Source: The Economic Times dated 20.10.2025

Mr. Bandopadhaya (name withheld) had the worst day ever when the income tax department sent him a draft assessment order that added Rs 2.28 crore (2,28,14,293) to his account. Bandopadhaya is a non-resident Indian citizen who hadn’t filed any income tax return (ITR) for the year in question.

After gathering information and details, the tax officer noticed that the assessee (Bandopadhaya) had made numerous financial transactions. Consequently, a tax notice under Section 148 of was issued, and in response, Bandopadhaya, filed his ITR on June 1, 2022, reporting a total income at Rs 3.83 lakh (3,86,620).

On March 17, 2023, the tax officer issued a draft assessment order under Section 144C of the Income Tax Act, 1961, adding Rs 2.28 crore (2,28,14,293) as unexplained money under Section 69A read with Section 115BBE and proposed a total income assessment of Rs 2.32 crore (2,32,00,913).

Feeling aggrieved with this draft assessment, Bandopadhaya filed his objections the Dispute Resolution Panel (DRP) on April 13, 2023. The DRP called for a remand report which was placed on record by the ITO/Assessing Officer on November 30, 2023, followed by a second remand report on December 21, 2023.

The DRP after taking reviewing the remand reports, concluded that the nature and source of money in the bank deposits made by the assessee (Bandopadhaya) were not satisfactorily explained. As a resuly, they dismissed the application of the assessee (Bandopadhaya) with a directive dated December 29, 2023. Following this, the Assessing Officer issued an assessment order on January 19, 2024, whicj included an addition of Rs 2.28 crore (2,28,14,293) as unexplained money under Section 69A in conjunction with Section 115BBE.

Unhappy with the DRP order, of DRP, Bandopadhaya appealed to the Income Tax Appellate Tribunal (ITAT) Ahmedabad. The ITAT Ahmedabad partially allowed his appeal and deleted all but Rs 63,133 of the income classified as unexplained money.

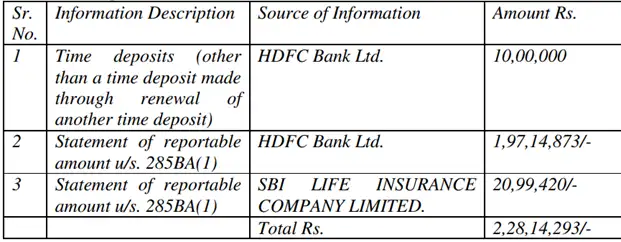

Here’s a table showing the nature and source of income which is the reason why Bandhopadhaya got the tax notice:

Source: ITAT Ahmedabad order

ITAT Ahmedabad says this

ITAT Ahmedabad in its judgement (ITA No. 458/Ahd/2024) said that they have heard both the parties and perused all the relevant materials available on record.

ITAT Ahmedabad said that it is pertinent to note that on page 13 to 23 of the directions dated December 29, 2023 passed by the DRP, the Assessing Officer himself has categorically mentioned that the assessee (Bandopadhaya) has filed copy of fixed deposit summary, copy of bank accounts statements with the HDFC and SBI, copy of investment in time deposit HDFC and copy of SBI life Insurance company and in fact the first remand report has also been reproduced and in the remark column related to the transactions where the assessee has explained the source of the funds.

The sources which have not been explained have been explained by the assessee (Bandopadhaya) which is reflected in the second remand report dated December 21, 2023 which is reproduced at page 35 to 40 of the DRP’s directions.

The assessee (Bandopadhaya) at that juncture has filed bank statements of various accounts and has also given the details of fixed deposits held by SBI and summarized explanation of credit and debit entries in his NRE/NRI held by SBI and HDFC bank.

ITAT Ahmedabad said: “From the remark column thereon it can be seen that only one entry of 63,133/- was not explained but the rest of the entries and the transactions were totally explained and verified by the Assessing Officer. It can be seen in para 4 of the said remand report at page 39 of the DRP’s direction.”

Judgement: “Once, the assessee (Bandopadhaya) has submitted all the credit entries along with debit entries and also that of the submission of employment verification letter, doubting the genuinely of the said documents without any basis is not justifiable on the part of the Assessing Officer as well as by the DRP. Thus, the Assessing Officer as well as CIT(A) except the entry of 63,133 should not have made addition u/s. 69A as unexplained money because the assessee (Bandopadhaya) has explained all the details of the rest of the entries. Thus, the appeal of the assessee is partly allowed except the component of Rs 63,133. In the result, the appeal of the assessee is partly allowed.”

Key learnings from this case

Gopal Bohra, partner, N. A. Shah Associates LLP, said to ET Wealth Online: The key learning from this ruling for every taxpayer whether resident or non-resident can be summarised as under:

1. Ensure that you file your tax return if taxable income exceeds maximum amount which is not chargeable to tax, or you satisfy any one of the followings where filing of income tax return is mandatory:

a) If you spent on foreign travel exceeding Rs. 2 lakhs

b) If electricity consumption exceeds Rs. 1 lakhs

c) Receipts from business exceeds Rs. 60 lakhs

d) Receipts from profession exceeds Rs. 10 lakhs

e) If total TDS/TCS exceeds Rs. 25,000/- (Rs. 50,000/- for senior citizen)

f) If bank deposit in one ore more current account exceeds Rs. 50 lakhs

g) If resident individuals, – holds any foreign assets or beneficial owners of any foreign asset or signing authority in any foreign bank account.

2. Tax department receives information in relation to certain transactions from third party (e.g. immovable property transaction of Rs. 30 lakhs or more, investment in mutual funds/bonds/debentures/deposits of Rs. 10 lakhs or more, payments in aggregate of Rs. 10 lakhs or more for one or more credit card, payment exceeding Rs. 2 lakhs in cash for goods or services, etc.), make sure that you have explanations and proper evidences about sources of such transactions.

3. Tax departments sends information about certain transactions through insight portal/SMS/emails if such transactions are not matched with tax return or if one failed to file tax return. When taxpayer receives such communication from the tax department, make sure to give appropriate response promptly.

4. You may periodically log in to the income tax department’s portal to check for any notices or orders issued, so that appropriate action can be taken promptly in case you are unaware of them.

Share this content: