|

|

|

|

|

|

|

|

This website contains information about recent changes mainly in GST laws. It also contains Articles on various topic in GST. Please visit the website and read more.

|

|

|

|

Dear Reader,

|

Please find newsletter for your reading and reference.

|

|

Newsletter no.96 dated 07.08.2023

|

|

|

Index of the Newsletter

- Recent updates

- GST in media

- Articles

- Lawgics by Ms.Nidhi Aggarwal

- GST notes by CMA Anil Sharma

|

|

|

|

|

|

|

CBIC issued clarification via F. No. CBIC-20016/75/2025-GST dated 25.09.2025 on requirement of separate GST registration for importers storing goods in Warehouses in other States

|

|

|

|

|

|

|

|

Department of Trade and Taxes, New Delhi issued Circular No. F.IV/42/T&T/Admn./Misc./2025/8464-67 date 23.07.2025

|

Several instances have come to the notice of the Competent Authority that GSTIs/ Field Functionaries to whom the physical verification visit of 'High Risk Score' Registration Application are marked, are not submitting the verification reports on time and in some cases the report is submitted with remarks that the address mentioned in the ARN is not in their jurisdiction.

|

The Competent Authority has taken a serious note of the aforementioned conduct of officials and directed that it is imperative upon the GSTI to whom the visit is marked, to conduct the visit and submit the report timely.

|

Any dereliction shall be viewed adversely and invite strict action as per rules.

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Circular no. 255/01/2026-GST dated 25.06.2026 to provide Clarification regarding jurisdiction in cases involving migration/ transfer of taxable persons from one jurisdiction to another jurisdiction.

|

|

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Circular no. 254/11/2025-GST dated 27.10.2025 regarding Assigning proper officer under section 74A, section 75(2) and section 122 of the Central Goods and Services Tax Act, 2017

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Notification no. 02/2026 – Central Tax dated 07.05.2026.

|

GOVERNMENT OF INDIA

MINISTRY OF FINANCE

DEPARTMENT OF REVENUE

|

Notification No. 02/2026 – Central Tax dated 07.05.2026

|

S.O. 2286(E).— In exercise of the powers conferred by sub-section (1A) of section 101A of the Central Goods and Services Tax Act, 2017 (12 of 2017) (hereinafter referred to as the said Act), the Central Government, on the recommendations of the Council, hereby empowers the Principal Bench of the Appellate Tribunal, New Delhi constituted under sub-section (3) of section 109 of the said Act, to hear appeals made under section 101B of the said Act.

|

This notification shall be deemed to have come into force on the 1st day of April, 2026.

|

BALASUBRAMANIAN KRISHNAMURTHY,

Joint Secretary

|

|

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Notification no. 01/2026 – Central Tax dated 21.04.2026 that Seeks to extends the due date for furnishing the return in FORM GSTR-3B for the month of March, 2026 till the twenty-first day of April, 2026.

|

GOVERNMENT OF INDIA

MINISTRY OF FINANCE

DEPARTMENT OF REVENUE

CENTRAL BOARD OF INDIRECT TAXES AND CUSTOMS

Notification No. 01 /2026 Central Tax dated 21.04.2026

|

G.S.R (E)… ( In exercise of the powers conferred by sub section (6) of section 39 of the Central Goods and Services Tax Act, 2017 (12 of 2017), the Commissioner, on the recommendations of the GST Council, hereby extends the due date for furnishing the return in FORM GSTR 3B for the month of March, 2026 till the twenty first day of April, 2026, for the registered persons who are required to furnish return under sub section (1) of section 39 read with clause (i) of sub rule (1) of rule 61 of the Central Goods and Services Tax Rules, 2017.

|

2. This notification shall come into effect from 20th day of April, 2026.

|

(Kangale Shrunkhala Motiram)

Director

|

|

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Notification no. 20/2025 – Central Tax dated 31.12.2025 which Seeks to notify Central Goods and Services Tax (Fifth Amendment) Rules, 2025

|

1. These rules may be called as the Central Goods and Services Tax (Fifth Amendment) Rules, 2025. They shall come into force from 1st day of February, 2026.

|

2. In the Central Goods and Services Tax Rules, 2017 (hereinafter referred to as the said rules), after rule 31C, the following rule shall be inserted, namely: —

|

"31D. Value of supply of goods on basis of retail sale price. -(1) Notwithstanding anything contained in the provisions of this Chapter, the value of supply of goods bearing the description specified in column (3), falling under the corresponding Chapter/ heading/ sub-heading/ tariff item specified in column (2), of the Table below, shall be deemed to be the retail sale price declared on such goods, less the amount of tax as applicable, namely: -

|

(2) The amount of applicable tax referred to in sub-rule (1) shall be determined in the following manner, namely: —

|

Tax amount = (Retail sale price X tax rate in % of applicable taxes) / (100+ sum of applicable tax rate).

|

Explanation. — For the purposes of this rule, —

|

(a) “applicable tax” means IGST or CGST or SGST or UTGST as the case may be.

|

(b) "retail sale price" means the maximum price declared on goods at which such goods in packaged

form may be sold to the ultimate consumer and includes all taxes, duties, surcharge or cess by

whatever name called;

|

(c) where on the package of any specified goods more than one retail sale price is declared, the

maximum of such retail sale price shall be deemed to be the retail sale price;

|

(d) where the retail sale price declared on packages of any specified goods is altered to increase the

retail sale price at any stage before, during, or after the supply, such altered retail sale price shall be

deemed to be the retail sale price;

|

(e) where different retail sale prices are declared on different packages for the sale of any specified

goods above in packaged form in different areas, each such retail sale price shall be the retail sale

price for the purposes of valuation of the specified goods intended to be sold in the area to which

the retail sale price relates.".

|

3. In the said rules, in rule 86B, in the first proviso, after clause (e), the following clause shall be inserted, namely: —

|

"(f) the registered person other than a manufacturer shall be exempted from the provisions of this rule only in respect of goods specified under rule 31D, on which the tax has been paid by the supplier on the basis of retail sale price:".

|

Note: The principal rules were published in the Gazette of India, Extraordinary, Part II, Section 3, Sub section (i) vide notification No. 3/2017-Central Tax, dated the 19th June, 2017, published vide number G.S.R. 610(E), dated the 19th June, 2017 and were last amended, vide notification No. 18/2025– Central Tax, dated the 31st October, 2025, vide number G.S.R. 805(E), dated the 31st October, 2025

|

|

|

|

|

|

|

|

Central Board of Indirect Taxes and Customs (CBIC) issued Notification no. 19/2025 – Central Tax dated 31.12.2025 which Seeks to notify supplies under section 15(5) of CGST Act for valuation based on Retail sale price (RSP)

|

|

|

|

|

|

Kolkata is likely to host the 57th meeting of the GST Council next month, sources said, although the Union Finance Ministry has not yet officially confirmed the venue or the schedule. The meeting is expected to be held in the second half of July, and could take up the next round of indirect tax policy reforms.

|

Hosting the meeting in Kolkata holds significance as it would mark one of the first major meetings of a Constitutional federal body in West Bengal after the Assembly elections. While the GST Council independently decides its agenda and meeting schedule, the choice of Kolkata would coincide with the Centre’s broader emphasis on strengthening the State’s profile as a destination for investment and financial activity following the change in government.

|

New reforms

The previous GST Council meeting, held on September 3, 2025, came after a gap of nearly nine months, despite the rules providing for at least one meeting every quarter. That meeting unveiled GST 2.0, including rate rationalisation and measures to ease compliance. Tax experts now expect the council to consider another set of policy reforms, some of which were discussed during 4th Annual Seminar on Direct and Indirect Taxes of the Bengal Chamber of Commerce & Industry (BCCI).

|

Vivek Jalan, Chairperson of the National Fiscal Affairs and Taxation Committee of BCCI, said that in the spirit of GST 2.0, which was launched to strengthen India’s manufacturing base, the council should correct the anomaly of non‑refund of Input Service ITC under the inverted duty structure. While GST 2.0’s rate rationalisation has supported consumption, the cost pressures has deepened on manufacturers. “Addressing this gap will ensure reducing cascading taxes, boosting competitiveness and advancing India’s vision of becoming the world’s third‑largest economy by 2047,” he said.

|

Also, it has been proposed before the GST Council to consider reducing the GST rate on autism care centres and allied sectors from 18 per cent to 5 per cent. Such a measure under GST would ease the financial strain on families and institutions, while reinforcing the government’s vision of inclusive growth. “By aligning tax policy with compassion, the council can ensure that essential services for differently‑abled children remain affordable, accessible and sustainable, a step that truly reflects the spirit of GST reforms,” said Jalan.

|

Source: The Hindu businesline

|

|

|

|

|

|

Press release ID 2279424 dated 30.06.26

|

The Government had earlier provided a full Customs Duty exemption on imports of critical petrochemical products till 30th June 2026, as a temporary and targeted relief in view of the conflict in West Asia and the consequent disruptions in global supply chains.

|

The exemption was provided to ensure sufficient availability of petrochemicals in the domestic market as Indian petroleum companies had been asked to concentrate on the production of LPG during this period. As the situation is gradually normalizing, to ensure a smooth and non-disruptive transition for the affected sectors, it has been decided to extend the said exemption by a further period of 15 days, that is, till 15th July 2026.The list of products covered remains the same as notified earlier.

|

The Government remains committed to supporting India's manufacturing sector. As before, the exemption is expected to benefit a wide range of sectors dependent on petrochemical feedstock and intermediates, including plastics, packaging, textiles, pharmaceuticals, chemicals, automotive components and other manufacturing segments. This will also provide relief to consumers of final products.

|

Link to previous press note issued:

|

|

|

|

|

|

|

|

Press release ID 2279409 dated 30.06.2026

|

|

In a major operation the officers of the Directorate of Revenue Intelligence (DRI) successfully dismantled a trans-border gold smuggling syndicate and seized 15 kg foreign-origin smuggled gold, valued at approximately Rs. 21.40 crore, operating from Delhi.

|

|

|

DRI officers intercepted an international courier consignment originating from Thailand at Courier Terminal, Delhi. The consignment was in the name of a firm linked to a foreign national.

|

A meticulous examination of the consignment declared as "worn gear", led to the recovery of eight disc-shaped pieces of foreign-origin gold, each weighing 1.5 kg, ingeniously concealed inside gear parts. In total, 12 kg smuggled foreign-origin gold was recovered from the courier consignment.

|

Simultaneous searches conducted at the residence of the intended recipient and the alleged mastermind resulted in the recovery of two more identical disc-shaped pieces of foreign-origin gold, each weighing 1.5 kg.

|

Four persons, including the mastermind, who is a repeat offender, and a foreign national have been arrested in relation with the case.

|

Preliminary investigations also reveal that crypto-currency was being used to transfer the money across borders to finance the smuggling.

|

|

|

|

|

|

2. GST in Media - Council meeting

|

|

|

|

|

Now that the income tax return filing time is here you can start the process by first preparing your tax return information and data. To submit your income tax return (ITR), you will need to use the e-filing ITR portal or the income tax utility. If you are trading in securities and futures and options (F&O) in the stock market, it's important to pay attention to the tax audit requirements.

|

This article explains when stock market traders should conduct a tax audit and then file their ITR.

|

Stock market trading income classification

Taxmann research says that typically intraday trading in the stock market, along with future and option trading, is considered income from speculative business unless you are a registered business that solely engages in stock market trading. If you are a registered business focused only on stock market trading, you will report this income as business income.

|

This article is about those individuals who do not own any registered business, but are simply trading in the stock market, such as students and salaried Employees.

|

According to Taxmann Research, any gains or losses from intra-day trading, classified as speculative transactions, are always subject to taxation under the income category: 'Profits and Gains from Business or Profession'.

|

'Speculative transaction' means a transaction in which a contract for purchase or sale of any commodity including stock and shares is periodically or ultimately settled otherwise than through actual delivery or transfer of the commodity or scrips.

|

The Income-tax Act classifies the business income into 'speculative' and 'non-speculative' categories. There are no separate provisions for computation and taxability of income from speculative business except for the provisions relating to set-off and carry forward of losses.

|

Taxmann Research says the income from speculative business is computed in the same way as normal business and taxed at rates applicable to the individual taxpayer.

|

However, any loss arising from speculative business is not allowed to be set off from any other income including income from non-speculative business. In other words, loss from speculative transactions can be set-off only against income from speculative transactions.

|

Applicability of tax audit for stock market traders

According to Taxmann Research, for checking the applicability of tax audit in such cases, the turnover from intra-day trading first has to be computed.

|

The computation of turnover is a very important factor as the applicability of tax audit is determined on the basis of turnover. In cases where total sales, turnover or gross receipt from the business during the previous year exceed Rs 1 crore, a tax audit is required.

|

However, the raised threshold limit of Rs 10 crore shall be applicable if cash receipts and cash payments during the year do not exceed 5% of the total receipt or payment, as the case may be.

|

In other words, if more than 95% of business transactions are done through banking channels, then tax audit is required only when the turnover exceeds Rs 10 crore.

|

Taxmann Research points out that as intra-day trading in shares is done through banking channels, the tax audit in such cases shall generally be required only when the turnover exceeds Rs 10 crore.

|

Computation of turnover

According to Taxmann Research, the Income-tax Act does not contain any provision or guidance for computation of turnover in the case of intra-day trading. However, the Guidance Note on Tax Audit issued by the ICAI prescribes the method of determining turnover in case of speculative transactions.

|

A speculative transaction refers to a transaction in which a contract for purchase or sale of any commodity or securities, is periodically or ultimately settled otherwise than by actual delivery or transfer of commodity or scrips.

|

Thus, in speculative transactions, there can be both positive and negative differences arising from the settlement of contracts. Each transaction resulting in a positive or negative difference is an independent transaction. In such transactions, though contract notes are issued for the full value of the purchased or sold asset, the entries in the books of account only contain the differences.

|

Accordingly, the aggregate of both positive and negative differences is to be considered as the turnover.

|

For example, Mr. X does the following intra-day trading of shares during the year:

|

Computation of turnover from intra-day trading of shares (speculative transactions).

|

In speculative transactions, the aggregate of both positive and negative differences (income and loss) is considered as the turnover. Thus, the turnover of Mr X shall be computed as follows:

|

Securities Amount of gain or (loss)

|

Set-off and Carry Forward of Losses

According to Taxmann Research, the losses from intra-day trading cannot be set off against income taxable under any other head, i.e., salaries, house property, capital gains and other sources.

|

The losses from speculative business (i.e., loss from intra-day trading) can be set-off only against speculative profits (i.e., profit from intra-day trading). These losses cannot be set off against normal business profits, though both of them fall under the same heads of income: 'profits and gains of business or profession'. However, losses from a normal business can be adjusted against the profits of a speculative business.

|

The unabsorbed loss can be carried forward for up to four Assessment Years. It can be set off only against the speculative business income in the subsequent years. It is important to note that you can carry forward the business loss, provided the ITR is filed on or before the due date.

|

If such ITR is not filed within the prescribed due date, the right to carry forward and set-off is lost.

|

Source: The Economic Times

|

|

|

|

|

|

|

|

When the Goods and Services Tax (GST) was implemented on July 1, 2017, one of its central promises was to eliminate tax cascading and allow seamless flow of input tax credit (ITC) across the value chain.

|

Nearly a decade later, GST has largely succeeded in replacing multiple indirect taxes with a unified system. But one part of the reform continues to generate friction for businesses: input tax credit.

|

Today, ITC has become one of the biggest sources of litigation, working-capital blockage and compliance anxiety under GST. What was designed as a pass-through mechanism has evolved into a compliance-driven process where access to credit depends not only on a company’s own actions, but also on supplier behaviour, invoice matching and portal-based validations.

|

From seamless credit to conditional credit

Experts say GST succeeded in reducing embedded taxation but the architecture of claiming credit has changed significantly.

|

Swaroop Repaka, head of product at ClearTax, told Business Standard that the original design worked on a different principle. “The original promise of input tax credit (ITC) was simple and powerful: kill the cascading of tax and let credit flow seamlessly across the chain. On the first count, GST has genuinely delivered; the embedded-tax problem of the old VAT + service tax + excise era is largely gone.”

|

However, he said, the ITC mechanism has quietly changed character. "We've moved from a self-assessed, trust-based model to a verification-based, supplier-dependent one," he said.

|

Over time, requirements such as invoice matching, GSTR-2B reconciliation, restrictions under Rule 36(4), Section 16(2)(aa), and now the Invoice Management System (IMS) have made credit eligibility more tightly linked to compliance data.

|

Nitin Vijaivergia, partner at Price Waterhouse & Co LLP, told Business Standard, “GST was envisioned as a seamless credit-based tax, eliminating cascading and taxing only value addition. While it has largely delivered on these objectives, the architecture of input tax credit has evolved from a seamless tax mechanism into a conditional entitlement.”

|

“Today, input tax credit is available not merely because tax has been paid, but only when every link in the compliance chain performs flawlessly," he said.

|

Why input tax credit has become a business risk

For businesses, delayed or denied credit directly affects cash flows. Under the current system, companies may have purchased goods, paid suppliers and fulfilled their obligations, but still face delays if supplier filings do not reflect correctly.

|

Maulik Manakiwala, partner - indirect tax, tax & regulatory advisory at BDO India, said: “One of the key challenges is the dependence on GSTR-2B for availing ITC. In cases where suppliers fail to furnish their GSTR-1 within the prescribed time, the corresponding ITC does not reflect in the recipient's GSTR-2B.”

|

This creates “blockage of working capital and delays in credit utilisation”, he told Business Standard.

|

Experts say the debate has gradually shifted from availability of credit to certainty of credit -- a distinction that increasingly influences business decisions and investment planning. Ashish Kumar, head of compliance at supply chain finance platform Vayana, told Business Standard, “Bigger companies have folded this straight into their vendor scorecards. And it's pretty common now for buyers to hold back the GST portion of a payment until the credit actually shows up in their GSTR-2B -- basically tying payment to compliance.”

|

Working-capital pressure and rising disputes

Businesses say supplier defaults are now among the biggest reasons for credit loss or delay.

|

Manakiwala said, “Companies today often lose, delay, or reverse input tax credit (ITC) mainly due to supplier not filing GST returns or paying tax; invoice mismatch or non-reflection in GSTR 2B; missing time limits or delayed claims; and inverted duty structure (higher tax on inputs than outputs).”

|

Sectors with long supply chains or refund dependence are particularly exposed.

|

Vijaivergia said that supplier-side compliance defaults frequently disrupt the flow of input tax credit. He further said inverted duty structures continue creating working-capital stress in sectors such as FMCG, textiles, footwear, fertilisers and renewable energy.

|

Ranjeet Mahtani, partner at tax and regulatory advisory firm Dhruva Advisors, told Business Standard that construction remains particularly vulnerable because project revenues arrive over longer cycles while input costs arise upfront.

|

What businesses want from GST’s next phase

Tax experts argue that the next stage of GST reform may not be about introducing new rules but reducing procedural friction.

|

Businesses want greater certainty that genuine credit will not be denied because of supplier defaults outside their control. Simpler reconciliation processes, clearer buyer protections, faster refunds and easier correction mechanisms remain among the key demands.

|

Repaka said the system has been optimised for revenue protection and the next phase should focus on restoring ease of doing business.

|

Source: Business Standard

|

|

|

|

|

|

|

|

In a dramatic twist, the Central Bureau of Investigation (CBI) on Tuesday arrested senior IAS officer Pardeep Kumar on the very day he retired, tightening its grip on the massive Rs 593-crore Haryana government funds scam.

|

Kumar, the former Member Secretary of the Haryana State Pollution Control Board (HSPCB), is the third IAS officer to be arrested in the case, according to a report of the Times of India. Investigators claim they have uncovered a direct link between him and the alleged siphoning of Rs 169 crore from HSPCB accounts maintained at IDFC First Bank's Sector 32 branch in Chandigarh.

|

The Rs 169-crore loss is being described by the CBI as the biggest financial hit suffered by any department caught in the wider scam.

|

According to the agency, Kumar had been evading investigators for nearly a week and had also sought anticipatory bail from a CBI court. Officials alleged that despite multiple notices, he failed to join the probe. He was eventually tracked down and taken into custody after CBI teams located him.

|

The agency has already arrested two other IAS officers — Ram Kumar Singh and Pankaj Agarwal — in connection with the case.

|

How the Alleged Fraud Worked

The HSPCB case is part of a much larger alleged banking fraud spanning eight Haryana government departments.

|

Investigators claim public money was diverted through fake or non-existent fixed deposits and suspicious banking transactions before being routed through shell companies.

|

The CBI alleges Kumar personally oversaw the investment process and facilitated the transfer of pollution board funds to the Chandigarh branch of the bank, allegedly exceeding prescribed limits for fixed deposits.

|

The probe found that government funds were first moved into a bank account that allegedly lacked documented departmental approval. Officials said the pollution board could not produce records explaining how the account was opened.

|

What investigators found next raised even more questions.

|

According to the CBI, the promised fixed deposits were never created. Instead, funds were allegedly drained through fraudulent debit transactions, resulting in a net loss of Rs 169 crore to the state exchequer.

|

22 arrested so far

With Kumar's arrest, the total number of arrests in the wider scam has risen to 22.

|

The CBI has already filed charge sheets against 17 accused, including six officials from IDFC First Bank and AU Small Finance Bank, three Haryana government officials, two companies, and six private individuals.

|

The agency is also probing related cases involving Chandigarh Smart City Limited (CSCL) and CREST, where charge sheets have already been filed.

|

In another major development, the CBI arrested two former bank officials linked to the Rs 593-crore fraud.

|

A special CBI court in Panchkula remanded Charanjeet Singh Randhawa, former branch head of AU Small Finance Bank, and Mohammad Shamim Dhar, former team head of IDFC First Bank's Government Business Group, to three days of CBI custody.

|

Investigators are continuing to trace the money trail and identify all those involved in what is emerging as one of Haryana's biggest alleged government fund scams.

|

Source: The Economic Times

|

|

|

|

|

|

|

|

CBIC -

To commemorate nine years of the Goods and Services Tax (GST), the Central Board of Indirect Taxes and Customs (CBIC) organized a special celebration at CSOI, New Delhi, on 1 July 2026. The event was held under the theme, ‘सुगम कर व्यवस्था, सशक्त भारत’, highlighting GST's

|

GST Indore -

The 9th #GSTDay was celebrated with great enthusiasm at CGST & Central Excise Commissionerate, Indore under the theme "सुगम कर व्यवस्था, सशक्त भारत".

|

GST Samvad an interaction among officers, taxpayers, trade & industry representatives, and tax professionals was organised on 30.06.2026 to commemorate nine years of GST as a transformative reform. The programme highlighted taxpayer facilitation initiatives, digital services, policy updates, and the importance of timely and voluntary compliance.

|

9 Years of GST! The CGST Indore Commissionerate celebrated the 9th anniversary of the Goods and Services Tax. The event marked nearly a decade of economic transformation and a unified national market.

|

Recognizing Excellence: The Department felicitated leading revenue contributors-Bharat Petroleum( @BPCLimited), HDFC Limited(@HDFCLTD), and MRF Limited(@MRF_Corporate)-for their exemplary tax compliance.10 dedicated departmental officers and a meritorious student were also honored

|

Taxpayer First: CGST Indore Commissioner Shri Peeyoush Bhati highlighted GST’s role in nation-building and announced that the Commissionerate will now regularly host monthly meetings with taxpayers to address grievances and ensure a transparent, efficient regime.

|

GST Aurangabad Commissionerate -

CGST AURANGABAD building lit up to kick in early 9th GST day celebrations

|

CGST Mumbai West -

As part of the #GSTPakhwada on occasion of upcoming 9th GST Day, on this year’s theme "सुगम कर व्यवस्था, सशक्त भारत” (Easy Tax System, Empowered India), CGST Mumbai West Commissionerate organised an Essay Writing Competition for officers and staff.

|

The winners and participants were felicitated by the Hon’ble Commissioner, CGST&C.Ex. Mumbai West appreciating their enthusiasm and insightful contributions.

|

WIRC of The Institute of Cost Accountants of India

Celebrating one of India’s landmark tax reforms that strengthened transparency, unity and the vision of One Nation, One Tax, One Market.

|

DGTPS MUMBAI CBIC

9वें GST दिवस के उपलक्ष्य में DGTS MZU & AZU द्वारा "Nine Years of GST: Perspective from Taxpayers" विषय पर Kendriya Vidyalayas के विद्यार्थियों हेतु एक वेबिनार आयोजित किया गया।

|

इस सत्र के माध्यम से GST के प्रति जागरूकता, वित्तीय साक्षरता को बढ़ावा दिया गया तथा विद्यार्थियों को राष्ट्र निर्माण में कराधान की भूमिका से अवगत कराया गया।

|

CGST Thane -

CGST Thane organized a 'Hindi & Marathi Essay Competition' for officers & staff

|

The Commissioner honored winners with certificates for outstanding performance

|

Celebrating language, awareness & commitment to GST

|

CGST MUMBAI EAST

As part of the 9th GST Day celebrations, CGST & Central Excise, Mumbai East Commissionerate organised Essay Writing and Drawing Competitions for students of Sandesh Vidyalaya & Junior College, Vikhroli (East), on 30.06.2026, with enthusiastic participation from young students.

|

The essay competition focused on GST and citizens’ responsibility towards tax compliance, while the drawing competition encouraged students to express ideas creatively. Prizes were awarded to winners, promoting taxation awareness and responsible citizenship among young minds.

|

As part of the 9th Anniversary celebrations of GST, CGST & Central Excise, Mumbai East Commissionerate organised GST "SAMVAD" and interactive session with members of trade and tax professionals on 29 June 2026 at Vikhroli to mark the occasion with active participation.

|

The session witnessed enthusiastic participation. Queries on filing of appeals, GST returns and other GST-related issues were addressed by officers, making it a valuable platform for knowledge sharing, constructive dialogue and promoting voluntary tax compliance across sectors.

|

CGST & Customs Thiruvananthapuram Zone

On the occasion of International Day Against Drug Abuse & Illicit Trafficking, the officers and staff of CGST & Customs Thiruvananthapuram Zone took a solemn pledge under the #NashaMuktBharatAbhiyan to build a society free from the menace of drugs.

|

DGTS AHMEDABAD CBIC

30.06.2026 को,DGTS AZU और MZU ने JG University के साथ मिलकर GST Awareness & Overview पर एक हाइब्रिड सेमिनार आयोजित किया।DGTS के Pr. ADG,श्री सुमित कुमार ने उद्घाटन भाषण दिया। CBIC के रिटायर्ड सुपरिटेंडेंट श्री जॉन क्रिश्चियन मुख्य वक्ता थे। #DGTS #GST #GSTDAY2026 #CBIC

|

Article Writing Competition 2026

To commemorate 9th Year of GST, Online Tax Update (OTU) launched 'Article Writing Competition 2026'. Registration starts today 1st July 2026 and ends on 15th July 2026. Article submission till 31st July 2026 and Winner Announcement in August, 2026. Cash Award + Certificate of Participation. Participation fees Rs. 300/- Read more

|

|

|

|

|

|

|

|

Centre has extended the last date for filing appeals before the Goods and Services Tax Appellate Tribunal (GSTAT) to July 31, 2026, giving taxpayers an additional month to submit their cases after a surge in filings led to technical difficulties on the GSTAT portal.

|

The extension applies to appeals filed under Section 112(1) read with Section 112(3) of the Goods and Services Tax (GST) law.

|

The revised deadline replaces the earlier cut-off of June 30, 2026, which had been notified by the government on September 17, 2025.

|

The decision follows recent representations from various stakeholders who flagged technical issues arising from a rush of appeals being filed on the GSTAT portal ahead of the deadline.

|

While noting that the original due date had been notified well in advance in September 2025, the government said filing activity had intensified sharply in recent weeks. It said 30,000 appeals were filed in the last 15 days alone, with daily filings touching a peak of 5,500 appeals.

|

Advising against eleventh-hour filings, the government urged taxpayers to complete their appeal submissions well in advance to ease pressure on the GSTAT portal.

|

The GST Appellate Tribunal serves as the first judicial appellate forum for taxpayers seeking to challenge orders issued by GST authorities after the disposal of their first appeals.

|

Source: The Economic Times

|

|

|

|

|

|

|

|

The disclosure of Clause 44 is mandatory in Tax Audit Report for the assessment year 2022-23 and onward. Every tax payer to whom the tax audit is applicable has to also furnish clause 44.

|

The taxpayer may or may not be registered under Goods and Services Tax Act but the disclosure is mandatorily required to be furnished.

|

|

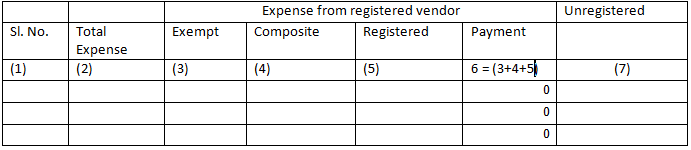

The format of clause 44 is given below:

|

|

|

The above format requires the bifurcation of ‘total amount of expenditure incurred by the taxpayer during the financial year’ into two heading – one is - the expenditure incurred for purchase or availing services from entities registered under GST and second the ‘expenditure incurred for purchase or availing services from entities not registered under GST’.

|

The expenses debited to Profit & Loss a/c will form the basis of this clause 44. That is the total expenses as appearing in Profit & Loss a/c will be shown in column (2) of the table above.

|

The expenditure incurred from registered entities will be further bifurcated into three headings viz. purchase of exempted goods or services (column (3)), purchase from a composition dealer (column (4)) and purchase of taxable goods or services (column (5)).

|

There is no break-up required for an expense incurred toward purchase or availing services from an unregistered dealer (column (7)).

|

The expenses such as ‘Salaries and PF, ESIC etc. will not form part of the report/ clause 44 as they are not an expense incurred from any vendor. However, the staff welfare expenses like canteen service, uniform purchase, tea, coffee etc. is an expense born from either a registered vendor or an unregistered vendor and therefore need to be considered for reporting.

|

Finance cost like interest on bank loan also will not be reported. Likewise depreciation, bad debts, provisions for expenses, power and fuel, petrol, diesel etc. will not form part of clause 44 disclosures.

|

Rest of the expenses like raw material, packing material, consumables, engineering items, professional fees, legal expenses, rent, rates and taxes, insurance etc. which are forming part of Profit and Loss a/c will be considered for this clause.

|

The total of all expenses reported in Financials will be considered in column (2) as stated above either expense head wise or as s single amount. This is because the clause does not clarifies as to whether the reporting is required expense wise or a single expense amount will suffice for reporting. So, one may furnish a single amount and keep the head wise expenses working as a supporting of the clause for audit and reference.

|

As shown in table below, the expense heading is for reference and amount in column (2) will only form the basis of the reporting including their further bifurcation into taxable, exempt, composition, registered and unregistered at respective columns. The amount at column (6) is the sum of column (3), (4) and (5) and the total of column (6) and column (7) will be equal to expense at column (2).

|

|

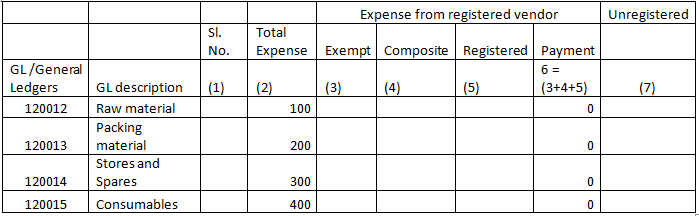

The working file will look like –

|

|

|

How to bifurcate the expenses into ‘purchases from registered vendor’ and their further bifurcation into taxable, exempt and composite vendor purchase and ‘purchase from unregistered vendor’.

|

The purchase report based on which return in Form GSTR-3B is prepared to be considered first. The report must have expense GL. Expense GL means the GL into which the cost has been debited while accounting the invoice. If said GL is not captured then it is suggested to add in the report with the help of IT/SAP / report developer etc. If the taxpayer is using SAP system then tax codes should also be captured to identify the product as exempt, taxable etc. or based on the taxes viz. IGST, CGST, SGST and GSTIN of the vendor the expenses can be segregated as taxable, exempt etc.

|

In the working, add a new column as ‘Remark’. Apply filter on ‘GSTIN’ in purchase report. Select blank and classify it as ‘unregistered’. Apply filter on transactions having GSTIN, select tax codes of exempt or in tax column as zero and check the item description as exempt to classify it as ‘registered-exempt’. And the transaction having GSTIN and GST amount then classify it as ‘registered-taxable’.

|

If the GSTIN is available and goods purchased /expense incurred is taxable and still GST is not charged by the vendor, then it means the vendor is a composite dealer. Classify such transaction as ‘registered-composite’. Alternatively, the GSTIN of the vendor can be searched at www.gst.gov.in to fetch the status of the vendor's GSTIN as ‘regular’ or ‘composition’ dealer.

|

Now, based on the fields viz. Remarks, General Ledgers (GL) and expense amount make a pivot table. Select GL at the ‘Row labels’ and remarks at ‘Column Labels’ and amount in ‘Values’ column.

The pivot table will look like –

|

|

In order to plot the expense in the base file, apply Vlookup like:

|

|

|

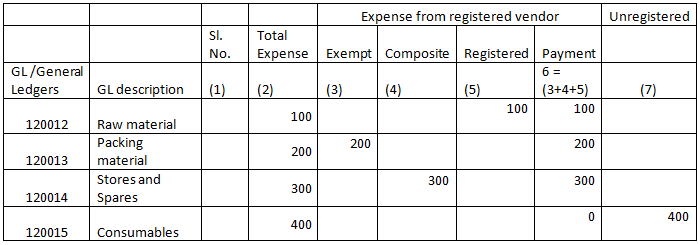

The expense will get plotted in respective columns after applying pivot as registered-exempt at column (3), registered-composite at column (4), registered-taxable at column (5) and unregistered vendor purchase at column (7).

|

There could be some entries in purchase report of which expense GL is not appearing. Instead clearing account is appearing. This is because in SAP system while GRN the inventory GL is debited. The expense GL is hit after the MIRO/Finance posting is done. Upon completion of MIRO the expense gets debited to expense GL / consumption GL.

|

As stated above, when a raw material is purchased it is accounted as an inventory. Thereafter when a production team makes a requisition to stores department to issue the inventory for consumption in their plant area , the material gets accounted into consumption GL.

|

The said consumption GL forms part of Profit & Loss account. Hence, in the purchase report wherever inventory or clearing GL appears identify their consumption GL and plot it in an addition column in the report.

|

With the basis of the purchase report most of the expenses GL as appearing in column (2) of table above would have been classified into respective expense head/column. And, for the expenses not captured in the purchase report for any reason then the respective expense's GL dump/report to be downloaded in excel.

|

Say for e.g. insurance GL. Take a dump/download from accounting system having, inter-alia’, ‘offsetting GL’ column, GL name etc.. In the offsetting GL column the vendor code is reflected (not for all transaction) and wherever the GRIR Clearing GLs appears the vendor code can be pulled from clearing GL dump having document number. Apply vlookup on document number and vendor code.

|

Once the vendor code is fetched then apply vlookup basis GSTIN with the vendor master. Same logic as discussed above need to be applied in the report i.e. add a column as ‘Remarks’ and classify expense as registered-taxable, registered-exempt, registered taxable and unregistered vendor.

|

In these GL, there will be an entry like – provisions accrued for an expense, pre-paid expense, rectification etc. Their classification into ‘registered’ or ‘unregistered’ purchase would be difficult. But, the logic one may apply is that, if the proportion of expense is more against registered-taxable then classify the aforesaid expense as ‘registered-taxable.

|

In the GL report tax codes also appear. It helps in classifying entry as taxable or exempt.

|

The expense can be further bifurcated and furnished as exempt in column (3), composition dealer purchase in column (4), registered purchase (5) and unregistered vendor purchase in column (7).

|

At the end, apply summation formula at the bottom of each of the column (3), (4), (5) and (7) individually. Apply percentage formula as exempt to total expense, composition to total expense, taxable to total expense and unregistered to total expense. The percentage so arrived will give a glimpse/idea as regard the pattern of purchase i.e. what % of purchases / expenses are from a registered vendor, taxable, exempt and purchase from unregistered vendor.

|

In case, the percentage does not depict fair scenario of type of purchase then revisit purchase report and expense GL and recheck the text field for nature of purchase and ensure correct classification is assigned to each line item.

|

By the above stated process, a clause 44 gets prepared to the best possible manner.

|

|

|

|

|

|

|

|

CA Nitin Bhuta, Mumbai has compiled and presented Clause 44 applicability in Tax audit report for A.Y. 2022-23 in the slider format/PDF in the link given below.

|

|

|

|

|

|

4 Lawgics by Ms.Nidhi Aggarwal

|

|

Ms. Nidhi Aggarwal is delighted to present GST Notes/Law in a simplified manner under the title “ Lawgics ”. The note is prepared in a series of PDFs encompassing GST Law and the interpretations thereof in simple manner. The author with a great vision to spread complex GST law in a simple manner amongst the taxpayers, tax professionals, students and knowledge seeker is presenting the Lawgics in piecemeal at regular interval.

|

|

|

|

|

|

|

5. GST Notes by CMA Anil Sharma

1) Shri CMA Anil Sharma, Shri CMA Gurdev Singh Saini and Smt. CMA Bhawna Sharma posted Chapter-15 containing CGST Act in simple language in PPT format. This is to make dealers, professionals, academicians, students etc. understand the basics of GST laws. Each Chapter in CGST Act, 2017 is explained in the form of Slides as given below for easy understanding of the Act:

|

Chapter-15 slides given below:-

|

|

|

|

|

|

|

|

|

|

|

You wish to publish your Article?

|

If you wish to share your article with maximum readers then please send the article at taxupdate.otu@gmail.com. We shall publish it with all due credit to you.

|

|

|

|

|

|

|

If you wish to subscribe to weekly Newsletter at Rs. 149/- for one year.

|

|

|

|

|

|

|

Hope the above updates is of use to you. Please share your input and feedback at taxupdate.otu@gmail.com

|

|

|

|

|

|

|

Visit our website

|

OTU provides you

|

- Articles on various topics

|

|

- Media - GST, Income Tax & Press R.

|

|

- Notes / Newsletter at 149/ p.a.

|

|

|

|

|