Definition of Input Service Distributor (ISD) as per Section 2(61) of the GST Act, 2017:

“Input Service Distributor” means an office of the supplier of goods or services or both which receives tax invoices towards the receipt of input services, including invoices in respect of services liable to tax under sub-section (3) or sub-section (4) of section 9 of this Actor under sub-section (3) or sub-section (4) of section 5 of the Integrated Goods and Services Tax Act, 2017, for or on behalf of distinct persons referred to in section 25, and liable to distribute the input tax credit in respect of such invoices in the manner provided in section 20.

An Overview to the meaning of ISD:

An ISD is a special category of taxpayer under GST that allows businesses to distribute the credit of input services to different branches or units. The ISD registration is typically used by businesses with multiple branches or offices, where the services are centrally received (like corporate office services), but the credit needs to be distributed among the various branches.

Purpose of the ISD:

- To facilitate the distribution of input tax credit (ITC) on input services to different units, branches, or divisions that cannot directly avail of the ITC.

- This ensures that the tax credit on services like legal, financial, or management services used across multiple branches is shared appropriately without loss of tax credit.

Key Amendments in Finance Act 2024:

Mandatory ISD Registration:

- Businesses operating in multiple states must register as an ISD if they receive input services centrally and wish to distribute the associated ITC to their distinct persons (branches or units).

- This mandates the use of the ISD mechanism for distributing ITC, eliminating the option to use the cross-charge method.

Inclusion of Reverse Charge Mechanism (RCM) Invoices:

- The definition of ISD now includes the distribution of ITC on services subject to RCM. This means that any input services received under RCM must be processed through the ISD mechanism for credit distribution.

Amendments to Section 20 of the CGST Act:

- Section 20 has been updated to outline the procedures for ISDs to distribute ITC. These amendments provide clarity on the manner and conditions under which credits can be allocated to various branches or units.

Effective Date:

- The amendments related to ISD provisions are scheduled to come into force on 1 April 2025 as per “Notification 16/2024 dated 6th of August 2024”. This gives businesses time to comply with the new requirements

Background:

Prior to the Finance Act 2024 amendment, businesses could use the cross-charge method, wherein the Head Office (HO) raised a tax invoice to the branch for input services; however, the Finance Act 2024 has removed the cross-charge mechanism, mandating the use of the Input Service Distributor (ISD) method for distributing input tax credits.

Solution to the Key Pain Points faced by Businesses:

1. Availing the GST Registration:

Businesses are supposed to take mandatory ISD Registration as per Section 24 of the GST Act, 2017 before 31st March 2025.

2. Re-assess the ITC Distribution mechanism:

Businesses with operations across multiple states should reassess their current ITC distribution methods. With the mandatory adoption of the ISD mechanism, transitioning from cross-charge methods may be necessary.

3. Determination of Common Credits used by all the branches:

-

- The ITC on input services alone must be distributed by determining which branch uses which input service, and the corresponding ITC should be appropriately allocated to the respective branch.

- The common credits are entity-specific as they may vary as per the Operations of the Entity.

- The most Common examples for common credits include:

- Audit Fee

- Consulting Fee

- Marketing Expenses

- Legal Charges

- Subscription Charges Paid

- Website Charges

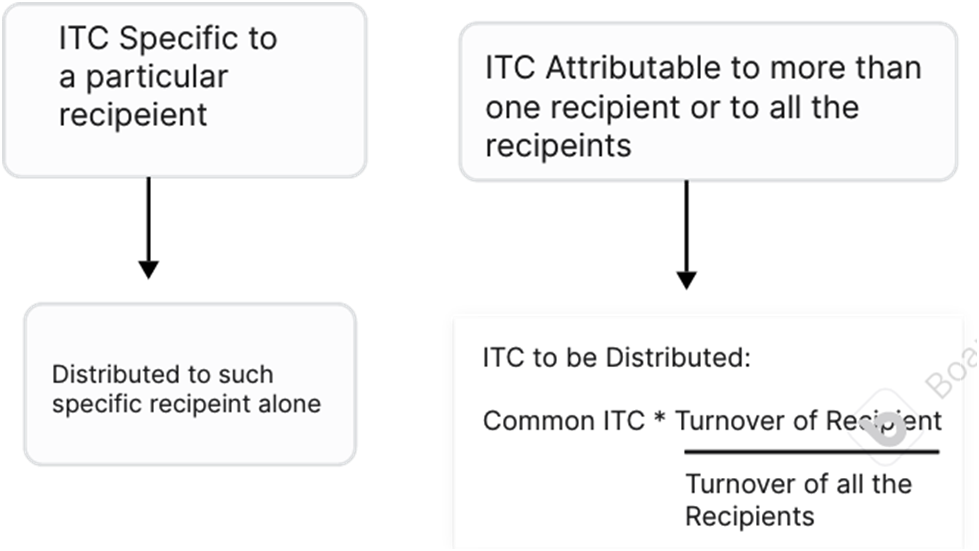

4. Basis to be used of Apportionment of ITC

The businesses should also take the Previous Year sales (if not available, then previous quarter’s sales) as the for making this apportionment.

The following method is prescribed for apportionment of the ITC:

5. Manner of Distribution of Credit:

The manner of Distribution would be dependent on the Type of GST to be distributed.

For ease of Understanding, the same is tabulated below:

| Credit of IGST | Recipient and ISD in same or Separate Place | ITC as IGST |

| Credit of UTGST or SGST or CGST | Recipient and ISD are in same state | ITC in UTGST/ SGST and CGST |

| Credit of UTGST or SGST or CGST | Recipient and ISD are in separate state | ITC as IGST |

6. How should Invoice be raised once ISD Registration is taken?

-

- The Head Office (HO) or the Entity has to inform all the vendors from whom service is availed with respect to the common ITC (Including RCM Supplies as mentioned in Section 9 of the GST Act, 2017) to raise invoice in the name of ISD and the mention the GSTIN of the ISD.

- Once the invoice is raised in the name of the ISD, the same auto populates in the GSTR-2B of the ISD and the same shall be apportioned to the respective recipients.

- The HO should also intimate all the vendors to raise invoice from 1st of April 2025.

7. Returns to be filed by ISD:

An ISD is required to file GST returns under form GSTR-6 before 13th of every month. This form is specifically for input service distributors, where they can report the input services received, the ITC received, and the distribution made to the branches.

8. Key Points to be noted to avoid litigations in future:

-

- The ITC Distribution should also encompass the ITC to be distributed to those branches which are dealing with completely exempt supplies too.

- Even Blocked Credit as per Section 17 of the GST Act, 2017 has to be distributed by the ISD and the recipient is not supposed to claim ITC on the same.

- ISD is supposed to raise invoice and Credit / Debit for reduction or increase in the ITC respectively.

- The Invoice for Credit Distribution shall contain all the attributes as mentioned in a normal invoice like Date, Name, Address, GSTIN, Invoice Number etc.

9. Excess Distribution of ITC:

If the GST Authorities suspect an excess distribution of ITC, they may proceed against the recipient under the principles of demand and recovery as set out in Section 73 to 84 of the GST Act, 2017.

Excess Distribution can primarily arise when the credit note is not adjusted with the ITC distributed previously.

10. Penalty for Non-Compliance:

As per the Finance Act 2024 amendments, businesses that are required to obtain ISD (Input Service Distributor) registration but fail to do so may face a penalty.

- Denial of ITC: If businesses distribute ITC via cross-charge instead of ISD, the tax authorities may reject the ITC claim.

- Recovery & Interest: Excess or incorrect ITC allocation by ISD will be recovered along with interest.

- Penalties: A minimum penalty of Rs. 10,000 or the amount of irregular ITC distributed will be imposed. In addition to this General Penalty of Rs. 25,000 can also be levied.

This article is a part of Article Writing Competition 2025.

Share this content: