by Dr. (CMA) Anamika Shukla

The Goods and Services Tax (GST) in India has introduced the Composition Scheme as a simplified taxation option for small taxpayers. This scheme aims to reduce the compliance burden and make taxation easier for businesses with a lower turnover.

Concept of Composition Scheme

The GST Composition Scheme is an alternative method of levying tax designed to simplify compliance for small businesses. It allows eligible taxpayers to pay GST at a fixed percentage of their turnover, rather than the regular GST rates. This scheme is intended to reduce the complexities of GST compliance, such as filing detailed returns and maintaining extensive records.

Features Of Composition Scheme

-> Simplified Compliance:

- Taxpayers under this scheme are required to file quarterly returns instead of monthly returns, reducing the frequency of compliance.

- The process of calculating and paying taxes is simplified, as it’s based on a fixed percentage of turnover.

-> Lower Tax Rates:

- The composition scheme offers lower tax rates compared to the regular GST regime.

- Reduced Record Keeping:

- Taxpayers are relieved from maintaining detailed records of inward and outward supplies, which simplifies accounting.

Eligibility Criteria:

To be eligible for the GST Composition Scheme, taxpayers must meet certain criteria:

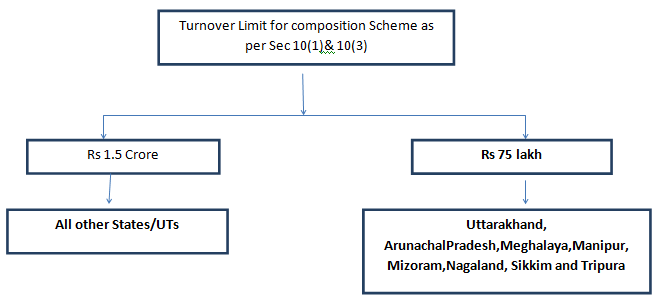

Turnover Limit:

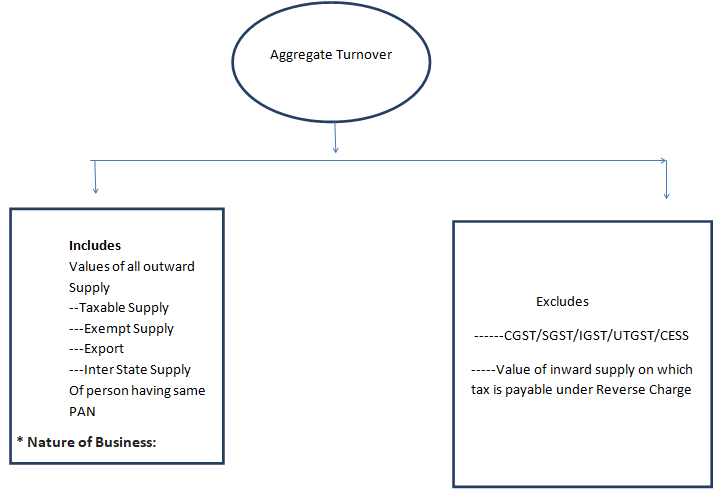

- The aggregate turnover in the preceding financial year must not exceed the prescribed limit.

Generally, this limit is Rs. 1.5 crore for normal category states [Sec 10(1)] and special category states (Uttarakhand, Arunachal Pradesh, Meghalaya, Manipur, Mizoram, Nagaland, Sikkim, and Tripura this limit is Rs 75 lakh.) [Sec 10(3)]

Person engaged in exclusively supply of services other than restaurant service whose aggregate turnover in the preceding financial year is up to 50 lakh are eligible for this scheme.[Sec 10(2A)].

- Certain businesses are not eligible for the composition scheme, such as:

- Manufacturers of certain notified goods, like ice cream, pan masala, and tobacco.

- Casual taxable person and Non-resident taxable persons.

- Businesses making inter-state supplies.

- Tax payers who supply goods through electronic commerce operators who are required to collect tax at source.

- Conditions:

- Taxpayers must not be involved in the supply of goods or services that are not taxable under GST.

- They cannot claim Input Tax Credit (ITC) on their purchases.

- They must display “composition taxable person” on their notice board at their principle place of business.

- They must also mention “composition taxable person” on every bill of supply issued by them.

GST Composition Scheme Rates:

| Composition Scheme | Category of Registered Person | Rate |

| For Goods | Manufacturer | 1% of Turnover |

| Restaurant Service | 5% of Turnover | |

| Others | 1% of Turnover | |

| For Services | 6% of Turnover |

| Category Of Person | How to exercise option | Effective Date of composition Levy |

| New Registration under GST | Intimation in the Registration Form GST REG-01 | From the effective date of Registration |

| Registered Person Opting For Composition Scheme | Intimation in Prescribed Form GST CMP-02 | Beginning of the Financial Year |

Benefits of the Composition Scheme

- Lower Tax Liability – Composition dealers pay GST at a reduced rate, which benefits small businesses with limited profit margins.

- Simplified Compliance – No need to maintain extensive records or file monthly returns, reducing paperwork and administrative costs.

- Reduced Filing Frequency – Composition dealers need to file quarterly returns instead of monthly returns.

- Ease of Doing Business – Small businesses can focus on operations rather than tax compliance

Limitations of the Composition Scheme

- No Input Tax Credit (ITC) – Composition dealers cannot claim ITC on purchases, increasing their effective tax burden.

- Restricted Interstate Trade – Businesses opting for this scheme cannot make interstatesales, limiting their market reach.

- Mandatory Payment from Own Pocket – Composition dealers cannot collect GST from customers, meaning the tax burden is included in the selling price.

- Limited Business Expansion – If the turnover exceeds the prescribed limit, the dealer must shift to the regular GST scheme and comply with standard tax requirements.

Comparison between: GST and Composition Scheme

| Features | Regular GST | Composition Scheme |

| Tax Rate | 5%, 12%, 18%, 28% | 1% / 5% / 6% |

| ITC Availability | Yes | No |

| Return Filing | Monthly | Quarterly |

| Interstate Sales | Allowed | Not Allowed |

| Tax Invoice Issuance | Yes | No (Bill of Supply) |

| Compliance Burden | High | Low |

Conclusion-

The Composition Scheme under GST is a beneficial provision for small businesses seeking to simplify tax compliance and reduce their financial burden. While it offers advantages like lower tax rates and fewer filings, businesses must carefully evaluate its restrictions, particularly the inability to claim ITC and the limitation on interstate sales.

For small traders, manufacturers, and eligible service providers, the Composition Scheme can be a viable option. However, as businesses grow, they may need to shift to the regular GST scheme for better flexibility and ITC benefits.

Before opting in, businesses should analyze their financials and seek professional guidance to ensure they make an informed decision.

This article is a part of Article Writing Competition 2025.

Share this content: