Services Tax Act, 2017 (12 of 2017) (hereinafter referred to as the said Act), the Central Government, on the recommendations of the Council, hereby empowers the Principal Bench of the Appellate Tribunal, New Delhi constituted under sub-section (3) of section 109 of the said Act, to hear appeals made under section 101B of the said Act.

|

This notification shall be deemed to have come into force on the 1st day of April, 2026.

|

BALASUBRAMANIAN KRISHNAMURTHY,

Joint Secretary

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Corrigendum on 12.06.2026 to Notification no. 45/2025 -Customs dated 24.10.2025 -

|

G.S.R…(E).- In the notification of the Government of India, Ministry of Finance (Department of Revenue) No. 45/2025-Customs, dated the 24th October, 2025, published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i), vide number G.S.R. 781(E), dated the 24th October, 2025, at page 291, in lines 12 and 14, for ‘1993’ read ‘1983’.

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Instruction no. 11/2026-Customs dated 23.06.2026 regarding Establishment of Green Channel for Customs Clearance of Pollution Response Equipment and Materials during Oil and Hazardous and Noxious Substances (HNS) Spill Emergencies

|

|

|

|

|

|

Export consignments to West Asia will continue to receive enhanced insurance cover against payment defaults until September 30, the Directorate General of Foreign Trade (DGFT) said in a notification on Monday.

|

Earlier, the enhanced cover for exporters taking credit risk insurance from Export Credit Guarantee Corporation (ECGC) was available for shipments to West Asia sent between March 16 and June 15.

|

The enhanced risk cover announced on March 19 was part of the Resilience and Logistics Intervention for Export Facilitation (RELIEF) scheme under the Export Promotion Mission (EPM) to support exports to West Asia in view of the Iran war.

|

"The eligibility timelines under Component II of the EPM RELIEF intervention are extended up to September 30, 2026 to support Indian exporters and mitigate logistics challenges arising out of the continuing West Asia Crisis," the DGFT said.

|

Source: The Economic Times

|

|

|

|

|

|

|

|

Directorate General of Foreign Trade (DGFT) issued Public Notice No. 17/2026-27 dated 04.06.2026 regarding Enlistment under Appendix 2E of FTP, 2023-Agency Authorised to issue Certificate of Origin (Non-Preferential)

|

|

|

|

|

|

|

|

Directorate General of Foreign Trade (DGFT) issued Trade Notice 07/2026-27 dated 03.06.2026 regarding request for comments on alignment of Schedule-II (Export Policy) of ITC (HS), 2022 consequent to amendments introduced under the Finance Act, 2026

|

|

|

|

|

|

|

|

Directorate General of Foreign Trade (DGFT) issued Notification No. 20/2026-27 dated 02.06.2026 regarding Applicability of Quality Control Orders (QCOs)/ BIS requirements on imports by Special Economic Zone (SEZ) Units and Developers - Amendment in Para 2.03(A)(iii) of FTP 2023

|

|

|

|

|

|

CBIC issued clarification via F. No. CBIC-20016/75/2025-GST dated 25.09.2025 on requirement of separate GST registration for importers storing goods in Warehouses in other States

|

|

|

|

|

|

|

|

Department of Trade and Taxes, New Delhi issued Circular No. F.IV/42/T&T/Admn./Misc./2025/8464-67 date 23.07.2025

|

Several instances have come to the notice of the Competent Authority that GSTIs/ Field Functionaries to whom the physical verification visit of 'High Risk Score' Registration Application are marked, are not submitting the verification reports on time and in some cases the report is submitted with remarks that the address mentioned in the ARN is not in their jurisdiction.

|

The Competent Authority has taken a serious note of the aforementioned conduct of officials and directed that it is imperative upon the GSTI to whom the visit is marked, to conduct the visit and submit the report timely.

|

Any dereliction shall be viewed adversely and invite strict action as per rules.

|

|

|

|

|

|

|

|

Directorate General of Goods & Services Tax (DGGST), South Zone, Chennai, is conducting a nationwide study on demand notices and adjudication orders to strengthen the working regime and promote a more trader-friendly ecosystem. The objective is to identify procedural gaps, understand root causes, and recommend reforms to enhance fairness, consistency, and administrative efficiency in adjudication.

|

This initiative is also aligned with the broader goal of improving the Ease of Doing Business, by ensuring that tax administration practices are transparent, predictable, and minimally intrusive for taxpayers.

|

As part of this study, a virtual interactive session has been scheduled with your association and members on 23.07.2025 (Wednesday) at 3:0 PM. The objective of the session is to solicit feedback and practical suggestions from trade and industry stakeholders, based on your experience with Show Cause Notices (SCNs), personal hearings, and adjudication orders.

|

You are requested to kindly:

|

- Share the names and contact details of participants from your association who will join the meeting;

- Come prepared with inputs highlighting specific concerns or patterns observed in SCNs and adjudication orders.

- Supplement the discussion, if possible, with case examples or material that could add depth and value to the deliberations.

The link for the virtual meeting will be shared with the confirmed participants in due course. We look forward to your valuable contribution to this important initiative.

|

|

|

|

|

|

The Central Board of Indirect Taxes vide F. No.225/56/2026/ITA-II dated 04.06.2026 issued Guidelines for Compulsory Selection of returns for Complete Scrutiny during the financial year 2026-27 - procedure for compulsory selection in such cases.

|

The Guidelines for Compulsory Selection of returns filed during the financial year 2025-26 under the Income-tax, Act 1961 are hereby issued in pursuance of Section 536(2)(c) of the Income-tax Act, 2025. The parameters for compulsory selection of returns for complete scrutiny during Financial Year 2026-27 and procedure for compulsory selection in such cases are prescribed as under:

|

3. For Assessing Officers in International Taxation and Central charges: Cases may be selected for compulsory scrutiny by the International Taxation and Central Charges following the above prescribed parameters at Para 2 with prior administrative approval of Pr.CIT/Pr.DIT/CIT/DIT concerned and these selected cases shall continue to be handled by International Taxation and Central Circle charges respectively, as earlier. It is further clarified that communication to NaFAC for access and /or further action after selection for Compulsory Scrutiny will not apply to the International Taxation and Central charges.

|

4. Time limit: As per the proviso to section 143(2) of the Income tax Act, 1961 and in terms of section 536(2)(c) of the Income-tax Act, 2025, the time limit for service of notice u/s 143(2) of the Income-tax Act, 1961 for the ITRs filed in the Financial Year (FY) 2025-26 is 30.06.2026.

|

5. These instructions may be brought to the notice of all concerned for necessary compliance.

|

|

|

|

|

|

Department of Consumer Affairs, Weights and Measures Unit, issued circular on 18.09.2025 vide no.I-10/14/2020-W&M to relax provisions contained in Rule 18(3).

|

Pursuant to advisory dated 09.09.2025 on the above subject, the Central Govt., has received representation from industry & trade associations about the need for simplifying the procedure for legal compliance by manufactures and importers of pre-packaged commodity in the wake of GST revision.

|

2. After considering the concerns of the industry and in supersession of earlier advisory dated 09.09.2025, the Central Government, has decided to allow such manufacturers/ packers/ importers / their representatives who may like to voluntarily affix additional revised price sticker, on unsold packages manufactured before 22nd September, 2025 and are lying with them, provided the original price declaration on the package is not obstructed. In this context, it is underlined that extant Rules do not mandate affixing revised price sticker by manufacturer/ packer/ importer/ their representatives on unsold packages manufactured before 22nd September, 2025 and are lying with them.

|

3. Apart from above, by virtue of powers vested under Rule 33 of the Legal Metrology (Packaged Commodities) Rules, 2011, the Central Government, has decided to waiver off the requirement in Rule 18(3) to issue Advertisement, about revised prices in two newspapers by manufacturers and importers.

|

4. Consequently, the manufacturer/ packers/ importers are now required to send only circulars to wholesale dealers/ retailers, etc. about revised prices with copy thereof endorsed to Director, Legal Metrology of the Central Government and Controller, Legal Metrology of All States/ UTs and to ensure price compliance at the retailer level.

|

5. However, the manufactures/ packers/ importers shall take immediate measures to sensitise dealers /retailers/ consumers about revision in GST rates through all possible channels of communication including electronic, print and social medial.

|

6. It is also clarified that any packaging material or wrapper which could not be exhausted by the manufacturer or packer or importer prior to revision of GST, may be used for packing of material upto 31st March, 2026 or till such date the packing material or wrapper is exhausted, whichever is earlier, after making corrections required in retail sale price (MRP) on account of implementation of GST by way of stamping or putting sticker or online printing as the case may be, at any place on the package.

|

7. Further to Para-6 above, it is informed that the declaration of the revised unit sale price on unsold pre-packaged commodities/ unused packaging material or wrapper bearing a pre-printed MRP is not mandatory. However, manufacturers/ packers/ importers / their representatives may declare the revised unit sale price voluntarily, if they so desire.

|

|

|

|

|

|

|

|

|

GSTN is taking downtime to enhance its services on the GST Portal on 27.06.2026 from 12:00 AM onwards until 2:30 am of 27.06.2026.

|

|

|

|

|

|

|

|

|

|

|

GSTN is taking downtime to enhance its services on the GST Portal on 12.06.2026 from 11:30 AM onwards until 7:30 am of 13.06.2026. We shall be enhancing services on the GST portal on : 12th June’26 11:30 PM onwards. GST Portal services will not be available until 13th June’26 07:30 AM. The inconvenience caused is regretted.

|

|

|

|

|

|

|

|

3. Lawgics by Ms.Nidhi Aggarwal

|

|

Ms. Nidhi Aggarwal is delighted to present judgment with a great vision to spread complex GST law in a simple manner amongst the taxpayers, tax professionals, students and knowledge seeker.

|

|

|

|

|

|

|

|

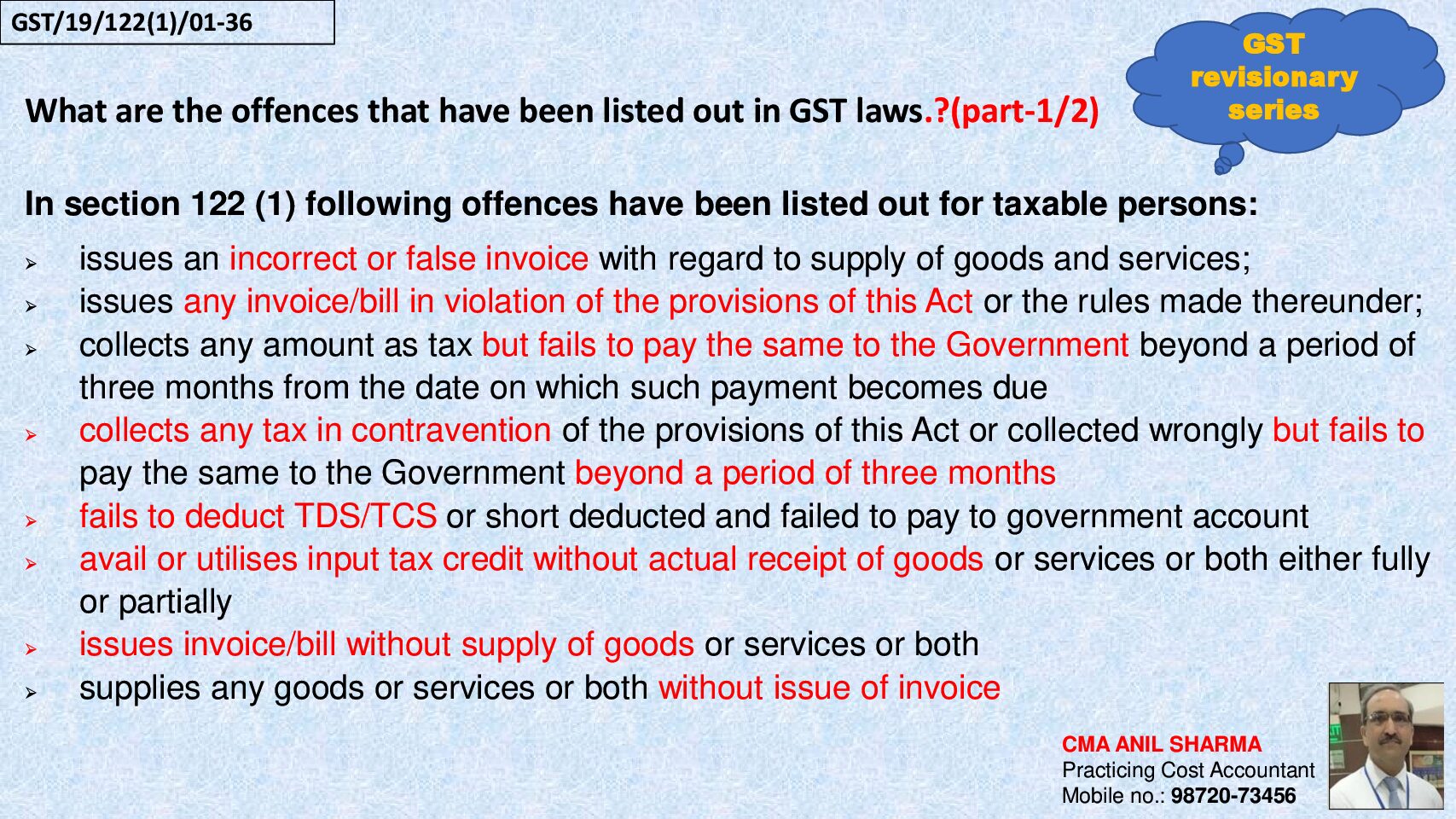

4. GST Notes by CMA Anil Sharma

1) Shri CMA Anil Sharma, Shri CMA Gurdev Singh Saini and Smt. CMA Bhawna Sharma posted Chapter-19 recently containing CGST Act in simple language in PPT format. This is to make dealers, professionals, academicians, students etc. understand the basics of GST laws.

|

Chapter-19th slide is given below.

|

|

|

|

|

|

|

|

|

5. GST/Income Tax in Media

|

|

|

|

|

|

|

|

|

|

|

|

|

Press release ID 2278205 dated 26.06.26

|

|

In a major crackdown against smuggling of foreign origin gold, the the Directorate of Revenue Intelligence (DRI) has successfully unearthed and dismantled a highly organised gold smuggling syndicate operating through Mumbai Airport. In this operation DRI detected and busted gold melting facility that was being used for melting of foreign origin smuggled gold.

|

|

|

Seized gold from melting facility in Mumbai

|

A total of nine persons involved across the entire smuggling chain, including the airport staff, her handler, three intermediaries, the melting facility operator, and three persons engaged in the melting process have been arrested. Further, about 6 kg foreign-origin smuggled gold recovered at the spot has been seized.

|

|

This case underscores the evolving sophistication of organised gold smuggling syndicates, which increasingly exploit insider access at airports and employ layered distribution networks to evade detection. In another operation at Bengaluru, DRI seized 1.8 kg 24 KT gold in paste form ingeniously concealed within the layers of garments of an international passenger. Subsequent follow up search at his residential premises led to seizure of around 1.5 kg gold jewellery, 45 kg silver, and Indian & foreign currencies. The person was arrested.

|

|

|

Gold in paste form concealed in undergarments; Seized at Bengaluru

|

|

earlier in this week, DRI has conducted a series of operations at other airports, railways station and land customs stations at Hyderabad, Rajkot, Calicut, Vishakhapatnam, Calicut, Guwahati and Petrapole, leading to the cumulative seizure of another 6 kg foreign-origin smuggled gold. Five persons have been arrested in these operations.

|

|

|

Overall, with busting of gold smuggling syndicate, these operations resulted in seizure of about 15 kg gold, 45 kg silver, valued at around Rs. 23 crore, and arrest of 15 persons.

|

|

|

|

|

|

|

|

The Central Board of Indirect Taxes and Customs (CBIC) organised an interactive session with representatives of Trade Associations, Chambers of Commerce, Exporters, Importers, Custodians, Customs Brokers, Logistics Service Providers, at New Custom House, Mumbai.

|

The event was presided over by Shri Vivek Chaturvedi, Chairman, CBIC; and Shri Yogendra Garg, Member (IT, Taxpayer Services & Technology), CBIC. Pr. Chief Commissioners of Mumbai Customs and GST, Joint Secretary (Customs), Commissioner (Customs & Export Promotion) and Commissioner, GST Policy Wing were also present along with other senior officers of the Department.

|

In his address, Shri Chaturvedi elaborated how the newly-introduced reforms, which emphasise trust-based governance in Indirect Taxes, announced in the Union Budget 2026–27, will contribute to the vision of the Government. He clarified the intricacies of the Budgetary policy changes and explained how the Customs is working towards simplification of Customs processes.

|

In his address, Shri Garg highlighted the benefits of a single integrated digital ecosystem connecting all export-import stakeholders, including other participating government agencies, to enable faster clearances, better business planning and strengthen Make in India.

|

Joint Secretary (Customs) informed that for public facilitation and for ease of understanding these initiatives, FAQs have been released by CBIC and are posted on the official website at https://www.cbic.gov.in.

|

The interaction with stakeholders was aimed at addressing the doubts of trade and industry and was followed by an interaction with media persons.

|

Shri Chaturvedi also held an interaction with the officers and staff working at the cutting edge level in Mumbai Customs, Airport, Courier Terminal and CGST to sensitise them regarding efficient implementation of reform initiatives and to enhance the ease of doing business for the trade and industry.

|

|

|

|

|

|

|

|

Press release ID 2227804 dated 13.02.2026

|

As part of its ongoing enforcement drive against fraudulent ITC claims, the Anti-Evasion Branch of the Central Goods & Services Tax (CGST), Delhi South Commissionerate, has unearthed another significant case of tax evasion and has arrested a Director of a private limited company engaged in trading of electronic goods for fraudulent availment of Input Tax Credit (ITC) amounting to ₹6.53 crore through bogus invoices of ₹36.28 crore.

|

Investigation revealed that the company had availed inadmissible ITC on the basis of invoices issued by multiple firms, some of which were found to be non-existent, non-functional, or having suspended/cancelled GST registrations. Field verification conducted by jurisdictional authorities confirmed that certain suppliers were bogus entities with no genuine business activity at their declared places of business.

|

Further inquiry established that the ITC was availed without actual receipt of goods and was utilized for discharge of GST liability, in contravention of the provisions of the Central Goods and Services Tax Act, 2017.

|

Based on the evidence gathered during investigation and statements recorded, the accused was arrested under Section 69 of the CGST Act, 2017 and produced before the Duty Magistrate and has been remanded to judicial custody for 14 days.

|

Further the investigation is ongoing to trace the flow of funds and identify any additional beneficiaries.

|

|

|

|

|

|

|

Hope the above updates is of use to you. Please share your input and feedback at taxupdate.otu@gmail.com

|

|

|

|

|

|

|

|

|

Visit our website

|

OTU provides you

|

- Articles on various topics

|

|

- Media - GST, Income Tax & Press R.

|

|

- Notes / Newsletter at 149/ p.a.

|

|

|

|

|