All India Central Excise Inspector Association Lucknow Circle, Lucknow wrote a letter to The Secretary, Department of Revenue, Ministry of Finance, New Delhi & The Chairman, Central Board of Indirect Taxes & Customs, New Delhi on 25.07.2023 as below –

Subject : Initiation of Pratidin System for Monitoring Work of All Posts within CBIC, and Objective assessment of Performance of every individual officer that may link to promotion later.

2. Request for Equitable Work Monitoring and Performance Assessment across all Posts within CBIC and not only of Superintendent and Inspectors but also of AC/DC/JC/ADC/Comm/Pr. Comm/CC/Pr. CC

Respected Sr/Mam,

We are writing to bring to your attention a matter of great significance concerning the equitable distribution of work and performance assessment within the CBIC.

We acknowledgement and appreciate the recent communication F. No. I(22)OTH/836/2023/486 dated 21.07.2023 issued by DGGST regarding the work of field officers on a real-time basis, known as “PRATIDIN,” (Copy enclosed). In light of this development, we wish to emphasize the urgent need for the comprehensive implementation of the Pratidin system across all posts within CBIC and its linkage to performance appraisal and promotions. Such a move is vital to ensure efficient monitoring of work and the objective measurement of performance.

Disproportionate Work Division: A Concerning Discrepancy

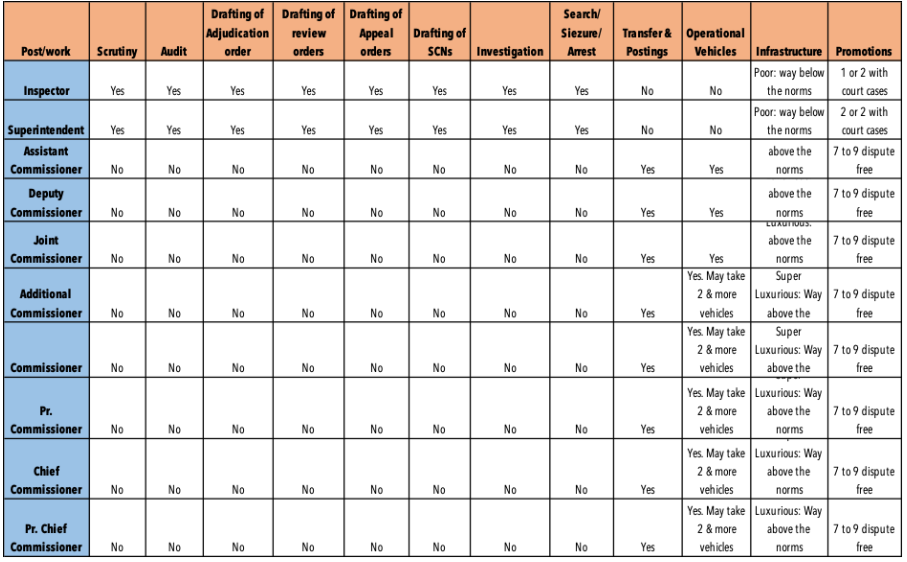

In recent times, our associations have sounded the alarm on the disproportionate division of work within CBIC. Group B officers have taken on the majority, consider it all, of the revenue-related tasks, while Group A officers predominantly hold all the higher posts without actively contributing expertise in crucial revenue matters such as scrutiny, investigation, audit, search, seizure, notices, adjudication, review, and refund. This state of affairs has created an environment where Group A officers secure numerous promotions without gaining the necessary experience and proficiency in revenue matters. It has also allowed these officers to form powerful groups that control and exploit public resources for personal luxury, while claiming credit for the exemplary work carried out by experienced and skilled Group B officers. The fact is the Indian ‘Revenue’ Service officers are not doing any original ‘Revenue’ related work.

Implementing Pratidin System for Transparency and Accountability

To rectify this glaring discrepancy, we have repeatedly requested a duty list for each cadre. We strongly believe that implementing the Pratidin system across all posts within CBIC will effectively define the responsibilities of each cadre, ensuring that work is carried out by officers according to their appropriate level of competence and designation. Presently, this system will clearly reveal that revenue matters are largely handled by Group B officers, while Assistant Commissioners (AC), Deputy Commissioners (DC), Joint Commissioners (JC), Additional Commissioners (ADC), Commissioners, Principal Commissioners (Pr. Comm), Chief Commissioners (CC), Principal Chief Commissioners (Pr. CC), Members, and Chairmen primarily monitor the Gr. B officers, with little or no direct involvement in revenue-related activities.

It is important to note that vital activities such as scrutiny, audit, and assessment, involving turnovers ranging from a mere 20,000 to without limit that means multi-crores, are the domain of Group B officers, while Group A officers often rely on their domination & control in administration for their work, rather than harnessing their expertise and participating actively in revenue matters. Thus, they never get the expertise, skills and knowledge to guide the subordinates, rather they totally depend on them for even their exclusive work This unjust division of work also places an undue burden on Group B officers, who are coerced into performing tasks beyond their jurisdiction, including the exclusive responsibilities of higher officers viz. adjudication, review, and refund processing. Not only does this negatively impact the morale of Group B officers, but it also presents opportunities for corrupt practices to flourish under the guise of their involvement.

Addressing Workload and Redundant Posts

Moreover, considering the proliferation of Principal Commissioners and above, it is pertinent to assess the necessity of the multiple posts that exist within CBIC. With one Commissioner overseeing the State Goods and Services Tax (SGST) for an entire state, it appears that the current number of Commissioners and above are too excessive to become a burden of taxpayers and results in excess monitoring. Implementing the Pratidin system will shed light on the actual workload of Commissioner level positions, assisting in evaluating the functional requirements and justifying the existence of multiple posts of such rank.

Promoting Transparency and Equitable Division of Work

Clarity must also be provided on the designation of “proper officers” for various sections of the law. For instance, if Assistant Commissioners (AC) or Deputy Commissioners (DC) are designated as proper officers for recovery under Section 79, adding the responsibility of recovering interest, orders-in-original, or funds from canceled registrations to the Range Officers’ Pratidin desk contradicts their prescribed roles. Similarly, physical verification under Section 25 should remain the mandate of AC/DC officers, and the revocation of canceled registrations should fall within their jurisdiction. Including such tasks under the purview of Range Officers on the Pratidin desk is inappropriate and undermines the integrity of work division within CBIC.

Additionally, the process of GST adjudication should involve all adjudicating authorities and not solely be restricted to Range Officers, especially since it is based on monetary thresholds. Implementing the Pratidin system across all CBIC posts will ensure proper and parallel division of work, eliminate non-functional and non-contributing positions, and promote transparency, accountability, and efficiency within the revenue department. This streamlined approach will result in optimal resource allocation, benefiting both officers and the general public.

Request for Immediate Attention and Intervention

We humbly request your immediate attention and intervention to rectify the disparities in work distribution within the revenue department of CBIC. The implementation of the Pratidin system, alongside its linkage to performance appraisal, is essential to establish transparency, define duties, encourage equal contribution, and enhance the overall effectiveness of CBIC. We eagerly await your response, which we hope will include concrete action plans to address this pressing issue.

Thank you for your valuable time and consideration. We remain committed to serving the nation’s interest and trust in your leadership in bringing about positive change within CBIC.

Encls. As above

Yours sincerely,

(Abhijat Srivastava)

Copy to: The Principal Chief Commissioner, CGST & C.Excise, Lucknow Zone with the request to initiate Pratidin across all the posts within CBIC.

2. The Pr. Commissioner / Commissioner / Pr. ADG / ADG of Commissionerates /Directorates of Lucknow zone with the request to initiate Pratidin across all the posts within CBIC.

3. The Secretary General, AICEIA with the request to raise this issue before every possible authority for o ensure efficient monitoring of work and the objective measurement of performance.

Share this content: